4 Effects Of Inflation On Your Personal Finances and Investments

Inflation is a general increase in the price of goods and services over time. In plain English, it means your money does not buy as much as it used to. That can sound like an economics textbook problem, but it is really a personal finance problem. Inflation affects your savings, investments, debt, retirement income, property costs, and everyday household budget.

I have been writing about financial and investment-related topics for more than two decades, and inflation is one of those subjects that always comes back into focus when people start feeling squeezed. You may not follow every monthly CPI report, but you definitely notice when groceries, insurance, rent, utilities, and borrowing costs start taking a bigger bite out of your income.

Inflation is commonly measured using the Consumer Price Index, or CPI. The CPI tracks price changes across a basket of consumer goods and services. If you want to compare the buying power of money across different years, you can also use our CPI inflation calculator.

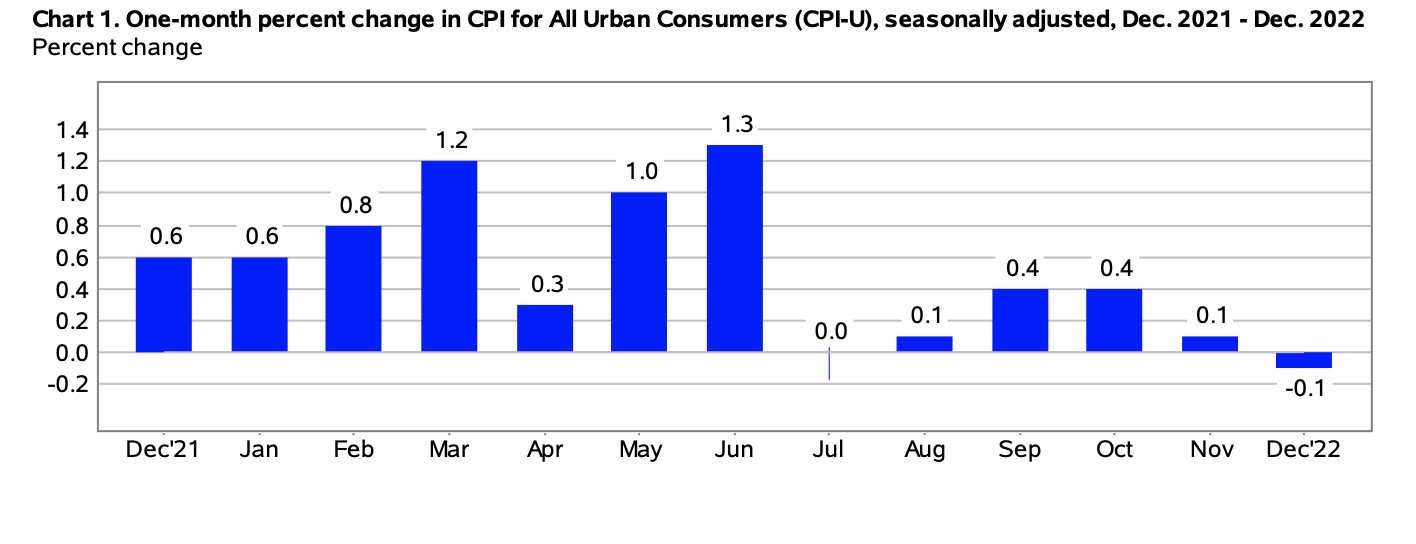

According to the U.S. Bureau of Labor Statistics, the Consumer Price Index for All Urban Consumers rose 3.8% over the 12 months ending April 2026. Core CPI, which excludes food and energy, rose 2.8% over the same period. That is lower than the worst inflation Americans experienced in 2022, but it is still high enough to matter when you are planning your savings, investments, and retirement.

Quick Takeaway

Inflation does not just make things more expensive. It changes the real value of your savings, income, investments, debt payments, and future retirement needs. The key is to think in terms of purchasing power, not just the dollar amount sitting in your account.

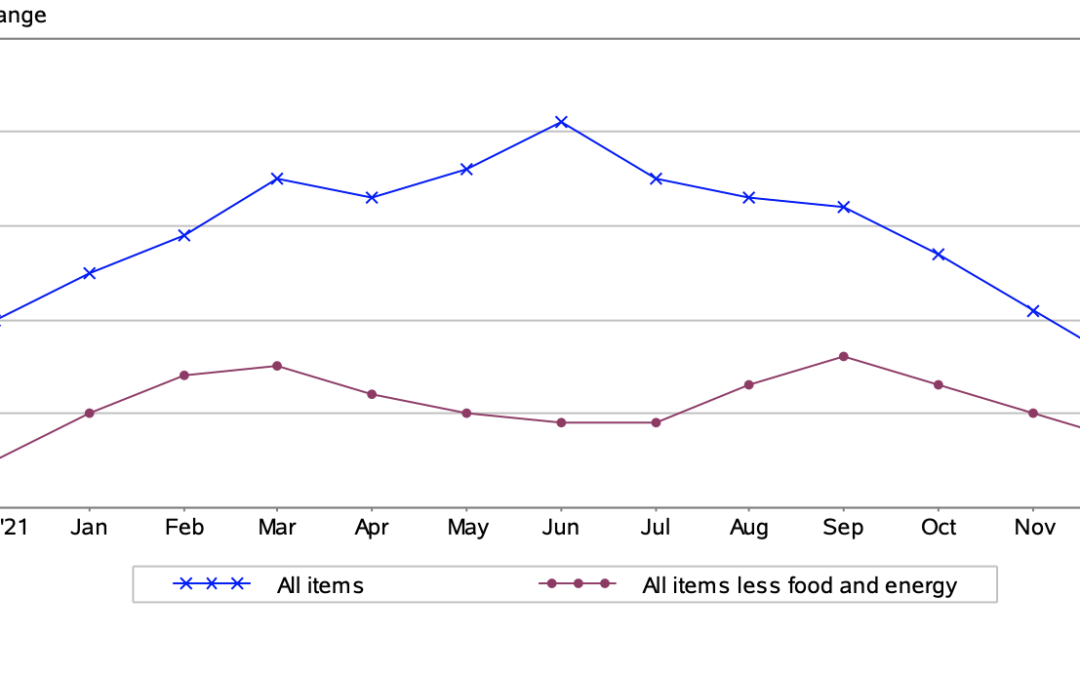

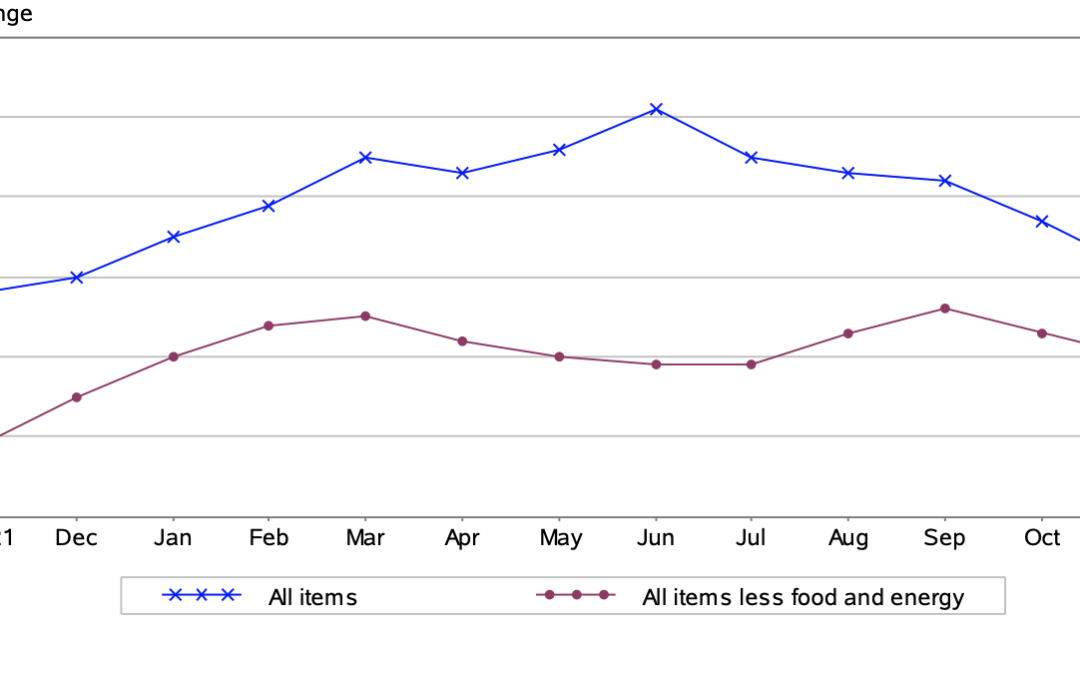

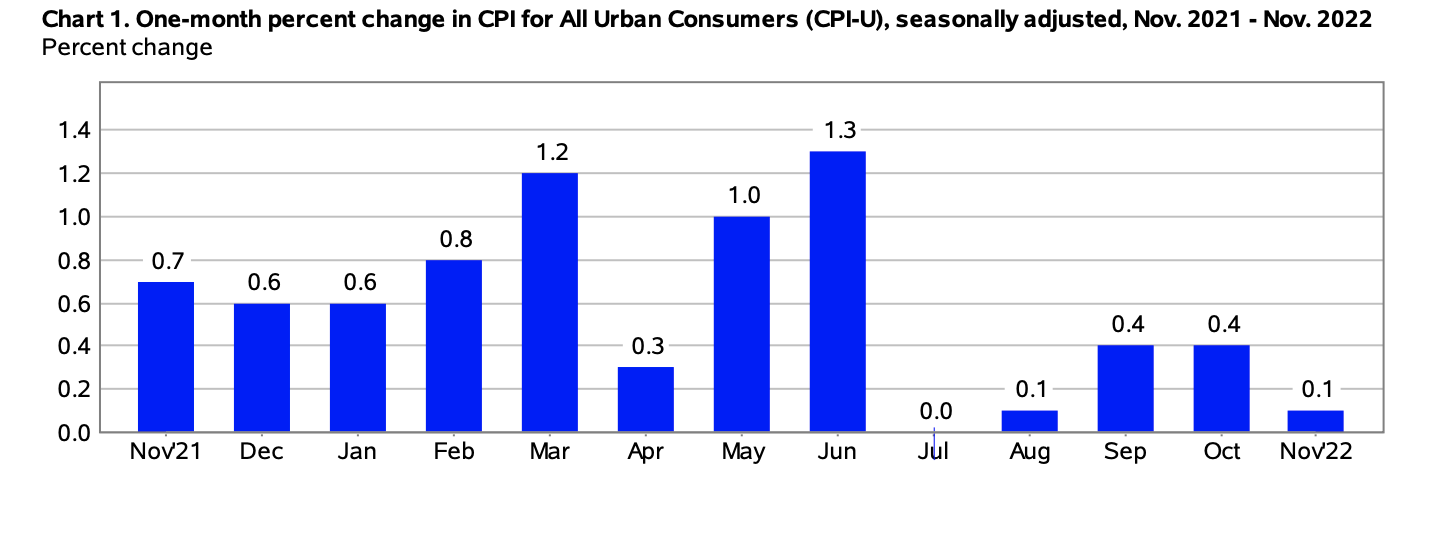

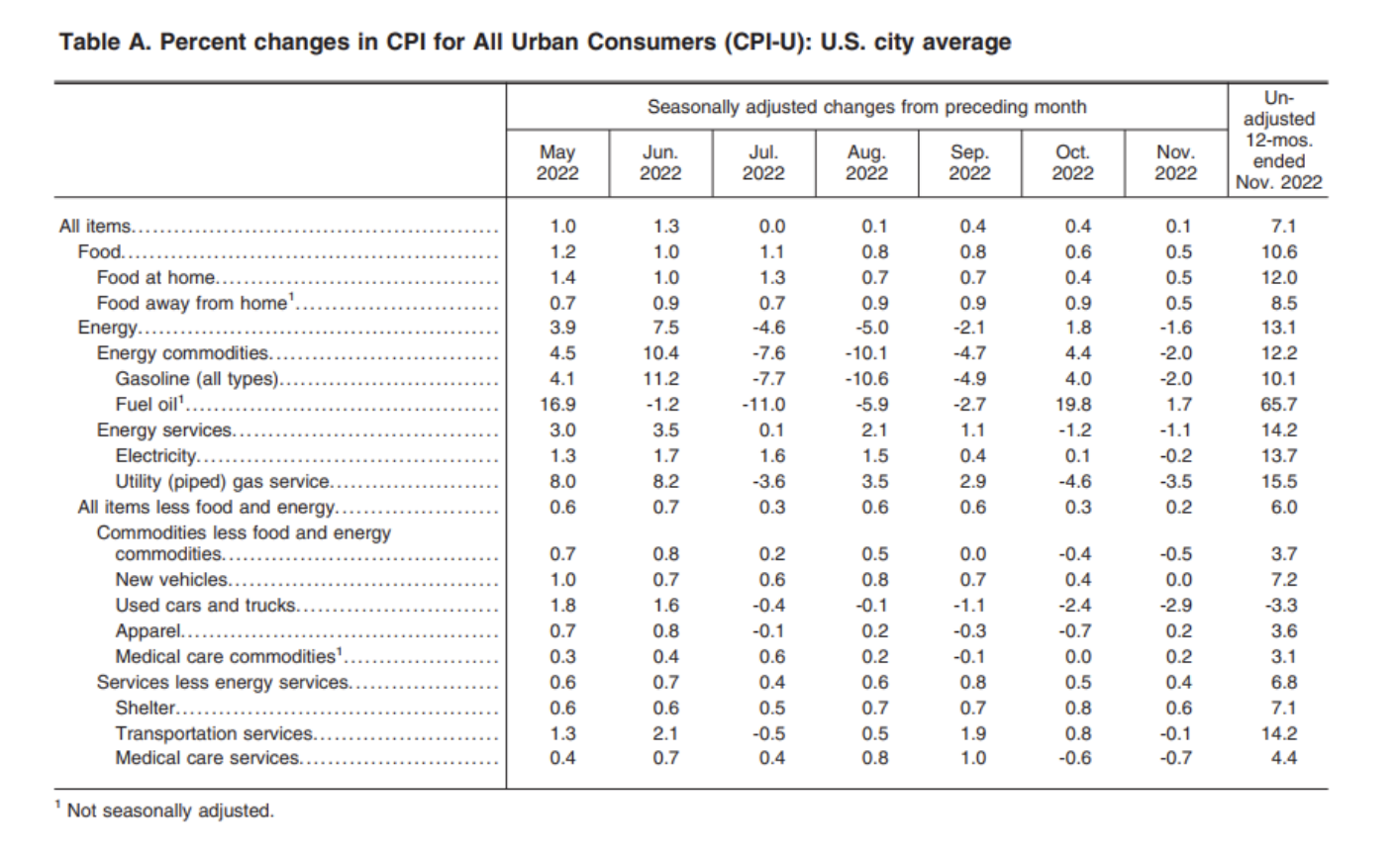

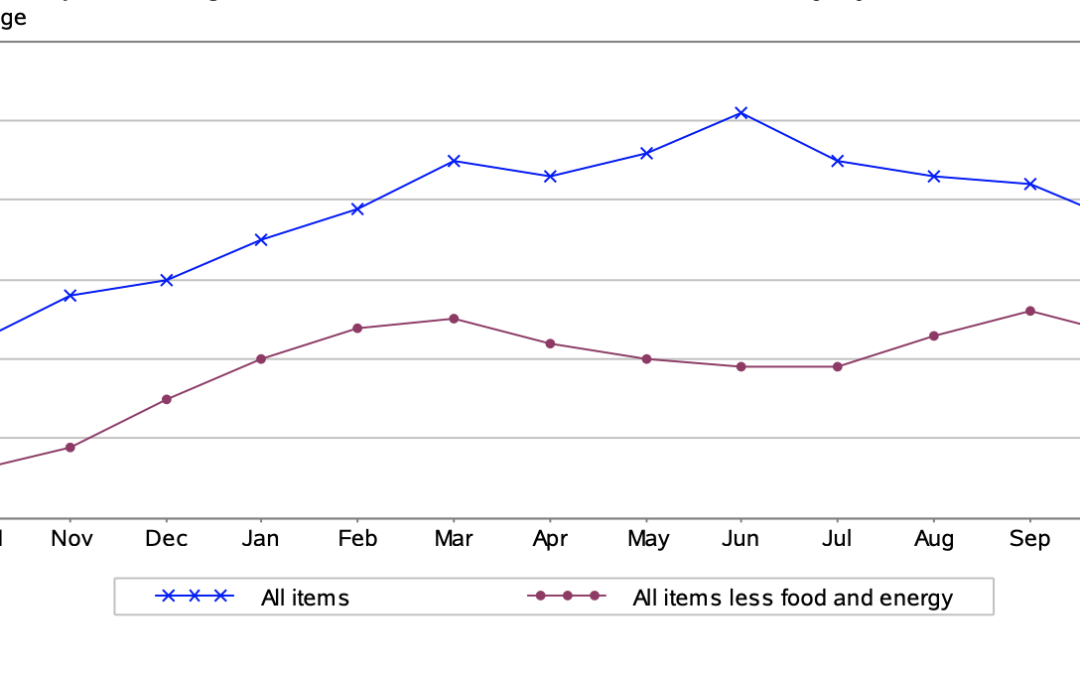

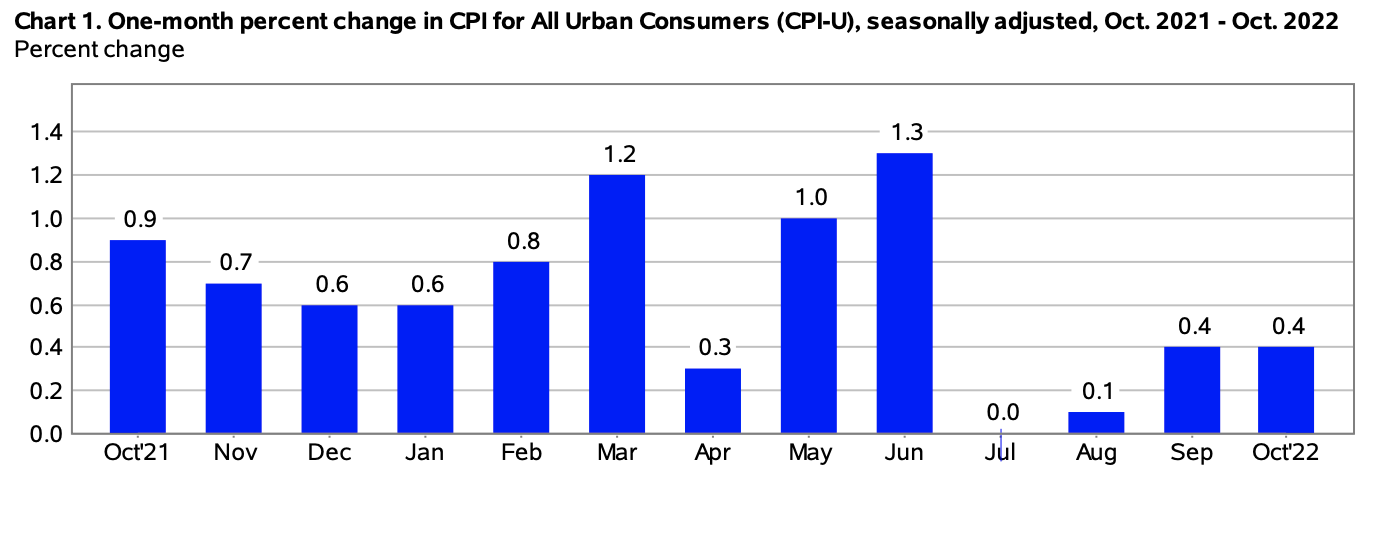

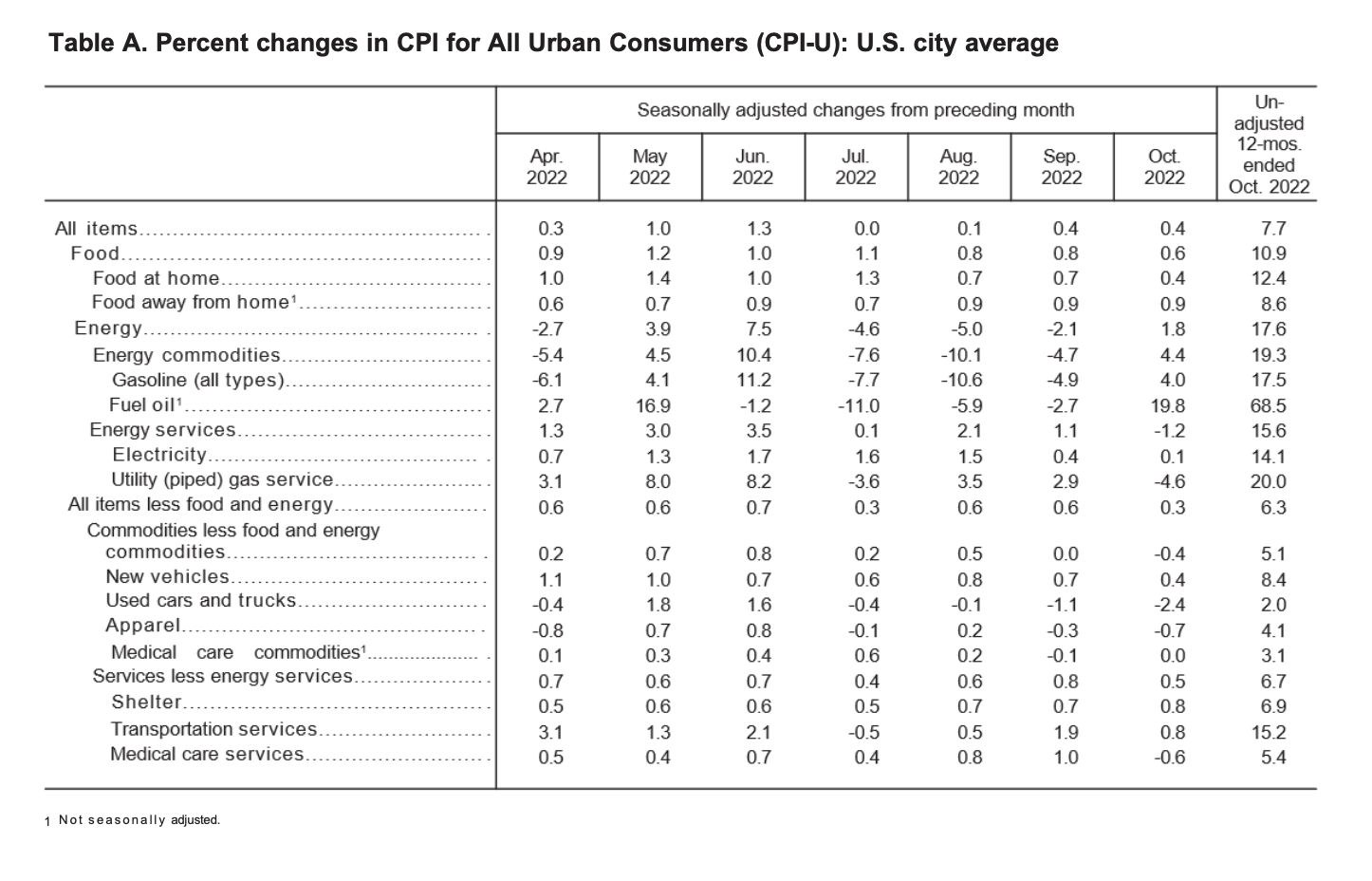

Historical CPI data helps show how inflation changes purchasing power over time. Source: Bureau of Labor Statistics

The Main Effects of Inflation on Your Personal Finances

Inflation does not affect every part of your financial life in the same way. Some assets may benefit from inflation. Some get hurt by it. Some debts become easier to handle, while others become more expensive.

| Area of Your Finances | How Inflation Can Affect It | What to Watch |

|---|---|---|

| Savings | Cash can lose purchasing power if interest rates do not keep up with inflation. | Real return after inflation and taxes. |

| Stocks | Companies may raise prices, but they may also face higher costs and lower margins. | Pricing power, earnings growth, and valuation. |

| Bonds | Fixed payments can become less valuable when inflation rises. | Interest rates, duration, and inflation protection. |

| Property | Property values and rents may rise, but ownership costs can rise too. | Mortgage type, insurance, taxes, repairs, and rates. |

| Retirement | Future expenses may be much higher than today’s expenses. | Inflation-adjusted income and withdrawal planning. |

The Effects of Inflation on Your Savings

One area most exposed to inflation is cash savings. A savings account can be a smart place for emergency money, short-term goals, and cash you may need quickly. I am not against holding cash. In fact, I think many people underestimate how important liquidity is when life gets messy.

But cash has one major weakness: it can quietly lose purchasing power if the interest rate on your account is lower than inflation.

For example, if you have $1,000 in a savings account earning 1% annually, you would have $1,010 after one year before taxes. But if inflation is running at 3.8%, you would need about $1,038 just to preserve roughly the same purchasing power. Your bank balance went up, but your real buying power went down.

This is what makes inflation so frustrating. You may not technically “lose” money in a savings account, but the money can still buy less over time.

Important point: The real return on savings is the interest rate you earn minus inflation. If your savings account earns 2% and inflation is 4%, your real return is roughly negative 2% before taxes.

This does not mean you should invest your emergency fund in the stock market. It means you should separate short-term savings from long-term wealth-building money. Cash is useful for stability and flexibility. But long-term money usually needs a plan that has a better chance of keeping up with inflation.

To understand how inflation has changed purchasing power historically, you can review our historical CPI tables or compare specific years using the calculator.

The Impact of Inflation on Stocks

Investing in stocks comes with more risk than keeping money in a savings account. Stock prices move up and down, and nobody can guarantee short-term returns. But over long periods, stocks have often helped investors protect and grow purchasing power better than cash.

That said, stocks are not automatically protected from inflation.

Inflation can affect stocks in a few different ways. When the economy is strong, companies may be able to raise prices, grow revenue, and increase earnings. That can support share prices. But when inflation rises too quickly, companies may also face higher costs for wages, raw materials, energy, shipping, rent, and financing. If those costs rise faster than revenue, profit margins can suffer.

This is why inflation can be especially difficult for companies that do not have pricing power. A business with a strong brand, essential products, and loyal customers may be able to pass some cost increases on to consumers. A weaker business may have to absorb those costs.

From an investor’s perspective, the real question is not only whether stocks go up in dollar terms. It is whether your investment return beats inflation over time.

Investor takeaway: During inflationary periods, focus on real returns, diversification, company quality, pricing power, debt levels, and your time horizon. Inflation can create pressure in the short term, but high-quality businesses may still help preserve purchasing power over the long term.

For a broader look at portfolio decisions during different economic conditions, you can read our guide on investing during inflation and deflation.

1979 $10,000 Treasury Bond. Fixed-income investments can be affected by inflation because future payments may lose purchasing power. Photo: Wikipedia

The Effects of Inflation on Bonds and Treasury Bills

Bonds and Treasury bills are often viewed as safer investments than stocks, but inflation can still affect them. The main issue is that many debt securities pay fixed interest. If inflation rises, those fixed payments may not buy as much as they did before.

For example, a bond paying 3% may look reasonable when inflation is 2%. But if inflation rises to 4% or 5%, the real value of that bond income may fall. This is one reason bond investors pay close attention to inflation expectations and interest rates.

Inflation can also affect bond prices through interest rates. When inflation is high, the Federal Reserve may keep interest rates higher to help bring inflation down. The Federal Reserve says it sets U.S. monetary policy to promote maximum employment and stable prices. When rates rise, older bonds with lower yields may become less attractive, which can push their market value down.

One option for investors worried about inflation is Treasury Inflation-Protected Securities, also known as TIPS. According to TreasuryDirect, TIPS are designed to help protect investors from inflation because the principal adjusts with changes in the Consumer Price Index.

TIPS are not perfect. They can still fluctuate in value, and they may have tax considerations depending on the account where they are held. But they can be useful for people who want part of their fixed-income portfolio linked to inflation.

You can learn more in our guide to inflation-protected bonds.

Property Ownership and Inflation

Property ownership can benefit from inflation, but it is not as simple as saying real estate always wins when prices rise.

On the positive side, property values and rents may rise over time. If you own a home with a fixed-rate mortgage, your principal and interest payment stays the same even as wages, rents, and general prices increase. That can make a fixed mortgage feel more affordable in real terms over time.

This is one reason many homeowners who locked in low fixed mortgage rates before rates rose have been reluctant to sell. Their monthly mortgage payment may be difficult to replace in the current rate environment.

However, inflation can also make property ownership more expensive. Home insurance, property taxes, repairs, materials, labor, utilities, and maintenance costs can all rise. Higher mortgage rates can also reduce buyer demand, which may make it harder to sell a property at the price you want.

| How Inflation Can Help Property Owners | How Inflation Can Hurt Property Owners |

|---|---|

| Fixed-rate mortgage payments may become cheaper in real terms. | Insurance, taxes, repairs, and maintenance may rise. |

| Property values may rise over long periods. | Higher mortgage rates can reduce affordability for buyers. |

| Landlords may be able to raise rents. | Operating costs may rise along with rental income. |

Real estate can be a useful inflation hedge in some situations, but it still depends on location, financing, purchase price, cash flow, and ownership costs.

Warren Buffett and the Matter of Inflation

Warren Buffett has written and spoken about inflation for decades, and his perspective is still useful for everyday investors. Buffett has long warned that inflation can quietly reduce the real value of investment returns, even when investors appear to be making money on paper.

In his classic 1977 Fortune essay, “How Inflation Swindles the Equity Investor,” Buffett explained why inflation can be difficult for both bondholders and stock investors. Bonds are vulnerable because future payments are made in dollars that may be worth less. Stocks can also struggle when inflation increases business costs, interest rates, and the amount of capital companies need just to maintain operations.

That does not mean Buffett believes people should avoid stocks. His broader investing philosophy has long favored owning high-quality businesses with durable competitive advantages, strong pricing power, and the ability to generate cash over long periods. Those traits can matter even more when inflation is eating into purchasing power.

Warren Buffett has written about inflation’s impact on investors for decades. Photo: Reuters/Carlo Allegri

The lesson for personal finance is simple: inflation is not just about higher grocery or gas prices. It also affects the real value of savings, bonds, retirement income, and investment returns. That is why investors need to think in terms of after-inflation returns, not just headline returns.

Inflation and Retirement Planning

Inflation becomes especially important when you are planning for retirement. If you are working, you may be able to earn more, change jobs, negotiate higher pay, or adjust your budget. Once you retire, your options may be more limited.

Retirees who depend heavily on fixed income can be vulnerable when prices rise. Even moderate inflation can have a major effect over long periods.

| Today’s Annual Spending | After 10 Years at 3% Inflation | After 20 Years at 3% Inflation |

|---|---|---|

| $40,000 | About $53,756 | About $72,245 |

| $60,000 | About $80,635 | About $108,367 |

| $80,000 | About $107,512 | About $144,489 |

This is why retirement planning should include inflation assumptions. A plan that looks comfortable in today’s dollars may look much tighter once you account for future housing, healthcare, food, insurance, travel, and utility costs.

Some people look at annuities, TIPS, dividend-paying stocks, real estate, or other income-producing assets as part of an inflation-aware retirement plan. None of these are perfect on their own, but they can each play a role depending on your age, risk tolerance, income needs, and total financial picture.

If you are researching this topic, you may also want to read our article on whether annuities are a good investment for inflation protection.

Planning for Inflation

Inflation is part of financial life. You cannot control the CPI, the Federal Reserve, energy prices, food prices, or global supply shocks. But you can build a financial plan that does not fall apart when prices rise.

In my view, the best approach is not to chase one perfect inflation hedge. It is to build layers of protection across your finances.

Practical Inflation Checklist

- Keep an emergency fund. Cash still matters, even if it does not always beat inflation.

- Watch your real return. Compare your savings and investment returns against inflation.

- Be careful with variable-rate debt. Credit cards and adjustable-rate loans can become more expensive when rates rise.

- Consider inflation-protected options. TIPS and other inflation-linked assets may help in certain portfolios.

- Invest for the long term. Diversified portfolios may help protect purchasing power over time.

- Review retirement assumptions. Future expenses may be much higher than today’s expenses.

- Follow CPI data. Use the CPI release schedule to track monthly inflation updates.

Gold is another asset people often consider during inflationary periods. I understand why. Gold has a long history as a store of value, and many investors look to it during periods of currency uncertainty or market stress. But gold is not a guaranteed inflation hedge in every period. It can be useful as a diversifier, but it should not be treated as a complete financial plan.

If you want to explore that topic further, we have a guide on gold and inflation. You can also use our inflation-adjusted gold return calculator to compare gold’s performance in real purchasing power terms.

For a broader look at possible inflation hedges, you may also find our article on inflation-resistant investments helpful. And if you want to understand why inflation can be measured in different ways, read our guide to different ways of measuring inflation.

Final Thoughts

Inflation affects personal finances because it changes the value of money. It can weaken the buying power of cash savings, pressure stocks and bonds, change the math on debt, complicate property ownership, and make retirement more expensive than expected.

The key is to think beyond nominal dollars. A $50,000 savings account, a 5% investment return, or a $60,000 retirement budget only tells part of the story. The more important question is what those dollars can actually buy after inflation.

That is why I believe inflation should be part of every serious financial plan. Not because you can predict it perfectly, but because ignoring it can make your savings, investments, and retirement plan look stronger than they really are.

If you want to stay current, you can review the latest 2026 U.S. inflation rate and CPI data and compare it with prior years such as the 2025 CPI and inflation data.

Frequently Asked Questions About Inflation and Personal Finances

How does inflation affect your personal finances?

Inflation affects your personal finances by reducing the purchasing power of your money. If prices rise faster than your income, savings, or investment returns, you may be worse off even if your account balances are higher in dollar terms.

How does inflation affect savings?

Inflation can reduce the real value of savings when the interest rate on your savings account is lower than the inflation rate. Savings accounts are still useful for emergency funds and short-term needs, but they may not be enough for long-term purchasing power protection.

How does inflation affect stocks?

Inflation can affect stocks by increasing business costs, interest rates, and pressure on consumer spending. Some companies can handle inflation better than others, especially those with strong pricing power, healthy balance sheets, and products people continue buying even when prices rise.

How does inflation affect bonds?

Inflation can hurt traditional bonds because fixed interest payments lose purchasing power when prices rise. Bond prices can also fall when interest rates increase. Inflation-protected securities, such as TIPS, are designed to help address this risk, although they can still fluctuate in value.

Is inflation good or bad for homeowners?

Inflation can help homeowners with fixed-rate mortgages because their monthly principal and interest payments stay the same while prices and wages may rise. However, homeowners may also face higher insurance, taxes, repairs, utilities, and maintenance costs.

Is inflation good or bad for debt?

Inflation can make fixed-rate debt easier to repay over time because the payment stays the same while the value of money declines. However, inflation can make variable-rate debt more expensive if interest rates rise, which is especially important for credit cards, adjustable-rate mortgages, and some personal loans.

How does inflation affect retirement?

Inflation can make retirement more expensive because future living costs may be higher than today’s costs. Retirees and future retirees should account for inflation when estimating income needs, withdrawal rates, healthcare costs, housing costs, and long-term savings goals.

What is the best way to protect your money from inflation?

There is no single best inflation hedge for everyone. A practical approach may include emergency savings, diversified investments, inflation-protected bonds, fixed-rate debt management, real estate, and possibly precious metals or other real assets depending on your goals and risk tolerance.

Why does my personal inflation rate feel higher than official CPI?

Your personal inflation rate may feel higher than official CPI if your biggest expenses are rising faster than the national average. For example, someone spending heavily on rent, groceries, insurance, healthcare, or gasoline may feel more pressure than the headline CPI number suggests.

How often is CPI data released?

The Bureau of Labor Statistics usually releases CPI data monthly. You can follow upcoming release dates using the CPI release schedule and compare current inflation data with historical CPI trends to see how prices have changed over time.