by Amine Rahal | Sep 16, 2025 | Definitions

Disclosure: Our content is not financial advice. Do your own research and speak to a licensed tax professional or financial advisor before taking action. We may earn commissions from products reviewed. (Learn more)

Tax Relief Advocates (www.taxreliefadvocates.com) is a California based tax relief firm that focuses on resolving IRS and state tax problems. They work on issues like unpaid back taxes, penalties, liens, levies, and wage garnishments. The process usually starts with a free consultation, then an investigation phase, followed by a customized resolution plan. In my experience reviewing this space, Tax Relief Advocates is a credible option for taxpayers who need representation on IRS or state matters. If your main challenge is unsecured consumer debt like credit cards or personal loans, I suggest also comparing providers that specialize in debt settlement, especially New Era Debt Solutions.

Looking for the Best Debt Relief in 2025?

Tax Relief Advocates handles tax problems. If your core issue is credit cards or personal loans, I recommend reviewing New Era Debt Solutions. In my opinion, New Era stands out for no upfront fees, a transparent process, and a strong record of client outcomes.

Check if you qualify with New Era

Visit Website

|

Company Snapshot

- Official Name: Tax Relief Advocates

- Official Website: www.taxreliefadvocates.com

- Headquarters: California

- Founded: More than a decade in operation

- Service Area: Federal IRS cases in most states, state tax services vary

- Primary Service: Tax relief and IRS representation

Legitimacy, Ratings and Reviews

From what I can see, the company presents the credentials I expect in a tax relief provider. They describe teams that include experienced tax professionals and they publish a clear step by step process. Reviews I find are generally positive with the usual mix that comes with tax cases, since outcomes depend on documentation, income, and the agency involved.

- Professional staffing: Cases are typically handled by enrolled agents, CPAs, and tax attorneys

- General sentiment: Many clients call out help stopping levies and setting realistic payment plans, with some noting longer timelines on complex files

Services Offered by Tax Relief Advocates

- Tax Investigation and Case Review with transcript analysis and compliance checks

- Offer in Compromise when financials meet eligibility rules

- Installment Agreements that structure affordable monthly payments

- Currently Not Collectible Status for consumers who cannot pay now

- Penalty Abatement requests when criteria are met

- Wage Garnishment and Bank Levy Help that aims to stop or release enforced collection

- Lien Guidance including withdrawal requests when eligible

- Audit Representation and appeals support

What Makes Tax Relief Advocates Different from Other Debt Relief Companies

Most debt relief companies in our rankings focus on consumer debt settlement. Tax Relief Advocates focuses on tax representation, which is a different specialization. Here is what stands out to me.

- Agency facing work. They work directly with the IRS and state agencies, not credit card issuers or personal loan lenders.

- Compliance first. A big part of tax relief is filing missing returns and getting compliant before negotiation. That is different from settlement programs that center on creditor negotiations.

- Resolution tools. The toolkit includes offers in compromise, installment agreements, penalty relief, and currently not collectible status. These are tax specific tools, not consumer lending tools.

- Representation. Cases are led by tax professionals who can speak to the IRS on your behalf. Debt settlement firms generally do not offer legal tax representation.

- Fee structure. Tax relief is often priced in phases such as investigation and resolution. Debt settlement typically charges a performance based fee after a settlement is approved.

| Category |

Tax Relief Advocates |

New Era Debt Solutions |

Typical Debt Settlement Company |

| Primary Focus |

IRS and state tax relief |

Unsecured consumer debt settlement |

Unsecured consumer debt settlement |

| Best For |

Back taxes, penalties, liens, levies, garnishments |

Credit cards, personal loans, medical bills |

Credit cards, personal loans, medical bills |

| Representation |

Handled by tax professionals who can deal with the IRS |

Negotiators handle creditor talks and client support |

Negotiators handle creditor talks and client support |

| Resolution Tools |

Offer in Compromise, Installment Agreement, CNC, penalty relief |

Lump sum or structured settlements with creditors |

Lump sum or structured settlements with creditors |

| Fee Approach |

Often phase based by investigation and resolution |

No upfront fees, success based after settlements |

Usually success based after settlements |

| Impact on Credit |

Focuses on tax liabilities, not credit card reporting |

Short term credit impact while accounts are delinquent |

Short term credit impact while accounts are delinquent |

| Typical Timeline |

Varies by agency response and documentation |

Often 24 to 36 months depending on funding |

Often 24 to 48 months depending on funding |

Tax Issues They Can Help With

- Unpaid IRS or state back taxes

- IRS penalties and interest

- Tax liens, wage garnishments, and bank levies

- Audit notices and appeals

- Filing compliance and missing returns

Pros

- Tax specific focus with a toolkit built for IRS and state matters

- Free consultation and a defined investigation phase

- Ability to communicate with agencies on your behalf

Cons

- Fees vary by case complexity and are not one size fits all

- Timelines depend on agency response times and documentation

- State rules differ, so availability and strategies can change by location

Final Thoughts

Tax Relief Advocates is a solid choice if you need help with the IRS or with a state tax agency. The service menu covers the main resolution strategies and the team can represent you in communications. Fees and timelines vary with the complexity of your case. If your main goal is to reduce unsecured consumer debt rather than handle tax issues, I recommend starting with New Era Debt Solutions and comparing outcomes before you decide.

👉 See if you qualify with New Era

👉 Read Our New Era Review

Frequently Asked Questions About Tax Relief Advocates

Disclosure: Our content is not financial or tax advice. Please do your own research and speak with a licensed tax professional or financial advisor. We may earn commissions from products or services reviewed. (Learn more)

1) Is Tax Relief Advocates a legitimate company?

In my view they operate like a standard tax relief firm. They describe teams that include tax professionals and they publish a clear process from consultation to resolution.

2) What tax problems does the company handle?

They focus on unpaid back taxes, penalties and interest, liens, levies, wage garnishments, audit notices, and missing returns. They can work on both IRS and many state cases.

3) How does the process work from start to finish?

It usually begins with a free consultation, then an investigation phase where transcripts and documents are reviewed, followed by a tailored plan such as an installment agreement, an offer in compromise when eligible, or another resolution.

4) What documents should I gather before the consultation?

Recent IRS or state notices, prior year returns, pay stubs, bank statements, a list of assets and monthly expenses, and any correspondence about liens, levies, or garnishments.

5) Do they only work with the IRS or also with states?

They handle IRS cases in most states. Availability for state tax work varies by location and by the rules of that state.

6) What is an Offer in Compromise and do I qualify?

An Offer in Compromise is a request to settle for less than the full balance when the financials show an inability to pay in full. Qualification depends on income, expenses, assets, and IRS formulas. The investigation phase is where the firm checks this.

7) Can the company stop a wage garnishment or bank levy?

They can request relief and often work to pause or release enforcement when the facts support it. Timing depends on the levy or garnishment type and on how quickly financials are provided.

8) What is Currently Not Collectible status?

It is a temporary status the IRS may grant when you cannot pay without hardship. Interest can still accrue and the IRS may review your situation later.

9) How does penalty abatement work?

If you meet criteria like first time abatement or reasonable cause, the firm can request that penalties be reduced or removed. Interest on the underlying tax can continue until the balance is paid.

10) How are fees structured?

Tax relief is often priced in phases. There is typically an investigation phase to gather data and determine eligibility, then a separate fee for resolution work. Prices depend on case complexity.

11) Do I pay anything upfront?

Many tax relief providers bill an initial investigation fee, then a second phase for the chosen strategy. Ask for a written agreement that explains the scope, the fees, and the refund policy.

12) How long does a typical case take?

Timelines depend on the agency, the documents provided, and the strategy used. Some steps can move quickly once financials are complete, while complex cases can take longer.

13) Will working with a tax relief firm hurt my credit score?

Tax resolution affects your tax account rather than revolving credit lines. Credit impact is usually indirect, for example when a public lien is recorded. The goal is to resolve the liability and prevent or remove enforcement when possible.

14) Can they remove a tax lien?

They can request release once the balance is paid or request withdrawal in certain situations. Approval depends on IRS or state rules.

15) Do they file missing returns or only negotiate?

Most tax relief plans start with compliance. That usually means filing missing returns before the IRS or a state will finalize a resolution.

16) What if I do not qualify for an Offer in Compromise?

Other tools exist. An installment agreement, penalty abatement, or Currently Not Collectible may be more realistic if an offer is not available.

17) Will I owe taxes on forgiven tax debt?

Some resolutions simply restructure payment rather than forgive balances. When a balance is reduced, tax reporting can vary by program and year. I recommend asking your tax professional to review any tax reporting that could apply.

18) Can the firm represent me without me speaking to the IRS?

Yes in many cases. With a signed authorization the firm can communicate with the IRS or a state on your behalf and keep you updated.

19) Are results guaranteed?

No. Results depend on financials, documentation, and the rules in effect. A reputable firm will outline what is realistic before you sign.

20) Can I do this on my own instead of hiring a firm?

Yes. The IRS and most states allow self representation. Many readers choose a firm when they want help with forms, timelines, and communications, or when there is enforcement already in place.

21) What happens to my tax refunds while I am in a resolution?

The IRS can apply refunds to outstanding balances during many programs. If you expect a refund, ask how that will be handled under your plan.

22) Will I need to stay current on new taxes during the program?

Yes. Staying current on new filings and estimates is usually required. Falling behind again can jeopardize a resolution.

23) Can the firm help with state garnishments and bank levies too?

Yes in many cases. State rules vary, so timelines and documentation needs can be different from the IRS.

24) What if my income or expenses change during the case?

Tell your case team right away. A change can affect eligibility for an offer, the size of payment in an installment plan, or the status of a hardship request.

25) Will the firm handle communication with collectors and field agents?

Once authorization is in place they can speak with the assigned revenue officer or collections unit and coordinate requests for information and next steps.

26) Can I pause the case and restart later?

You can usually pause, but interest may continue and enforcement can resume. Ask about any fees if you stop and start.

27) What should I ask before I sign an agreement?

Ask about fees, milestones, who will work on your case, expected timelines, what happens if you do not qualify for an offer, and how communications will work.

28) How should I prepare to make the process faster?

Gather documents early, respond quickly to information requests, file any missing returns, and keep track of income and expenses with simple worksheets.

29) Do they help with business tax issues?

Some firms handle payroll tax and sales tax cases. Ask whether your business taxes are in scope and what documents are needed.

30) What happens after my case is resolved?

Plan for compliance going forward. File on time, make estimates if required, and keep an emergency fund so you do not slip back into a balance due.

by Amine Rahal | Sep 13, 2025 | Definitions, gold

Disclosure: The information on this page is for education only and is not financial, investment, or tax advice. CPIInflationCalculator.com may earn commissions from partner links. Precious metals carry risk, including loss of principal. Past performance does not guarantee future results. Please consult a licensed financial advisor and a tax professional before acting.

If inflation is eating away at your portfolio, one investment you may have looked at is precious metals. Physical metals are known to be a good hedge against inflation and paper markets, but which precious metal should you invest in: gold or silver? In this article, we’ll cover the pros and cons of both to help you decide on your precious metal allocation. First, let’s look at this comparison table:

| Factor |

🟡 Gold |

⚪ Silver |

| Market Value |

Higher price per ounce |

Much lower price per ounce |

| Volatility |

Lower volatility, more stable |

Higher volatility, more prone to price swings up or down |

| Liquidity |

Highly liquid, easier to buy and sell in large quantities |

Liquid but may have less demand in large quantities |

| Industrial Use |

Limited use compared to silver |

Significant industrial demand (electronics, EV, solar energy, tech, etc) |

| Supply and Demand |

More stable due to its primary use as a store of value |

Fluctuates based on industrial demand and economic cycles |

| Hedge Against Inflation |

Strong hedge, tends to rise during infla |

For me, the highlight of this table is how easy it is to store gold. An $80k gold bar can fit in your pocket, which makes it very convenient, cheap and easy to store. This factor greatly contributes to the fact that gold is an amazing store of value. However, this also makes it very difficult to “spend”. In a scenario where the dollar is worth nothing and you want to use your precious metals as currency for everyday expenses, silver might be a better choice.

Gold: The Classic Choice

Gold investing goes back thousands of years. Virtually every holy book mentions it. Now, why should you consider gold? For the following reasons:

- Stability: Almost every known civilization has valued gold for thousands of years, and even now, people often see it as a safe haven during economic uncertainty. Its price tends to be more stable over time.

- Inflation Hedge: History has shown that when the cost of living rises, gold prices often increase too. This makes it a good option for preserving your purchasing power during high-inflation times.

- Global Acceptance: Gold is recognized and valued worldwide. If you ever need to sell, it’s generally easy to find a buyer, especially if you have recognized bullion coins and bars like American gold Eagles or Canadian Maple Leafs.

- Less Volatility: Gold prices don’t fluctuate as wildly as some other investments, which can make it a calmer ride for investors.

Things to keep in mind:

- Higher Cost: Gold is more expensive per ounce than silver. This means you’ll need more money upfront to invest. Also, each gold investment company has different fees, with some charging very high premiums. We encourage you to shop around. Look for a company with competitive prices for their gold coins and bars.

- Slower Growth Potential: Because it’s more stable, you might see slower gains compared to more volatile investments.

Silver: The Dynamic Alternative

Silver is the most conductive metal on earth, which makes it needed in multiple industries, including Electric Vehicles, Electronics, Medicine and many more. Its various uses mean that its value goes beyond its investment potential. In a nutshell, you should consider investing in silver because:

- Affordability: Silver is much cheaper than gold. Why is that helpful? It allows you to start investing with a smaller amount of money.

- Industrial Demand: As we covered earlier, silver is used in many industries from electronics to EVs to solar panels. This can drive up demand and potentially its price.

- Growth Potential: Silver prices can rise quickly, offering the chance for significant gains if the market moves in your favor. If being the key word.

Things to keep in mind:

Making Your Decision

Before deciding on whether you should buy gold or silver as a hedge against inflation, consider your goals and comfort level:

- Are you looking for stability and a long-term store of value? Gold might be the better choice for you.

- Are you open to taking more risk for the chance of higher returns? Then silver could be more up your alley.

- Do you have a smaller budget to start investing? Silver allows you to enter the market without needing a large sum of money.

Now, how about both?

- Diversification: Investing in both gold and silver can help balance your portfolio. Really! Gold can provide stability. Silver offers growth potential.

- Hedging Bets: Holding both metals means you’re not putting all your eggs in one basket.

Final Thoughts

Ultimately, the choice between investing in gold vs silver depends on your individual financial situation, investment goals, and how much risk you’re comfortable taking on. It also depends on your understanding of the pros and cons of both metals. Do you believe the pros of one outweigh the pros of the other? There is no single right answer. Our final thoughts are:

- Do Your Research: Look into current market trends, historical price movements, and forecasts.

- Consult a Professional: It might be helpful to talk to a financial advisor who can offer personalized advice.

- Think Long-Term: Precious metals are generally considered long-term investments.

As always, we would like to remind you that investing always comes with risks, and there’s no guaranteed return. But with careful consideration and planning, you can make a choice that aligns with your financial goals. Always speak to your financial advisor before making any investment decision. Understand that past results don’t guarantee future returns. Invest wisely. Also, given the inflation we had to endure in the last few years, make sure you analyze your financial situation fully to determine whether you should be investing in a new asset class like precious metals. You should NEVER use debt or credit to buy physical metals or invest in anything else. If you’re in high debt, we recommend looking at different debt relief options to see how you can alleviate your debt, before thinking about investing.

Gold vs Silver: Frequently Asked Questions

1) Should I dollar cost average or wait for dips?

I prefer a simple plan. Dollar cost averaging removes the guesswork. If you enjoy timing, you can blend DCA with small buys on pullbacks.

2) Coins, bars, or rounds. What is best?

Coins from major mints are the most liquid and carry higher premiums. Bars are cheaper per ounce and efficient for larger amounts. Rounds are private mint products that can be cost effective but may resell for a bit less.

3) Why do premiums over spot vary so much?

Brand, format, and demand drive premiums. Small pieces cost more per ounce to make and ship. In stressed markets premiums can spike even if spot is flat.

4) How do I verify authenticity?

Buy from reputable dealers, keep assay cards and serial numbers intact, and use basic checks like weight and dimensions. Higher end tools include XRF and specific gravity tests. When in doubt, ask a dealer to test.

5) Home safe, bank box, or depository?

Home storage is convenient but needs a real safe and insurance. Bank boxes are discrete but not insured by the bank. Depositories add professional security and insurance for a fee. I like splitting storage for redundancy.

6) How easy is it to sell quickly?

Gold is the easiest. Most large dealers post live buy prices and fund fast. Silver is liquid but bulkier to ship and may have wider spreads. Keeping popular products helps.

7) What moves gold and silver prices day to day?

Real interest rates, the dollar, central bank flows, and risk sentiment matter for gold. Silver adds an industrial layer, so manufacturing trends and solar demand can swing it harder.

8) Are ETFs a good substitute for physical?

ETFs add convenience, tight spreads, and easy rebalancing. Physical removes some counterparty risk and tracks spot after premiums. Some investors hold both to balance convenience and sovereignty.

9) Can I put metals in an IRA?

Self directed IRAs can hold certain bullion that meets fineness rules. Numismatic coins usually do not qualify. Custodian, storage, and trading fees apply. I suggest confirming details with the custodian before you buy.

10) How are taxes handled when I sell?

Tax treatment depends on jurisdiction and product type. Keep purchase records and talk to a tax professional about reporting and capital gains. I avoid giving specific tax rates here since rules change.

11) What percentage of a portfolio makes sense?

That comes down to risk tolerance and goals. I often see ranges from a small single digit allocation to a mid single digit allocation. The right number depends on your total plan, not a rule of thumb.

12) Is “junk silver” still useful?

Pre 1965 US 90 percent silver coins can be a low premium way to get fractional silver. Liquidity is good with dealers and many stackers know the melt value.

13) Does silver tarnish matter?

Tarnish does not change metal content. For aesthetics, store in dry, cool conditions with anti-tarnish strips or capsules. Bars and rounds are fine to leave as is if you plan to hold long term.

14) Are kilo bars better than 1 oz coins?

For low premiums per ounce, kilo bars win. For flexibility and resale, 1 oz coins win. Many investors mix sizes so they can sell in smaller chunks when needed.

15) What if premiums blow out during a crisis?

It happens. Retail supply can get tight and premiums climb. Having some metal on hand before you need it helps. ETFs can fill short term gaps if you accept market risk and fund rules.

16) Do central banks buy silver too?

Central banks focus on gold as a reserve asset. Silver demand is driven more by industry and investors, which is one reason silver is more cyclical.

17) How often should I rebalance?

Pick a cadence you will follow. Quarterly or annual checkups are common. If metal weights drift far from your target, trim or add to get back in range.

18) Are there ethical or sourcing labels to look for?

Many large refiners follow responsible sourcing standards from industry bodies. If this is important to you, ask dealers which refiners and programs they support.

19) Can I travel with coins or bars?

You can, but know your local reporting rules and security risks. I keep travel minimal and use insured shipping or a depository transfer when possible.

20) Will gold or silver help if inflation cools?

They can still diversify a portfolio even when inflation cools. Drivers shift toward real yields and risk sentiment. The long term case does not rely on inflation alone.

by Alex Demolitor | Sep 11, 2025 | Definitions

The August 2025 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation increased by 0.4% for the month, double the 0.2% rise in July. These data were released at 8:30 am EST on September 11, 2025, by the Bureau of Labor Statistics (BLS). Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 2.9%, up from 2.7% in July.

The results aligned near economists’ consensus estimates. The table below is courtesy of Investing.com. The left column represents August’s figures, while the right column represents forecasters’ expectations. As you can see, core came in as expected, while the monthly headline figure outperformed.

While Fed Chairman Jerome Powell hinted at a potential rate cut later this month, the FOMC has been cautious in its approach to monetary policy. Rather than encourage another round of inflation by cutting rates prematurely, the committee has prioritized price stability, and today’s results did little to eliminate the concerns.

Used cars and trucks were the primary outliers, with both rising by 1.0% MoM. Gasoline prices also rose by 1.9% MoM after declining by 2.2% in July. Core inflation (which excludes the impacts of food and energy), rose by 0.3% in August, matching the 0.3% from July, and slightly outperforming the 0.2% in June.

Food Prices

The food index rose by 0.5% MoM in August following a flat reading in July. All six major grocery store food indexes increased:

- Cereals and bakery products (+0.1%)

- Meats, poultry, fish, and eggs (+1.0%)

- Dairy and related products (+0.1%)

- Fruits and vegetables (+1.6%)

- Nonalcoholic beverages (+0.6%)

- Other food at home (+0.1%)

Maintaining its momentum, the food away from home index rose by 0.3%, mirroring July, and slightly underperforming the 0.4% increase in June.

Energy Prices

The energy index jumped by 0.7% in August after declining by 1.1% in July. Gasoline prices increased by 1.9%, electricity by 0.2%, while natural gas dropped by 1.6%.

Core CPI

The August core CPI rose by 0.3% month-over-month and 3.1% Y-o-Y. Below is an itemized breakdown of the main price fluctuations seen in the core CPI reading:

- Shelter index: (+0.4%) [July: +0.2%]

- Rent index: (+0.3%) [July: +0.3%]

- Owners’ equivalent rent: (+0.4%) [July: +0.3%]

- Motor vehicle insurance: (+0.0%) [July: +0.1%]

- Medical care services: (-0.1%) [July: +0.8%]

- Physician services: (+0.3%) [July: +0.2%]

- Hospital services: (+0.0%) [July: +0.5%]

- Airline fares: (+5.9%) [July: +4.0%]

Seasonally Unadjusted CPI

Before seasonal adjustments, the CPI-U for August 2025 increased by 2.9% Y-o-Y to an index level of 323.976. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

Cuts Coming?

While the U.S. labor market has been weakening for some time, conflicting data had the FOMC preaching patience. However, with several sources converging recently and signaling a slowdown, a September rate cut is likely a done deal.

For example, the BLS released its latest U.S. nonfarm payrolls report on Sep. 5. The economy added 22,000 net new jobs (well below expectations), and the report stated:

“The change in total nonfarm payroll employment for June was revised down by 27,000, from +14,000 to -13,000, and the change for July was revised up by 6,000, from +73,000 to +79,000. With these revisions, employment in June and July combined is 21,000 lower than previously reported.”

Thus, while a 21,000 miscount may not seem like much, the key revelation was that June’s revision to -13,000 was the first net negative print since 2021.

To that point, the BLS reported on Sep. 9 that annual revisions showed the U.S. added 911,000 fewer jobs over the last 12 months than previously reported. An excerpt read:

“The preliminary estimate of the Current Employment Statistics (CES) national benchmark revision to total nonfarm employment for March 2025 is -911,000 (-0.6 percent), the U.S. Bureau of Labor Statistics reported today. The annual benchmark revisions over the last 10 years have an absolute average of 0.2 percent of total nonfarm employment.”

Finally, The Conference Board revealed on Aug. 26 that Americans’ assessment of the labor market continued to deteriorate. Stephanie Guichard, Senior Economist, Global Indicators at The Conference Board, said, “Consumer confidence dipped slightly in August but remained at a level similar to those of the past three months. The present situation and the expectation components both weakened. Notably, consumers’ appraisal of current job availability declined for the eighth consecutive month.”

More importantly, The Conference Board’s ‘labor differential’ metric soared to a new cycle high.

To explain, the gray line above tracks the U.S. unemployment rate, while the red line above tracks the labor differential. When the red line rises, it means that more survey respondents believe that jobs are “hard to get” versus “plentiful.”

Furthermore, with a rising red line often a precursor to a higher unemployment rate, the sharp spike on the right side of the chart should be a cause for concern for the FOMC.

All in all, while inflation uncertainty remains high, the second half of the FOMC’s dual mandate — maximum employment — remains challenged. Therefore, a continuation of the trend should result in more rate cuts in the months ahead.

As the drama unfolds, gold is the clear winner. The yellow metal hit another record high in September, and Goldman Sachs expects more upside in the months and years ahead.

To explain, the blue line above tracks the consolidated gold holdings of global central banks, while the red dashed line above tracks Goldman Sachs’ projection over the next several months.

As you can see, continued demand from the largest buyers should help keep the gold price elevated for the foreseeable future.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Please seek the guidance of a financial advisor before making any investment decision.

In addition, if credit concerns have increased alongside the economic uncertainty, there are solutions. American Debt Relief provides debt settlement services, including negotiating with creditors to help eliminate or reduce the monthly payments on your unsecured debts like credit cards, medical bills, and personal loans. Similarly, Money Management International can help lower your interest rates, remove late payment fees, and negotiate lump sum settlements. Services are also available for student loans, bankruptcy, disaster recovery, homebuying, reverse mortgages, and military families.

Last, CreditAssociates can help you become debt-free in as little as 24–36 months. There are no upfront fees, but the group only provides assistance with unsecured debts and some business loans.

Remember, speaking with a professional can help you avoid bankruptcy and protect your credit score. For more options, please consult our list of debt management firms that can help get you back on track.

by Alex Demolitor | Aug 12, 2025 | Definitions

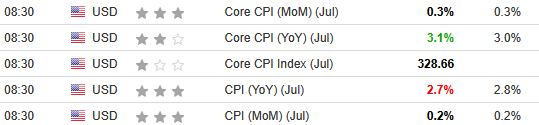

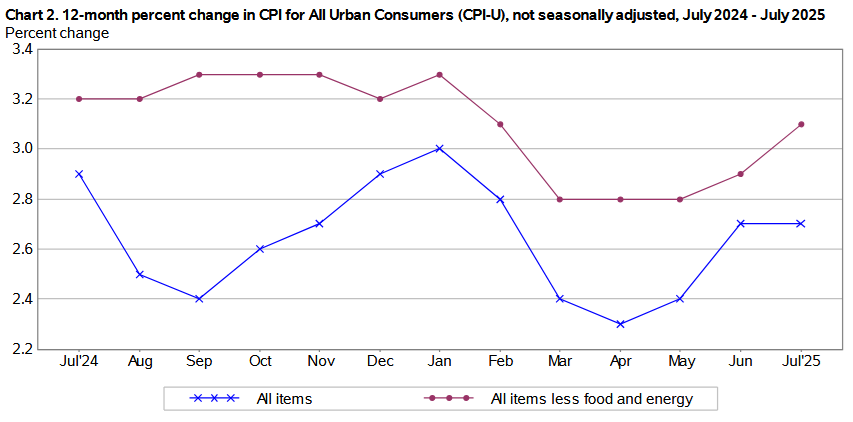

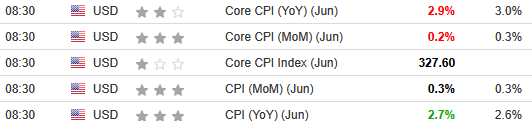

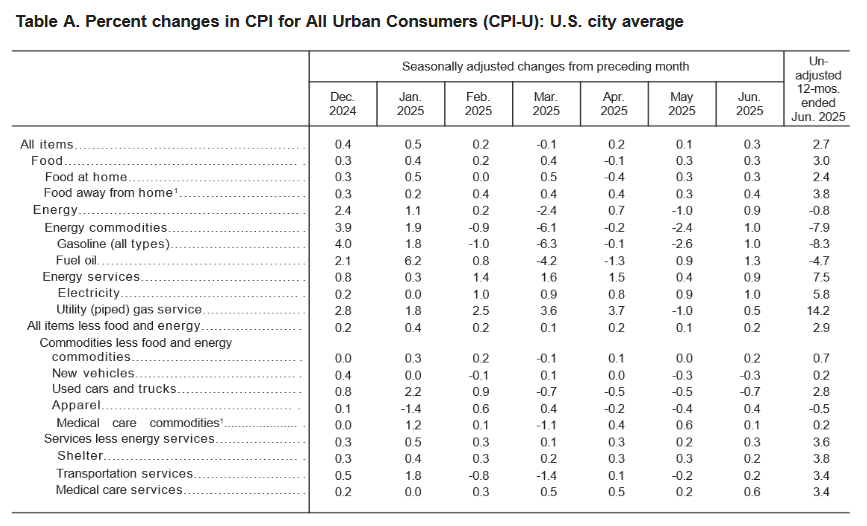

The July 2025 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation increased by 0.2% for the month, slightly below the 0.3% rise in June. These data were released at 8:30 am EST on August 12, 2025, by the Bureau of Labor Statistics. Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 2.7%, matching the figure from June.

The mixed results aligned near economists’ consensus estimates. The table below is courtesy of Investing.com. The left column represents July’s figures, while the right column represents forecasters’ expectations. As you can see, core inflation outperformed, while headline inflation underperformed.

After the latest FOMC meeting on Jul. 30, Chairman Jerome Powell said during his press conference:

“Higher tariffs have begun to show through more clearly to prices of some goods, but their overall effects on economic activity and inflation remain to be seen. A reasonable base case is that the effects on inflation could be short-lived, reflecting a one-time shift in the price level. But it is also possible that the inflationary effects could instead be more persistent, and that is a risk to be assessed and managed.”

Thus, with today’s inflation results doing little to alleviate those concerns, more data will likely be needed before the FOMC feels comfortable cutting rates.

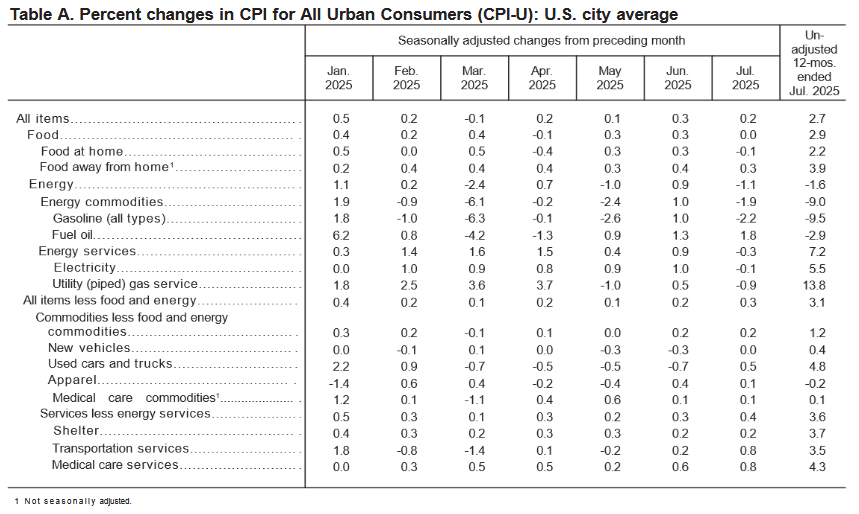

Transportation and medical care services were noticeable outliers in July, with each rising by 0.8% MoM, while fuel oil jumped by 1.8% MoM despite overall energy prices declining by 1.1% MoM. Core inflation (which excludes the impacts of food and energy), rose by 0.3% in July, up from 0.2% in June and 0.1% in May.

Food Prices

The food index was flat in July after rising by 0.3% MoM in June and May. Two of the six major grocery store food indexes increased, one was flat, and the other three realized deflation:

- Cereals and bakery products (-0.2%)

- Meats, poultry, fish, and eggs (+0.2%)

- Dairy and related products (+0.7%)

- Fruits and vegetables (+0.0%)

- Nonalcoholic beverages (-0.5%)

- Other food at home (-0.5%)

Maintaining its momentum, the food away from home index rose by 0.3%, as restaurant prices continue to outperform grocery store products.

Energy Prices

The energy index decreased by 1.1% in July after rising by 0.9% in June. Gasoline prices fell by 2.2%, natural gas by 0.9%, and electricity by 0.1%.

Core CPI

The July core CPI rose by 0.3% month-over-month and 3.1% Y-o-Y. Below is an itemized breakdown of the main price fluctuations seen in the core CPI reading:

- Shelter index: (+0.2%) [June: +0.2%]

- Rent index: (+0.3%) [June: +0.2%]

- Owners’ equivalent rent: (+0.3%) [June: +0.3%]

- Motor vehicle insurance: (+0.1%) [June: +0.1%]

- Medical care services: (+0.8%) [June: +0.6%]

- Physician services: (+0.2%) [June: +0.2%]

- Hospital services: (+0.5%) [June: +0.7%]

- Airline fares: (+4.0%) [June: -0.1%]

Seasonally Unadjusted CPI

Before seasonal adjustments, the CPI-U for July 2025 increased by 2.7% Y-o-Y to an index level of 323.048. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

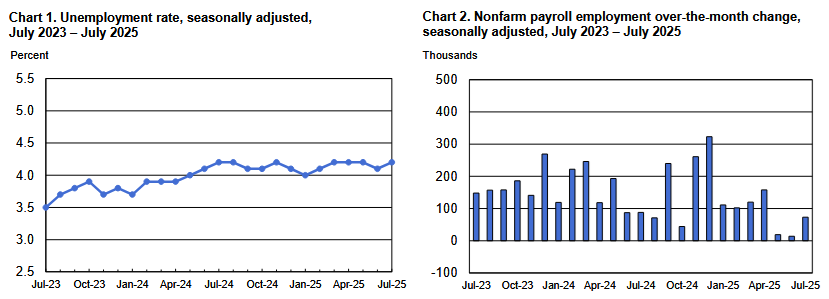

Tough Job Ahead?

The on-again, off-again, relationship with rate cuts continues to play out, as surprising labor market revisions confirmed the lingering weakness present in private data sources.

For example, U.S. job openings have declined, and ADP recently reported a net loss in its monthly private payrolls. However, the data was largely ignored because U.S. nonfarm payrolls — sourced from the Bureau of Labor Statistics (BLS) — continued to show solid growth and healthy hiring. But, that all changed on Aug. 1. The report stated:

“Revisions for May and June were larger than normal. The change in total nonfarm payroll employment for May was revised down by 125,000, from +144,000 to +19,000, and the change for June was revised down by 133,000, from +147,000 to +14,000. With these revisions, employment in May and June combined is 258,000 lower than previously reported.”

Thus, while the unemployment rate held steady near 4.2%, the blue bars furthest to the right of the second chart below show how the pace of employment growth has declined significantly over the last few months.

Moreover, the massive downward revisions further complicate the FOMC’s already tough balancing act between taming inflation and maintaining maximum employment.

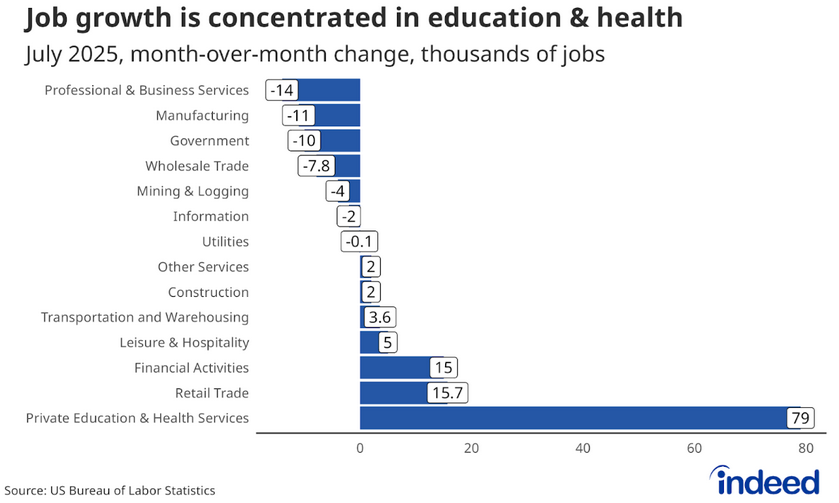

To that point, Indeed noted on Aug. 1 that the composition of hiring in July was equally troubling. An excerpt read:

“The sectoral breakdown from the jobs report is especially striking, with private education and health services adding 79,000 jobs, while other sectors, including professional and business services, manufacturing, and government, lost more than 10,000 jobs each. While the healthcare and social assistance sub-sector accounts for just 14.6% of total jobs in the economy, 48.8% of all employment growth in the US has occurred in this sub-sector over the past year….

“The increasing concentration of jobs in certain sectors and an outright contraction of jobs in many others does not bode well for the market going forward.”

So, while the FOMC’s latest Summary of Economic Projections has market participants expecting two rate cuts before the end of 2025, Vice Chair of Supervision, Michelle Bowman, advocated for three interest rate reductions on Aug. 9 to act as a hedge “against the risk of a further erosion in labor market conditions and a further weakening in economic activity.” Yet, other committee members prefer a wait-and-see approach, and there is plenty of division among the group.

All in all, there is so much volatility in the data that one month’s sunshine becomes next month’s storm. And with tariff uncertainty still lingering, FOMC members may struggle to form a clear consensus in the months ahead.

In contrast, the economic tension is bullish for gold, with the yellow metal hitting a new record high in August — surpassing $3,500 — and the long-term momentum remains intact.

To explain, Goldman Sachs still expects gold to hit $4,000 by mid-2026. The investment bank’s latest analysis (the dashed red line) is well ahead of what’s priced into the futures market (the dashed gray line), which means there’s still room for traders to shift their expectations upwards.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Please seek the guidance of a financial advisor before making any investment decision.

In addition, if credit concerns have increased alongside the economic uncertainty, there are solutions. Americor helps individuals and families with debt settlement, credit counseling, and provides consolidation loans by converting high-interest debt into products with lower interest rates and more manageable monthly payments.

Likewise, National Debt Relief offers advice, counselling, and negotiates with unsecured creditors to reduce your outstanding balance. It’s also a member of the American Fair Credit Council (AFCC) and the International Association of Professional Debt Arbitrators (IAPDA).

Finally, Trinity Debt Management is a nonprofit Christian group that delivers similar debt relief services and may be well-suited for Americans seeking faith-based advice and solutions.

Remember, speaking with a professional can help you avoid bankruptcy and protect your credit score. For more options, please consult our list of debt management firms that can help get you back on track.

by Alex Demolitor | Jul 15, 2025 | Definitions

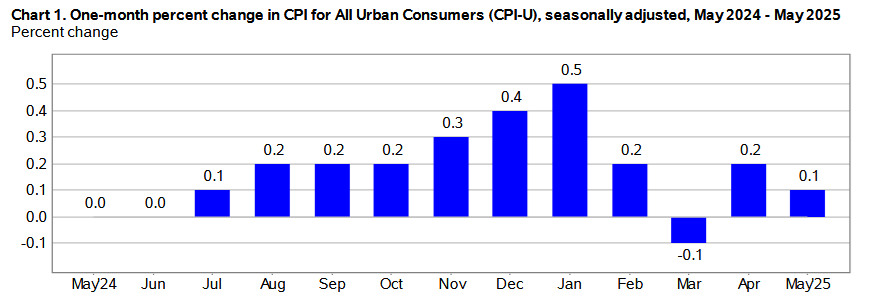

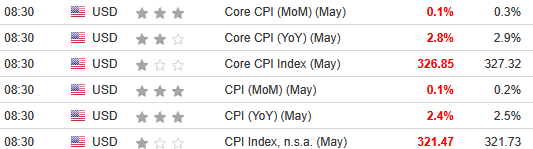

The June 2025 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation rose by 0.3% for the month, up from 0.2% in May. These data were released at 8:30 am EST on July 15, 2025, by the Bureau of Labor Statistics. Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 2.7%, a jump from 2.4% Y-o-Y in May.

The mixed results aligned near economists’ consensus estimates. The table below is courtesy of Investing.com. The left column represents June’s figures, while the right column represents forecasters’ expectations. As you can see, core was cool, while the headline figure was somewhat hot.

Despite that, fresh tariff threats could increase the FOMC’s inflation concerns. Chairman Jerome Powell said recently that resurgent inflation “is a risk. As the people who are supposed to keep stable prices, we need to manage that risk. That’s all we’re doing…. It is just something you want to approach carefully. If we make a mistake people will pay the cost for a long time.”

Thus, today’s data may not have done enough to alleviate those concerns.

Electricity, gasoline, and fuel oil led the headline increase, as the metrics rose by 1% or more MoM . Core inflation (which excludes the impacts of food and energy), rose by 0.2% in June, up from 0.1% in May.

Food Prices

The food index jumped by 0.3% MoM in June, matching May, and three of the six major grocery store food indexes realized deflation once again:

- Cereals and bakery products (-0.2%)

- Meats, poultry, fish, and eggs (-0.1%)

- Dairy and related products (-0.3%)

- Fruits and vegetables (+0.9%)

- Nonalcoholic beverages (+1.4%)

- Other food at home (+0.2%)

Maintaining its momentum, the food away from home index rose by 0.4%, as restaurant inflation accelerated in June.

Energy Prices

The energy index increased by 0.9% in June after falling by 1.0% in May. Gasoline prices rose by 1.0%, natural gas by 0.5%, and electricity by 1.0%.

Core CPI

The June core CPI rose by 0.2% month-over-month and 2.9% Y-o-Y. Below is an itemized breakdown of the main price fluctuations seen in the core CPI reading:

- Shelter index: (+0.2%) [May: +0.3%]

- Rent index: (+0.2%) [May: +0.2%]

- Owners’ equivalent rent: (+0.3%) [May: +0.3%]

- Motor vehicle insurance: (+0.1%) [May: +0.7%]

- Medical care services: (+0.6%) [May: +0.2%]

- Physician services: (+0.2%) [May: -0.3%]

- Hospital services: (+0.7%) [May: +0.4%]

- Airline fares: (-0.1%) [May: -2.7%]

Seasonally Unadjusted CPI

Before seasonal adjustments, the CPI-U for June 2025 increased by 2.7% Y-o-Y to an index level of 322.561. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

Trump’s Tariff Threats

After a three-month tariff reprieve, U.S. President Donald Trump ignited trade war fears again by threatening new levies on Canada, Mexico, Brazil, and the EU. And while most of the dues don’t come into effect until Aug. 1, and he could announce another pause when the deadline arrives, the uncertainty is another headache for the FOMC.

With the committee largely adopting a wait-and-see approach to interest rate cuts, the longer the uncertainty lingers, the more time and data they need to assess the situation. Consequently, while inflation remains above their 2% target and the labor market looks solid on the surface, the tariff diversion could distract from the underlying warning signs.

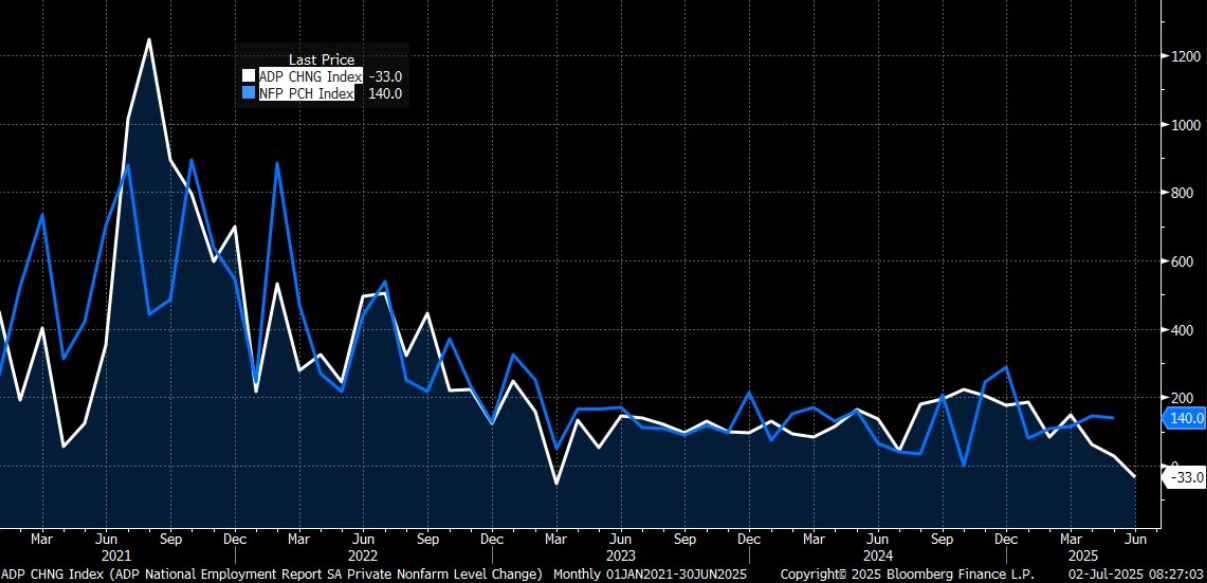

For example, U.S. nonfarm payrolls came in at 147,000 on Jul. 3, and the unemployment rate declined from 4.2% to 4.1%. However, ADP reported on Jul. 2 that private employers cut 33,000 jobs in June, which was a rare negative print from the payrolls provider. So, while government job gains helped bolster the former, the corporate sector could be signaling that tariff uncertainty is hurting business prospects.

To explain, the blue line above tracks the monthly change in the private component of U.S. nonfarm payrolls, while the white line above tracks the monthly change in ADP’s figures. If you analyze the connection, you can see the pair often moves in a similar direction.

More importantly, the gap on the right side of the chart shows how negative ADP payrolls (the white line) contrast the strength of the NFP number (the blue line). As such, the U.S. labor market may be weaker than it appears.

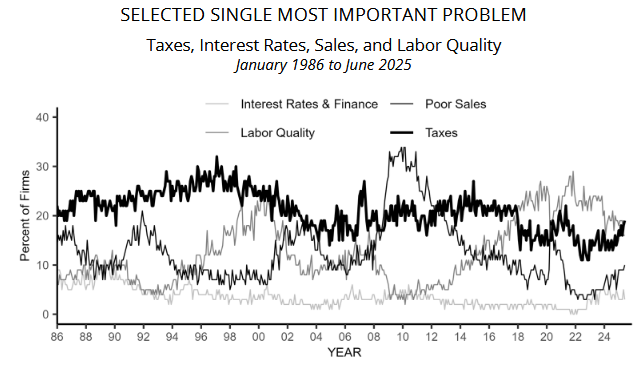

To that point, the NFIB released its latest Small Business Optimism Index on Jul. 8. The report noted that 10% of respondents cited poor sales as their single most important problem, the highest reading since March 2021.

To explain, the second-darkest line on the chart above tracks the poor sales component. If you analyze the right side of the chart, you can see that it continues to trend higher and is unlikely to reverse until the macroeconomic clouds clear. Furthermore, if a sales slump continues to plague U.S. small businesses, they may respond by reducing headcount and further weakening the labor market.

All in all, while tariffs will likely exacerbate the growth and employment slowdown, the economic turmoil is bullish for gold. The yellow metal remains in an uptrend and concerns about the U.S. dollar and its safe-haven status have investors and central banks allocating more capital toward gold.

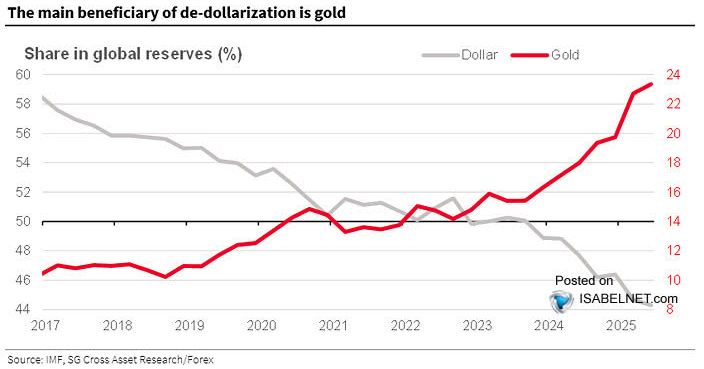

To explain, the gray line above tracks the share of U.S. dollar reserves held by global central banks, while the red line above tracks the share of gold reserves held by global central banks. If you analyze the post-COVID shift, you can see that U.S. debt and spending concerns caused global institutions to reduce their USD exposure and increase their gold assets. And with the trend poised to continue, flows and fundamentals should keep gold elevated for the foreseeable future.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Please seek the guidance of a financial advisor before making any investment decision.

In addition, if credit concerns have increased alongside the economic uncertainty, you’re not alone. New Era Debt Solutions is a top-rated debt settlement company that can help alleviate unsecured claims in as little as 24 to 48 months. Similarly, Family Credit Management is an excellent nonprofit credit counseling agency that provides the education and resources necessary to determine the optimal path to financial well-being.

For debt consolidation, Mariner Finance is a reputable personal loan provider that caps its APRs at 35.99%. You can borrow $1,000 to $25,000 (up to $50,000 in select states) and solutions are available for applicants that often don’t qualify at traditional banks.

Remember, speaking with a professional can help you avoid bankruptcy and protect your credit score. To learn more, please consult our list of debt management firms that can help get you back on track.

by Alex Demolitor | Jun 11, 2025 | Definitions

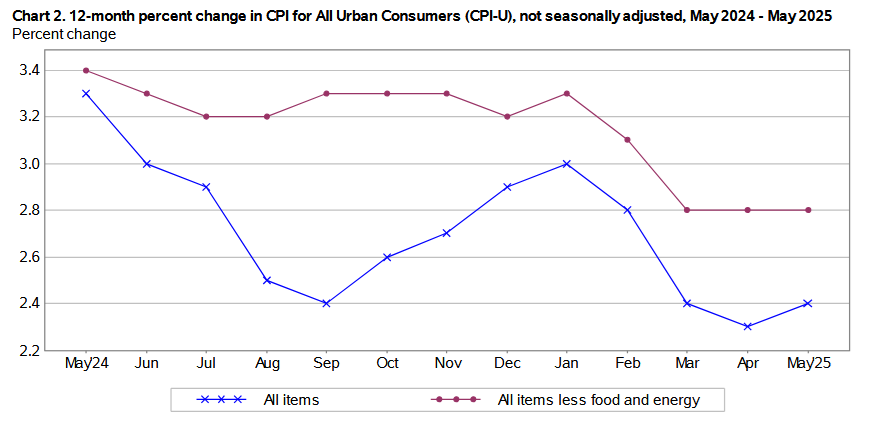

The May 2025 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation rose by 0.1% for the month, down from April’s 0.2% increase. These data were released at 8:30 am EST on Tuesday, June 11, 2025, by the Bureau of Labor Statistics. Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 2.4%, a small rise from the 2.3% Y-o-Y in April.

The downside surprise was more welcome news, as the results missed economists’ consensus estimates. The table below is courtesy of Investing.com. The left column represents May’s figures, while the right column represents forecasters’ expectations. As you can see, tariffs have not been as inflationary as anticipated.

Despite the deceleration, the FOMC has been increasingly concerned about inflation. The May meeting Minutes (released on May 28) stated:

“The substantial upward revision to the inflation forecast in 2025 was judged to leave the risks around the inflation projection balanced in that year. Thereafter, the staff continued to view the risks around the inflation forecast as skewed to the upside, with recent increases in some measures of inflation expectations raising the possibility that inflation would prove to be more persistent than the baseline projection assumed.”

As a result, with the FOMC somewhat offside in its projection, a weaker CPI could surprise market participants in the months ahead.

Gasoline, used cars and trucks, and apparel led May’s downside momentum, while shelter held steady at 0.3% MoM. Core inflation (which excludes the impacts of food and energy), rose by 0.1% in May, declining from the 0.2% rise in April.

Food Prices

The food index jumped by 0.3% MoM in May, after falling by 0.1% in April, and three of the six major grocery store food indexes realized deflation:

- Cereals and bakery products (+1.1%)

- Meats, poultry, fish, and eggs (-0.4%)

- Dairy and related products (-0.1%)

- Fruits and vegetables (+0.3%)

- Nonalcoholic beverages (-0.3%)

- Other food at home (+0.7%)

Maintaining its momentum, the food away from home index rose by 0.3%, as restaurant inflation stayed resilient.

Energy Prices

The energy index dropped by 1.0% in May, a noticeable turn from the 0.7% increase in April. Gasoline prices fell by 2.6%, while natural gas deflated by 1%, and electricity jumped by 0.9%.

Core CPI

The May core CPI rose by 0.1% month-over-month and 2.8% Y-o-Y. Below is an itemized breakdown of the main price fluctuations seen in the core CPI reading:

- Shelter index: (+0.3%) [April: +0.3%]

- Rent index: (+0.2%) [April: +0.2%]

- Owners’ equivalent rent: (+0.3%) [April: +0.4%]

- Motor vehicle insurance: (+0.7%) [April: +0.6%]

- Medical care services: (+0.2%) [April: +0.5%]

- Physician services: (-0.3%) [April: +0.3%]

- Hospital services: (+0.4%) [April: +0.6%]

- Airline fares: (-2.7%) [April: -2.8%]

Seasonally Unadjusted CPI

Before seasonal adjustments, the CPI-U for May 2025 increased by 2.4% Y-o-Y to an index level of 321.465. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

Juggling the Dual Mandate

While inflation has been the primary driver of the FOMC’s caution, it’s important to remember that maximum employment is the second half of the committee’s dual mandate. And with mixed data hitting the wire recently, slower job growth could support rate cuts in the months ahead.

On the positive side, U.S. nonfarm payrolls outperformed expectations on Jun. 6, as the economy added 139,000 new jobs in May, and the unemployment rate held firm at 4.2%. However, the report stated:

“The change in total nonfarm payroll employment for March was revised down by 65,000, from +185,000 to +120,000, and the change for April was revised down by 30,000, from +177,000 to +147,000. With these revisions, employment in March and April combined is 95,000 lower than previously reported.”

As a result, prior months were weaker than they appeared, and another downward revision could occur next month. Moreover, the unemployment rate continues to creep higher off of its 2023 low.

As further evidence, ADP’s private payrolls missed expectations on Jun. 4. The report stated, “The pace of hiring in May reached its lowest level since March 2023.” Furthermore, firms of all sizes reduced their headcounts in May, with the only positive contribution of 51,000 additions coming from firms with 50-249 employees. Conversely, layoffs were driven by small establishments.

Finally, the NFIB released its small business employment report on May 31. The release stated: “A seasonally adjusted net 12 percent of owners plan to create new jobs in the next three months, down 1 point from April. Job creation plans remain in weak territory compared to recent history.”

Furthermore, “Seasonally adjusted, a net 26 percent reported raising compensation, down 7 points from April and the lowest reading since February 2021. This was the greatest monthly decline since April 2020. A net 20 percent (seasonally adjusted) plan to raise compensation in the next three months, up 3 points from April. Clearly, the pressure of labor costs on inflation is easing.”

Thus, with hiring intentions and expected wage increases both heading in negative directions, a weaker U.S. labor market could prompt the Fed to ease monetary policy during the summer months. If so, the dovish recalibration could push gold to another record high. The yellow metal has been one of the best-performing assets in 2025, and ETF flows could be the next bullish catalyst.

To explain, the Deutsche Bank chart above shows how after four negative years, gold ETF flows turned positive in 2025. However, the blue bar furthest to the right is relatively small, and prior periods saw much larger inflows that were sustained for several years.

As such, a repeat of recent history could support a gold bull market that lasts into 2026 and beyond.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Please seek the guidance of a financial advisor before making any investment decision.

In addition, if credit concerns have increased alongside the economic uncertainty, you’re not alone. New Era Debt Solutions is a top-rated debt settlement company that can help alleviate unsecured claims in as little as 24 to 48 months. Similarly, Family Credit Management is an excellent nonprofit credit counseling agency that provides the education and resources necessary to determine the optimal path to financial well-being.

For debt consolidation, Mariner Finance is a reputable personal loan provider that caps its APRs at 35.99%. You can borrow $1,000 to $25,000 (up to $50,000 in select states) and solutions are available for applicants that often don’t qualify at traditional banks.

Remember, speaking with a professional can help you avoid bankruptcy and protect your credit score. To learn more, please consult our list of debt management firms that can help get you back on track.