Andrew

Andrew McCarthy is an expert in all things inflation. He has a Bachelors in Economics and has been working in the finance industry for over two decades.

by Andrew | Jul 17, 2015 | BLS, CPI, Definitions, In the news, Inflation, Monthly CPI Updates

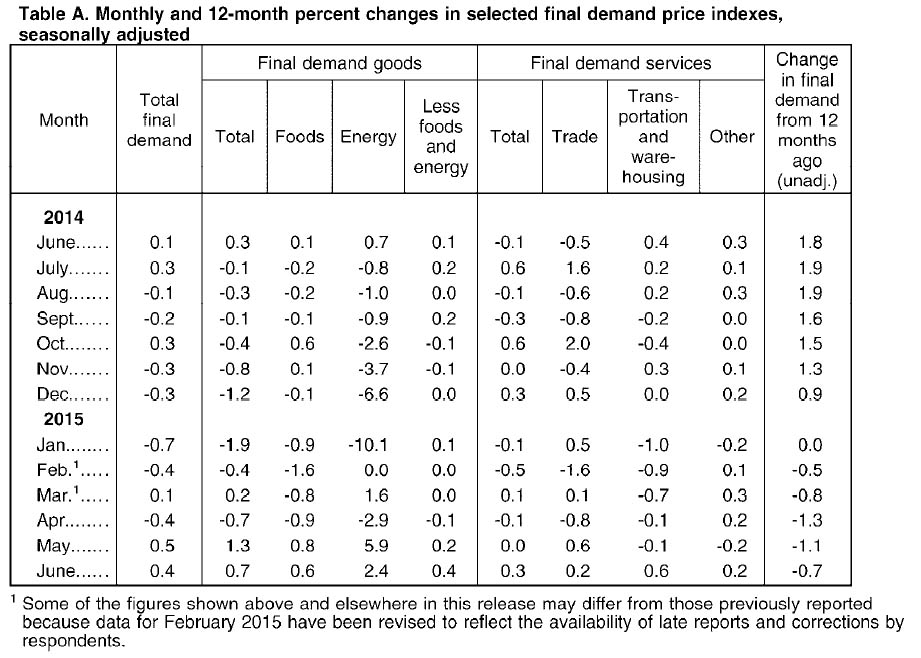

U.S. consumer prices increased for the fifth consecutive month in June, led higher by a rebounding price of gasoline, although there was nothing in the latest release which should pose any immediate alarm for markets or consumers at large. The latest report from the BLS reported an overall increase in headline inflation of 0.3% month on month – an increase that was inline with nearly all economists polled prior to the announcement. Looking at the headline number on an annualized basis, inflation rose 0.1 percent In the 12 months through June, following an unchanged reading for the month of May.

Gasoline prices rose 3.4% month on month, following a 10.4 percent surge in May. Given the recent volatility in crude oil prices and inventory data in July, there could be scope for the influence of rising gas prices to subside in coming months. Oil is currently trading within the $50-60 / bbl range, well below the levels seen in May and June.

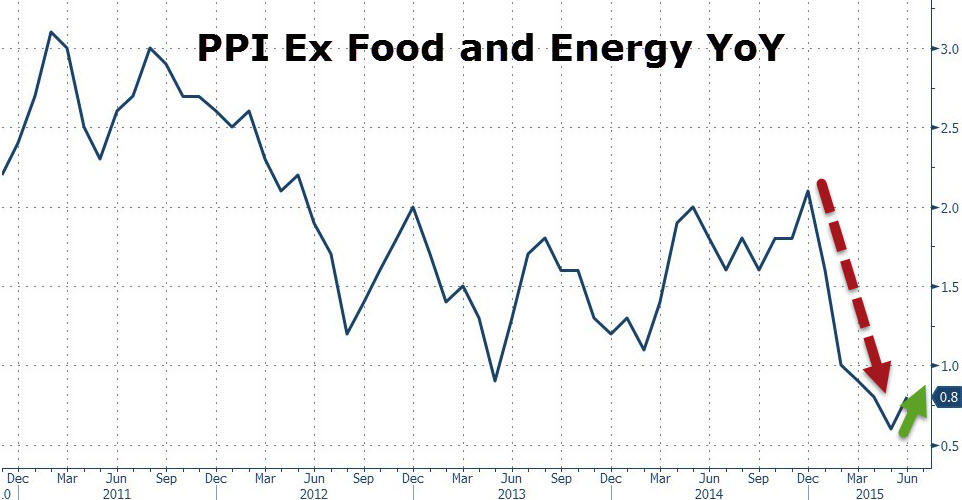

Core CPI, which excludes food and energy related costs, increased 0.2 percent month on month following a rise of 0.1% previously. On an annualized basis, core CPI has now risen 1.8 percent.The June reading continues to highlight just how tame the inflationary environment is within the US economy at present. The strong dollar is helping to keep a lid on inflation by reducing the price of imports and wholesale costs. The strong US dollar has been been spurred partly by a flight to safety due to concerns in Europe and China, and partly by the market’s anticipation of a Fed rate hike later this year. We should expect to start hearing comments regarding the damaging effects of the stronger dollar by Fed officials in the weeks and months ahead should this trend continue.

The food index posts largest increase since September 2014

The price of food increased 0.3% in June, largely to an ongoing shortage in wholesale eggs which has caused a sharp jump in retail egg prices across the nation. Egg prices jumped 18.3% in June, the largest monthly gain since August 1973. Elsewhere, the index for meats, poultry, fish, and eggs rose 1.4 percent in June, with the beef index rising 0.9 percent. Food prices are likely to remain elevated in the coming months as the aftermath of the bird flu epidemic works its way through the supply chain. Wholesale food costs have been consistently increasing in PPI surveys, and these costs are likely to make their way down to the consumer in the weeks and months ahead.

Medical Price Inflation starting to cool off

Medical related inflation cooled in June which will be a welcome deviation from the overall trend in 2015. The price for Medical Care Services fell -0.2% in June and the prices for Medical Care Commodities remained unchanged month on month. Health care costs have been one of the largest contributors to inflation over the past 12 months, with both indices rising 2.3 percent and 3.3 percent respectively.

Rent Prices continue to Climb Higher

The shelter index climbed 0.3% in June, and 3% on an annualized basis as the supply of housing continues to shrink in key regions. Rent increases are also amongst the largest contributors to overall inflation in the United States within the past 12 months.

Outlook for Rates

This month’s CPI data contains no surprises, and the relatively tame reading in the core number on the back of the strong US dollar will likely stick in the minds of Fed officials in the weeks ahead. Globally, sentiment continues to wane dramatically given the continued turmoil in Greece, and increasingly China. While Greece appears to be on the verge of some sort of political settlement, the headline risk remains. In China’s case, there is a very real danger of investor sentiment turning, which could spell disaster for emerging markets overall. Latin American and South East Asian markets look at particular risk, especially on the currency front. The fate of these regions would be sealed in no uncertain terms should the Fed raise rates, and it is for this reason that it appears increasingly unlikely that the Fed will raise by year end, despite all of their rhetoric and expressed intention to do so.

by Andrew | Jul 15, 2015 | Definitions

US producer prices rose for the month of June, comfortably beating analyst expectations and rising by the fastest pace in nearly three years according to data just release by the Bureau of Labor and Statistics. Surging prices for gasoline helped lift input prices across the board, and may signal the deflationary spiral which has been affecting both the consumer and producer markets for several months may be finally beginning to abate. The BLS reported producer price index for final demand increased 0.4 percent versus analyst expectation of 0.2%, and a print of 0.5% last month. The latest data builds on gains from May, and will be a welcome waypoint for those concerned about deflation taking root within the economy, although with economic tensions on the increase globally, it appears to soon to call victory in this regard.

Rising Gasoline Prices Continue to Push Prices Higher

Rising gasoline prices, which rose 4.3 percent in June, accounted for nearly thirty percent of this month’s increase in prices for final demand goods. June marks the second month of surging gas prices following a 17 percent increase in May. The price of food input costs also rose, with the price of eggs in particular remaining elevated due to the bird flu outbreak which has led to a drastic cut in supply across the United States. Food prices rose 0.6 percent with wholesale eggs soaring 84.5%.

Yellen Reiterates the Fed’s Desire to Raise Rates

Elsewhere on the inflation related front, Fed Chairwoman Janet Yellen appeared before the House Financial Services Committee in Washington and reiterated the Fed’s intention to raise rates should the economy continue to “evolve as expected” in the coming months. In her statement Yellen went onto say that she expected growth to “strengthen over the remainder of this year and the unemployment rate to decline gradually”. The Fed has made no secret that any rate increase will be highly dependent on supporting data – most of which has been conflicting at best in recent months.

Yellen’s comments may fall on increasingly sceptical ears within the market, as a combination of increasingly disruptive forces worldwide begin fusing themselves into the perfect financial storm. Ongoing turmoil and potential contagion within Greece is likely to suppress European economic activity for the rest of the year as politicians lurch from one unworkable scenario to the next. China is also beginning to spark real concern amongst investors and could trigger a worldwide slowdown in the months ahead.

Canada throws in the Towel

The knock on effects from China are already being felt, with the Bank of Canada unexpectedly slashing its GDP target from 1.9% to 1.1%. Second quarter GDP in particular was axed from 1.8% to -0.5%. In what could be the first signs from a western central bank of just how bad things are becoming globally. As part of the announcement the Bank of Canada cut benchmark interest rates to 0.5% – a record low.  The BOC cited collapsing investment in the oil and gas sector as one of the main drivers of the slowdown, with investment forecast to shrink by up to 40% this year alone.

The BOC cited collapsing investment in the oil and gas sector as one of the main drivers of the slowdown, with investment forecast to shrink by up to 40% this year alone.

With Canada just a hop, skip and a jump away from the US border – the difficulty facing the Fed going forward is clear – they simply cannot raise rates when the rest of the world is attempting to ease. The results will be a full on run on most commodity and emerging market currencies.

CPI Preview for June

Consumer prices are expected to follow producer prices higher when they are announced on Friday – with rebounding food and energy costs likely to boost overall prices for the average American household. Headline inflation is forecast to increase 0.3% month on month, with core inflation expected to post a similar increase of 0.2%. Prices overall are likely to have increased 0.1% on an annualized basis, which if correct, would be an important psychological barrier to overcome as year on year data has been negative or flat throughout 2015. Core inflation will be the watched closely, with the market forecasting an increase of 1.8% on an annualized basis.

Regardless of the number on Friday, it is becoming increasingly obvious that conventional monetary policy is running out of steam and markets are not likely to be happy.

by Andrew | Jul 10, 2015 | In the news, Inflation

Rising tensions within global financial markets were the dominant concerns among Fed officials according to minutes just released from their June policy meeting, leading to yet another delay in the Fed’s widely anticipated normalization of interest rate policy. Uncertainty surrounding the future of Greece and ongoing market weakness in China triggered a cautious tone among most members, although signs of continued strength in the domestic economy, especially the labor and housing markets provided enough signs encouragement for other members to favor a rate hike in the near future.

The tug of war between these two forces will be the dominant theme for Fed watchers going forward, and signs of either beginning to dominate in the weeks ahead should offer some more concrete insight into the timing of the Fed’s next move.

In the Fed’s own words:

“Many participants emphasized that, in order to determine that the criteria for beginning policy normalization had been met, they would need additional information indicating that economic growth was strengthening, that labor market conditions were continuing to improve, and that inflation was moving back toward the Committee’s objective.”

The Fed is essentially adopting a “wait and see” approach before pulling the trigger on a rate hike which might seem premature in hindsight.

The Good – Labor Market Continues to Pick Up

On a positive note, job creation and improved employment prospects according to official figures has buoyed the Fed’s expectations for wage growth to pick up for the rest of the year. Recent consumer confidence surveys echo the Fed’s optimism, with average consumers hopeful of real wage increases in the coming months. Increased wage growth would help boost the domestic economy going forward, and the Fed will likely keep monitoring the retail sales data and employment figures closely in the weeks and months ahead for signs of a solid platform of growth emerging.

The Bad and The Ugly – Greece Weighs on Fed Outlook

Dissecting the June minutes in more detail reveals the Fed’s growing concern about the disruptive influence of overseas market turmoil arriving on domestic shores. Greece clearly weighed on policy makers minds, with particular focus on the contagion “Grexit” would cause for European financial institutions, and the domino effect this could have on US banks.

The Fed didn’t mince any words in this regard.

“[M]any participants expressed concern that a failure of Greece and its official creditors to resolve their differences could result in disruptions in financial markets in the euro area, with possible spillover effects on the United States.”

An important point to note is that the June FOMC policy meeting took place well before the most recent turmoil in Greece really flared up. It’s almost certain that the Fed would be adopting even softer language surrounding Greece given recent events. The Chinese stock market has also imploded in recent weeks, and is likely to overshadow even Greece in the near future as the biggest threat to worldwide economic stability. In recent weeks China has employed a variety of increasingly desperate measures to help slow the stock market decline, but neighboring countries in the Asia Pacific region will be looking on anxiously for signs of contagion in the near future.

Inflation continues to remain below target

On the inflation front, the minutes identified stabilizing oil prices as a potential boost to inflationary pressures within the economy in the coming months. The Fed expects increased energy costs combined with a tightening labor market to help push inflation back towards its target of 2% by the end of year – current levels are well below target.

Summing up the inflation environment and economic picture in the Fed’s own words:

“The information reviewed for the June 16-17 meeting suggested that real gross domestic product (GDP) was increasing moderately in the second quarter after edging down in the first quarter. Labor market conditions improved somewhat further in recent months. Consumer price inflation continued to run below the FOMC’s longer-run objective of 2 percent and was restrained significantly by earlier declines in energy prices and decreases in prices of non-energy imports. Survey measures of longer‑run inflation expectations remained stable, while market-based measures of inflation compensation were still low.”

In summary, it is clear there is growing sense of frustration within the Fed with regards to its inability to start normalizing rates which have been set near zero percent since the onset of the 2008 crisis. With ongoing stress in world financial markets, the Fed knows a premature hike in rates would be enough to send many nations over the edge into a full blown recession. Upcoming domestic data will be key in the coming weeks, should there be a deterioration in the domestic economic picture, then all bets for any form of rate hike this year would certainly be off.

by Andrew | Jun 18, 2015 | Definitions

May CPI numbers released by the BLS came broadly in line with expectations, with headline inflation posting an increase of 0.4% versus expectations of 0.5%. The core measure, excluding food and energy, rose 0.1% versus consensus estimates of 0.2%.

Rebounding gasoline prices were the biggest contributor to rising prices, with the gasoline index rising 10.4%. Other energy costs were mixed, and medical related costs continued to rise with the medical care commodities index rising 0.4% and the medical care services index rising 0.2%. The CPI data comes on the heels of yesterdays rate decision by the FOMC, and today’s data breathes no new significant life into our argument for rates to continue to remain fixed for the foreseeable future.

Key Highlights from the June FOMC Statement

Yesterday’s rate hike decision was a relatively tame event marketwise, although revisions in some key projections were enough to spur a moderate bout of USD weakness across the board. Delving into the statement, the Fed painted an improving economic picture, noting overall improvements since the first quarter of this year. Signs of improvement in the labor market were given particular mention.

On potential signs of growing unease with the relative strength of the US Dollar versus its peers, the Fed once again reiterated sluggish growth in US exports. While no special mention of the dollar was included in this month’s statement, currency targeting is likely to feature much more on the market’s radar going forward.

Current Conditions In the Fed’s own words:

“Information received since the Federal Open Market Committee met in April suggests that economic activity has been expanding moderately after having changed little during the first quarter. The pace of job gains picked up while the unemployment rate remained steady. On balance, a range of labor market indicators suggests that underutilization of labor resources diminished somewhat. Growth in household spending has been moderate and the housing sector has shown some improvement; however, business fixed investment and net exports stayed soft.”

With regards to inflation, the Fed reiterated its forecast for inflation to normalize towards its 2% target on the back of stabilizing energy prices and tightening labor markets in general.

“Inflation is anticipated to remain near its recent low level in the near term, but the Committee expects inflation to rise gradually toward 2 percent over the medium term as the labor market improves further and the transitory effects of earlier declines in energy and import prices dissipate.”

GDP Projections Downgraded, Unemployment Forecasts Rise

Somewhat surprisingly given the Fed’s upbeat language in its written statements from the June meeting, are the negative forecast revisions for both GDP and unemployment going forward. GDP projections were but from 2.3%-2.7% to 1.8%-2.0% – a fairly sizeable downgrade, and perhaps a growing reflection of the real headwinds facing the economy at present. Continued stress in the energy sector, which has seen sustained layoffs in the first half of this year, is showing signs of of having a wider impact on the economy at large. The Fed’s projections reflect this new reality, with unemployment forecasts for 2015 raised from 5.0%-5.2% to 5.2%-5.3%.

FOMC Members increase dovish stance

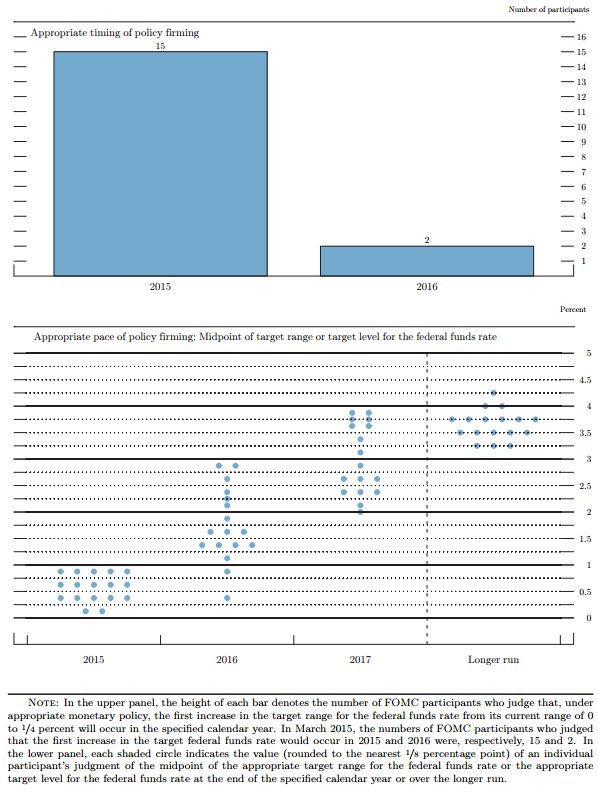

Revisions in the Fed’s quantitative forecasts were also backed up by a softening stance in the “dot” surveys of where each member expects the Fed Funds rate to be over the next two years. While the survey is conclusive that FOMC members expect a rate hike at some point this year, the magnitude of the rise is less clear. The overall drop from 1.875% to 1.625% in expectations for the Fed Funds rate in 2016 in many ways highlights the dwindling conviction affecting many FOMC members with regards to the extent of the “upcoming” rate hikes.

In summary, inflation is starting to show signs of stabilizing, with the deflationary month on month trends eradicated for the time being. While not evident in this month’s release, increased input costs on the producer front are likely to stoke higher inflation going forward. Medical inflation is an increasingly worrying trend, and is likely to hurt average Americans in a big way in the near future.

by Andrew | May 22, 2015 | Definitions

CPI for April came in broadly inline with market expectations with core inflation (ex Food and Energy) rising +0.3% MoM vs expectations of +0.2%. Broader CPI rose +0.1% bang inline with market forecasts. Annualized figures show a persistent deflationary trend, declining -0.2% YoY inline with analyst forecasts. Weekly earnings may well draw the Fed’s attention, with the data showing significant signs of improvement rising +2.3%. Combined with the positive jobs numbers of late, the employment situation does seem to be gathering steam.

Energy prices declined across the board, falling -1.3% MoM and -19.4% YoY. Gasoline fell -1.7% and Fuel Oil posted a decline of -8.4% MoM.

In a worrying continuation of last month’s data, medical prices surged +0.7% MoM and was the highest contributor to the Core inflation figure.

The slightly than higher Core CPI numbers are causing a sharp spike in the Dollar Index post announcement, however the relatively benign number combined with the slowdown in nearly all major economic indicators over the past month are likely to reduce the possibility of any potential rate hike at the Fed’s upcoming June policy meeting. Markets are awaiting Fed chief Yellen’s commentary later today for any revised signal in rate expectations.

Economic Indicators have been weak across the board

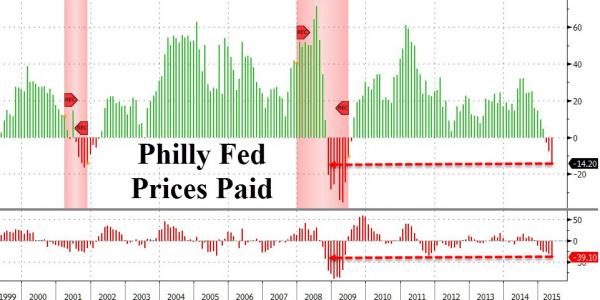

Philly Fed

Recent data from the Philly Fed indicate a slowdown in the manufacturing sector with the index posting further declines in May, posting a 6.7 print versus 8.0 consensus estimates. Despite a brief bounce in April, the index has now missed expectations for 7 out of the past 9 months and is growing reflection of the malaise starting to creep into the real economy. Prices paid for new orders plunged at an alarming pace, with declines also present in the average workweek.

PMI

The Markit US Manufacturing PMI survey released earlier this week reinforces the evidence of further weakness creeping into the manufacturing sector. May PMI data slowed to 53.8 versus expectations of 54.5, and extends the weakness of the April data which registered the biggest miss of expectations on record. Manufacturing PMI is now at it lowest level in over a year when the US was gripped in the middle of severe winter weather. PMI weakness is a growing trend across the world, with European, and Chinese surveys all pointing in a similar direction.

The strong dollar has been attributed with causing most of the headwinds for the manufacturing sector and is likely to be a concern for policy makers going forward. Declining export sales highlight further problems with the strong dollar, with US data falling for the past two consecutive months. April also saw the first rise in input costs for 2015, as the rebounding crude oil price began creeping into production costs.

Given the impact the stronger dollar is having on the broader economy, the Fed is likely to adopt a cautious approach going forward, and will likely increase commentary around the impact the relative strength of the currency is having going forward. Rate hikes in the near future would likely exacerbate problems in the export and manufacturing sector, and the Fed will be keeping this in mind at the June policy meeting.

FOMC Minutes paint a mixed picture for rate hikes going forward

The minutes from the last policy meeting released earlier this week reflected growing concern about current bond market volatility, and over extended valuations in the stock market. Examining the minutes in detail reveals a more proactive stance by the Fed in trying to jawbone the equity markets onto a more sustainable path without having to use the threat of an actual rate hike.

Some of the more noteworthy commentary includes:

In their discussion of financial market developments and financial stability issues, policymakers highlighted possible risks related to the low level of term premiums. Some participants noted the possibility that, at the time when the Committee decides to begin policy firming, term premiums could rise sharply—in a manner similar to the increase observed in the spring and summer of 2013—which might drive longer-term interest rates higher. In this connection, it was suggested that the tendency for bond prices to exhibit volatility may be greater than it had been in the past, in view of the increased role of high-frequency traders, decreased inventories of bonds held by broker-dealers, and elevated assets of bond funds.

A few anticipated that the information that would accrue by the time of the June meeting would likely indicate sufficient improvement in the economic outlook to lead the Committee to judge that its conditions for beginning policy firming had been met. Many participants, however, thought it unlikely that the data available in June would provide sufficient confirmation that the conditions for raising the target range for the federal funds rate had been satisfied, although they generally did not rule out this possibility. Participants discussed the merits of providing an explicit indication, in postmeeting statements released prior to the commencement of policy firming, that the target range for the federal funds rate would likely be raised in the near term. However, most participants felt that the timing of the first increase in the target range for the fed-eral funds rate would appropriately be determined on a meeting-by-meeting basis and would depend on the evo-ution of economic conditions and the outlook. In keeping with this data-dependent approach, some participants further suggested that the postmeeting statement’s description of the economic situation and outlook, and of progress toward the Committee’s goals, provided the appropriate means by which the Committee could help the public assess the likely timing of the initial increase in the target range for the federal funds rate.

On balance, April CPI has gone some way in postponing any imminent rate hike which could have some bearing on the USD in the coming days and weeks. Yellen’s commentary later today will prove crucial for market sentiment. We stay tuned.