by Sarah Bauder | Dec 3, 2019 | Inflation

Inflation is a general increase in the price of goods and services, and a decline in the value of a nation’s currency. Conversely, deflation is a decrease in the price of goods and services, when the rate of inflation falls below 0%. Additionally, the purchasing power of a nation’s currency will increase during deflation. Inflation is measured by the consumer price index (CPI). The CPI measures the changes in the value of a basket of consumer goods and services purchased by households. In this article, financial experts share their views on whether or not investors should be worried about inflation and deflation.

This Inflation Or Deflation Debate Mixes A Lot Of People Up Because The Same Causal Forces Can Potentially Lead To Both Scenarios

“This inflation or deflation debate mixes a lot of people up because the same causal forces (such as high debt levels) can potentially lead to both scenarios depending on the policy response.

When analyzed in isolation, the current macro environment is deflationary. Debt levels as a percentage of GDP are beyond the point of sustainability, and aging demographics lead to slower economic growth and a larger financial burden on younger generations, leading to high default risk over the next decade. Debt defaults involve the destruction of both liabilities and assets; other peoples’ money, which makes this an extremely deflationary prospect.

However, there is virtually no way that the global financial system, as currently structured, would allow a deflationary debt default to occur in countries that control their own currencies. Historically, the policy response to economic environments with this high of a debt load is for governments and central banks to print their way out of it. In a purely fiat system, there’s nothing stopping financial authorities from increasing the money supply to pay all obligations in nominal terms, even if it causes inflation and fails to pay back those obligations in true purchasing power terms.

Therefore, a deflationary or dis-inflationary environment is possible in the intermediate-term, but an inflationary outcome is almost inevitable over the long term due to the policy response to those deflationary or dis-inflationary forces. Rarely in history do fiat monetary systems allow themselves to default nominally.”

Lyn Alden, founder of Lyn Alden Investment Strategy

Looking Forward Over The Next 12 Months We Do Expect A Dip In The Markets And Some Inflation

“In an inflationary environment the value of money decreases, which spurs consumption and investment. Deflation makes it profitable to simply sit on one’s savings while the value of those savings increases without any special effort, disincentivizing consumption and investing.

Looking forward over the next 12 months we do expect a dip in the markets and some inflation. Therefore we are therefore poised and ready for investment opportunities that may crop up over this period.”

Robin Lee Allen, Managing Partner, Esperance Private Equity

The Commonly-Cited CPI Metric Might Not Be The Best For Practical Purposes

“Sensing you will likely receive numerous responses to your prompt declaring whether investors should worry about potential inflation or deflation, I thought I would offer up a viewpoint about why the commonly-cited CPI metric might not be the best for practical purposes.

The Consumer Price Index (CPI) has long served as the foundational inflation measure for economic activity. In fact, it underpins the health of an economy because a stable CPI measure indicates opportunity for economic prosperity. Absent predictable CPI readings, consumers will not have an accurate signal about price expectations and may change their behavior in detriment to the economy as a whole.

One major limitation to the current CPI measure is its inability to incorporate decisions consumers might actually make when evaluating a fixed basket of goods. For example, when a price increases for one consumer product included in the selection of goods used to measure CPI, many consumers would choose to switch to a substitute. CPI doesn’t account for this reality. Instead, CPI assumes the consumer would simply pay more for the same product. Reality usually shows a different response in the form of choosing a substitute product.

Instead, a better measure, which accounts for this substitution effect would be “chained CPI.” This more closely resembles the substitution decisions consumers would make in response to rising prices of certain items as opposed to simply paying more for the same good. This metric will capture the switching dynamic.”

Riley Adams, CPA

A Cost-Averaging Strategy Into A Healthy, Low-Cost, Diversified Stock Portfolio

“For anyone investing in their future over the long term, they know that everything moves through cycles. There are booms, and there are recessions. Sometimes the latter morph into depressions. And inside these, there are deflationary and inflationary times. Piecing it all together, unless you are an econometric expert, is almost impossible.

The problem is that events in the economy can move fast between inflationary and deflationary forces. Reaction time can be a severe challenge. For the everyday, hard-working American who puts some earnings aside at the end of every month and religiously injects it into a portfolio, keep it up. By cost averaging over time, you automatically smooth out the many ragged edges and the volatility shocks. Then, my recommendation is to invest it in the S&P 500 (a low-cost fund) that evenly spreads every invested dollar over the public markets’ best stocks. By so doing, you are trusting growth stocks and companies immersed in unearthing and refining commodities like gold and platinum (inflationary hedges). Also, defensive stocks like businesses in consumer goods, and well-known dividend-paying stocks (deflationary hedges). You may want to put a small percentage outside the S&P 500 fund into Treasury Inflation-protected treasuries, investment bonds, and keep some cash on hand (both deflationary protectors).

In short, I recommend a cost-averaging strategy into a healthy, low-cost, diversified stock portfolio as the spearhead of a balanced approach to counteract market ups and downs, rollicked by inflation and deflation from within.”

Gordon Polovin, finance expert, serves on the advisory board for Wealthy Living Today

It’s Definitely Something That People Should Be Concerned About

“Central Banks around the world have a target to keep inflation at roughly around 2% (depending on the country this can be higher or lower). Anything more or less than that can be harmful to the economy. If the inflation is too high, prices of goods and services will rise sharply, and the value of cash or bonds will fall. This has happened numerous times in countries like Germany (after the war), Argentina, Zimbabwe etc. Things can get so bad sometimes that prices double every few hours! This is called hyperinflation and Zimbabwe eventually ended up abolishing its currency and instead using foreign currencies as legal tender! Inflation that is too low or negative (deflation) is equally dangerous. It essentially means that good and services will be cheaper tomorrow than they are today. This incentivizes hoarding of cash. With less demand, economic growth slows down and businesses begin to suffer. Inflation levels also impact export competitiveness compared to other countries, foreign investments and can also impact the value of personal or national debts. It’s definitely something that people should be concerned about which is why Central Banks have set targets in the first place.”

Gaurav Sharma, Founder at BankersByDay

Deflation Can Mean A Drop In Wages Or A Drop In Market Prices

“Deflation can mean a drop in wages or a drop in market prices. Not everyone experiences these drops equally and those who are already secure in a higher paycheck won’t notice either of these factors. However, those who are at the bottom of the business have something to worry about. They are likely to experience a cut in hours or a cut in pay, meaning that while they might notice a drop in market prices, they won’t have the additional income to appreciate it. It’s also important to consider that people are constantly looking for a better deal. In the hopes of finding this deal, people will often stop buying and wait. This can cause a dip in sales and cause trouble with the economy.

Inflation doesn’t necessarily make people secure, however. Inflation means a bump in prices, meaning that the dollar in your pocket is worth less than it was before inflation. Now your paycheck doesn’t go as far and you’re concerned about that. You’ll have less for superfluous spending. You’ll hold onto what little wealth you have and as a result the economy will start to dip.”

Chane Steiner, CEO, Crediful.com

The Outlook Right Now Looks Like One Of Slower Inflation And Because Of That The Risk Of Deflation Is More Of A Concern Now

“Currently the outlook right now looks like one of slower inflation and because of that the risk of deflation is more of a concern now than that of inflation. There are a number of reasons for slower inflation including an aging demographic, technology advancement, inflation expectations, and a stronger dollar. Studies have shown that the aging of demographics has a negative correlation for inflation. In other words, that as a population ages, inflation starts to fall. A good example of this would be Japan, which has battle very low inflation for around the last 25 years. Technology advancement has brought down the price of goods that use new technologies intensively. Historically there has been a correlation of higher productivity with lower inflation. Productivity has been lower recently ,so unless this changes this could be a reason why we start to see inflation rise.

Next, inflation expectations is an important factor in inflation. The higher people think prices are going to go, the more workers will want higher wages, and the higher businesses will believe their costs, and the prices they can charge, will rise. The opposite is true as well, as we are currently seeing inflation expectations from that of the University of Michigan as well as the break-even inflation rate set in Treasury inflation-protected securities. Finally, the stronger dollar leads to lower inflation. This happens because a strong dollar makes foreign imports cheaper which in turn result is cheaper products at U.S. stores, and those lower prices translate to low inflation. So, in order to see the inflation outlook change, we would need to see changes in these factors in order to make that happen.”

Scott Pederson, Financial Advisor, Harmony Wealth Managment LLC

Investor Should Be Worried About Inflation And Deflation

“Yes, the investor should be worried about inflation and deflation. These both are the major economic factors, and investors should keep them in mind before investing money.

Inflation means the increase in the price of products and a decrease in the value of money value. Regarding this basic rule, investors should invest in products whose return or profit margin would be higher than the inflation rate. For example: If the investor is investing $100 and is expected to get $2 profit next year. He must see what would be the inflation rate. If it would be 3%, then the investor is at a loss of $1.

In times of deflation, investors should preserve the capital or invest in the good having the high return potential in the future. Investment in gold is recommended because no matter what, even after a minimal decrease, its prices go high. So, the rule of thumb is either to preserve the capital or invest it in the products with the potential of higher ROI. Business bankruptcy rates increase during this period. So, do not keep your stock shares or corporate bonds in the companies having the risk of bankruptcy. Instead, invest them in potential business or goods to remain on the safe side. “

CJ Xia, VP of Marketing & Sales at Boster Biological Technology

Both Have Negative Consequences

“Generally, as the economy recovers, banks are able to loan out their excess reserves to the public. With the increase in money supply, inflationary pressure is also built, causing the prices of goods and services to rise. This worries ordinary citizens, especially those who live pay check-to-pay check because the affordability of basic goods and services is more difficult.

On the other hand, deflation impacts consumers by way of raising their purchasing power since goods and services have become more affordable. But while this may be good news to the public, the same thing cannot be said for enterprises who are affected by the low prices of their goods and services. Eventually when deflation persists, they will be forced to cut jobs and shut down. The public then experiences decline in incomes and therefore, consumer confidence plunges.”

Doug Keller, Writer, Finance Fox

Both inflation and deflation are economic components that unfortunately cannot be avoided. Keep up with monthly inflation rates and the CPI via the Bureau of Labor Statistics release schedule. In order to offset the market ups and downs during periods of inflation and deflation, a diversification strategy for one’s portfolio is the best bet.

by Sarah Bauder | Oct 14, 2019 | Inflation

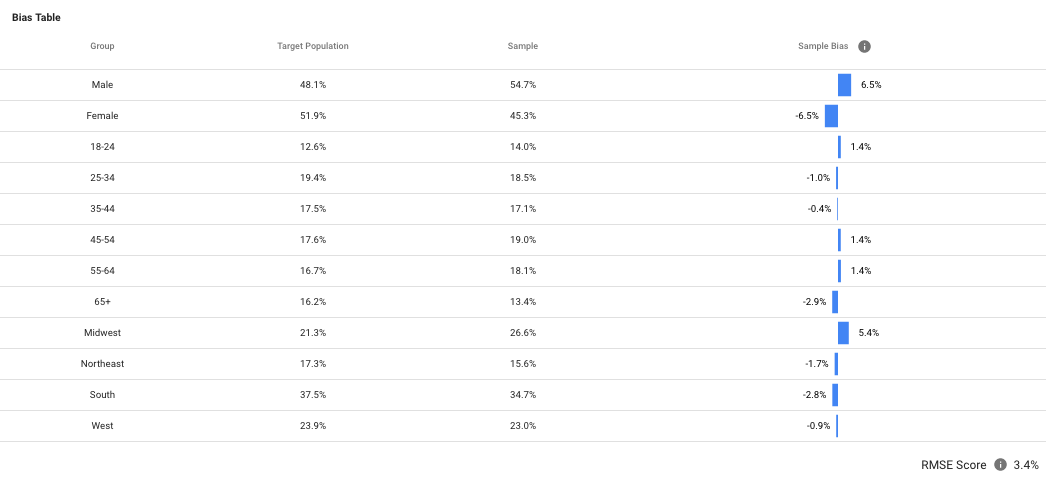

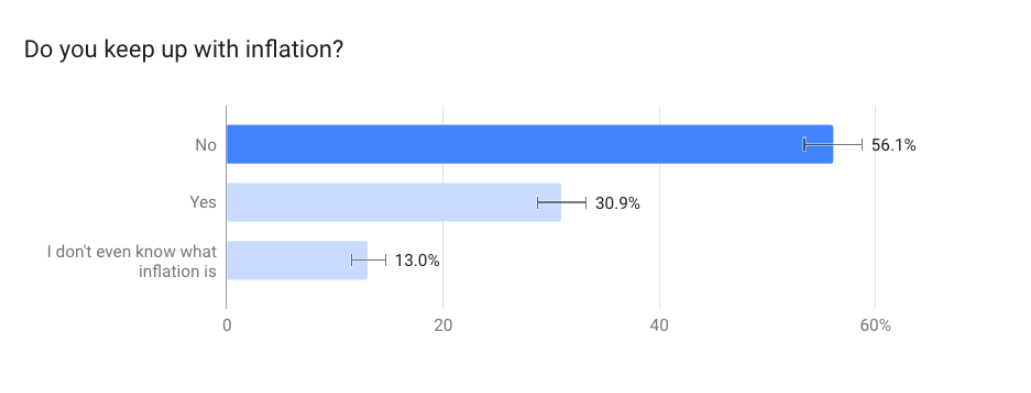

We conducted a survey asking 1,500 US respondents whether or not they kept abreast of inflation. We used Google Surveys and targeted males and females between the ages of 18 to 65+ from coast to coast. We asked the following question with three possible responses:

Do you keep up with inflation?

- No

- Yes

- I don’t even know what inflation is

The Average American Woman Does Not Keep Up With Inflation, Especially 18 to 24-year-olds

The overwhelming response of Americans, who took part in the survey, indicated that they did not keep up with inflation. A full 56.1% chose this response.

When demographic filters were applied to the survey results factoring females, very compelling insight was discovered. The percentage leaped to 63.6% and skyrocketed to an astounding 75.1% of females between 18-and 24-years-old.

Conversely, when demographic filters targeted specifically males, 48% stated that they did not keep abreast of inflation. Of the males between 18 and 24 who responded to the survey, 59.8% chose this option.

One possible explanation for the drastic variance of the percentage between genders could be the finance sector. Although blessedly changing, positions across the spectrum of finance and business have typically been held by males – thus, making a larger percentage of males more inclined to keep up with inflation.

Males Are More inclined To Keep Abreast Of Inflation, Especially Middle-Aged Males

The second most popular response to the survey was 30.9% of respondents indicated that they did, in fact, keep up with inflation.

Yet, when demographic filters were applied focusing specifically on gender, 38.9% of male respondents stated that they kept up with inflation, while conversely, 23.5% of female respondents selected the same option.

When the demographic filters targeted middle-aged males between 45 and 64-years-old, the results soared to 42%. Because almost half of this cohort indicated that they kept up with inflation, they have the highest percentage of respondents who answered “yes” to the survey question.

These results could further be demonstrative of the fact that males, especially middle-aged males, populate a higher percentage of positions across the spectrum of finance and business, which would warrant them keeping up with inflation.

American Women Between 25 and 34-years-Old Indicate That They Don’t Know What Inflation Is

Of the American respondents who participated in the survey, 13% indicated that they didn’t even know what inflation was.

Yet, interesting insight was discovered when demographic filters were applied to the results, targeting specifically gender. 13.1% of male respondents indicated that they did not know the definition of inflation, while 12.9% of female respondents chose the same response.

However, when demographic filters focused specifically on females between 25 and 34-years-old, 18.6% of this age bracket indicated that they didn’t know what inflation was. Thus, it was the second most popular response to the survey question for this demographic.

Conclusion

Based upon the results of this survey, more than half of all Americans who responded did not keep abreast of inflation. Although a higher percentage of males who participated indicated that they did not know the definition of inflation, the highest percentage of respondents who did not know what it was were females aged 25 to 34. Yet, males, especially middle-aged males, were more inclined to keep up with it. This could be explained by the fact that as a generalization, jobs within areas of finance and business which would necessitate keeping abreast of inflation, are typically dominated by males.

Details About The Study And RMS Score

by Sarah Bauder | Aug 28, 2019 | Inflation

Annuities are a popular insurance contract that provides guaranteed returns for a set period or for a lifetime. In this article, financial experts discuss whether or not annuities represent a good investment for inflation protection.

Carefully Evaluate Any Annuity And Pay Special Attention To The Inflation Riders And How It is Calculated

“Single-Premium Annuities are not designed to be inflation protection, they are insurance product designed so that you don’t run out of money. Annuities are simply a promise to pay you and income for the rest of your life how long or short that may be. Annuity companies usually offer the opportunity to purchase or not purchase an inflation rider when you purchase one of these contracts. An annuity is not really an investment to protect against inflation because your actual return, that is how many and long you receive payments- is primarily delivered by how long you live!

An inflation rider might be purchased and in this case, inflation might outpace the contract terms and your payment would be adjusted upwards to keep up with the rising costs of goods and you would see your real income keep up with the rising costs. Inflation may be similar to historical averages and your income would be similar throughout the term of the contract.

Currently, we are at near-historic low rates of in inflation and if an example consumer purchased an SPIA and then saw a run-up in inflation, the real income of the annuitant could be significantly reduced. Inflation may be very low and you may have paid a premium for inflation protection, but if the inflation rate was very low you may have been better off not purchasing the option.

This only covers single-premium annuities, there are also period certain annuities, return of premium annuities and many more. The main point is to carefully evaluate any annuity and pay special attention to the inflation riders and how it is calculated, as well as understand the pros and cons of

the contract you are evaluating.”

Jason B. Ball, CFP®, ChFC®, CLU®, Ball Comprehensive Planning, LLC

When Setup Properly Annuities Can Provide A Lifetime Income Stream

“I am an independent insurance broker specializing in annuities – and yes – I believe annuities are a good investment.

When setup properly, annuities can provide a lifetime income stream for individuals and couples. That income stream can also increase each year based on moves in the CPI index. And once the income stream increases, it can’t go back down.

A guaranteed lifetime income annuity that increases payments based on moves in the CPI (or other inflation indexes) can be a valuable piece to any retirement plan. It acts as a pension plan and can reduce the financial strain that comes along with the overall market volatility we’ve experienced the last decade and a half.”

Adam M. Hyers, President, Hyers and Associates, Inc.

Annuities Are A Great Way To Make Sure Your Money Grows

“Annuities are a great way to make sure your money grows at a rate that outpaces inflation. Annuities are also often guaranteed not to go down when the market goes down. This means they are protecting you against losing everything in a crash as well, making them ideal for people who need to have a certain amount of money each month to live on when they are no longer working.”

Stacy Caprio, Financial Blogger, Fiscal Nerd

They Come With Several Costly Caveats That Do Not Make Them Worthwhile For Most Investors

“Annuities are not a great buffer against inflation. They provide guaranteed returns, but they come with several costly caveats that do not make them worthwhile for most investors.

Annuities typically have several fees (including administrative or death benefit costs) associated with them above the cost of investment fund management fees. Inflation-protected annuities have additional fees for this benefit as well.

Annuities payments are not guaranteed. If the insurance company an investor purchased from goes bankrupt, it is possible that the individual might lose their payments.

If the investor decides they no longer want to the annuity, there is usually a penalty fee to cancel it and withdraw the money.

In general, a better strategy would be to invest in low-fee options that return healthy dividends. Over time the stock market historically outperforms what an annuity can offer, so investors with many years to go will do much better putting their available funds into 401K and IRA options than to purchase annuities now.”

Isaiah Goodman, Becoming Financial

Good Investment For Inflation Protection But Should Not Be Used As Pure Inflation Protection Vehicles

“Annuities can be a good investment for inflation protection but should not be used as pure inflation protection vehicles. They should only be used as inflation protection vehicle if the investor has an additional concern such as running out of money too quickly, having a stable income for peace of mind, or having some form of downside protection. Most annuities offer a cost of living adjustment rider which allows the income to scale based on one of the economic inflation metrics. However, annuities are primarily insurance for running out of money too fast. The way this happens is that you either live too long, you can’t budget to save your life, or you panic every time the market gets volatile.

If you don’t think you experience one of these core problems than there are a variety of better investments, you can make to protect your self from inflation concerns. If you are conservative in nature you can buy Treasury Inflated Protection Securities. Not only are they guaranteed by the federal government, but they are very stable investment. Their payments adjust directly based on inflation, so it is a direct hedge for inflation. However, if you want the best inflation-adjusted investments then look no further than the stock market. Equities are the best available investment when it comes to inflation. The cost of your day to day goods will directly be represented in the cost of goods these companies sell.”

Alex Caswell, CFA CFP, Wealth Planner, RHS Financial

Annuities Are A Very Misunderstood Product

“Annuities are a very misunderstood product. Annuities are a popular choice for investors who want to receive a steady income stream in retirement. There are different types of annuities that can play a beneficial part in anyone’s holistic strategy. As an industry professional, I believe that annuities serve a purpose for anyone, and can’t fall into a lump-sum of good or bad.”

Danita M. Harris, Managing Member, Guice Wealth Management

Fixed And Indexed Annuities Will Almost Certainly Beat Inflation With No Risk Of Loss

“Most long-term instruments will likely beat inflation, and therefore are good for inflation protection; however, most individuals who are looking for inflation protection are also just as concerned with the safety of principal and long-term liquidity. Fixed and indexed annuities will almost certainly beat inflation with no risk of loss, offering significantly higher interest rates than most fixed instruments. Additionally, annuities are tax-deferred, resulting in an even higher effective rate of interest. Once the surrender period has expired (usually between about five and ten years), most annuities are completely liquid provided the account owner is age 59.5 or older, unless of course, the account is annuitized (set to pay out a guaranteed income stream, usually for life or beyond).”

Rob Drury, Executive Director, Association of Christian Financial Advisors

It Depends What Type Of Annuity You Choose To Invest In

“I think it depends on what type of annuity you choose to invest in. Inflation can be unpredictable, and since annuities tend to be long-term investments, they may not be the best way to protect your finances from inflation. Even in a fixed annuity, you would guarantee the same amount of capital in return, but inflation could potentially negate any capital gains from this type of investment.

However, you could take out an immediate annuity that would start paying out in the short-term, making it a very viable option. This way you could start receiving your investment in small parts over the course of time, which is better than receiving a lump sum in the distant future. Smaller short-term capital gains will help you hedge against rising inflation, and you can always halt your annuity in the event inflation rises unexpectedly in the future.”

Igor Mitic, Co-Founder, Fortunly.com

It Is Generally Not The Top Of Mind Reason One Would Purchase An Annuity

“Annuities CAN have a place in someone’s overall financial planning for part of someone’s overall assets. Inflation protection could be a component of the reason why one would purchase an annuity, although the more common reasons found involve potential guarantees of income for life and the death benefit…always for additional fees. There are step-up features whereby the income benefit base steps up each year, or where the death benefit base steps up annually…or both. The increasing income base can mitigate the effects of inflation, depending on the specifics of the particular feature. There is not a one-size-fits-all, in that annuities can be tied to the stock market [variable annuity], a fixed rate of return [fixed annuity], or tied to an index [indexed annuity]. The fees can vary depending on the insurance carrier and the ancillary benefits purchased. The distribution options can vary as well, depending on the income need. All of that said, while inflation protection can be a component of the features of an annuity, it is generally not the top of mind reason one would purchase an annuity.”

Jimmy Masters, AIF(r), CRPS(r), Vice President – Investments, The Alcaraz Fisher Justis Wealth Management Group of Wells Fargo Advisors

Although annuities provide guaranteed payments to investors, there is no overall consensus as to whether or not they provide good inflation protection. If you are thinking about investing in annuities, take into account what the financial experts have discussed in this article, and always do your due diligence.

by Sarah Bauder | Aug 28, 2019 | Inflation

Inflation protected bonds, or more specifically, Treasury inflation protected securities (TIPS) are Treasury bonds designed to protect against inflation. The principle of TIPS rises with inflation, and pays interest twice a year, at a fixed rate. In this article, industry experts discuss specific things investors should know about inflation protected bonds.

Best For Savings Not Investment

“Treasury inflation protected securities are meant to help protect your principal amount from the effects of inflation. Your invested amounts are adjusted regularly in accordance to changes in the consumer price index – the official inflation indicator in the country. And the inflation-adjusted principal amounts will be used to determine your possible interest earnings. Some important things to note about TIPS include:

It pays less than ordinary government securities: You can expect the interest rate for TIPS to be a few points below that of ordinary bills and bonds. But a TIPS holder stands to benefit in two ways; one is through regular principal amount adjustments in accordance with CPI changes and the second in form of the agreed interest.

Inflation is currently not an issue: TIPs is supposed to caution you against volatile changes in inflation like in the case of 2007/8 economic downturn when the purchasing power decreased by 3.84%.

The Treasury Direct account can be cumbersome: Unlike stocks, you can buy

TIPS directly from the government through a Treasury direct account. But I believe you are better off using a TIPS fund for two reasons. The managers are more experienced and therefore able to tell the best buys and also because it is more effective than using the sluggish Treasury Direct website.

Best for savings not investment: You are better off using TIPs for savings and not for investments because they post lower returns and are essentially designed to protect the principal amount from depreciating at the expense of earning solid incomes.”

Edith Muthoni, Chief Editor, Leanbonds.com

The Current Fed Policy On Interest Rates

“There is no doubt of an accelerating attraction to inflation-protected U.S. government bonds. The key to answering why this is occurring rests with the current Fed policy on interest rates. The facts are that the nominal and inflation-adjusted bond yields have dropped over the past 12 months (i.e., taking the 10-year U.S. government bond yields as an interest rate yardstick.) The economy is still chugging along in full-growth mode, thus exerting pressure on future yields and boosting bond prices still more. At the same time, the Fed’s go-to inflation gauge (measuring inflation over five years starting today) indicates an expected rate of just over 1.8%. We don’t expect the Fed to resume increasing interest rates until we see a small excess over the expectation. The scenario painted above points to inflation-protected bonds outperforming the categories with zero protection (i.e., nominal rate bonds). Even if reality overtakes expectations and the Fed pushes interest rates earlier than expected, inflation-protected bonds like TIPS (Treasury Inflation-Protected Securities) should continue to head the pack. The reasoning is that inflation will be back in play to spur the Fed’s change of direction, and therefore TIPS (indexed to the inflation rate) will continue to thrive. Either way, you are a winner in our view.”

Gordon Polovin, Finance Expert, Serves on the Advisory Board, Wealthy Living Today

These Types Of Investments Are Best Suited For Individuals Who Are In Or Approaching Retirement

“Treasury inflation protected bonds (TIPS) are designed to help investors protect against the effects of rising prices. These types of investments are best suited for individuals who are in or approaching retirement as they are a hedge against inflation and they provide the strongest bond hedge against default risk. TIPS also provide income in the form of coupon payments. These payments are generally paid semiannually and are based as a fixed percentage of the face value of the bond. The fixed-rate is applied to the principal, and like the interest payments, it can rise with inflation and fall with deflation. A couple of important things to note are that once TIPS mature, the investor will receive the greater of their original investment or the adjusted higher principal amount. Meaning the investor can’t lose money during a deflationary period. TIPS are best used in non-taxable accounts (Traditional or Roth IRA, etc.) because the increase in the bond’s value will cause a taxable event each year there is an increase.”

Jordan Sester, Founder/Investment Advisor Rep, J.S Financial Group

(Photo: Wikipedia)

You’re Better Off Owning Them In IRAs

“They’re not spectacular. Treasury inflation protected bonds TIPS are government bonds so there’s no default risk. The coupons are small. You run the risk of losing value if you sell prior to maturity. You will lose value in times of deflation. When the face value adjusts each year due to inflation it creates a taxable event. You’re better off owning them in IRAs where you won’t have to report taxes. They do hedge a risk.”

Chane Steiner, CEO, Crediful

Pay investors A Fixed Interest Rate As The Bond’s Par Value Adjusts With The Inflation Rate

“Treasury Inflation-Protected Securities (TIPS) are a form of U.S. Treasury bond designed to help investors hedge against inflation. These types of bonds are indexed to inflation, they have full faith and credit backing of the U.S. government. They pay investors a fixed interest rate as the bond’s par value adjusts with the inflation rate. TIPS pay interest at a rate that is fixed when the bond is purchased. Because the rate is applied to the adjusted principal, however, interest payments can vary in amount from one period to the next. The actual coupon payment (the amount of interest you receive), then, will fluctuate every six months, because it is calculated based on the new inflation-adjusted full value of the bond for the following year. One has to consider whether the variable income is a factor that fits their lifestyle, goals, and needs before purchasing.”

Jimmy Masters, AIF(r) CRPS(r), Vice President-Investments, The Alcaraz Fisher Justis Wealth Management Group of Wells Fargo Advisors

Inflation protected bonds protect investors from the negative effects of rising prices. As with any investment vehicle, there are advantages and disadvantages to investing in Treasury inflation protected securities. If you are interested in TIPS, factor in what these industry experts have discussed, and remember to do your due diligence.

by Sarah Bauder | May 30, 2019 | Inflation

The general consensus amongst economists is that US inflation is low. This was corroborated by favorable reports by the Department of Labor at the beginning of May. Yet, what trajectory will inflation take in the next half-decade? In this article, 5 experts weigh in on where US inflation is heading in the next 5 years.

The Fed Does Not Expect Inflation To Rise Significantly

“Inflation management is one of the primary roles of the Federal Reserve, so you can look to them for indications of inflation expectations.

The Fed will raise interest rates when it expects inflation to get above the 2% target. By raising interest rates, the Fed makes borrowing less attractive so spending and inflation will fall. Most recently, the Fed has announced that they do not plan to raise interest rates through 2021. This means that they do not expect inflation to rise significantly.

The Fed has also said they expect for unemployment to increase slightly. Again, this indicates low inflation. If less people are employed, then less people will have money to spend and create that upward pressure on prices that causes inflation.”

Brandon Renfro, Professor, Financial Planner

Not Much Organic Inflation

“Speaking as a consumer I do not believe there will be much ‘organic inflation’ in the next five years. A lot of people never fully recovered from the Great Recession. They’re saving a little bit more and do not fully trust the recovery. In addition the baby boomers are all approaching retirement age and will be living on fixed incomes. Healthcare costs are a major concern. According to statistics the economy is booming and yet a lot of people do not feel that is the case in their personal life.

Many people are working in Gig Economy jobs, which are in essence temporary assignments with no health benefits. Examples include driving for Uber, Lyft, Grub Hub, Door Dash, or Amazon delivery. These are not the type of positions, which fueled the economy in past generations.

Inflation is generally caused by consumers pumping a lot of money into the economy and taking on large amounts of debt. The wounds of the Great Recession have yet to heal. People are not automatically assuming they will be better off a year from now. Whenever one feels uncertain about the future they are reluctant to spend lavishly. Any spending they do is usually measured.

Having said that world affairs such as tariff wars and instability in the Middle East could cause inflation without any assistance from consumers. A major rise in oil costs could ripple through the economy causing prices to rise in other sectors of the economy. However, fear has a way of causing people to spend even less which leads to higher unemployment and recession. That would eliminate any inflation bubble.

We’re not likely to see any real inflation until the average working person believes the backbone of the economy is solid with good paying jobs. Right now adults are taking jobs from teenagers such as delivering newspapers, cutting lawns, snow removal, and working in fast food restaurants. This explains why there is a sudden push to make the minimum wage $15. We may not see historically high inflation for another 10 years!”

Kevin Darné, Author, Continuing Education Instructor

Rates Must Creep Back Up To Historic Levels

“Where’s US inflation heading in the next 5 years? – This is impossible to pin down precisely, but I believe that short of a recession, rates must creep back up to historic levels.

In spite of trade wars, government shutdowns and the resultant delay in statistics, the business cycle goes on. That said, corporations have used all the cost-cutting tricks in the world. Now is the time for increasing prices on the ground level as well as at the Fed Open Market Committee.

Complicating matters is that persistently low inflation and low rates hamstring the options that central banks have historically used to address crises. Again, in order to relieve this psychological pressure rates and inflation must creep up.”

Robin Lee Allen, Managing Partner, Esperance PE

A Modest Stagnation Of Growth Rates Can Be Expected

“Considering the latest development in trade and monetary policy, it can be expected that the U.S. inflation rate will remain at modest levels.

Given the uncertain outcome of the ongoing trade war, as well as highly leveraged corporate debt levels, which weigh on the outlook of the world economy, a modest stagnation of growth rates can be expected.

Another point to consider is the Fed’s shift in interest rate expectations. The expected monetary easing is an indication of concerns about low growth and geopolitical tensions.

Since the conundrum about the missing effect of the last quantitative easing programs still prevails, especially the question why full employment did not yield to higher inflation, it remains at least questionable if another round of quantitative easing would lead to higher inflation. The Federal Reserve Bank of St. Louis 5-Year Forward Inflation Expectation Rate (T5YIFR) dropped in the last year from 2.16% to 1.94% and from 2.47% to 1.94% within the last 5 years, even though the Fed deployed massive quantitative easing programs.”

Dr. Stephan Unger, Assistant Professor of Economics, Saint Anselm College

A Recession Within The Next 5 Years

“I predict inflation will stay around 2% for the next 3 years unless a recession hits sooner in which case I think the government will print more money and drive up inflation at a drastic rate. I think there will be a

recession within the next 5 years, so when that hits inflation may be as high as 10% in just one year.”

Stacy Caprio, Financial Blogger, Fiscal Nerd

Given economic indicators, the Fed has projected that there will be no real threat of skyrocketing inflation in the coming years. However, there are numerous variables that can shift which would alter that forecast. Ultimately, only time will provide the definitive answer.

by Sarah Bauder | May 29, 2019 | Inflation

Inflation and deflation can have a significant impact on the performance of a portfolio. It is crucial for investors to understand investment strategies to weather these two economic factors. In this article, experts provide valuable tips and insight into what investors need to know when investing during inflation and deflation.

Avoid Having High Cash Balances

“A top rule for investing during inflation is to avoid having high cash balances. Since money loses it’s purchasing power during such phases, investors should aim at investing into assets which are immune against devaluation, such as physical goods, e.g. gold, silver, other commodities, real estates, etc.

But also an investment into stocks would be good advice since stock prices tend to increase in times of inflation. The reason is that investors flee out of cash and are looking for any types of investment.

In times of deflation, investors should consider to hold cash and to invest in bonds, especially long-term bonds, since interest rates are likely to decline and therefore bond prices.”

Stephan Unger, assistant professor of economics, Saint Anselm College

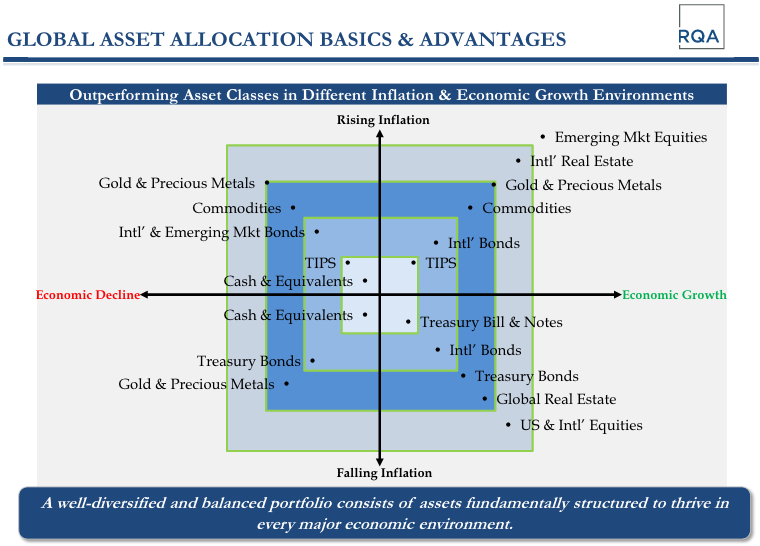

Utilize The Power Of Diversification

(Credit: Richmond Quantitative Advisors)

“The above illustration details global asset classes that tend to outperform during rising inflation and falling inflation. You can further delineate if the economy is in a declining stage or growth stage to provide four full quadrants of global asset performance.

The four quadrants include:

* Inflation with Growth – Inflationary Boom

* Inflation with declining Growth – Inflationary Stagnation

* Deflation with Growth – Deflationary Boom

* Deflation with declining Growth – Deflationary Bust

Based on the illustration, there are ways to position one’s portfolio for certain environments the US encounters. The main focus for investors should be to utilize the only free lunch in investing which is the power of diversification. By diversifying across assets within these four quadrants, one has the highest likelihood of weathering the storm (even if it is not clear where it may occur across the quadrants). Investors need to know those asset classes that have the ability to outperform in each quadrant and then assess their personal asset allocation decisions accordingly.”

Andrew S. Holpe, Managing Member, Richmond Quantitative Advisors

Investors Need To Generate After-Tax Returns

“Most people create investment portfolios to invest their assets to outpace the rate of inflation. The financial markets and governments prefer an environment with low, controllable inflation growth. These conditions allow for expansion while enabling governments to repay current debt with future-value currency.

According to Morningstar, a consensus of financial analysts predict that long-term inflation will grow at 2.48% per annum. Simply put, an investor needs to generate an after-tax return above this inflation rate to stand still and protect the purchasing power of their money.

The most prudent way to ensure success is to build a highly diversified portfolio of stocks, bonds, real estate, commodities, and cash-like liquidity. Limit your single-name stock concentration per issue to not more than 5%. Construct a bond portfolio focusing on credit-quality and that the current yield of your bond portfolio exceeds the effective duration of your portfolio. Effective duration is the sensitivity to a change in interest rates. The combination of these factors allow for growth and provide additional protection during a recession and deflationary environments.

During deflationary environments, consumers defer purchases because they expect lower prices in the future. That reality convinces more people that prices are falling and induces more deferral of purchases, etc. This virulent feedback loop is difficult to change and often requires extraordinary policy measures by central banks. During the credit crisis, the Federal Reserve (FED), Bank of Japan (BOJ) and the European Central Bank (ECB) all implemented radical policy measures to fight deflation. A flight to safety…underweight stocks, overweight cash, foreign exchange (FX), insured CDs, and sovereign bonds are prudent positioning during deflation of asset values. Your cash is worth more in terms of purchasing power as time goes on so there is some inherent return to cash even if there is little or no interest income.”

Paul Bowers, Managing Director, Compass Family Offices

Invest in Commodities And Real Estate

“Typically, assets that an investor would invest during inflationary times would be hard assets such as commodities and real estate. Commodities would include energy such as oil and gas as well as industrial and precious metals (not necessarily gold), You would NOT want to invest in bonds since interest rates rise during inflation and would result in declining bond prices. Many investment advisors recommend gold but I view it as more of a crisis manager rather than an inflationary hedge. In fact, one could argue that gold might be better used as a hedge during deflationary times since deflation tends to occur in a rapidly deteriorating economy when investors flock to protect their assets.

Stocks tend not to do well in deflationary environments. One reason often provided is that revenue and earnings are under duress as prices decline, which would eventually translate into lower stock prices.”

Cliff Caplan, CFP(r), AIF(r), Neponset Valley Financial Partners

Two Sides Of The Same Coin

“Economic factors such as inflation and deflation have a direct bearing to investors’ portfolio. Both are two sides of the same coin. Inflation is the rate at which general prices for goods or services are increasing while deflation is the decline in prices.

Investors need to know how these two factors can affect their investment portfolio. In certain situations, both inflation and deflation can occur at the same time, and this poses a more difficult prospect of protecting your investment. But whether it’s deflation or inflation, there are steps you can take to avert this threat.

If it’s inflation, investors can use the stock market to protect their portfolio. Normally, rising prices are good for equities. International bonds can also provide a solution in this case. Investors can buy international bonds in countries that are not experiencing inflation and hence reduce the impact of razing inflation.

In times of deflation, the most appropriate way to deal with it is to acquire high-quality bonds rather than stocks. Bonds tend to perform well during these times. Government-issued bonds and foreign bonds provide excellent options.”

Edith Muthoni, Chief Editor, Leanbonds.com

Investments Need To Beat The Rate Of Inflation

“It’s important to consider your real rate of return when you expect inflationary markets. Your investments need to beat the rate of inflation in order to make any real progress. If inflation is 8%, you need to make at least 8% on your investments just to break even. If your investments only earn 5% during an 8% inflation period, your real rate of return is roughly -3%. You made money, but not enough to keep up.

There are ways to invest specifically in anticipation of inflation. The simplest is to invest more aggressively in stocks. Since equity investments do better over longer horizons they are often a good inflation hedge. One drawback though is you do need to plan to hold the stocks for a long time. Since stocks tend to be more volatile, you’ll need to plan for a longer investment term. In the short-term, your stock values could fall.

A direct way to invest for inflation is to purchase securities that have explicit inflation terms. The most common of these is the Treasury Inflation Protected Security, or TIPS. These are government bonds whose par value, and therefore interest you receive, adjusts with changes in the consumer price index. You can get these in terms as short as five years.

Another way to invest for inflation is to buy rental real estate. The reason rental real estate is an inflation hedge is because of the rent payments. You can adjust those for inflation when your tenant’s lease expires. If your terms on an annual basis, you would be able to make the adjustment every year.”

Brandon Renfro, Professor, Financial Planner

Regardless of the economic climate, a diversified portfolio is essential. Diversification is crucial when factoring both periods of inflation and deflation. When making investment decisions, take into account these expert tips and always do your due diligence.