by Alex Demolitor | Oct 10, 2024 | Monthly CPI Updates

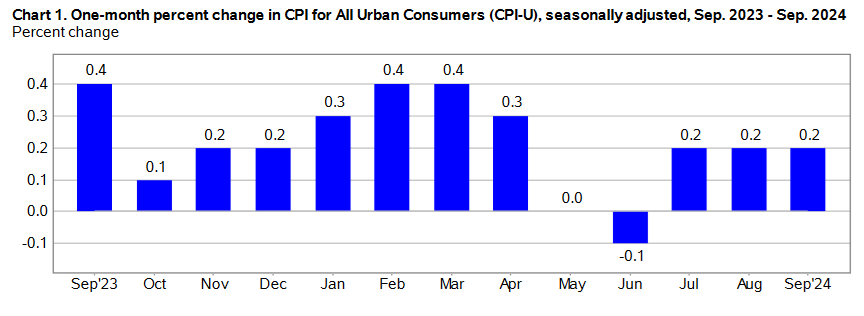

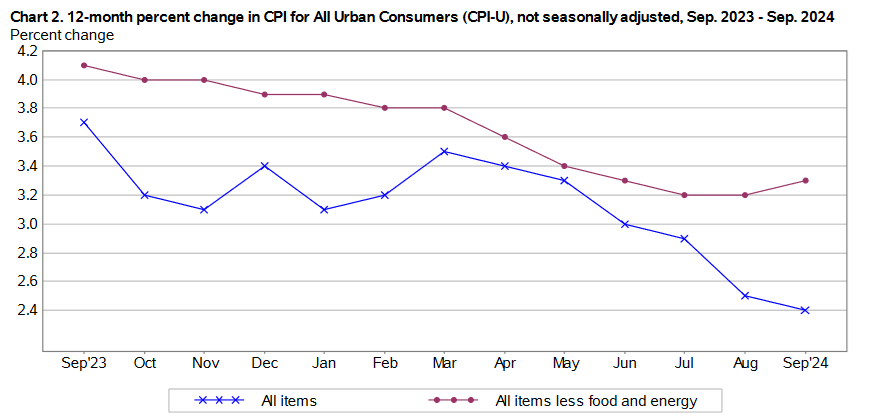

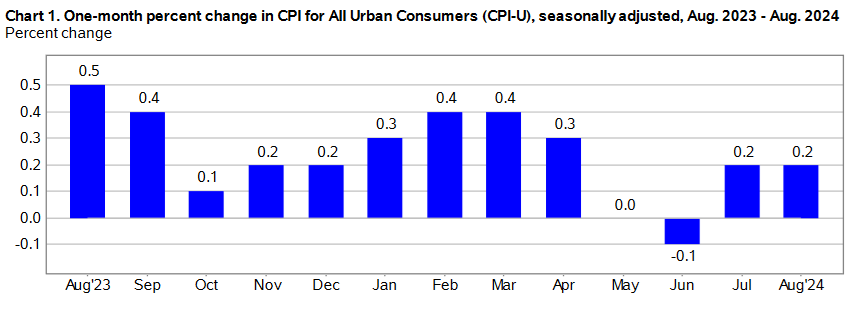

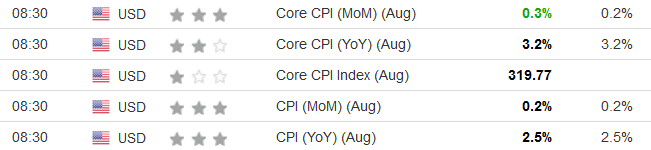

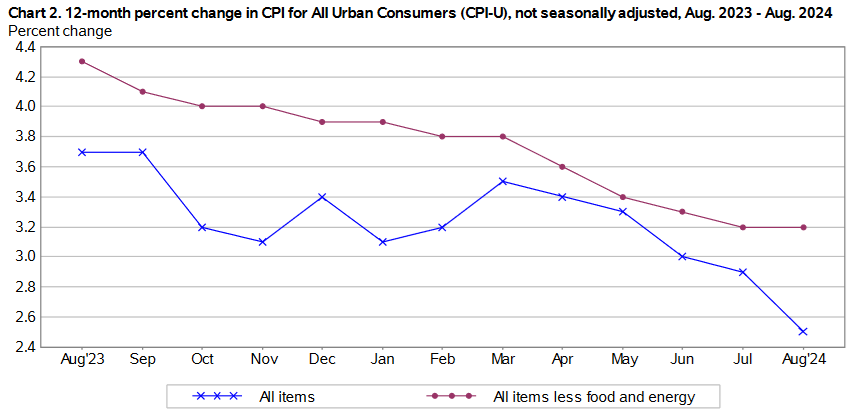

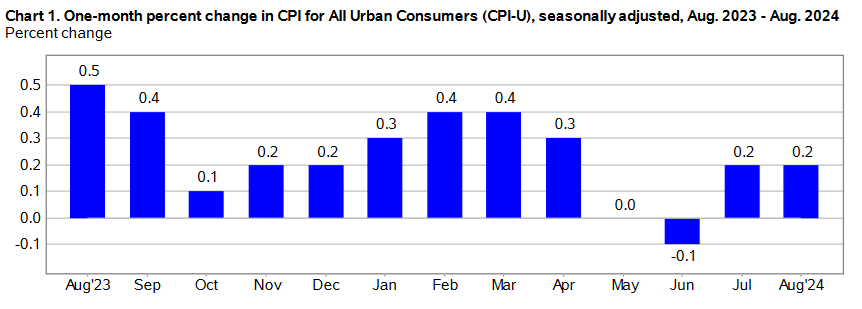

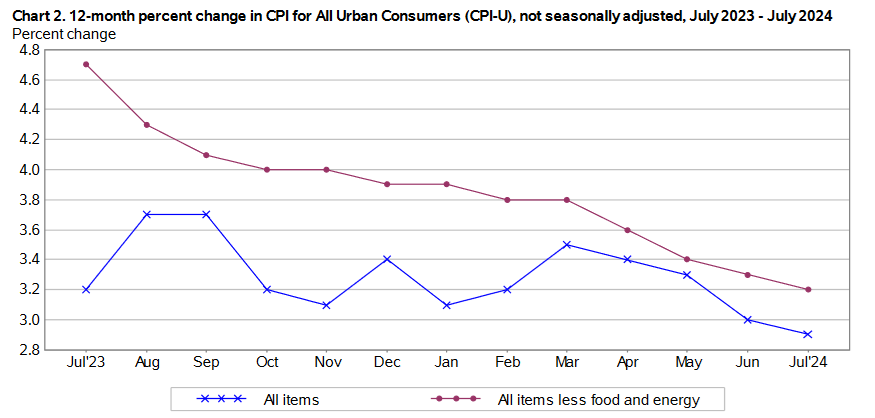

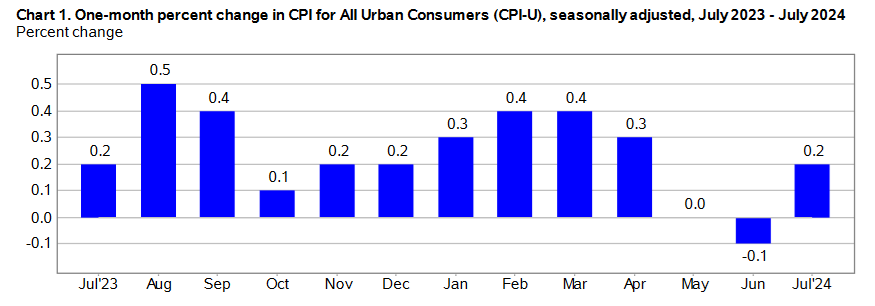

The September 2024 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation increased by 0.2% for the month, matching July and August’s 0.2% rise. These data were released at 8:30 am EST on Thursday, October 10, 2024, by the Bureau of Labor Statistics. Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 2.4%, down from July’s 2.9% and August’s 2.5% prints.

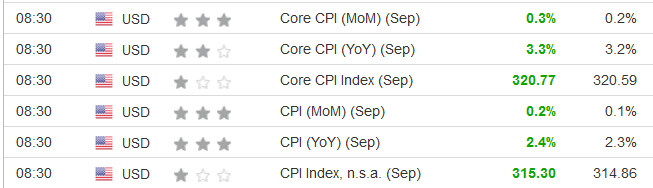

Although the results were relatively mild, all of the CPI metrics outperformed economists’ consensus estimates. The table below is courtesy of Investing.com. The left column represents September’s figures, while the right column represents forecasters’ expectations. As you can see, each data point (marked in green) was stronger than expected.

After FOMC Chairman Jerome Powell said during his annual Jackson Hole Economic Symposium speech that rate cuts were on the horizon, the committee delivered a 50 basis point rate cut on Sep. 18. Powell said during his post-meeting press conference:

“As inflation has declined and the labor market has cooled, the upside risks to inflation have diminished, and the downside risks to employment have increased. We now see the risks to achieving our employment and inflation goals as roughly in balance, and we are attentive to the risks to both sides of our dual mandate.”

He added: “If the economy remains solid and inflation persists, we can dial back policy restraint more slowly. If the labor market were to weaken unexpectedly or inflation were to fall more quickly than anticipated, we are prepared to respond. Policy is well positioned to deal with the risks and uncertainties that we face in pursuing both sides of our dual mandate.”

Thus, while Powell voiced concerns about both sides of the monetary policy equation, today’s inflation print highlights how fits and starts should be expected along the way.

Global markets had mixed responses to the CPI data, as stocks, bonds, precious metals, and the U.S. dollar moved relatively calmly in different directions.

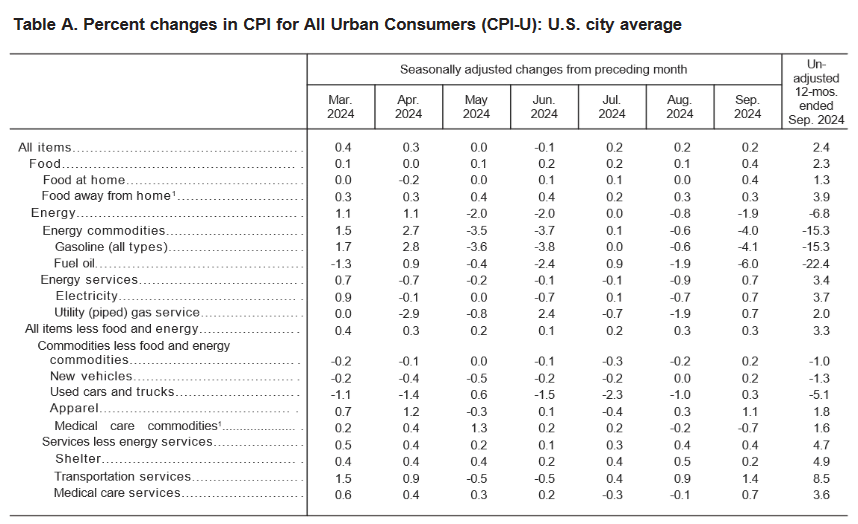

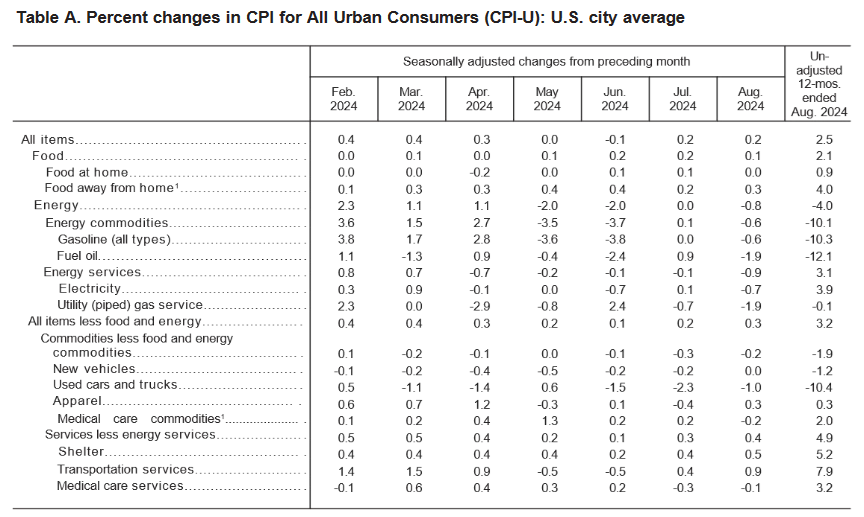

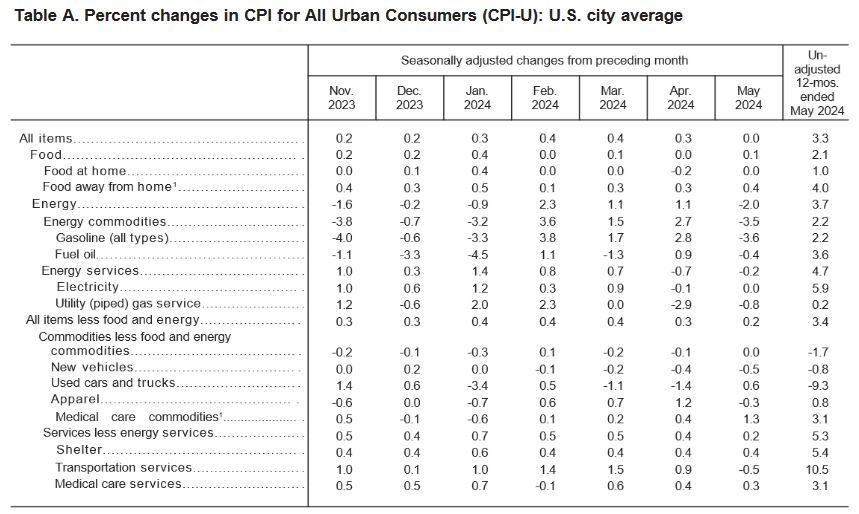

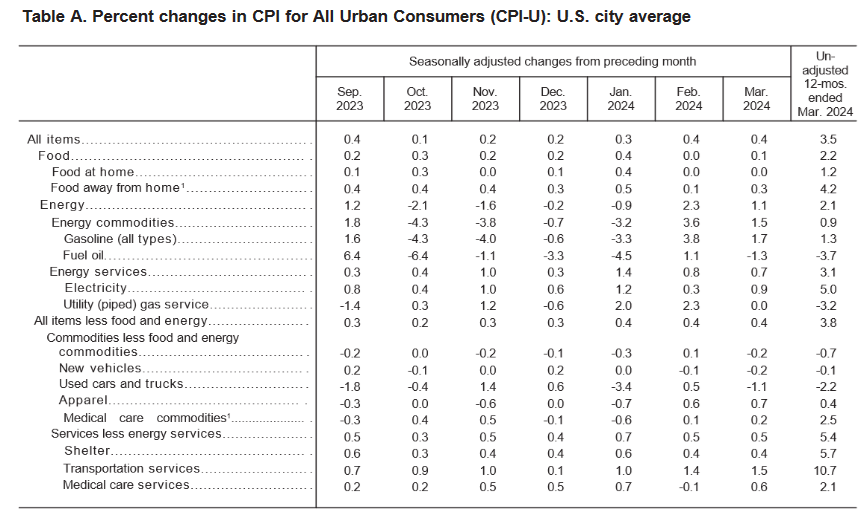

Notable monthly results within September’s headline inflation data showed transportation services prices jumped by 1.4%, apparel by 1.1%, and medical care services by 0.7%. Core inflation (which excludes the impacts of food and energy), rose by 0.3% in September, matching August’s print. However, the shelter index rose by 0.2%, a noticeable decline from the 0.5% reported in August.

Food Prices

The food index increased by 0.4% in September, well above the 0.1% recorded in August. Five of the six major grocery store food indexes showcased inflation, while one was flat.

- Cereals and bakery products (+0.3%)

- Meats, poultry, fish, and eggs (+0.8%)

- Dairy and related products (+0.1%)

- Fruits and vegetables (+0.9%)

- Nonalcoholic beverages (+0.0%)

- Other food at home (+0.2%)

In addition, the food away from home index rose by 0.3% in September, mirroring August’s rise, and highlighting how restaurant prices continue to outpace overall inflation.

Energy Prices

The energy index declined by 1.9% in September, building on the 0.8% drop in August. Gasoline prices plunged by 4.1% (5.1% without seasonal adjustments), while electricity and natural gas prices both rose by 0.7%.

Core CPI September 2024

The September core CPI rose by 0.3% month-over-month and 3.3% Y-o-Y. Below is an itemized breakdown of the main price fluctuations seen in the core CPI reading:

- Shelter index: (+0.2%) [August: +0.5%]

- Rent index: (+0.3%) [August: +0.4%]

- Owners’ equivalent rent: (+0.3%) [August: +0.5%]

- Motor vehicle insurance: (+1.2%) [August: +0.6%]

- Medical care services: (+0.7%) [August: -0.1%]

- Physician services: (+0.9%) [August: +0.0%]

- Hospital services: (NA) [NA]

- Airline fares: (+3.2%) [August: +3.9%]

Seasonally Unadjusted CPI Data for September 2024

Before seasonal adjustments, the CPI-U for September 2024 increased by 2.4% Y-o-Y, rising to an index level of 315.301. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

Was a 50 Basis Point Rate Cut a Mistake?

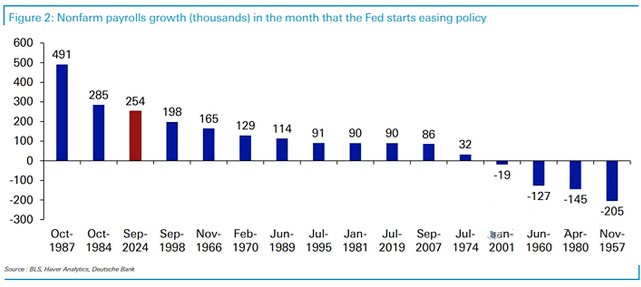

While investors were nervous that the FOMC was ‘behind the curve,’ September’s U.S. nonfarm payrolls report came in more than 100k above expectations.

The chart below from Deutsche Bank highlights how it was the third-largest employment increase in the same month the FOMC cut interest rates since 1957. If you analyze the red bar on the left, you can see the 254k jobs added implies the U.S. economy remains in solid shape. Consequently, with inflation outperforming expectations today, it may give the FOMC cause for pause at its next meeting.

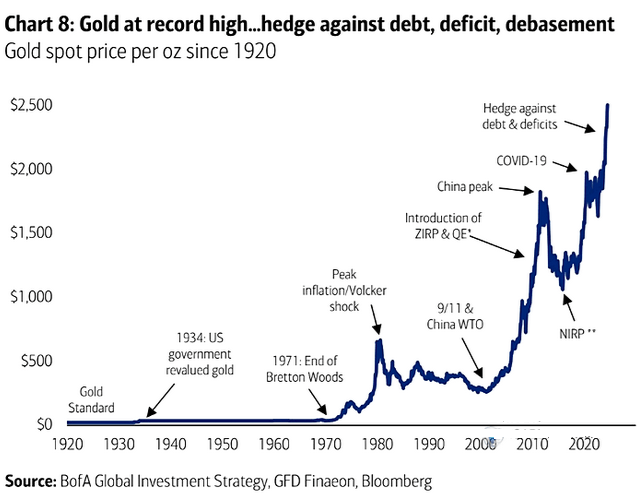

Overall, risk assets have rallied recently, as economic strength is good news for many of the 2024 winners like Bitcoin, Ethereum, gold, silver, and U.S. stocks. Moreover, gold has shined the brightest throughout the year, and Bank of America told clients that rising debt levels and U.S. dollar uncertainty continue to fuel the bull market.

Plus, with gold performing well during periods of calm and crisis, the chart below highlights how it’s often a portfolio ally when global uncertainty strikes.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Remember, seek the guidance of a financial advisor before making any investment decision.

by Alex Demolitor | Sep 11, 2024 | Monthly CPI Updates

The August 2024 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation increased by 0.2% for the month, matching July’s 0.2% rise. These data were released at 8:30 am EST on Wednesday, September 11, 2024, by the Bureau of Labor Statistics. Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 2.5%, down from July’s 2.9% and June’s 3.0% prints. It was the smallest Y-o-Y increase since February 2021.

Adding more merit to the rate-cut argument, most of the CPI metrics matched economists’ consensus estimates. The table below is courtesy of Investing.com. The left column represents August’s figures, while the right column represents forecasters’ expectations. As you can see, the monthly core CPI (marked in green) was stronger than expected, while the others (marked in black) met expectations.

As the financial market’s worst-kept secret, the Federal Open Market Committee (FOMC) is widely expected to cut interest rates on Sep. 18. Chairman Jerome Powell said during his annual Jackson Hole Economic Symposium speech on Aug. 23:

“The time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks.

“We will do everything we can to support a strong labor market as we make further progress toward price stability. With an appropriate dialing back of policy restraint, there is good reason to think that the economy will get back to 2 percent inflation while maintaining a strong labor market. The current level of our policy rate gives us ample room to respond to any risks we may face.”

Thus, while investors debate whether Powell will opt for a 25 or 50 basis point rate cut, the future direction of the U.S. interest rates has become abundantly clear.

Global stock markets largely declined after the CPI release, as volatility has increased in recent weeks. Conversely, Treasury bonds, precious metals, and the U.S. dollar exhibited mixed performances.

August’s headline inflation deceleration was driven by lower utility gas prices (-1.9%), fuel oil (-1.9%), and used cars and trucks (-1.0%). Core inflation (which excludes the impacts of food and energy), rose by 0.3% in August, up from 0.2% in July, and 0.1% in June. The shelter index rose by 0.5% (up from 0.4% in July) and the BLS described the jump as “the main factor in the all items increase.”

Food Prices

The food index increased by 0.1% in August, a deceleration from June and July’s 0.2% prints. Two of the six major grocery store food indexes showcased inflation, while four realized deflation.

- Cereals and bakery products (-0.1%)

- Meats, poultry, fish, and eggs (+0.8%)

- Dairy and related products (+0.5%)

- Fruits and vegetables (-0.2%)

- Nonalcoholic beverages (-0.7%)

- Other food at home (-0.3%)

In addition, the food away from home index rose by 0.3% in August, ahead of July’s 0.2% rise, meaning restaurants continue to increase their menu prices.

Energy Prices

The energy index declined by 0.8% in August after experiencing a flat performance in July. Electricity and natural gas prices slumped by 0.7% and 1.9%, respectively, while gasoline prices dropped by 0.6% excluding seasonal adjustments.

Core CPI August 2024

The August core CPI rose by 0.3% month-over-month and 3.2% Y-o-Y. Below is an itemized breakdown of the main price fluctuations seen in the core CPI reading:

- Shelter index: (+0.5%) [July: +0.4%]

- Rent index: (+0.4%) [July: +0.5%]

- Owners’ equivalent rent: (+0.5%) [July: +0.4%]

- Motor vehicle insurance: (+0.6%) [July: +1.2%]

- Medical care services: (-0.1%) [July: -0.3%]

- Physician services: (+0.0%) [July: +0.1%]

- Hospital services: (NA) [July: -1.1%]

- Airline fares: (+3.9%) [July: -1.6%]

Seasonally Unadjusted CPI Data for August 2024

Before seasonal adjustments, the CPI-U for August 2024 increased by 2.5% Y-o-Y, rising to an index level of 314.796. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

25 or 50?

With investors’ anxiety on full display since August, the debate has shifted from battling inflation to avoiding a recession. Some market participants believe the FOMC is ‘behind the curve,’ meaning that interest rates have been too high for too long and the committee can’t avoid an economic slowdown.

The latest U.S. Job Openings and Labor Turnover Survey (JOLTS) showcases a material decline in employment opportunities, which highlights Powell’s point that “upside risks to inflation have diminished, and the downside risks to employment have increased.”

Therefore, while the debate between a 25 or 50 basis point rate cut should intensify over the next several days, only time will tell if the recent deceleration is a growth scare or something more ominous.

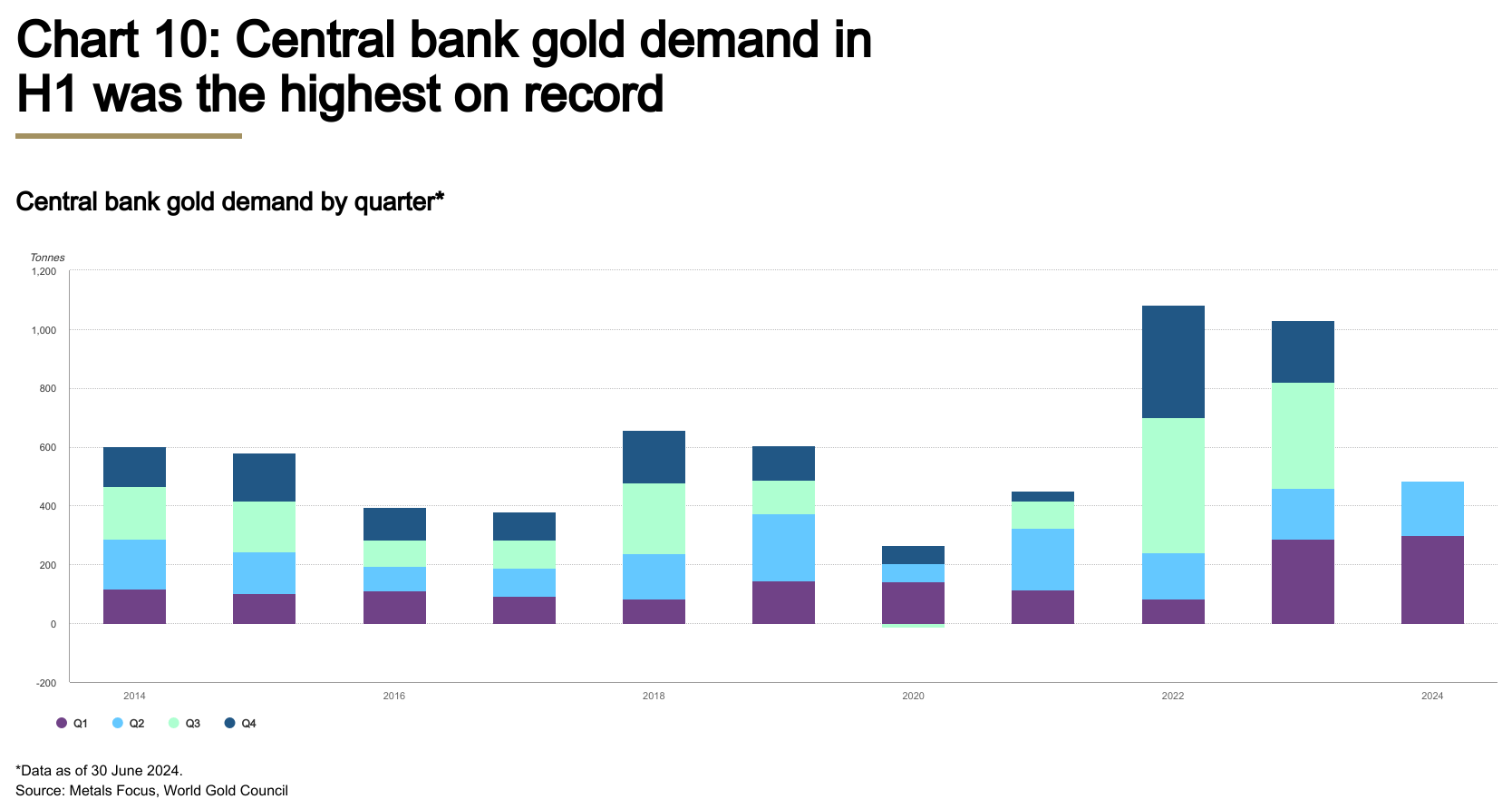

Overall, risk assets have suffered recently, and 2024 winners like Bitcoin, Ethereum, gold, silver, and U.S. stocks have pulled back from their recent highs. However, global central banks have piled into the yellow metal, and the World Gold Council noted on Jul. 30, “Combined with Q1 net purchases, central bank gold demand in H1 totaled 483t, the highest first half year in our data series.” As a result, physical demand for bullion remains robust.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Remember, seek the guidance of a financial advisor before making any investment decision.

by Alex Demolitor | Aug 14, 2024 | CPI, Monthly CPI Updates

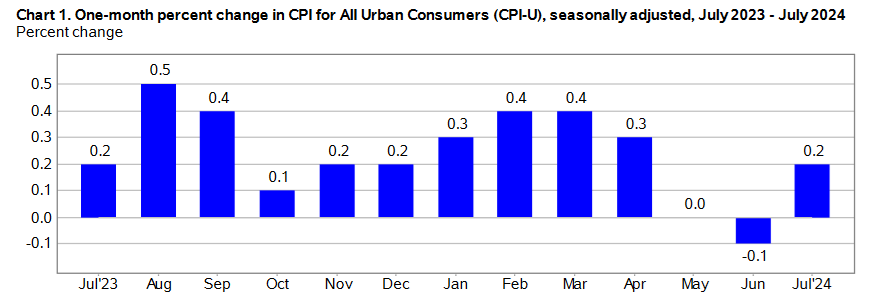

The July 2024 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation increased by 0.2% for the month, a rise from June’s 0.1% decline. These data were released at 8:30 am EST on Wednesday, August 14, 2024, by the Bureau of Labor Statistics. Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 2.9%, decelerating from June’s 3.0% Y-o-Y CPI print.

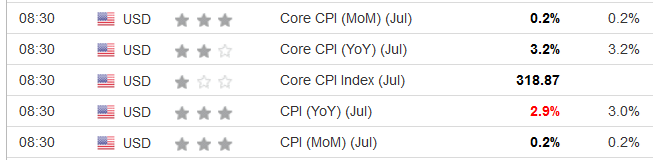

Doing little to derail the chances of future rate cuts, most of the CPI metrics matched economists’ consensus estimates. The table below is courtesy of Investing.com. The left column represents July’s figures, while the right column represents forecasters’ expectations. As you can see, the Y-o-Y CPI (marked in red) was weaker than expected, while the others (marked in black) met expectations.

To that point, while Fed Chairman Jerome Powell said on Jul. 31 that “we’re not quite at that point” where a lower overnight lending rate is justified, he added, “We’re getting closer to the point at which it’ll be appropriate to reduce our policy rate.”

Moreover, the FOMC’s latest Monetary Policy Statement noted that “The Committee judges that the risks to achieving its employment and inflation goals continue to move into better balance.” In other words, the FOMC has become more attentive to a slowing U.S. labor market, which may pave the way for less emphasis on inflation and foster monetary easing.

Global markets had a mixed response to the CPI release, with American and European indices largely remaining range-bound. Likewise, Treasury bonds, precious metals, and the U.S. dollar had mostly small reactions since the as-expected CPI data wasn’t much of a surprise.

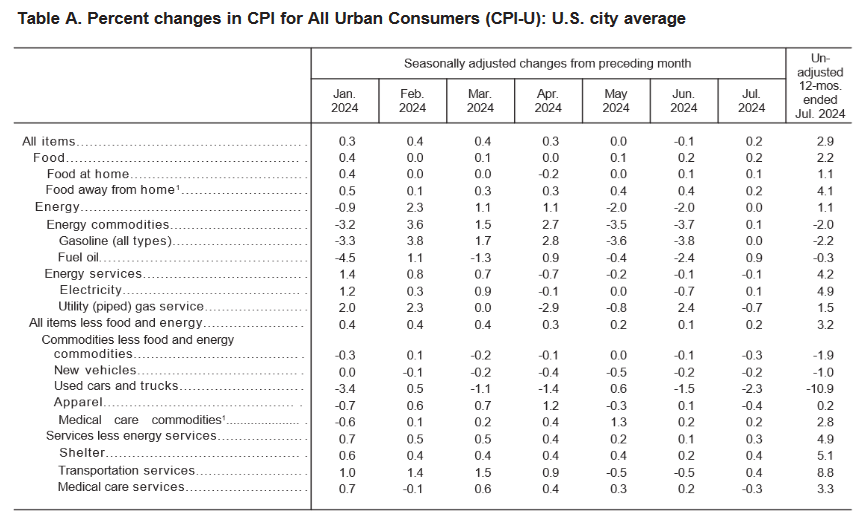

July’s headline inflation deceleration was driven by lower used cars and trucks prices (-2.3%), utility gas (-0.7%), and apparel (-0.4%). Core inflation (which excludes the impacts of food and energy), rose 0.2% in July, a small increase from June’s 0.1% rise. The shelter index rose 0.4% and accounted for nearly 90% of the headline CPI’s rise.

Food Prices

The food index increased by 0.2% in July, matching the 0.2% print from June. Three of the six major grocery store food indexes showcased inflation, while three realized deflation.

- Cereals and bakery products (-0.5%)

- Meats, poultry, fish, and eggs (+0.7%)

- Dairy and related products (-0.2%)

- Fruits and vegetables (+0.8%)

- Nonalcoholic beverages (+0.5%)

- Other food at home (-0.5%)

In addition, the food away from home index rose by 0.2% in July, a noticeable slowdown from the 0.4% recorded in May and June. Consequently, restaurants pared back some of their pricing practices this month.

Energy Prices

The energy index was flat in July after falling 2.0% in June. Electricity and fuel oil prices rose by 0.1% and 0.9%, respectively, while natural gas prices fell by 0.7%. Gasoline prices were also flat in July on a seasonally adjusted basis and up by 0.8% excluding adjustments.

Core CPI July 2024

The July core CPI rose by 0.2% month-over-month, which is within the Fed’s range of expectations. On a Y-o-Y basis, the metric rose 3.2%. Below is an itemized breakdown of the main price fluctuations seen in the core CPI reading:

- Shelter index: (+0.4%) [June: +0.2%]

- Rent index: (+0.5%) [June: +0.3%]

- Owners’ equivalent rent: (+0.4%) [June: +0.3%]

- Motor vehicle insurance: (+1.2%) [June: +0.9%]

- Medical care services: (-0.3%) [June: +0.2%]

- Physician services: (+0.1%) [June: +0.1%]

- Hospital services: (-1.1%) [June: +0.1%]

- Airline fares: (-1.6%) [June: -5.0%]

Seasonally Unadjusted CPI Data for July 2024

Before seasonal adjustments, the CPI-U for July 2024 increased (+2.9%) Y-o-Y, rising to an index level of 314.540. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

Growth Concerns Overshadow Inflation?

Because price stability is only one-half of the Fed’s dual mandate, investors always worry that too much emphasis on inflation could slow economic growth and derail the other half of the dual mandate — maximum employment.

As a result, while the financial markets have stabilized in recent days, last week’s ‘flash crash’ and calls for emergency rate cuts highlight the anxiety that occurs alongside rate-cutting cycles. Historically, rate cuts have sometimes preceded recessions, so investors are looking for clues that a hard landing can be avoided. Thus, weaker data is good for financial assets as long as it’s not too weak.

Consequently, 2024 winners like Bitcoin and Ethereum have suffered recently, as have U.S. stocks. And while silver has fallen below the important $30 level, gold has largely maintained its strength. Therefore, the yellow metal has shown an ability to perform during good and bad periods throughout 2024.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Remember, seek the guidance of a financial advisor before making any investment decision.

by Alex Demolitor | Jun 12, 2024 | Monthly CPI Updates

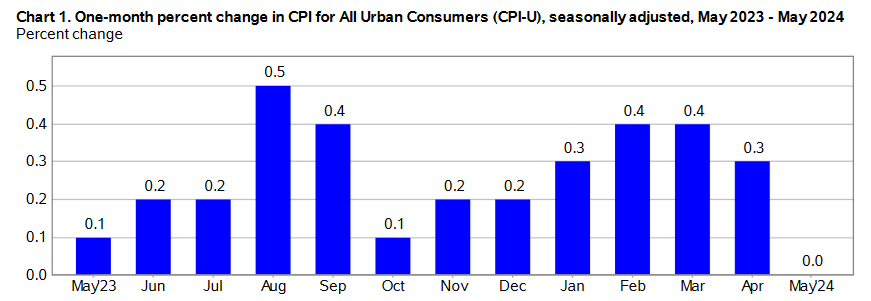

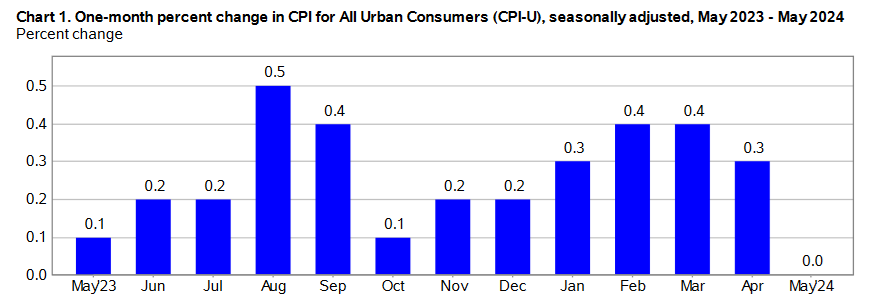

The May 2024 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation was flat for the month, coming in below April’s increase (+0.3%). These data were released at 8:30 am EST on Wednesday, June 12, 2024, by the Bureau of Labor Statistics. Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 3.3%, which is also a deceleration from April’s 3.4% Y-o-Y CPI reading.

Adding fuel to the rate-cut debate, the headline and core CPIs came in below economists’ consensus estimates. The table below is courtesy of Investing.com. The left column represents May’s figures, while the right column represents forecasters’ expectations. As you can see, the monthly and Y-o-Y CPIs (marked in red) were weaker than expected.

Furthermore, the Federal Open Market Committee (FOMC) releases its Monetary Policy Statement today at 2 p.m. ET. The group is widely expected to maintain the federal funds rate at its 5.25% to 5.5% range. However, Chairman Jerome Powell holds his press conference at 2:30 p.m. ET, and he should discuss the Committee’s projections and shed light on the path of interest rates in the months ahead. With U.S. government and consumer credit card debt at or near record highs, monetary easing would certainly help reduce the strain on low-income households.

Global markets lauded the CPI slowdown, with American and European indices climbing. Similarly, Treasury bonds and precious metals rallied as rate-cut expectations increased, while the U.S. dollar suffered as market participants adopted a more dovish outlook.

May’s headline inflation deceleration was driven by lower gasoline prices (-3.6%), utilities (-0.8%), new vehicles (-0.5%), and transportation services (-0.5%). Core inflation (which excludes the impacts of food and energy), rose 0.2% in May, the weakest monthly reading in 2024. The indexes for airline fares, new vehicles, communication, recreation, and apparel led the declines.

Source: Bureau of Labor Statistics

Food Prices

The food index increased by 0.1% in May after remaining flat in April. Uncooked poultry and beef roasts declined by 2.6% and 3.1%, respectively, while margarine fell by 2.7% and carbonated drinks sunk by 2.0%. Two of the six major grocery store food indexes showcased deflation, two were unchanged, and the other two increased.

- Cereals and bakery products (+0.2%)

- Meats, poultry, fish, and egg (+0.2%)

- Dairy and related products (-0.5%)

- Fruits and vegetables (+0.0%)

- Nonalcoholic beverages (-0.3%)

- Other food at home (+0.0%)

In addition, the food away from home index jumped 0.4% in May, outperforming the 0.3% increases from the previous two months. As a result, restaurants continue to demonstrate resilient pricing power.

Energy Prices

The energy index dropped 2.0% in May, a noticeable decline from April’s 1.1% rise. Gasoline and natural gas prices also fell by 3.6% and 0.8%, while the fuel oil index was down 0.4%. The index for electricity was flat in May.

Core CPI May 2024

The May core CPI rose by 0.2% month-over-month, the lowest monthly print in 2024. On a Y-o-Y basis, the metric rose +3.4%. Below is an itemized breakdown of the main price fluctuations seen in the core CPI reading:

- Shelter index: (+0.4%) [April: +0.4%]

- Rent index: (+0.4%) [April: +0.4%]

- Owners’ equivalent rent: (+0.4%) [April: +0.4%]

- Motor vehicle insurance: (-0.1%) [April: +1.8%]

- Medical care services: (+0.3%) [April: +0.4%]

- Physician services: (+0.0%) [April: +0.1%]

- Hospital services: (+0.5%) [April: +0.6%]

- Airline fares: (-3.6%) [April: -0.8%]

Source: Bureau of Labor Statistics

Seasonally Unadjusted CPI Data for May 2024

Before seasonal adjustments, the CPI-U for May 2024 increased (+3.3%) Y-o-Y, rising to an index level of 314.069. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

Source: Bureau of Labor Statistics

Gold Bugs Rejoice

With the CPI slowdown supporting lower interest rates and a weaker U.S. dollar, gold has been one of the best-performing assets in 2024. Likewise, silver has really shined in recent weeks. Since precious metals futures contracts are priced in USD, a weaker greenback makes it more affordable for foreign investors to purchase the yellow metal. As such, lower Treasury yields, a weaker dollar, and increased rate-cut enthusiasm create a profitable environment for gold enthusiasts.

However, if other commodities exhibit similar strength, bullish bets on assets like oil, gasoline, food, lumber, etc. could increase inflation in the months ahead. Moreover, lower interest rates increase American’s disposable income, which could boost consumption during the summer months when economic activity is typically strong.

Thus, 2024 winners like gold, silver, Bitcoin, and Ethereum are betting that the Fed will find it difficult to tame inflation without causing a recession that sparks the next round of quantitating easing. In contrast, the S&P 500 and NASDAQ Composite have soared on hopes that inflation will fade and a soft landing will materialize. Only time will tell which team claims victory.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Remember, seek the guidance of a financial advisor before making any investment decision.

by Alex Demolitor | May 17, 2024 | Monthly CPI Updates

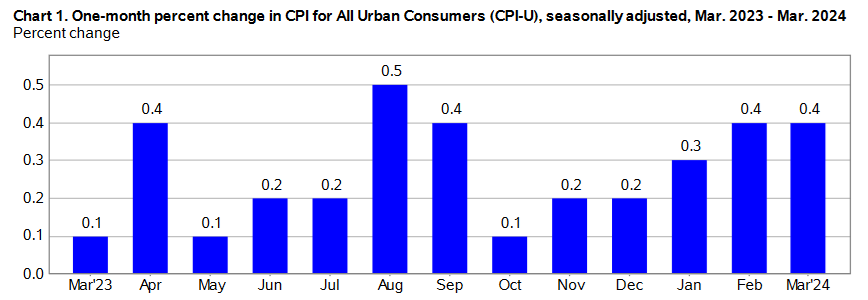

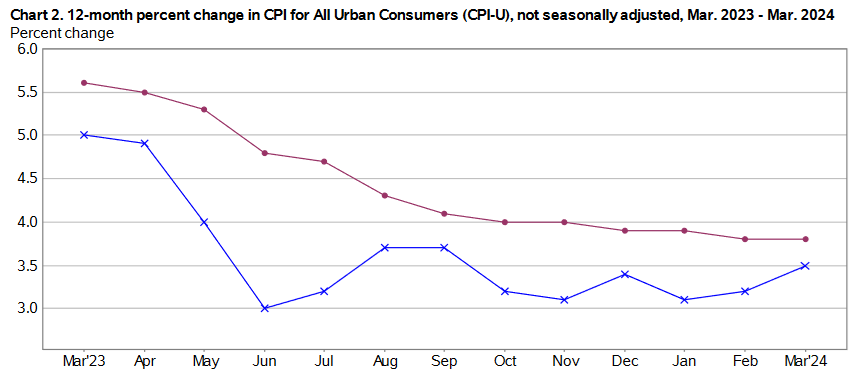

The March 2024 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation rose by 0.4% for the month, matching the price acceleration seen in February (+0.4%). These data were released at 8:30 am EST on Wednesday, April 10, 2024, by the Bureau of Labor Statistics. Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 3.5%, which is an acceleration from February’s 3.2% Y-o-Y CPI reading.

According to CNBC, economists surveyed by Dow Jones had expected a 0.3% monthly gain and a 3.4% Y-o-Y increase, meaning the March results exceeded Wall Street’s expectations. Given the sticky price pressures and the U.S.’s economic resilience, the data emboldened Fed officials to preach patience as it relates to potential rate cuts.

The Federal Reserve’s federal funds rate sits at 5.25% to 5.5%, which has pushed mortgage and credit card interest rates to multi-year highs. The development has also occurred alongside record U.S. government and consumer credit card debt. However, the U.S. economy remains supported by near-record-low unemployment and above-trend GDP growth.

Global markets had a mixed response to the CPI print, with Europe’s Stoxx 600 index ending the day in positive territory, while U.S. markets sold off.

March’s headline inflation outperformance was driven by higher gasoline prices (+1.7%), transportation services (+1.5%), electricity (+0.9%), and apparel (+0.7%). Core inflation (which excludes the impacts of food and energy), rose 0.4% in March, matching the upticks from January and February. The primary contributors were shelter, motor vehicle insurance, medical care, apparel, and personal care.

Source: Bureau of Labor Statistics

Food Prices

The food index rose 0.1% in March, surpassing February’s reading. Conversely, the food at home index remained flat for the second consecutive month. Three of the six major grocery store food group indexes declined in March, with the cereals andbakery products index showcasing its largest one-month seasonally-adjusted decrease since the BLS began tallying the data in 1989:

- Cereals and bakery products (-0.9%)

- Meats, poultry, fish, and egg (+0.9%)

- Dairy and related products (-0.1%)

- Fruits and vegetables (+0.1%)

- Nonalcoholic beverages (0.3%)

In addition, food away from home rose by 0.3% in March, which annualizes to 3.67%. As a result, restaurants demonstrated resilient pricing power during the month.

Energy Prices

Turning to the energy complex, the index rose +1.1% in March, a material deceleration from the 2.3% rise in February. This month’s uptick was largely driven by higher gasoline and electricity prices, partially offset by a drop in fuel oil prices.

Core March 2024 CPI

The March core CPI rose by 0.4% month-over-month, mirroring the increases from January and February. On a Y-o-Y basis, the metric rose +3.8%. Below is an itemized breakdown of the main price fluctuations seen in the core CPI reading:

- Shelter index: (+0.4%) [February: +0.4%]

- Rent index: (+0.4%) [February +0.5%]

- Owners’ equivalent rent: (+0.4%) [February: +0.4%]

- Motor vehicle insurance: (+2.6%) [February: +0.9%]

- Medical care services: (+0.6%) [February: -0.1%]

- Physician services: (+0.1%) [February: -0.2%]

- Hospital services: (+1.0%) [February: -0.6%]

- Airline fares: (-0.4%) [February: +3.6%]

Source: Bureau of Labor Statistics

Seasonally Unadjusted CPI Data for March 2024

Before seasonal adjustments, the CPI-U for March 2024 increased (+3.5%) Y-o-Y, rising to an index level of 312.332. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

Source: Bureau of Labor Statistics

Gold Keeps Shining Despite Higher Interest Rates

Even with Treasury yields, a strong U.S. dollar, and real (inflation-adjusted) interest rates marching higher, gold has maintained its reputation as an inflation hedge. Moreover, with geopolitical tensions increasing its appeal, the yellow metal has more than rate-cut enthusiasm supporting its ascent.

Although forecasts of the first cut moved from March to September, Wall Street analysts still expect the Fed to ease monetary conditions to support the housing market and indebted consumers.

Consumer confidence has taken a noticeable hit recently, as The Conference Board and University of Michigan’s metrics highlight an environment where Americans worry about the cost of living and housing affordability. However, with lower interest rates supporting consumers’ wallets at the expense of higher inflation, the Fed has a tough challenge on its hands.

As the drama unfolds, market participants have pushed assets like gold, silver, and cryptocurrencies like Bitcoin and Ethereum to cycle highs, further emphasizing uncertainty over the Fed’s ability to control inflation.

Furthermore, with stocks near record highs and investors worried about the safety of the U.S. dollar, cash seems less appealing than it once was, even with short-term bonds offering yields near 5%.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Remember, seek the guidance of a financial advisor before making any investment decision.

by Alex Demolitor | May 17, 2024 | Monthly CPI Updates

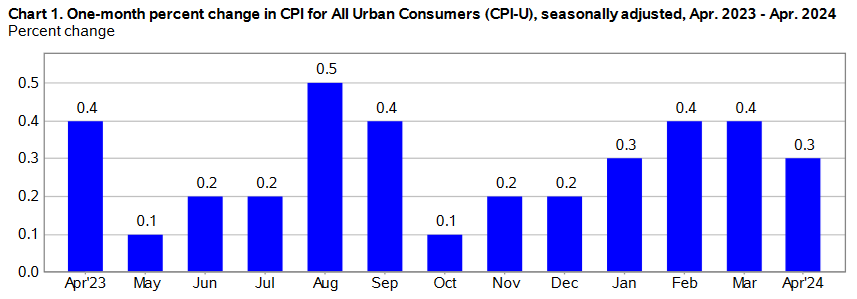

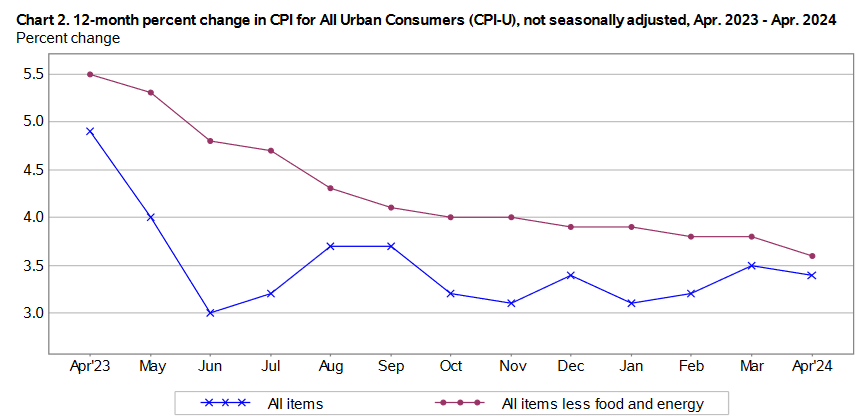

The April 2024 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation rose by 0.3% for the month, a notch below March’s increase (+0.4%). These data were released at 8:30 am EST on Wednesday, May 15, 2024, by the Bureau of Labor Statistics. Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 3.4%, which is also a slowdown from March’s 3.5% Y-o-Y CPI reading.

CNBC noted that April’s monthly increase came in below economists’ consensus estimate of 0.4%, while the Y-o-Y figure was in line with expectations. The slowdown should be welcome news for the Fed, as the FOMC’s projection of 100 basis points of rate cuts has been derailed by the stubborn pricing pressures. However, with Fed Chairman Jerome Powell cautious about encouraging another acceleration, it will be interesting to see how his tone evolves in the weeks ahead.

The Federal Reserve’s federal funds rate remains at 5.25% to 5.5%, and the ascent has been a burden on the housing market and Americans strapped with credit card debt. With record U.S. government and consumer credit card debt still present, monetary easing would certainly help reduce the strain on low-income households.

As expected, global markets responded positively to the CPI slowdown, with American and European indices climbing, while the NASDAQ Composite hit a new all-time high. Similarly, Treasury bonds rallied as rate-cut expectations increased. In contrast, the U.S. dollar suffered as market participants adopted a more dovish view.

March’s headline inflation deceleration was driven by lower utility prices (-2.9%), used cars and trucks (-1.4%), and food at home (-0.2%). Core inflation (which excludes the impacts of food and energy), rose 0.3% in April, a drop from the 0.4% seen in January, February, and March. The indexes for used cars and trucks, household furnishings and operations, and new vehicles helped lead the declines.

Source: Bureau of Labor Statistics

Food Prices

The food index was flat in April after jumping by 0.1% in March. Headlining the pullback, the index for meats, poultry, fish, and eggs fell in April, led by a 7.3% decline for eggs. Fruits and vegetables and nonalcoholic beverages also showcased deflationary trends:

- Cereals and bakery products (+0.6%)

- Meats, poultry, fish, and egg (-0.7%)

- Dairy and related products (+0.1%)

- Fruits and vegetables (-0.8%)

- Nonalcoholic beverages (-0.2%)

In addition, food away from home rose by 0.3% in April, which matches March and annualizes to 3.67%. As a result, restaurants are still passing through higher wage and input costs.

Energy Prices

Mirroring the March reading, the energy index rose +1.1% in April, with gasoline up 2.8% and fuel oil up 0.9%. Conversely, the index for natural gas fell 2.9% and electricity prices eased by 0.1%.

Core April 2024 CPI

The April core CPI rose by 0.3% month-over-month, which was below January, February, and March’s 0.4% reading. On a Y-o-Y basis, the metric rose +3.6%. Below is an itemized breakdown of the main price fluctuations seen in the core CPI reading:

- Shelter index: (+0.4%) [March: +0.4%]

- Rent index: (+0.4%) [March: +0.4%]

- Owners’ equivalent rent: (+0.4%) [March: +0.4%]

- Motor vehicle insurance: (+1.8%) [March: +2.6%]

- Medical care services: (+0.4%) [March: +0.6%]

- Physician services: (+0.1%) [March: +0.1%]

- Hospital services: (+0.6%) [March: +1.0%]

- Airline fares: (-0.8%) [March: -0.4%%]

Source: Bureau of Labor Statistics

Seasonally Unadjusted CPI Data for April 2024

Before seasonal adjustments, the CPI-U for April 2024 increased (+3.4%) Y-o-Y, rising to an index level of 313.548. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

Source: Bureau of Labor Statistics

Gold Continues to Climb

With the CPI slowdown supporting lower interest rates and a weaker U.S. dollar, gold has basked in the glory. Since gold futures contracts are priced in USD, a weaker greenback makes it more affordable for foreign investors to purchase the yellow metal. As such, lower Treasury yields, a weaker dollar, and increased rate-cut enthusiasm have created the perfect environment for gold enthusiasts.

However, with other commodities joining the party, expectations of a dovish Fed could increase inflation in the months ahead, if assets like oil, gasoline, and food commodity prices rise. Moreover, lower interest rates increase American’s disposable income, which could boost consumption during the summer months when economic activity is typically strong.

Thus, 2024 winners like gold, silver, Bitcoin, and Ethereum are betting that the Fed will find it difficult to tame inflation without causing a recession that sparks the next round of quantitating easing.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Remember, seek the guidance of a financial advisor before making any investment decision.