by Amine Rahal | Apr 10, 2026 | gold

✅ Reviewed by: Lauren Brown | Last updated: 2026

Are you thinking of investing in physical gold or silver to diversify against inflation, market uncertainty, or geopolitical risk? Below is our 2026 roundup of top-rated U.S. precious metals dealers and Gold IRA companies, with a practical focus on what actually affects outcomes:

premiums (markups), annual IRA fees, storage, buyback terms, and how “pushy” the sales process feels.

Our top pick in 2026: Noble Gold Investments 🥇

If you want a beginner-friendly Gold IRA company with a simple onboarding process, strong reputation signals, and a free educational guide, Noble Gold is our current top recommendation.

Request the free gold guide

Common friction points investors don’t expect (read this first):

- Rollover timing: IRA/401(k) transfers can take 7–21+ days depending on your custodian and plan administrator.

- Total cost is more than “spot price”: you pay dealer premiums plus separate custodian + storage fees in most IRAs.

- Product choice changes cost: common bullion coins/bars typically have lower premiums than proof/collectible coins.

- Buybacks vary: “buyback program” doesn’t always mean the same thing. Ask how pricing is set (spot, bid/ask, spreads).

- Sales pressure is real: if you feel rushed, pause and compare 2–3 quotes in writing.

Quick picks (who each company is best for)

| Company |

Best for |

|

Beginner-friendly onboarding, low minimums, simple gold & silver IRA setup, and a free educational guide. Request Noble Gold’s Free 2026 Kit. |

|

Education-first help, white-glove gold IRA rollovers, investors who want hands-on guidance |

|

High-net-worth investors who want a premium, education-led experience |

|

Investors wanting broad coin/bullion selection and flexible starting amounts |

Tip: Most readers do best by shortlisting 2–3 companies, requesting their free info kits, then comparing premiums, annual IRA fees, buyback policies, product selection, and service.

What to request from each company (so you can compare apples to apples):

- A written fee schedule: custodian fee, annual maintenance, storage/insurance, and any transaction fees

- A quote showing the premium over spot for the exact products you want (example: 1 oz Gold Eagle vs 1 oz bar)

- Your storage options (segregated vs non-segregated) and which depository is used

- Buyback details: how they price repurchases and typical timelines

Cost reality check

What a Gold IRA typically costs (so you can spot bad deals)

| Cost bucket |

What it is |

What to ask |

| Dealer premium |

Markup over spot for coins/bars (varies by product) |

“What percent over spot is this exact item?” |

| Custodian fee |

IRA administration (often annual; sometimes setup fee too) |

“Send me the full fee schedule in writing.” |

| Storage + insurance |

Vault storage (segregated vs non-segregated) + insurance |

“Which depository? What’s the annual storage rate?” |

| Exit costs |

Selling back (spread), shipping, liquidation fees (if any) |

“How do you price buybacks and how fast do you settle?” |

Note: The company you choose matters, but the product you choose can matter just as much. Proof/collectible coins often carry higher premiums than standard bullion.

How we rank

Our ranking criteria (and what we weigh most)

- Pricing transparency: clear explanations of premiums, fees, and what you’re actually buying

- Customer experience: responsiveness, education quality, and low-pressure onboarding

- IRA execution: rollover paperwork support, custodian/depository coordination, and process reliability

- Product quality: availability of common bullion options (coins/bars) and IRA-eligible metals

- Reputation signals: BBB, Trustpilot, Google, complaint history, and consistency across platforms

Note: Third-party review platforms can be imperfect. We treat ratings as one data point, not the whole story.

When in doubt, we prioritize written quotes and written fee schedules.

Website: noblegoldinvestments.com

Phone: (626) 605-3152

Location: Texas (storage options through approved partners/depositories)

Minimum investment: $10,000

CEO: Collin Plume

Gold IRA support: Yes

Why we ranked it #1: Noble tends to work well for readers who want a straightforward onboarding, a beginner-friendly experience, and a broad selection of common coins and bars without needing a very large minimum to get started.

Noble is one of the better-known precious metals firms in the U.S. with a broad selection of coins and bars. They’re beginner-friendly, strong on education, and can help IRA and 401(k) owners diversify with gold and silver through approved custodians. Compared with some competitors, Noble feels like a cleaner starting point for the average investor who wants a simple setup and a free educational guide before moving forward.

Questions to ask Noble (so you avoid surprises)

- “Can you show me the all-in annual IRA costs for my target account size?”

- “What are today’s premiums for popular bullion (not proof/collectible coins)?”

- “Which storage option are you quoting: segregated or non-segregated?”

Best for

- Newer investors who want a straightforward IRA rollover experience

- People who want a wide selection of common IRA-eligible metals

- Investors starting around the $10k range

Not ideal for

- Investors who only want ultra-low premiums with minimal guidance

- Collectors pursuing rare numismatic strategies

Want deeper research? Read the full review here:

Noble Gold review.

Website: goldencrestmetals.com

Phone: (833) 426-3825

Location: California (Calabasas)

Minimum investment: $10,000

Leadership: Rich Jacoby (CEO/Owner)

Gold IRA support: Yes (supports IRA-eligible metals via approved custodians/depositories)

Why we ranked it #2: GoldenCrest is a strong fit for investors who want education-first guidance and help coordinating the rollover process. For many readers, the “win” isn’t chasing the lowest premium, it’s avoiding mistakes: product mismatch, unclear fees, or a confusing IRA setup.

GoldenCrest Metals is an education-first dealer that helps clients open and fund Precious Metals IRAs and also supports cash purchases. What stands out is its boutique, hands-on service model, easy phone access, and frequent promos aimed at lowering first-year costs. It partners with approved custodians and mainstream depositories and is designed for investors who want more guidance through the rollover process.

Questions to ask GoldenCrest (so you can compare fairly)

- “For the exact products I’m considering, what’s the premium over spot today?”

- “Which custodian/depository options do you recommend, and what are the annual fees for each?”

- “If I need to sell later, how do you price buybacks and what’s the typical timeline?”

Best for

- First-time Gold IRA rollovers and hands-on guidance

- Investors who care about education and support

- People comparing premiums and fee schedules carefully

Not ideal for

- Ultra-DIY buyers who only want the absolute lowest premium

- Collectors seeking niche, hard-to-find numismatics

To learn more about GoldenCrest Metals:

Request the free gold kit

Tip: Request the kit, then ask for a quote on two specific products (one coin + one bar) to compare premiums.

Website: augustapreciousmetals.com

Phone: 1 (844) 615-4484

Location: California

Minimum investment: $50,000

CEO: Isaac Nuriani

Gold IRA support: Yes

Why we ranked it #3: Augusta is best suited to investors who want a high-touch, education-led process and are comfortable with the higher minimum. For the right person, the “premium” experience is the point.

Augusta is a selective gold IRA provider known for a high-touch education model and premium customer experience. They’re often a better match for investors with larger balances who want a slow, thorough, and explained approach before purchasing.

Questions to ask Augusta (to understand value vs cost)

- “What are the total first-year costs including custodian + storage, and what can be waived?”

- “Which products do you recommend for lower premiums (coins vs bars)?”

- “How does your buyback process work and what’s typical turnaround time?”

Best for

- High-net-worth investors and retirees

- People who want deep education before buying

- Investors comfortable with the $50k minimum

Not ideal for

- Smaller accounts under $50k

- Investors who want a quick, no-frills buy

Website: birchgold.com

Phone: 1-877-749-7738

Location: Iowa

Minimum investment: $5,000

CEO: Laith Alsarraf

Gold IRA support: Yes

Why we ranked it #4: Birch is often appealing if you want a lower starting minimum and broad product availability, while still getting help with rollovers and storage coordination.

Birch Gold Group is a well-known provider with broad product availability and a lower entry minimum than many competitors. It’s often a good match for investors who want selection and support without committing $10k+ immediately.

Questions to ask Birch (to keep costs tight)

- “What are my lowest-premium bullion options today (coins vs bars)?”

- “What are the annual custodian + storage fees for the storage setup you’re quoting?”

- “If I sell back, how is the buyback price determined?”

Best for

- Investors starting around $5k–$10k

- Those who want a wide selection of coins and bullion

- IRA rollovers with guidance and support

Not ideal for

- People who only care about the lowest possible premium

- Buyers who want to avoid any phone-based sales process

Website: americanhartfordgold.com

Phone: 1-800-462-0071

Location: California

Minimum investment: $10,000

CEO: Sanford Mann

Gold IRA support: Yes

American Hartford Gold is a large, well-known dealer with strong visibility and a big review footprint. Like many mainstream firms, you’ll want to compare bullion vs premium coin pricing and confirm the full fee schedule (custodian + storage) before funding an IRA.

Best for

- Investors who want a recognizable, high-volume dealer

- People who plan to compare product pricing carefully

- IRA rollovers where you want phone support

Not ideal for

- People who want a fully self-serve, online checkout experience

- Anyone not willing to ask about markups and fees in writing

Website: advantagegold.com

Phone: 1-888-501-9001

Location: Texas

Minimum investment: $10,000

CEO: Kirill Zagalsky

Gold IRA support: Yes

Advantage Gold is known for educational positioning and broad visibility. If you’re comparing them with other firms, focus on all-in annual IRA costs (custodian + storage + any maintenance), plus the premium you’ll pay on common IRA-eligible coins.

Best for

- Investors who want education and guided onboarding

- IRA rollovers where you want help with paperwork

- People comparing multiple custodians/storage options

Not ideal for

- Buyers who refuse any phone-based sales process

- People who only want the lowest-possible premium

Website: roslandcapital.com

Phone: 1-866-942-2962

Location: California

Minimum investment: $2,000

CEO: Marin Aleksov

Gold IRA support: Yes

Rosland is a long-running dealer with broad retail reach and a lower entry point than many IRA-first firms. If you’re IRA-focused, ask about custodian choice, storage partners, and exact premiums on the products you’re considering.

Best for

- Smaller starting amounts vs typical $10k minimums

- Buyers who want phone support and a known brand

- People comparing both cash metals and IRAs

Not ideal for

- Ultra-DIY investors who only want “lowest premium online”

- Anyone who won’t request pricing in writing

Website: americanbullion.com

Phone: 1-800-465-3472

Location: California

Minimum investment: $10,000

CEO: Nevtan Akcora

Gold IRA support: Yes

American Bullion is a long-time player in the Gold IRA category. If you’re comparing options, focus on the custodian fee schedule and the premium you’ll pay on a few standard IRA-eligible products.

Best for

- Investors who want rollover support through the process

- People starting around the $10k level

- Those who value phone-based guidance

Not ideal for

- Self-serve buyers who want transparent online pricing and checkout

- Anyone uncomfortable asking about markups

Website: goldalliance.com

Phone: 1-888-642-3314

Location: Nevada

Minimum investment: $20,000

CEO: Joseph Sherman

Gold IRA support: Yes

Gold Alliance is a Nevada-based firm and is often positioned around customer support. Because the minimum is higher, ask specifically about first-year total costs and get a quote for common bullion products to compare premiums.

Best for

- Investors who prioritize service and higher-touch support

- People with $20k+ to allocate

- IRA rollovers with more hand-holding

Not ideal for

- Smaller investors under $20k

- Anyone who wants to avoid phone calls entirely

Website: monex.com

Phone: 1-800-444-8317

Location: California

Minimum investment: $10,000

CEO: Louis Carabini

Gold IRA support: Yes

Monex is one of the oldest brands in the category and has been operating since the 1960s. If you’re comparing Monex with newer IRA-focused firms, make sure you understand how pricing is quoted, the buyback process, and any account-related fees.

Best for

- Investors who prefer established legacy brands

- People comparing multiple quote-based dealers

- IRA buyers who want help with setup and logistics

Not ideal for

- People who only want instant online pricing and checkout

- Anyone unwilling to request fee details up front

Website: goldco.com

Phone: 1-855-465-3472

Location: California

Minimum investment: $10,000

CEO: Trevor Gerszt

Gold IRA support: Yes

Goldco is a major name in the Gold IRA category and offers a broad range of IRA-eligible coins and bars. Because some firms emphasize premium coin offerings, always ask for bullion options + premiums, and confirm buyback process details.

Best for

- Investors who want a large, established IRA-focused firm

- People who want guided rollover help

- Buyers comparing coin selection and education resources

Not ideal for

- Anyone who won’t compare premiums across 2–3 dealers

- Ultra-DIY buyers who only want online checkout

Website: jmbullion.com

Phone: (800) 276-6508

Location: Texas (Dallas)

Minimum investment: None (order minimums vary by payment method)

CEO: Robert (Rob) Pacelli

Gold IRA support: Yes

JM Bullion is one of the largest online bullion retailers in the U.S. and is often appealing for buyers who want a lower barrier to entry. If you’re using an IRA, confirm exactly how their IRA program works with partner custodians, and compare product premiums + total annual IRA costs.

Best for

- Buyers who want broad inventory and a low starting barrier

- People comparing multiple bullion products quickly

- Investors who want to research and self-educate

Not ideal for

- People who want one dedicated rep guiding everything end-to-end

- Investors who don’t want to compare fees across custodians

What to look for in a gold investment company

- Reviews and ratings: Use them as a data point, but still ask hard questions about fees and premiums.

- Premiums and markups: Ask what percent over spot you’ll pay for each product. Compare the same product across 2–3 companies.

- IRA support: Confirm how they handle rollovers, paperwork, and storage coordination.

- Product mix: Know the difference between standard bullion, proof coins, and collectibles (premiums can be dramatically different).

- Sales transparency: Avoid pressure to buy high-priced collectibles that don’t match your goals.

- Buyback terms: Ask how they price buybacks and what the typical settlement timeline is.

Tip: Gold doesn’t pay dividends or interest. Ask about liquidity and buyback policies before committing.

If someone is pushing a “once in a lifetime” coin deal, that’s a reason to slow down and compare.

If you’re looking for a company not listed here, see Gold IRA Guide’s extended list:

Best Gold IRA Companies.

Gold Investment FAQ

What is a gold investment company?

A gold investment company is a dealer that sells physical precious metals (gold, silver, etc.).

Many also help facilitate precious metals IRAs by coordinating with approved custodians and depositories.

Are there fees or costs associated with gold IRAs?

Yes. Costs can include dealer premiums (markup over spot), custodian fees, storage fees, insurance, and transaction fees.

Always request a written fee schedule and compare at least 2–3 companies.

How long does a 401(k) or IRA rollover into gold usually take?

It depends on your current custodian/plan administrator and whether paperwork is complete.

Many rollovers land in 1–3 weeks, but some take longer.

Ask your dealer how they support paperwork, and ask your custodian what their typical processing window is.

What are the risks of investing in gold?

Key risks include price volatility, opportunity cost (gold produces no income), storage/security expenses for physical metals, and liquidity friction if selling during periods of stress. Diversification and a long-term view can help manage risk.

Are gold bars or gold coins better?

Bars often have lower premiums. Widely recognized bullion coins are popular for liquidity.

Proof and collectible coins can carry much higher premiums, so confirm what you’re buying and why.

What’s the best way to compare quotes from 2–3 companies?

Pick two identical products and request written quotes showing premium over spot.

Then compare the annual custodian + storage fees for the IRA structure being quoted.

This removes most of the confusion fast.

What percentage of a portfolio should be allocated to gold and silver?

There’s no one-size-fits-all answer. Some investors allocate a small portion as a hedge.

Your allocation depends on risk tolerance, time horizon, income needs, and broader diversification.

Should I store gold at home or in a vault?

Storing significant amounts at home can increase security and insurance concerns.

Many investors prefer professional vault storage, especially for IRA holdings which must follow custodial rules.

Should I use my IRA or 401(k) to invest in gold?

If you want physical metals inside a retirement account, you generally need a self-directed IRA structure with an approved custodian.

This can help avoid early withdrawal penalties, but fees and rules apply.

Amine Rahal (Writer)

Amine is an entrepreneur, investor and financial writer covering the U.S. economy, inflation, alternative investments, and cryptocurrencies.

He has been involved in the space for over a decade.

Lauren Brown, CFA (Reviewer)

Lauren has 13+ years of experience in wealth management and financial planning. She is a CFA charterholder with a Bachelor’s degree in Finance

and has worked with asset management firms advising high-net-worth clients.

by Lauren Brown | Feb 18, 2026 | gold

If you’re thinking about investing in gold or silver, especially for your retirement, Augusta Precious Metals is a company that often comes up. They’ve been around since 2012, and they focus mainly on helping people set up and manage precious metals IRAs. They’re all about making sure you’re well-informed before diving into investing. However, they may not be right for all investors. Keep reading to learn more…

Who is Augusta Precious Metals?

- Company: Augusta Precious Metals

- Company address: 8484 Wilshire Blvd #515, Beverly Hills, CA 90211

- Company’s phone: (844) 615-4484

- Company’s URL: www.augustapmira.com

- Products sold: gold and silver (coins and bars).

- Retirement accounts supported: IRA, 401k, SEP, TSP, and more.

Augusta Precious Metals is a gold investment company that specializes in accounts that are known as precious metal IRAs (see this article to learn more about these accounts). The team behind the company leads with a clear focus on integrity and customer service.

Management Team (Augusta Precious Metals)

Who are the key members of the company?

- Isaac Nuriani – Founder & CEO

Isaac Nuriani, CEO of Augusta Precious Metals

As founder of the company, Isaac Nuriani is also its current CEO. With a background in economics, he established the company with a vision to help people diversify their retirement portfolios through precious metals. Nuriani emphasizes educating investors and maintaining transparency, aiming to build long-term relationships based on trust and reliability.

- Devlyn Steele – Director of Education

Devlyn Steele, Director of Education

Devlyn Steele plays a crucial role in the company by leading the educational efforts. With over a decade of experience in financial services, Steele is responsible for helping customers understand the market dynamics and benefits of investing in gold and silver. He’s often the face behind the company’s webinars and educational videos, breaking down complex financial topics into understandable insights.

- Howard Smith – Chief Financial Officer (CFO)

Howard Smith, Director of Finance

Howard Smith brings extensive experience to the company in the areas of corporate finance and operations. His focus is on ensuring Augusta maintains a solid financial structure while effectively managing costs and operations. This focus aligns with the company’s mission to provide clear and transparent fee structures to its customers.

Overview of Augusta’s Reputation & Reviews

Here’s a quick overview of the ratings and reviews the company has received from its customers:

What Augusta Offers

- Gold & Silver IRAs: This is their bread and butter. They help you roll over your existing retirement accounts (like a 401k) into IRAs backed by physical gold or silver.

- Buying Direct: You can also buy gold or silver directly with cash if you just want to hold onto physical metals.

- Education: One of their key selling points is the way they prioritize educating you about investing in precious metals. They’ve got guides, videos, and even one-on-one webinars.

The Good Stuff

- Focus on Education 📚: Augusta puts a big emphasis on making sure you understand what you’re investing in. They offer in-depth resources and straightforward explanations – keeping you well-informed at every step. Devlyn Steel conducts educational conferences with new investors to explain everything they need to know about their potential gold investment.

- Transparent Fees 💡: No one likes hidden fees, and Augusta seems to get that. They’re pretty upfront about what you’ll be paying, which is super important when you’re dealing with Gold IRAs that have storage and management costs.

- Dedicated Support 👥: You get a personal representative to guide you through the whole process, and a lot of people seem to appreciate having a single point of contact for all their questions.

- Solid Ratings ⭐: They’ve got good ratings across the board from places like the Better Business Bureau (BBB) and Business Consumer Alliance (BCA). This usually means customers trust them and encounter fair treatment.

- Buyback Option: If you ever want to sell your gold or silver, they offer a buyback program, which could be helpful if you need to cash out.

The Not-So-Great Parts

- High Minimum Investment 💰: They require you to invest at least $50,000 to get started, which can be a deal-breaker if you’re not looking to invest a large amount.

- Higher Fees on Premium Coins: Augusta sells both standard and premium bullion coins and bars. Premium coins come at higher premiums (obviously) so be aware of that.

- Limited Options: Augusta focuses only on gold and silver, so if you’re hoping to diversify with other metals like platinum or palladium, you’re out of luck.

- Delivery Delays 📦: During periods of high demand, there have been a few reports of delays in getting physical metals delivered. Not a huge issue, but something to keep in mind if quick access to your assets is important to you.

What About the Fees?

- Setup & Custodial Fees: They’re pretty clear about their fees for setting up and managing your Gold IRA. Still, it’s always a good idea to double-check with them directly.

- Storage Fees: Since your gold or silver is stored securely, there are annual storage fees. They use segregated storage, keeping your assets separate and giving you extra peace of mind.

What Do Customers Say?

- Positive Feedback 👍: Most reviews talk about how transparent and knowledgeable the staff are, and how much they appreciate the company’s educational approach. People feel more confident and well-prepared in their investment decisions.

- Negative Feedback 👎: The main complaints are about the high minimum investment and occasional delivery delays. While these aren’t widespread, some customers mention the issue.

Bottom Line

If you’re looking for a company to help you diversify your retirement savings with gold or silver, Augusta Precious Metals has a good reputation. They’re big on transparency and education, which can be reassuring if you’re new to this kind of investment. Just keep in mind that they have a high minimum investment requirement, and their focus is strictly on gold and silver.

Before making any big decisions, it’s always smart to think about your goals and budget. And, if you’re unsure, a chat with a financial advisor might help you figure out if this fits into your overall strategy.

Augusta Precious Metals – FAQ

1. Is Augusta Precious Metals Legitimate?

Yes, Augusta Precious Metals is a legitimate company with physical offices and thousands of customers. They have a solid reputation for customer education and, perhaps more importantly, transparency. The Better Business Bureau (BBB) as well as the Business Consumer Alliance (BCA) both reflect high ratings for the company which is also ranked well by TrustLink.

2. Pros and Cons of Augusta Precious Metals

- Pros: Strong focus on customer education, transparent fee structure, highly rated customer service, and positive customer feedback.

- Cons: High minimum investment requirement ($50,000), higher premiums on certain coins, limited range of precious metals (primarily gold and silver), and occasional delivery delays reported.

3. What Are the Fees and Prices for a “Augusta Precious Metals IRA?”

Just like any gold dealer, Augusta charges premiums/spreads on the coins and bars you purchase from them. These spreads can range from 5% to 30% (or more!). The exact cost depends on both the rarity and type of coin. Ask about the breakdown of their fees based on the coins and bars you are interested in. Also, when you open an Augusta Gold IRA, there are fees for account setup, storage, and custodial services. You may obtain a waiver on these fees, depending on whether they have a promo when you call them. These annual fees vary but are generally a flat yearly rate ranging between $200 and $300, so it’s essential to confirm with a company representative. Augusta is known for its clear and upfront fee structure, so there are no hidden surprises.

4. Is There a Minimum for Investment with Augusta Precious Metals?

Yes. The minimum investment for an IRA account with Augusta Precious Metals is typically (around) $50,000.

5. Are There Common Complaints With Augusta Precious Metals?

The most common complaints relate to the high minimum investment amount and occasional delays in delivering physical metals during high-demand periods. Some customers also wish for a broader selection of precious metals beyond gold and silver.

6. Is There Free Shipping With Augusta Precious Metals?

Yes, Augusta often provides free shipping for precious metals purchases, particularly for IRA accounts. It’s a good idea to confirm this detail with a representative as promotions can vary.

7. Does Augusta Precious Metals Have A Refund Policy?

Augusta offers a buyback program, allowing customers to sell their metals back at a competitive rate. However, refund policies can depend on market conditions and specific agreements, so it’s essential to discuss this with them directly, BEFORE you place a purchase or open a Gold IRA account.

8. How Does Augusta Precious Metals Compare to Goldco or American Harfford?

Augusta, American Hartford and Goldco all offer Gold and Silver IRAs with a focus on portfolio diversification. Augusta is known for its educational approach and transparency, while Goldco gets recognition for its broad range of products and personalized services. Your investment needs and preferences will dictate your choice. We recommend you contact all of them and compare their prices and offerings.

9. Is There a Lawsuit Against Augusta Precious Metals?

There are no significant public records or updates on lawsuits specifically against Augusta Precious Metals. However, investors should always perform their due diligence and review the company’s history and customer feedback. We recommend you check PACER and the SEC’s databases and search for the company name there for the most recent data.

10. How Do I Set Up a (Gold or Silver) IRA through Augusta Precious Metals?

To set up an IRA, you’ll need to speak with an Augusta representative who will guide you through the rollover process. They will help you move funds from your existing retirement accounts into a self-directed IRA AND aid in selecting the type of precious metals to hold.

11. Joe Montana and Augusta Precious Metals – How Are They Related?

Joe Montana, the legendary NFL quarterback, is a paid brand ambassador for Augusta Precious Metals. He reportedly became a customer after his financial advisors recommended Augusta, and he has since publicly endorsed the company.

12. Does Augusta Precious Metals Offer Promo Codes or Discounts?

Occasionally, Augusta may offer promotions or discounts on services, but these can vary. Speak to a representative directly about any ongoing promotions.

13. Is it Safe to Invest With Augusta Precious Metals?

Augusta emphasizes security and transparency in its dealings. It’s important to work with a trusted company when dealing with Gold IRA accounts. See this notice from the CFTC to learn more about some of the scams that unscrupulous gold companies have been using to lure investors. They have a compliance department and offer insured and segregated storage options for their precious metals and are generally a trusted name in the industry.

14. How Many Years Has Augusta Precious Metals Been Operating?

Augusta Precious Metals has been operating since 2012, focusing on providing secure and transparent precious metals investment options.

To learn more about Augusta, we recommend that you request their free gold kit.

.

by Amine Rahal | Sep 13, 2025 | Definitions, gold

Disclosure: The information on this page is for education only and is not financial, investment, or tax advice. CPIInflationCalculator.com may earn commissions from partner links. Precious metals carry risk, including loss of principal. Past performance does not guarantee future results. Please consult a licensed financial advisor and a tax professional before acting.

If inflation is eating away at your portfolio, one investment you may have looked at is precious metals. Physical metals are known to be a good hedge against inflation and paper markets, but which precious metal should you invest in: gold or silver? In this article, we’ll cover the pros and cons of both to help you decide on your precious metal allocation. First, let’s look at this comparison table:

| Factor |

🟡 Gold |

⚪ Silver |

| Market Value |

Higher price per ounce |

Much lower price per ounce |

| Volatility |

Lower volatility, more stable |

Higher volatility, more prone to price swings up or down |

| Liquidity |

Highly liquid, easier to buy and sell in large quantities |

Liquid but may have less demand in large quantities |

| Industrial Use |

Limited use compared to silver |

Significant industrial demand (electronics, EV, solar energy, tech, etc) |

| Supply and Demand |

More stable due to its primary use as a store of value |

Fluctuates based on industrial demand and economic cycles |

| Hedge Against Inflation |

Strong hedge, tends to rise during infla |

For me, the highlight of this table is how easy it is to store gold. An $80k gold bar can fit in your pocket, which makes it very convenient, cheap and easy to store. This factor greatly contributes to the fact that gold is an amazing store of value. However, this also makes it very difficult to “spend”. In a scenario where the dollar is worth nothing and you want to use your precious metals as currency for everyday expenses, silver might be a better choice.

Gold: The Classic Choice

Gold investing goes back thousands of years. Virtually every holy book mentions it. Now, why should you consider gold? For the following reasons:

- Stability: Almost every known civilization has valued gold for thousands of years, and even now, people often see it as a safe haven during economic uncertainty. Its price tends to be more stable over time.

- Inflation Hedge: History has shown that when the cost of living rises, gold prices often increase too. This makes it a good option for preserving your purchasing power during high-inflation times.

- Global Acceptance: Gold is recognized and valued worldwide. If you ever need to sell, it’s generally easy to find a buyer, especially if you have recognized bullion coins and bars like American gold Eagles or Canadian Maple Leafs.

- Less Volatility: Gold prices don’t fluctuate as wildly as some other investments, which can make it a calmer ride for investors.

Things to keep in mind:

- Higher Cost: Gold is more expensive per ounce than silver. This means you’ll need more money upfront to invest. Also, each gold investment company has different fees, with some charging very high premiums. We encourage you to shop around. Look for a company with competitive prices for their gold coins and bars.

- Slower Growth Potential: Because it’s more stable, you might see slower gains compared to more volatile investments.

Silver: The Dynamic Alternative

Silver is the most conductive metal on earth, which makes it needed in multiple industries, including Electric Vehicles, Electronics, Medicine and many more. Its various uses mean that its value goes beyond its investment potential. In a nutshell, you should consider investing in silver because:

- Affordability: Silver is much cheaper than gold. Why is that helpful? It allows you to start investing with a smaller amount of money.

- Industrial Demand: As we covered earlier, silver is used in many industries from electronics to EVs to solar panels. This can drive up demand and potentially its price.

- Growth Potential: Silver prices can rise quickly, offering the chance for significant gains if the market moves in your favor. If being the key word.

Things to keep in mind:

Making Your Decision

Before deciding on whether you should buy gold or silver as a hedge against inflation, consider your goals and comfort level:

- Are you looking for stability and a long-term store of value? Gold might be the better choice for you.

- Are you open to taking more risk for the chance of higher returns? Then silver could be more up your alley.

- Do you have a smaller budget to start investing? Silver allows you to enter the market without needing a large sum of money.

Now, how about both?

- Diversification: Investing in both gold and silver can help balance your portfolio. Really! Gold can provide stability. Silver offers growth potential.

- Hedging Bets: Holding both metals means you’re not putting all your eggs in one basket.

Final Thoughts

Ultimately, the choice between investing in gold vs silver depends on your individual financial situation, investment goals, and how much risk you’re comfortable taking on. It also depends on your understanding of the pros and cons of both metals. Do you believe the pros of one outweigh the pros of the other? There is no single right answer. Our final thoughts are:

- Do Your Research: Look into current market trends, historical price movements, and forecasts.

- Consult a Professional: It might be helpful to talk to a financial advisor who can offer personalized advice.

- Think Long-Term: Precious metals are generally considered long-term investments.

As always, we would like to remind you that investing always comes with risks, and there’s no guaranteed return. But with careful consideration and planning, you can make a choice that aligns with your financial goals. Always speak to your financial advisor before making any investment decision. Understand that past results don’t guarantee future returns. Invest wisely. Also, given the inflation we had to endure in the last few years, make sure you analyze your financial situation fully to determine whether you should be investing in a new asset class like precious metals. You should NEVER use debt or credit to buy physical metals or invest in anything else. If you’re in high debt, we recommend looking at different debt relief options to see how you can alleviate your debt, before thinking about investing.

Gold vs Silver: Frequently Asked Questions

1) Should I dollar cost average or wait for dips?

I prefer a simple plan. Dollar cost averaging removes the guesswork. If you enjoy timing, you can blend DCA with small buys on pullbacks.

2) Coins, bars, or rounds. What is best?

Coins from major mints are the most liquid and carry higher premiums. Bars are cheaper per ounce and efficient for larger amounts. Rounds are private mint products that can be cost effective but may resell for a bit less.

3) Why do premiums over spot vary so much?

Brand, format, and demand drive premiums. Small pieces cost more per ounce to make and ship. In stressed markets premiums can spike even if spot is flat.

4) How do I verify authenticity?

Buy from reputable dealers, keep assay cards and serial numbers intact, and use basic checks like weight and dimensions. Higher end tools include XRF and specific gravity tests. When in doubt, ask a dealer to test.

5) Home safe, bank box, or depository?

Home storage is convenient but needs a real safe and insurance. Bank boxes are discrete but not insured by the bank. Depositories add professional security and insurance for a fee. I like splitting storage for redundancy.

6) How easy is it to sell quickly?

Gold is the easiest. Most large dealers post live buy prices and fund fast. Silver is liquid but bulkier to ship and may have wider spreads. Keeping popular products helps.

7) What moves gold and silver prices day to day?

Real interest rates, the dollar, central bank flows, and risk sentiment matter for gold. Silver adds an industrial layer, so manufacturing trends and solar demand can swing it harder.

8) Are ETFs a good substitute for physical?

ETFs add convenience, tight spreads, and easy rebalancing. Physical removes some counterparty risk and tracks spot after premiums. Some investors hold both to balance convenience and sovereignty.

9) Can I put metals in an IRA?

Self directed IRAs can hold certain bullion that meets fineness rules. Numismatic coins usually do not qualify. Custodian, storage, and trading fees apply. I suggest confirming details with the custodian before you buy.

10) How are taxes handled when I sell?

Tax treatment depends on jurisdiction and product type. Keep purchase records and talk to a tax professional about reporting and capital gains. I avoid giving specific tax rates here since rules change.

11) What percentage of a portfolio makes sense?

That comes down to risk tolerance and goals. I often see ranges from a small single digit allocation to a mid single digit allocation. The right number depends on your total plan, not a rule of thumb.

12) Is “junk silver” still useful?

Pre 1965 US 90 percent silver coins can be a low premium way to get fractional silver. Liquidity is good with dealers and many stackers know the melt value.

13) Does silver tarnish matter?

Tarnish does not change metal content. For aesthetics, store in dry, cool conditions with anti-tarnish strips or capsules. Bars and rounds are fine to leave as is if you plan to hold long term.

14) Are kilo bars better than 1 oz coins?

For low premiums per ounce, kilo bars win. For flexibility and resale, 1 oz coins win. Many investors mix sizes so they can sell in smaller chunks when needed.

15) What if premiums blow out during a crisis?

It happens. Retail supply can get tight and premiums climb. Having some metal on hand before you need it helps. ETFs can fill short term gaps if you accept market risk and fund rules.

16) Do central banks buy silver too?

Central banks focus on gold as a reserve asset. Silver demand is driven more by industry and investors, which is one reason silver is more cyclical.

17) How often should I rebalance?

Pick a cadence you will follow. Quarterly or annual checkups are common. If metal weights drift far from your target, trim or add to get back in range.

18) Are there ethical or sourcing labels to look for?

Many large refiners follow responsible sourcing standards from industry bodies. If this is important to you, ask dealers which refiners and programs they support.

19) Can I travel with coins or bars?

You can, but know your local reporting rules and security risks. I keep travel minimal and use insured shipping or a depository transfer when possible.

20) Will gold or silver help if inflation cools?

They can still diversify a portfolio even when inflation cools. Drivers shift toward real yields and risk sentiment. The long term case does not rely on inflation alone.

by Sarah Bauder | Dec 10, 2019 | gold

Considering that precious metals such as gold have enjoyed a bullish market, there’s no better time than now to invest. An easy way for investors to keep abreast of the price of the glittering metal is with a gold calculator. The question that arises is gold and inflation. In this article, 4 experts discuss whether gold is a good inflation hedge.

Gold Might Be A Valuable Addition To A Portfolio, But Not Because It Is A Good Hedge Against Anything

“In times of economic uncertainty, many advisors suggest gold as a hedge, especially against inflation. In other words, the expectation is that holding gold in the portfolio will compensate for other assets declining in value. Luckily, we don’t need to leave this question to opinion. Instead, we can answer it based on quantifiable facts.

The Federal Reserve Bank of St. Louis maintains a site nicknamed FRED, providing time series of almost any aspect of the U.S. economy. As a measure of inflation, we can use the Consumer Price Index for All Urban Consumers.

By dividing the gold fixing price by the consumer price index, we can inflation-adjust the gold price. With the data available on FRED, we can do so back to 1968. If gold was a good hedge against inflation, we should see the resulting chart continuously trend up.

Unfortunately, this is not what we see. Instead, we can identify the following course periods:

– from 1968 to 1980, gold was by far outperforming inflation

– after 1980, gold prices fell by 75%, and it took until 2011 for prices to recover

– from 2011 to 2015, inflation-adjusted gold prices fell by 30%

– since 2015, gold prices have been mostly flat

Interpreting these results, we find that over the 50-years from 1968 to 2019, gold prices rose about six times faster than inflation. This single finding supports the idea of gold being a good hedge against inflation. However, there have been long periods of underperformance: for about half the time throughout the past 50 years, gold prices were not only lagging inflation but declining at high rates.

In summary, we believe that gold might be a valuable addition to a portfolio, but not because it is a good hedge against anything. Instead, gold can have a place in an investor’s portfolio because its price is mostly uncorrelated to any other economic factor. However, investors considering gold should have a long investment horizon, and only allocate a small percentage of their funds to gold.”

Felix Bertram, Owner, Investment Adviser Representative, Bertram Solutions LLC

Since The US Dollar Is Based On Gold, That Makes Gold A Good Inflation Hedge

“Since the US dollar is based on gold, that makes gold a good inflation hedge because if the US starts printing too much money and dollars lose their value, anyone who has gold will retain its value even if the dollar becomes worthless from over-printing and inflation.”

Stacy Caprio, Deal Scoop

Gold Isn’t A Hedge Against Inflation

“Gold isn’t a hedge against inflation. It’s a hedge against volatility.

Gold peaked in the early 1980s and then declined for many years. Inflation grew while the price of gold fell. When the price of gold reached its nadir, the stock market was booming in the late 1990s. Then, as the markets corrected in the early 2000s, gold began its ascent. The price of gold seems to do well when people are not making money in financial markets and not when inflation is actually rising.”

Holmes Osborne, CFA, Osborne Global Investors

You Never Really Know What Is Going To Be An Inflation Hedge Until After The Event

“Up until 2007 the gold price largely tracked the increase in Federal Debt, but since then the relationship has largely broken. Initially, the gold price outperformed the increase in US debt, but more recently, it seems to have underperformed.

The million-dollar question being why? And will all this money printing lead to inflation.

With bonds yields being so low, invariably negative, you’d expect inflation. But it’s not happening. One would also expect gold to do well – let’s say, better than it has. But that clearly has not happened.

But is that about to change?

At Mines & Money last week I spoke with a portfolio manager at a US pension Fund. Although I know he’s always been an advocate of gold, he told me that more and more fund managers were looking at the yellow metal. Increasingly viewing it as a “safe haven asset”.

This does not seem to have fed into the gold market yet, but that doesn’t mean it won’t. Time to take a look at the history books.

Appreciate they 1970’s was a long time ago, but if you compare the bull market back then, with the one we’re in now, two things really jump out at you.

Firstly, how the gold price over the past 20 years or so has largely mirrored what happened in the 1970’s and secondly, if the gold price were to take off AND history was to repeat itself, the gold price could go A LOT HIGHER.

Right now, with the increasing debt and general uncertainty in the World across the World, do you think it’s ridiculous to have at least 1% of your wealth in gold? I don’t

You never really know what is going to be an inflation hedge until after the event. But right now, I think gold should be part of a solution – not THE solution. Because I don’t think there is A solution.”

Simon Popple, Brookville Capital

Taking into account the current uncertainties and volatility apropos of the global economy, gold is a good addition to a diversified portfolio. For those US investors interested in investing in gold with an IRA, have a look at the top Gold IRA companies. In addition, for those who already own gold and are considering storing it offshore, have a look at the top companies for your offshore gold investment.

by Ryan Barnes | Mar 25, 2015 | CPI, Definitions, gold, Inflation

The U.S. economy got a little economic boost today with a stronger-than-expected CPI reading for February, and a strong Purchasing Manager’s Index (PMI) that continued to project GDP growth.

Headline CPI and core CPI both came in 0.2% higher than January, as slight price hikes at the pump for refined products balanced out a general breather in the declines in some of the base commodities. The headline numbers had been tracking negative for the past three months, which everyone was pretty much ok with chalking up to crude oil. Just so long as GDP growth came in respectably, there wasn’t any reason to panic.

But core CPI (ex-food and energy costs) was already lagging behind Fed goals of around 2%, and already in the midst of sending deflationary ripples up the global goods chain, into…well, just about everything.

Muddled Waters for First Rate Hike

It’s created a tense chess match between investors and the Fed the past few weeks. It started just after the stellar (as in +295,000) February jobs report last month, when the consensus started to form that the Fed would have to act sooner rather than later in creating a interest rate normalization cycle.

The key first step of that cycle is getting us off the floor of zero percent rates – a stance that doesn’t befit a growing economy and presents what Yellen herself has called an “asymmetrical risk”.

U.S. Definitely Growing…But How Much?

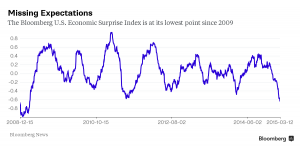

Just as soon as we seemed to have some headway into a summer rate increase, nearly every economic indicator in the U.S. started been printing well below analyst estimates. In fact, the depth of our misses has hit a multi-year high, according to Bloomberg analysis:

In light of this reversal, both investors and the Fed have had to take stock of things. First quarter GDP estimates continue to be ratcheted down – from the 2.5% – 3.0% level I highlighted last month (a number that was freshly lowered at the time) to an average Q1 GDP estimate of about 1.5% today.

Cranky Markets are Volatile Markets

It’s why we’ve seen a spike in volatility around every asset class – fixed income, forex, commodities, and equities have all been bumping around trying to align their compass to the next clear trend line. Would the Fed remove “patient” in the March FOMC meeting? Was September the new June (for the first rate hike)? Was 2015 off the table entirely?

Answering these questions is challenging enough in isolation, but it’s been exacerbated by the stunning rise the the USD index, which alters true price action in commodities and long bonds. The surging U.S. dollar is a de facto rate hike. It lowers the cost of imports dramatically (a deflationary force), and it makes our exports more expensive overseas.

And while the realities of pricier U.S. exports certainly hurt some companies more than others, the simple fact is that close to 50% of the total revenues of the S&P 500 member companies is derived in a currency other than the U.S. dollar.

2014, Part Deux?

It’s quite astonishing how much the first quarter of this year is looking like the first quarter of last year. Tick by tick, indicator by indicator, we seem to be replicating that market environment.

This time last year we were watching interest rates hit new lows, but convinced the party had to end any moment – inflation was coming, and we needed to position ourselves away from fixed income and into equities, gold, and other commodities. Fixed income turned out to deliver stronger returns than even equities did.

GDP looked to be on track for a good start to the year, but then a bout of really bad whether caused us to actually contract as an economy in Q1. Most of the top analysts said “don’t worry, we’ll be strong in the back half of the year”, and sure enough we were. The U.S. turned in over 4.5% growth in the next two quarters.

Looking around today, it’s much the same setup – so far. The key differences between then and now are this:

1) the unemployment rate is lower than last year; we have clearly moved close enough to full unemployment in the Fed’s eyes that it’s no longer an impediment to a rate increase. That box is checked off.

2) the USD is much stronger (10-20% or more) against every major global currency. As I’ve discussed, this move alone is the equivalent of a 25-50 bps rate hike.

In fact, if the dollar hadn’t been zooming so hard the past six months, there’s a chance the Fed would’ve put a token 25bp hike out there last week. Instead, Yellen reminded us that the Fed isn’t there to make things easy for investors, saying the Fed “can’t provide and shouldn’t provide” certainly to markets when it comes to the timing of rate hikes.

We don’t seem to be in any danger of that.