by Sarah Bauder | May 10, 2026 | CPI, Inflation

Inflation is a general increase in the price of goods and services over time. In plain English, it means your money does not buy as much as it used to. That can sound like an economics textbook problem, but it is really a personal finance problem. Inflation affects your savings, investments, debt, retirement income, property costs, and everyday household budget.

I have been writing about financial and investment-related topics for more than two decades, and inflation is one of those subjects that always comes back into focus when people start feeling squeezed. You may not follow every monthly CPI report, but you definitely notice when groceries, insurance, rent, utilities, and borrowing costs start taking a bigger bite out of your income.

Inflation is commonly measured using the Consumer Price Index, or CPI. The CPI tracks price changes across a basket of consumer goods and services. If you want to compare the buying power of money across different years, you can also use our CPI inflation calculator.

According to the U.S. Bureau of Labor Statistics, the Consumer Price Index for All Urban Consumers rose 3.8% over the 12 months ending April 2026. Core CPI, which excludes food and energy, rose 2.8% over the same period. That is lower than the worst inflation Americans experienced in 2022, but it is still high enough to matter when you are planning your savings, investments, and retirement.

Quick Takeaway

Inflation does not just make things more expensive. It changes the real value of your savings, income, investments, debt payments, and future retirement needs. The key is to think in terms of purchasing power, not just the dollar amount sitting in your account.

Historical CPI data helps show how inflation changes purchasing power over time. Source: Bureau of Labor Statistics

The Main Effects of Inflation on Your Personal Finances

Inflation does not affect every part of your financial life in the same way. Some assets may benefit from inflation. Some get hurt by it. Some debts become easier to handle, while others become more expensive.

| Area of Your Finances |

How Inflation Can Affect It |

What to Watch |

| Savings |

Cash can lose purchasing power if interest rates do not keep up with inflation. |

Real return after inflation and taxes. |

| Stocks |

Companies may raise prices, but they may also face higher costs and lower margins. |

Pricing power, earnings growth, and valuation. |

| Bonds |

Fixed payments can become less valuable when inflation rises. |

Interest rates, duration, and inflation protection. |

| Property |

Property values and rents may rise, but ownership costs can rise too. |

Mortgage type, insurance, taxes, repairs, and rates. |

| Retirement |

Future expenses may be much higher than today’s expenses. |

Inflation-adjusted income and withdrawal planning. |

The Effects of Inflation on Your Savings

One area most exposed to inflation is cash savings. A savings account can be a smart place for emergency money, short-term goals, and cash you may need quickly. I am not against holding cash. In fact, I think many people underestimate how important liquidity is when life gets messy.

But cash has one major weakness: it can quietly lose purchasing power if the interest rate on your account is lower than inflation.

For example, if you have $1,000 in a savings account earning 1% annually, you would have $1,010 after one year before taxes. But if inflation is running at 3.8%, you would need about $1,038 just to preserve roughly the same purchasing power. Your bank balance went up, but your real buying power went down.

This is what makes inflation so frustrating. You may not technically “lose” money in a savings account, but the money can still buy less over time.

Important point: The real return on savings is the interest rate you earn minus inflation. If your savings account earns 2% and inflation is 4%, your real return is roughly negative 2% before taxes.

This does not mean you should invest your emergency fund in the stock market. It means you should separate short-term savings from long-term wealth-building money. Cash is useful for stability and flexibility. But long-term money usually needs a plan that has a better chance of keeping up with inflation.

To understand how inflation has changed purchasing power historically, you can review our historical CPI tables or compare specific years using the calculator.

The Impact of Inflation on Stocks

Investing in stocks comes with more risk than keeping money in a savings account. Stock prices move up and down, and nobody can guarantee short-term returns. But over long periods, stocks have often helped investors protect and grow purchasing power better than cash.

That said, stocks are not automatically protected from inflation.

Inflation can affect stocks in a few different ways. When the economy is strong, companies may be able to raise prices, grow revenue, and increase earnings. That can support share prices. But when inflation rises too quickly, companies may also face higher costs for wages, raw materials, energy, shipping, rent, and financing. If those costs rise faster than revenue, profit margins can suffer.

This is why inflation can be especially difficult for companies that do not have pricing power. A business with a strong brand, essential products, and loyal customers may be able to pass some cost increases on to consumers. A weaker business may have to absorb those costs.

From an investor’s perspective, the real question is not only whether stocks go up in dollar terms. It is whether your investment return beats inflation over time.

Investor takeaway: During inflationary periods, focus on real returns, diversification, company quality, pricing power, debt levels, and your time horizon. Inflation can create pressure in the short term, but high-quality businesses may still help preserve purchasing power over the long term.

For a broader look at portfolio decisions during different economic conditions, you can read our guide on investing during inflation and deflation.

1979 $10,000 Treasury Bond. Fixed-income investments can be affected by inflation because future payments may lose purchasing power. Photo: Wikipedia

The Effects of Inflation on Bonds and Treasury Bills

Bonds and Treasury bills are often viewed as safer investments than stocks, but inflation can still affect them. The main issue is that many debt securities pay fixed interest. If inflation rises, those fixed payments may not buy as much as they did before.

For example, a bond paying 3% may look reasonable when inflation is 2%. But if inflation rises to 4% or 5%, the real value of that bond income may fall. This is one reason bond investors pay close attention to inflation expectations and interest rates.

Inflation can also affect bond prices through interest rates. When inflation is high, the Federal Reserve may keep interest rates higher to help bring inflation down. The Federal Reserve says it sets U.S. monetary policy to promote maximum employment and stable prices. When rates rise, older bonds with lower yields may become less attractive, which can push their market value down.

One option for investors worried about inflation is Treasury Inflation-Protected Securities, also known as TIPS. According to TreasuryDirect, TIPS are designed to help protect investors from inflation because the principal adjusts with changes in the Consumer Price Index.

TIPS are not perfect. They can still fluctuate in value, and they may have tax considerations depending on the account where they are held. But they can be useful for people who want part of their fixed-income portfolio linked to inflation.

You can learn more in our guide to inflation-protected bonds.

Property Ownership and Inflation

Property ownership can benefit from inflation, but it is not as simple as saying real estate always wins when prices rise.

On the positive side, property values and rents may rise over time. If you own a home with a fixed-rate mortgage, your principal and interest payment stays the same even as wages, rents, and general prices increase. That can make a fixed mortgage feel more affordable in real terms over time.

This is one reason many homeowners who locked in low fixed mortgage rates before rates rose have been reluctant to sell. Their monthly mortgage payment may be difficult to replace in the current rate environment.

However, inflation can also make property ownership more expensive. Home insurance, property taxes, repairs, materials, labor, utilities, and maintenance costs can all rise. Higher mortgage rates can also reduce buyer demand, which may make it harder to sell a property at the price you want.

| How Inflation Can Help Property Owners |

How Inflation Can Hurt Property Owners |

| Fixed-rate mortgage payments may become cheaper in real terms. |

Insurance, taxes, repairs, and maintenance may rise. |

| Property values may rise over long periods. |

Higher mortgage rates can reduce affordability for buyers. |

| Landlords may be able to raise rents. |

Operating costs may rise along with rental income. |

Real estate can be a useful inflation hedge in some situations, but it still depends on location, financing, purchase price, cash flow, and ownership costs.

Warren Buffett and the Matter of Inflation

Warren Buffett has written and spoken about inflation for decades, and his perspective is still useful for everyday investors. Buffett has long warned that inflation can quietly reduce the real value of investment returns, even when investors appear to be making money on paper.

In his classic 1977 Fortune essay, “How Inflation Swindles the Equity Investor,” Buffett explained why inflation can be difficult for both bondholders and stock investors. Bonds are vulnerable because future payments are made in dollars that may be worth less. Stocks can also struggle when inflation increases business costs, interest rates, and the amount of capital companies need just to maintain operations.

That does not mean Buffett believes people should avoid stocks. His broader investing philosophy has long favored owning high-quality businesses with durable competitive advantages, strong pricing power, and the ability to generate cash over long periods. Those traits can matter even more when inflation is eating into purchasing power.

Warren Buffett has written about inflation’s impact on investors for decades. Photo: Reuters/Carlo Allegri

The lesson for personal finance is simple: inflation is not just about higher grocery or gas prices. It also affects the real value of savings, bonds, retirement income, and investment returns. That is why investors need to think in terms of after-inflation returns, not just headline returns.

Inflation and Retirement Planning

Inflation becomes especially important when you are planning for retirement. If you are working, you may be able to earn more, change jobs, negotiate higher pay, or adjust your budget. Once you retire, your options may be more limited.

Retirees who depend heavily on fixed income can be vulnerable when prices rise. Even moderate inflation can have a major effect over long periods.

| Today’s Annual Spending |

After 10 Years at 3% Inflation |

After 20 Years at 3% Inflation |

| $40,000 |

About $53,756 |

About $72,245 |

| $60,000 |

About $80,635 |

About $108,367 |

| $80,000 |

About $107,512 |

About $144,489 |

This is why retirement planning should include inflation assumptions. A plan that looks comfortable in today’s dollars may look much tighter once you account for future housing, healthcare, food, insurance, travel, and utility costs.

Some people look at annuities, TIPS, dividend-paying stocks, real estate, or other income-producing assets as part of an inflation-aware retirement plan. None of these are perfect on their own, but they can each play a role depending on your age, risk tolerance, income needs, and total financial picture.

If you are researching this topic, you may also want to read our article on whether annuities are a good investment for inflation protection.

Planning for Inflation

Inflation is part of financial life. You cannot control the CPI, the Federal Reserve, energy prices, food prices, or global supply shocks. But you can build a financial plan that does not fall apart when prices rise.

In my view, the best approach is not to chase one perfect inflation hedge. It is to build layers of protection across your finances.

Practical Inflation Checklist

- Keep an emergency fund. Cash still matters, even if it does not always beat inflation.

- Watch your real return. Compare your savings and investment returns against inflation.

- Be careful with variable-rate debt. Credit cards and adjustable-rate loans can become more expensive when rates rise.

- Consider inflation-protected options. TIPS and other inflation-linked assets may help in certain portfolios.

- Invest for the long term. Diversified portfolios may help protect purchasing power over time.

- Review retirement assumptions. Future expenses may be much higher than today’s expenses.

- Follow CPI data. Use the CPI release schedule to track monthly inflation updates.

Gold is another asset people often consider during inflationary periods. I understand why. Gold has a long history as a store of value, and many investors look to it during periods of currency uncertainty or market stress. But gold is not a guaranteed inflation hedge in every period. It can be useful as a diversifier, but it should not be treated as a complete financial plan.

If you want to explore that topic further, we have a guide on gold and inflation. You can also use our inflation-adjusted gold return calculator to compare gold’s performance in real purchasing power terms.

For a broader look at possible inflation hedges, you may also find our article on inflation-resistant investments helpful. And if you want to understand why inflation can be measured in different ways, read our guide to different ways of measuring inflation.

Final Thoughts

Inflation affects personal finances because it changes the value of money. It can weaken the buying power of cash savings, pressure stocks and bonds, change the math on debt, complicate property ownership, and make retirement more expensive than expected.

The key is to think beyond nominal dollars. A $50,000 savings account, a 5% investment return, or a $60,000 retirement budget only tells part of the story. The more important question is what those dollars can actually buy after inflation.

That is why I believe inflation should be part of every serious financial plan. Not because you can predict it perfectly, but because ignoring it can make your savings, investments, and retirement plan look stronger than they really are.

If you want to stay current, you can review the latest 2026 U.S. inflation rate and CPI data and compare it with prior years such as the 2025 CPI and inflation data.

Frequently Asked Questions About Inflation and Personal Finances

How does inflation affect your personal finances?

Inflation affects your personal finances by reducing the purchasing power of your money. If prices rise faster than your income, savings, or investment returns, you may be worse off even if your account balances are higher in dollar terms.

How does inflation affect savings?

Inflation can reduce the real value of savings when the interest rate on your savings account is lower than the inflation rate. Savings accounts are still useful for emergency funds and short-term needs, but they may not be enough for long-term purchasing power protection.

How does inflation affect stocks?

Inflation can affect stocks by increasing business costs, interest rates, and pressure on consumer spending. Some companies can handle inflation better than others, especially those with strong pricing power, healthy balance sheets, and products people continue buying even when prices rise.

How does inflation affect bonds?

Inflation can hurt traditional bonds because fixed interest payments lose purchasing power when prices rise. Bond prices can also fall when interest rates increase. Inflation-protected securities, such as TIPS, are designed to help address this risk, although they can still fluctuate in value.

Is inflation good or bad for homeowners?

Inflation can help homeowners with fixed-rate mortgages because their monthly principal and interest payments stay the same while prices and wages may rise. However, homeowners may also face higher insurance, taxes, repairs, utilities, and maintenance costs.

Is inflation good or bad for debt?

Inflation can make fixed-rate debt easier to repay over time because the payment stays the same while the value of money declines. However, inflation can make variable-rate debt more expensive if interest rates rise, which is especially important for credit cards, adjustable-rate mortgages, and some personal loans.

How does inflation affect retirement?

Inflation can make retirement more expensive because future living costs may be higher than today’s costs. Retirees and future retirees should account for inflation when estimating income needs, withdrawal rates, healthcare costs, housing costs, and long-term savings goals.

What is the best way to protect your money from inflation?

There is no single best inflation hedge for everyone. A practical approach may include emergency savings, diversified investments, inflation-protected bonds, fixed-rate debt management, real estate, and possibly precious metals or other real assets depending on your goals and risk tolerance.

Why does my personal inflation rate feel higher than official CPI?

Your personal inflation rate may feel higher than official CPI if your biggest expenses are rising faster than the national average. For example, someone spending heavily on rent, groceries, insurance, healthcare, or gasoline may feel more pressure than the headline CPI number suggests.

How often is CPI data released?

The Bureau of Labor Statistics usually releases CPI data monthly. You can follow upcoming release dates using the CPI release schedule and compare current inflation data with historical CPI trends to see how prices have changed over time.

by Liam Hunt | Jul 12, 2023 | Inflation, Monthly CPI Updates

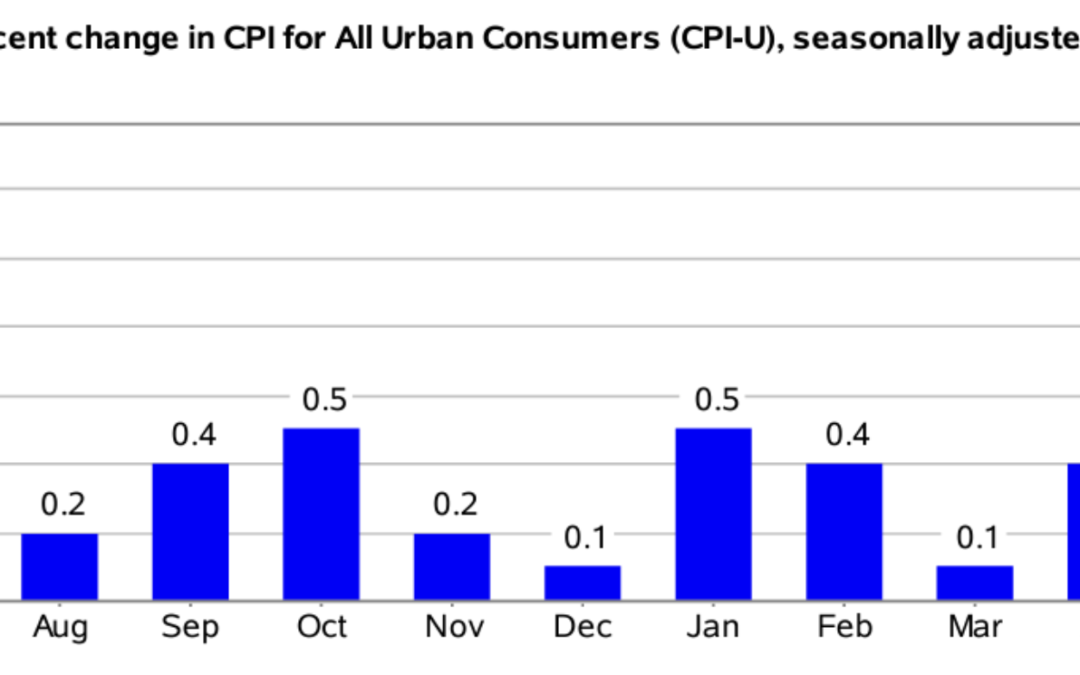

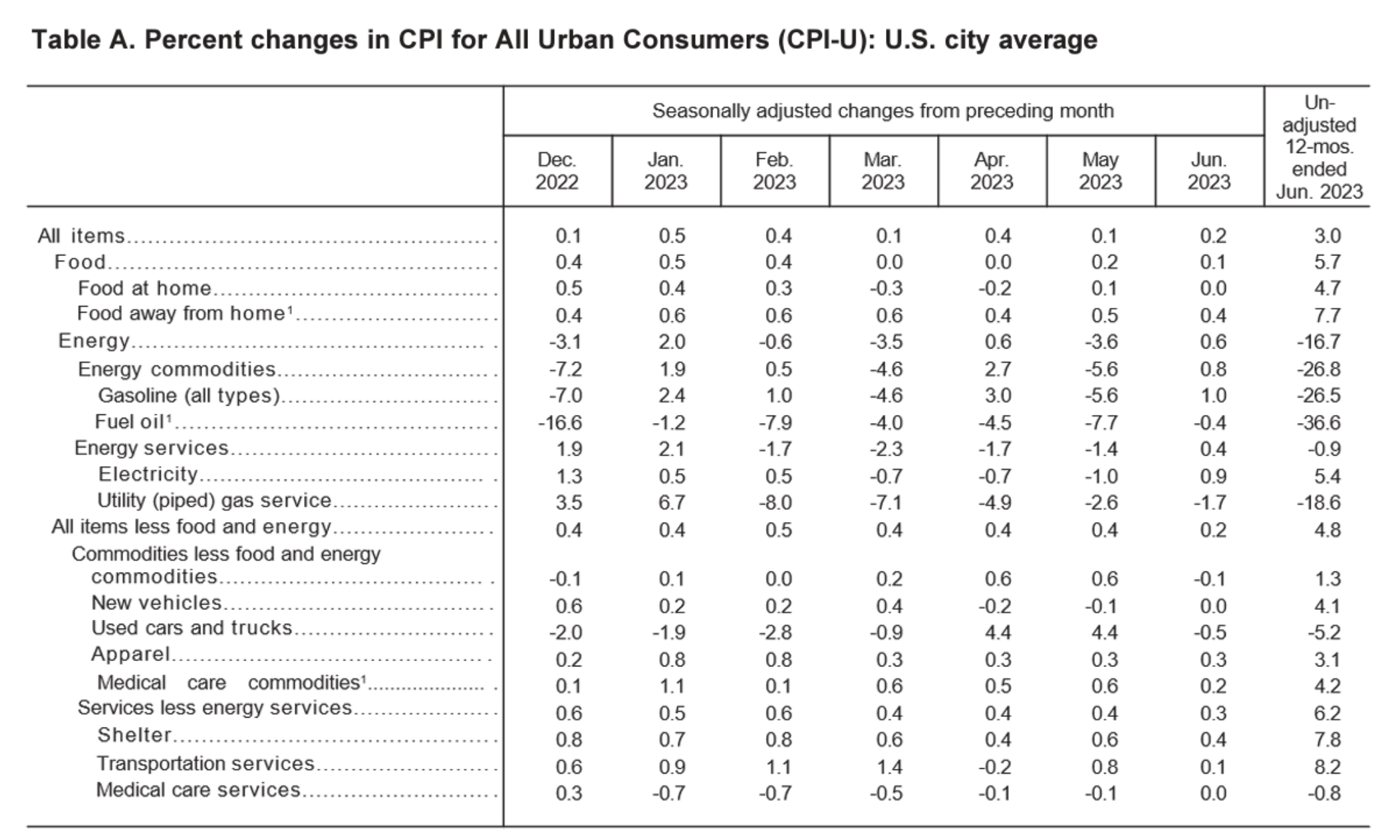

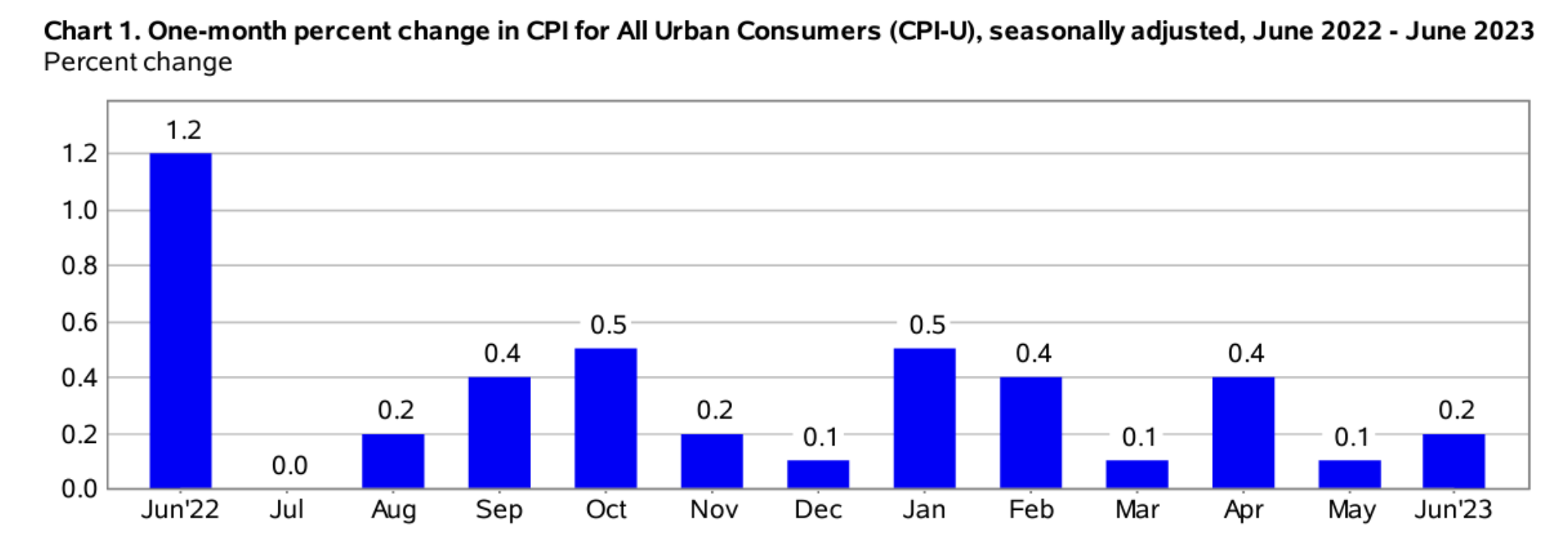

The Consumer Price Index for All Urban Consumers (CPI-U) increased by 0.2% on a seasonally unadjusted basis in June 2023, according to the Bureau of Labor Statistics report published July 12. Year-over-year, before seasonal adjustment the all-items index grew by 3.0%, constituting a major deceleration in the CPI-U from May’s 4.0% reading.

June’s rosy CPI report is the lowest in two years, when March 2021’s CPI report came in at 2.6% year-over-year. This month’s CPI report fared better than economists and investors expected, causing an immediate surge in the benchmark stock market indices on the morning of July 12. The rapid deceleration of the inflation rate in the U.S. is being taken by many as evidence that the Federal Reserve’s hawkish interest rate policy is performing as intended by successfully reining in inflation.

Nonetheless, the June 2023 CPI numbers are still 50% higher than the Fed’s target inflation rate of 2%—a figure that some doubt is possible to achieve without future rate hikes from the central bank.

Source: Bureau of Labor Statistics

June’s monthly CPI figure (0.2) came in higher than the previous month’s (0.1). The previous month’s “blip” in the monthly CPI report can be largely explained by the base-year effect seen between April 2021 and 2022 due to the Russian invasion of Ukraine, an event that saw immediate and large-scale price increases in oil, gas, and certain natural resources. These prices then partially settled in the subsequent months.

As depicted in the table above, the June 2023 CPI figure was largely driven by increases in consumer energy commodities and overall energy price increases.

Food Prices

The food index rose 0.1 percent in June after going unchanged in April and increasing 0.1 percent in May, representing a core market segment where consumer prices stagnated compared to the month prior. Notably, egg prices fell 7.3 percent in June after falling significantly in May—in total, egg prices have fallen by nearly half since the start of the year following a devastating avian flu outbreak that killed 43 million hens in 2022.

The meats, poultry, and eggs index dropped by 0.4 percent in June on the heels of an even large 1.2 percent decrease in May(-1.2%). However, year-over-year, the food at home index has risen by 4.7 percent, meaning your total grocery bill today compared to June 2022 is nearly 5 percent higher on average.

Energy Prices

The energy index rose in June May (0.6%) after falling in May. Notably, gasoline prices increased by 1.0 percent after dropping 5.6 percent in May. Concurrently, natural gas fell by 1.7 percent in June, marking the third consecutive month of natural gas price cuts. Fuel oil prices also fell, by about 0.4 percent in June.

Overall, energy costs inched up in June, constituting a minor deviation in the general trendline of falling energy prices ongoing since March. Year-over-year, energy prices are up 16.7 percent over 12 months.

Core June 2023 CPI

Regarding the core CPI data for June 2023 (inflation less food and energy), the index rose 0.2% month-over-month in June, down from a 0.6 percent acceleration in May. Below is an itemized breakdown of the main price fluctuations seen within June’s core CPI reading:

- Shelter index: +0.4% (+0.6% in May)

- Used cars and trucks: +4.4 (+4.4% in May)

- Lodging away from home: (-2.0%) (+1.8% in May)

- Medical care index: +0.1% (unchanged from May)

- Household furnishings: +3.6%

- Airline fares: (-8.1%) (-3.0% in May)

Source: Bureau of Labor Statistics

Seasonally Unadjusted CPI Data for June 2023

Before seasonal adjustments, the CPI-U for June 2023 increased (+0.3%) for the month, rising to an index level of 305.109. Since these figures are unadjusted, they include regular seasonal price fluctuations that generally occur by the same margins every year.

Now Is The Time to Protect Your Wealth

Although June’s CPI report may seem rosy, the U.S. dollar is only continuing to lose value by the day. The result? Millions of American families with less purchasing power than they had the month prior, making it that much harder to make ends meet. While inflation is beginning to enter familiar territory, the average American household has lost the equivalent of $7,400 in annual wages due to inflation and rate hikes since 2021.

Luckily, we can mitigate the adverse effects of inflation. Consider speaking to your financial advisor about diversifying your investment portfolio with alternative assets that may help insulate your savings from the devaluation of the U.S. dollar.

Gold and silver have historically outperformed traditional securities during most recessions and economic crises, including the 2020 stock market crash and the 2008 global financial crisis. For many, gold functions as an inflation hedge, providing a much-needed store of value when fiat assets depreciate. No wonder why it’s sought after by many successful investors like Ray Dalio and Kevin O’Leary as a risk management tool.

Want to get started investing in silver or gold? Open an account today with one of the best-rated gold IRA service providers. While you’re at it, stay up-to-date on inflation news in the months ahead. You can easily keep tabs on how inflation is holding back your household’s purchasing power by using our free CPI inflation calculator tool that tracks the wealth-eroding effects of inflation.

by Amine Rahal | Jun 30, 2023 | Definitions, Inflation

In the realm of economics, three terms often crop up in discussions about the health of an economy: inflation, recession, and depression. While they are interconnected in various ways, each term represents a distinct economic phenomenon with different implications for the economy and, by extension, for investors, businesses, and consumers. This article will delve into the definitions of inflation, recession, and depression and explore how they are linked. Let’s start by looking at a comparison table:

|

Inflation |

Recession |

Depression |

| Definition |

General increase in prices. |

Significant decline in economic activity, typically for two quarters or more. |

Severe and prolonged downturn in economic activity. |

| Impact on Economy |

Decreases purchasing power. Can stimulate economic activity when moderate, but leads to instability when too high. |

Results in higher unemployment, decreased consumer spending, and economic slowdown. |

Severe declines in employment and production, often causing significant economic hardship. |

| Common Causes |

Excessive growth in the money supply, demand-pull, or cost-push factors. |

Various, including financial crises, economic bubbles, or external shocks. |

Often a severe or prolonged recession, but can also be caused by a financial crisis or large-scale economic dislocation. |

| Central Bank Response |

May raise interest rates to slow economic activity and curb inflation. |

May lower interest rates and increase government spending to stimulate economic activity. |

Similar to recession, but response typically needs to be larger and more sustained. May involve significant fiscal policy responses as well. |

| Link to Other Two Terms |

High inflation can lead to a recession. Recession can lead to low inflation or deflation. |

Can turn into depression if severe and prolonged. Lower demand during a recession can lead to lower inflation. |

Could lead to deflation due to lower demand. However, policy responses could potentially lead to inflation. |

Inflation

Inflation is the rate at which the general level of prices for goods and services is rising, eroding purchasing power. In other words, as inflation increases, each unit of currency buys fewer goods and services. Inflation is updated monthly.

Moderate inflation is typical in a growing economy and can even stimulate economic activity. However, if it gets out of hand, it can lead to economic instability. The BLS uses the CPI to measure inflation.

The Federal Reserve, like most central banks, aims to control inflation by adjusting interest rates. Lower interest rates encourage spending and investment, which can boost economic activity and, potentially, inflation. Higher interest rates can slow economic activity and curb inflation.

Recession

A recession is typically defined as a significant decline in economic activity spread across the economy, lasting more than a few months. This is often seen in real GDP, real income, employment, industrial production, and wholesale-retail sales. Economists generally agree that two consecutive quarters of negative GDP growth indicate a recession.

Recessions can be caused by various factors, including financial crises, external shocks, and the bursting of economic bubbles. Policymakers often respond to recessions by lowering interest rates and increasing government spending, aiming to stimulate economic activity.

Depression

A depression represents a severe and prolonged downturn in economic activity. It’s more extended and more profound than a recession, characterized by significant declines in output, employment, and trade, often lasting several years. The most notable example is the Great Depression of the 1930s.

Depressions are rare, and economists don’t have a standardized definition like they do for a recession. However, they generally agree that depressions involve a substantial contraction in economic activity that lasts several years.

How Are They Linked?

Inflation, recession, and depression are intertwined in many ways:

- Inflation and Recession: Too much inflation can lead to a recession. When prices rise too quickly (hyperinflation), consumers can struggle to afford goods and services, and businesses can find it challenging to plan for the future. If the central bank tries to combat high inflation by raising interest rates too quickly, it can cool the economy too much and lead to a recession.

- Recession and Inflation: On the flip side, recessions can lead to lower inflation or even deflation (a general decrease in prices). In a recession, demand for goods and services falls, which can lead to lower prices.

- Recession and Depression: If a recession is particularly severe and prolonged, it can turn into a depression. While there’s no strict dividing line, depressions involve higher unemployment, lower output, and more significant declines in standards of living than recessions.

- Inflation and Depression: Inflation rates during a depression can vary. Sometimes, depressions can involve deflation, as demand for goods and services falls and businesses lower prices to try to entice customers. However, economic policy responses to a depression could lead to inflation. For example, if the government responds by increasing the money supply or government spending dramatically, it could eventually lead to increased inflation.

In summary, inflation, recession, and depression are all interconnected elements of economic cycles. By understanding these terms and their relationships, we can better grasp the complexities of economic health and make

FAQ

Q1: What causes inflation? A1: Inflation can be caused by various factors, including excessive growth in the money supply, demand-pull inflation where demand for goods and services outpaces supply, or cost-push inflation where the cost of raw materials or wages increase.

Q2: How can inflation be controlled? A2: Central banks often aim to control inflation by adjusting interest rates. By raising interest rates, central banks can decrease borrowing and spending, thus reducing inflation. Conversely, lowering interest rates can stimulate borrowing and spending, potentially leading to increased inflation.

Q3: What are the signs of a coming recession? A3: Common signs of a coming recession include a decline in the GDP, higher unemployment rates, lower consumer spending, decrease in business profits, and a volatile stock market.

Q4: How can a recession affect the average person? A4: During a recession, people might face job loss or reduced working hours. They may also see the value of their investments decrease, and it could become harder to get credit.

Q5: What’s the difference between a recession and a depression? A5: The main difference between a recession and a depression is the duration and severity of the economic downturn. A recession is a temporary decline in economic activity, typically lasting six months to a year. A depression, on the other hand, is a severe and prolonged economic downturn, often lasting several years.

Q6: How do governments respond to a depression? A6: In a depression, governments may enact expansive fiscal policies, such as increasing government spending, cutting taxes, or both, to stimulate the economy. Central banks may also adopt expansionary monetary policies, such as lowering interest rates or implementing quantitative easing.

Q7: Can a depression lead to inflation? A7: A depression could potentially lead to deflation due to lower demand. However, the economic policy responses to a depression, such as increasing the money supply or government spending, could eventually lead to increased inflation.

Q8: How does a recession affect inflation? A8: A recession typically leads to lower inflation or even deflation. This is because, in a recession, the demand for goods and services falls, which can lead to lower prices. However, the specific impact on inflation can vary depending on the nature and severity of the recession, and the policy responses to it.

Q9: What role do central banks play in managing the economy through these cycles? A9: Central banks play a crucial role in managing the economy through inflation, recession, and depression. They often use tools like interest rates and open market operations to influence the money supply, aiming to stabilize prices and maintain low unemployment rates.

by Sarah Bauder | May 11, 2022 | CPI, Inflation

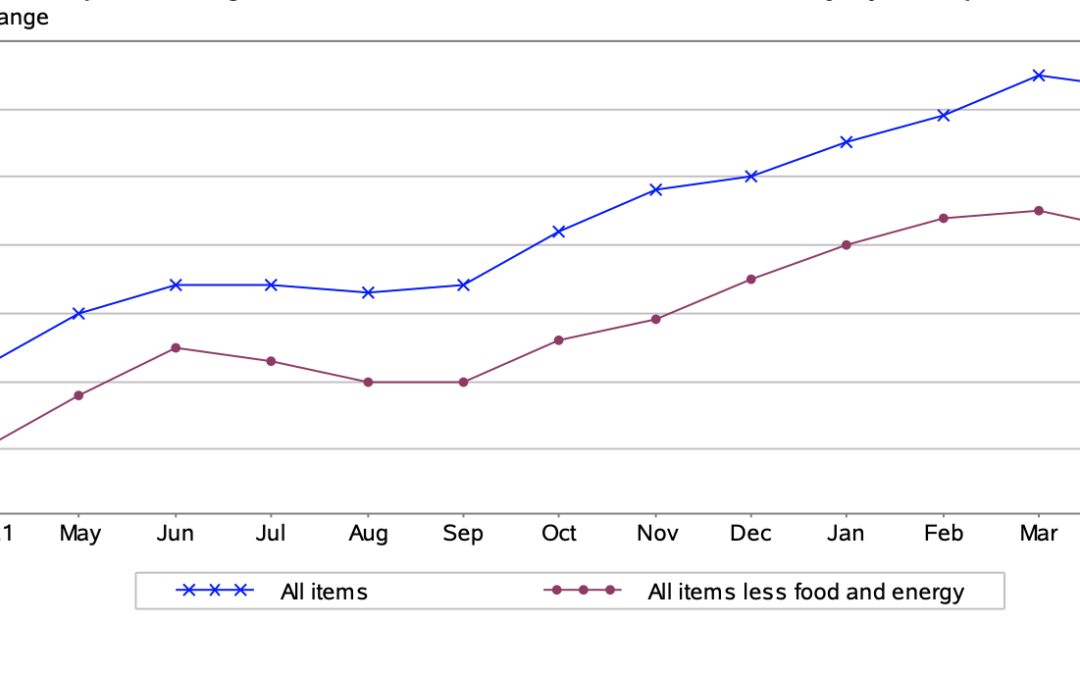

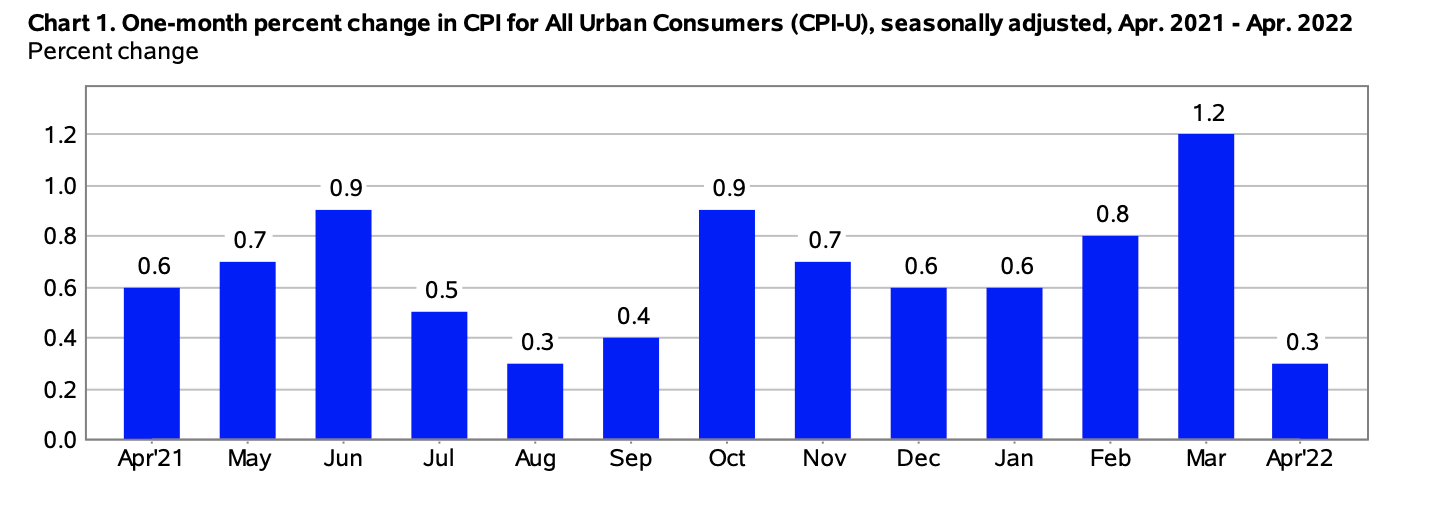

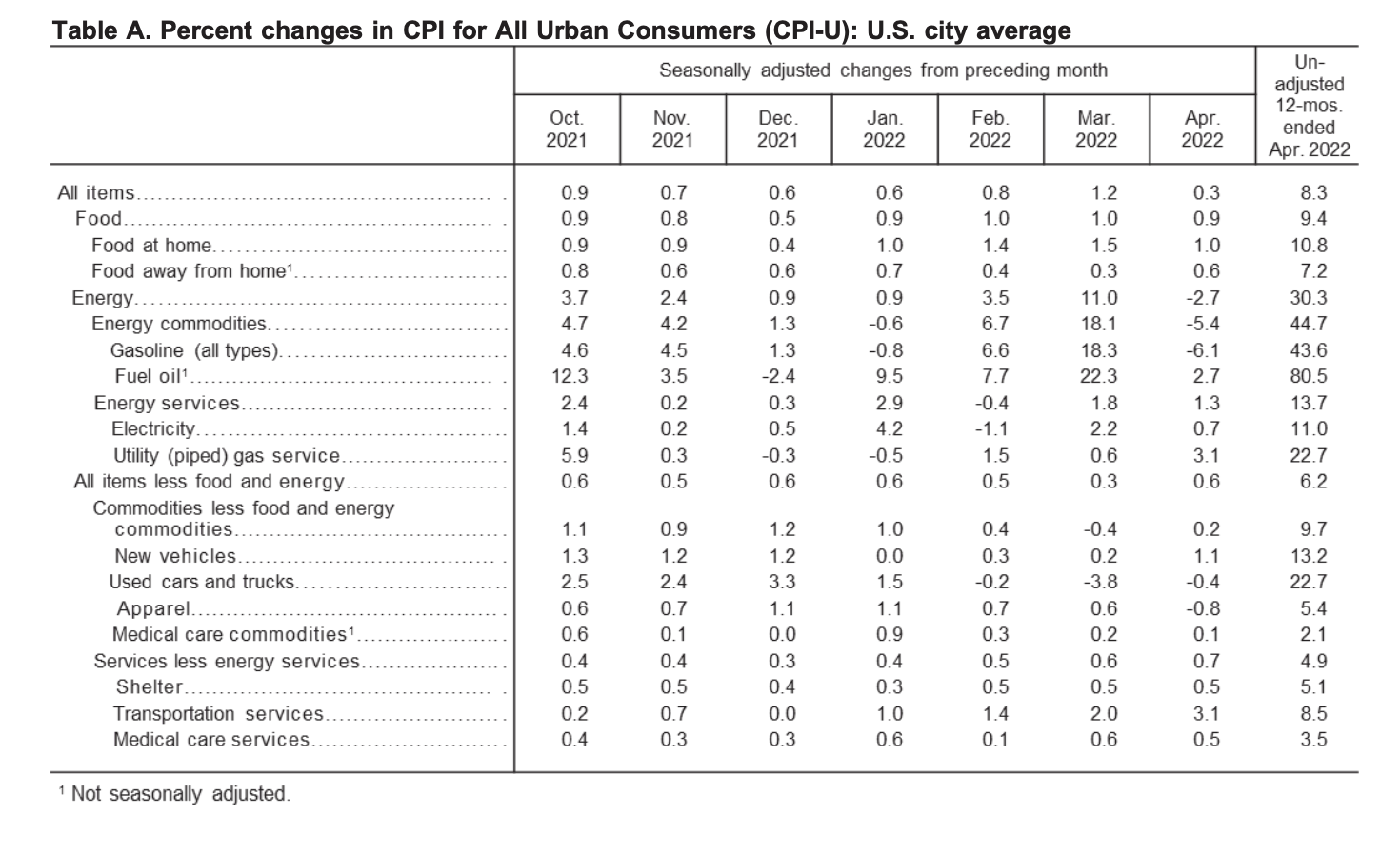

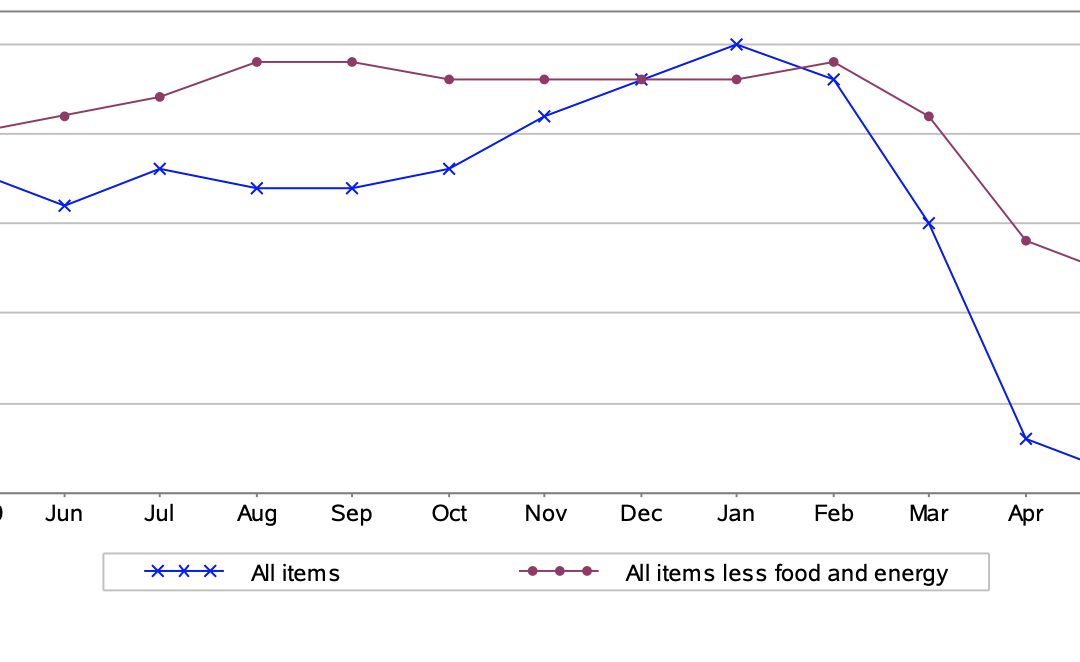

The Consumer Price Index for All Urban Consumers (CPI-U) rose by 0.3% on a seasonally adjusted basis in April, reported the U.S. Bureau of Labor Statistics. Since this time last year, the all items index grew by 8.3% prior to seasonal adjustment.

“Increases in the indexes for shelter, food, airline fares, and new vehicles were the largest contributors to the seasonally adjusted all items increase. The food index rose 0.9 percent over the month as the food at home index rose 1.0 percent. The energy index declined in April after rising in recent months. The index for gasoline fell 6.1 percent over the month, offsetting increases in the indexes for natural gas and electricity.

The index for all items less food and energy rose 0.6 percent in April following a 0.3-percent advance in March. Along with indexes for shelter, airline fares, and new vehicles, the indexes for medical care, recreation, and household furnishings and operations all increased in April. The indexes for apparel, communication, and used cars and trucks all declined over the month.

The all items index increased 8.3 percent for the 12 months ending April, a smaller increase than the 8.5-percent figure for the period ending in March. The all items less food and energy index rose 6.2 percent over the last 12 months. The energy index rose 30.3 percent over the last year, and the food index increased 9.4 percent, the largest 12-month increase since the period ending April 1981,” stated the Bureau of Labor Statistics in its monthly report.

(Source: U.S. Bureau of Labor Statistics)

Food

The index for food rose by 0.9% in April, marking the seventh consecutive monthly rise in this index. The food at home index saw a 1% for the month, with five of the six grocery store food composite indexes all experiencing percentage increases.

The food at home index rose 10.8% over the last 12 months, the largest 12-month increase since the period ending November 1980. The index for meats, poultry, fish, and eggs increased 14.3% over the last year, the largest 12-month increase since the period ending May 1979. The other major grocery store food group indexes also rose over the past year, with increases ranging from 7.8% (fruits and vegetables) to 11% (other food at home).

The index for food away from home rose 7.2% over the last year. The index for full-service meals rose 8.7% over the last 12 months, the largest 12-month increase since the inception of the index in 1997. The index for limited-service meals rose 7% over the last year, while the index for food at employee sites and schools fell 30%, reflecting widespread free lunch programs,” explained the bureau.

Energy

The index for energy decreased 2.7% in April, after soaring 11% the previous month. Gasoline prices dropped 6.1% after leaping 18.3% in March. Composite energy indexes all saw percentage rises including the natural gas index by 3.1% and the electricity index by 0.7%.

“The energy index rose 30.3% over the past 12 months. All the major energy component indexes increased over the year. The gasoline index increased 43.6% and the fuel oil index rose 80.5%. The index for electricity rose 11%, and the index for natural gas increased 22.7% over the last 12 months,” explained the Bureau of Labor Statistics.

(Source: U.S. Bureau of Labor Statistics)

All Items Less Food and Energy

The all items less food and energy index grew 0.6% in April. The index for shelter rose 0.5%. The index for rent increased 0.6% and the owners’ equivalent rent index increased by 0.5%.

“The index for all items less food and energy rose 6.2 percent over the past 12 months. Virtually all major components have increased over the span. The shelter index rose 5.1 percent over the last year, and the medical care index increased 3.2 percent. Several transportation indexes show notable increases including used cars and trucks (+22.7 percent) and new vehicles (+13.2 percent). The index for airline fares rose 33.3 percent over the last year, the largest 12-month increase since the period ending December 1980,” stated the bureau in its report.

Source cited: https://www.bls.gov/news.release/archives/cpi_05112022.htm

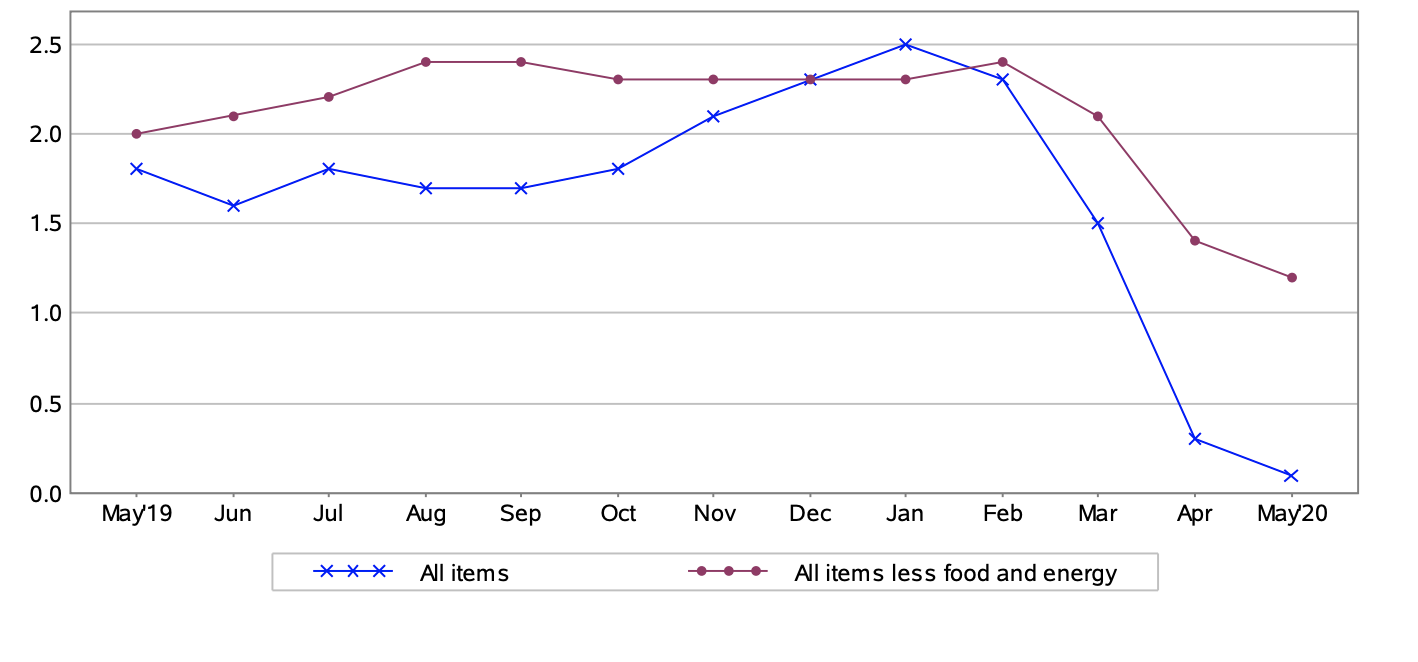

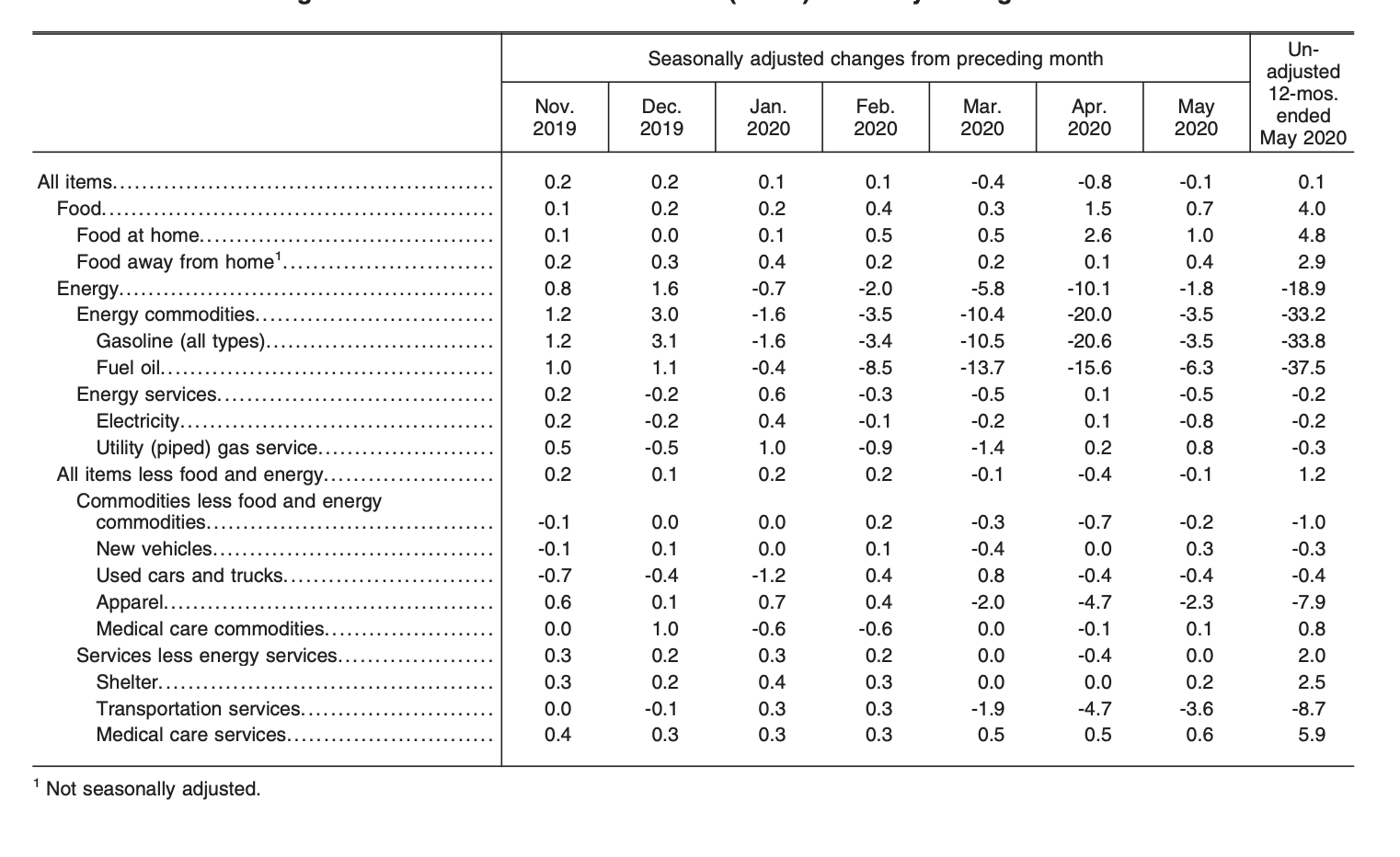

by Sarah Bauder | Jun 10, 2020 | CPI, Inflation

The Consumer Price Index for All Urban Consumers (CPI-U) dropped 0.1% in May, after plummeting 0.8% in April, reported the US Bureau of Labor Statistics. This percentage is on a seasonally adjusted basis.

The all items index has edged up 0.1% before seasonal adjustment, over the past year.

(Source: US Bureau of Labor Statistics)

Energy Index

The index for energy dropped 1.8% in May, after plunging 10.1% in April (which marked the steepest monthly decline for the index since November 2008). Gas prices dropped 3.5% in May, after plunging 20.6% in April. The index for electricity also decreased 0.8%, which was the largest one month drop since May 2015, stated the US Bureau of Labor Statistics. Conversely in May, the natural gas index increased by 0.8%.

Overall over the last 12-month period, the index for energy declined 18.9%, with all major energy indexes seeing significant decreases. Gas prices plunged33.8%, and the fuel oil index likewise plummeted 37.5%. In addition, the natural index fell 0.3%, and the electricity index dropped 0.2% over the past 12 months.

Food Index

In May, the food index rose by 0.7%. The increase was contributed to the 3.7% rise in the index for meats, poultry, fish, and eggs, stated the US Bureau of Labor Statistics. Additionally, the bureau reported that the beef index soared 10.8% in May, marking the largest monthly increase of the index since records have been kept.

Over the last 12 months, the food at home index has risen 4.8%. The index for meats, poultry, fish, and eggs rose 10% since this time last year. This marks the steepest 12-month rise in this index since May 2004, reported the bureau.

(Source: US Bureau of Labor Statistics)

All Items Less Food and Energy Index

In May, the all items less food and energy index dropped 0.1%. Component indexes all saw declined including motor vehicle insurance by 8.9%, the apparel index by 2.3%, and the airline fare index by 4.9%. Conversely, the shelter index increased by 0.2%, as did the medical care index by 0.5%.

Over the last 12-month period, the index for all items less food and energy increased by 1.2%. The index for shelter edged up 2.5%, as did the medical care index by 4.9%. Component indexes that saw major decreases were the airline fare index by 28.8% and motor vehicle insurance by 14.3%, reported the US Bureau of Labor Statistics.

Source cited: https://www.bls.gov/news.release/archives/cpi_06102020.htm

by Sarah Bauder | Jan 8, 2020 | Inflation

By definition, inflation is the general increase in the price of goods and services, and the decrease in the purchasing value of a nation’s currency. Inflation is measured in the consumer price index (or simply CPI), which in turn, calculates the value of a basket of consumer and services purchased by the average household. In this article, 5 experts discuss things you didn’t know about inflation.

I Think A Lot Of People Don’t Really Think About Inflation And Their Money Losing Buying Power

“I think there’s a lot of people out there who either just don’t know about inflation period, or don’t think about it. We all intuitively know things get more expensive over time. A Subway Foot Long used to be $5, now its $8 or $9, things go up in price but I think a lot of people don’t really think about inflation and their money, losing buying power.

I was recently talking to a family friend who left a job of 20 years. They had something like 18k in their retirement account despite making a very good living and having been there 20 years. On the other hand I had been at a much lower paying job for something like 5 years and had over 25k in my 401k. It turned out this family friend wasn’t investing, they were just letting money sit in their retirement account because they were scared of risk and scared of investing. I was trying to explain to them that while all investments have risk, what he’s doing now is guaranteed to lose him money through inflation and over time a pretty substantial amount of money. He didn’t seem to get it and continues to let his retirement money just sit and lose over time.”

John Frigo, Digital Marketing Lead, My Supplement Store

The Word “Inflation” As Originally Coined Applied Entirely To The Quantity Of Money

“The average American does not know or appreciate that the word ‘inflation’ as originally coined, applied entirely to the quantity of money. That is to say, inflation is merely an increase in the quantity of money and bank notes that are in circulation plus the quantity of bank deposits that are subject to check. As such, current operations by Central Banks around the world that electronically create ‘money’ or ‘reserves’ through open market operations and programs such as ‘quantitative easing’ are themselves sufficient to satisfy the original definition of ‘inflation’, even if there is no measurable increase on the price on consumer goods.”

David Reischer, Esq. Banking & Business Attorney, LegalAdvice.com

The Average American Has A Hard Time Even Describing What Inflation Is

“The average American attending my workshops on the basics of personal and household finances knows that inflation is something that can hurt their wallet, but they have a hard time even describing what inflation is.

Many people accept that inflation results in higher prices for goods and services, but they do not understand it as an annual change. Rather, they think of it like they would a sales tax, like something added onto the normal price of goods and services.

The average American knows that prices for gasoline, food and cars were much lower when they were younger, but there is a disconnect between the change in prices and the principle of inflation.

The simplest description of inflation I see my adult students understanding is this: You know how prices seem to go up year after year? That is inflation.

Most adults in my classes typically guess that inflation is far higher than it is, believing it is close to 10% a year rather than the 2.5% to 3.5% rate is has been for the past couple decades. However, even at 3.5%, they do not understand that prices will actually DOUBLE in just twenty years. The Rule of 72 is a powerful tool for teaching about the impact of inflation over time.”

Todd Christensen, Education Manager, Money Fit by DRS

The Correlation Between Interest Rates And Monetary Inflation

“Very few people understand the correlation between interest rates and monetary inflation. When interest rates are suppressed below the GDP rate, which is a reflection of economic output, then interest rates anywhere in the interest curve below this rate results in people being paid to borrow. This is because the rate of interest is below the rate of monetary inflation and thus people are encouraged to expand in ways that are not necessarily economic. To that end, assets that are tied to the interest rate complex largely rise in price as interest rates are lowered.

While the apparent gains in value for assets tied to interest rates like real estate, bonds, commodities, collectibles, may seem engendered by real market demand, in most cases the demand is artificially being created by inflation tied to below market price interest rates. Central Bank meddling in the pricing mechanism for interest rates, which some would say is the most important price in a free market, distorts all markets and that’s why many assets are highly susceptible to the boom-bust cycle of bubbles.”

Brian Ma, Broker, Flushing Real Estate Group

Investing In Real Estate Is The Best Hedge Against Inflation

“One of the most important things which the average American does not know about inflation is that investing in real estate is the best hedge against it. While people are generally aware of the many benefits of real estate investments such as relatively low risk and monthly rental income, they often fail to appreciate the fact that investing in real estate properties protects one’s money against inflation. While housing markets take temporary downturns as a result of economic and demographic factors, they always bounce back. Regardless of which market you look at, real estate prices follow an upward trend in the medium and long term. This is due to the constant increase in housing demand (due to population growth) and the fact that the land on which properties are built is a very limited resource. If we look at data from the past few decades, the average annual appreciation rate in the US exceeds the average annual inflation rate. In 2020 inflation in the US is forecast to reach about 2%, while the increase in the median home value is expected to reach about 2.2%. This means that once again the real estate appreciation rate will exceed the inflation rate, offering investors protection of their financial resources.”

Daniela Andreevska, Marketing Director, Mashvisor

Unfortunately, inflation is an economic reality that is unavoidable. You can keep abreast of the monthly inflation rates and the CPI via the Bureau of Labor Statistics release schedule. The best strategy to hedge against inflation is to ensure that one has a diversified portfolio.