The PBOC stunned world markets this week with a series of consecutive devaluations of the Yuan, dropping nearly 5 percent against the US dollar and poised to weaken even further in the days and weeks ahead. The Yuan devaluation is just the latest in long list of policy responses to help stimulate China’s slowing economy, although this latest move is likely to have broad reaching implications for the rest of the world. Chinese monetary authorities increased the currency’s reference rate against the dollar by 1.9% without warning in the early hours of Tuesday morning, and have continued to intervene in the broader currency markets ever since. The biggest move in the CNY prior to Tuesday’s devaluation was a meager 0.15% as the currency remained tightly controlled by the authorities, emphasising just how shocking the 1.9% move on Tuesday has been for investors’ collective psyche. Chinese officials have been justifying the devaluation by pointing to the strength in the US dollar over the past year which has caused the Yuan to appreciate significantly against the Euro and British pound in particular. While the Chinese argument has some merits, many analysts are viewing the move as an escalation of the “beggar thy neighbor” currency wars which have been raging throughout the world since the onset of the financial crisis in 2008. The obvious question world markets are currently having to contend with now that China has officially entered the global currency war, what implications will this latest move have for broader markets including China’s immediate neighbors, the US dollar, and Federal Reserve policy going forward?

Emerging Markets Set to Follow China’s Lead

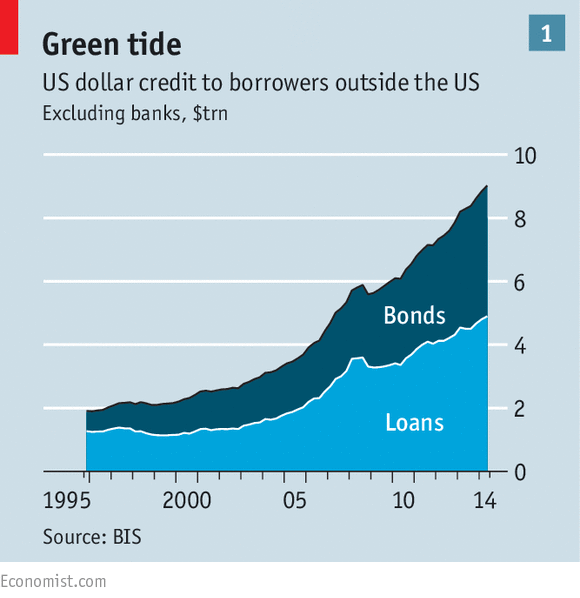

One of the biggest threats to emerge from the recent Yuan devaluation is a potential full blown currency crisis in emerging world FX rates. Prior to China’s devaluation, many of these countries were already struggling with weak currencies and mounting current account deficit issues. Collapsing commodity prices have placed a significant strain on these countries budgets, and now they face the unenviable task of having to devalue their currencies further in order to keep in step with China. The risk of contagion from this sort of mass currency intervention is clear. Many corporates in Asia and other emerging markets have been borrowing US dollars since the 2008 crisis due to the zero percent interest rates and widespread belief that their own domestic currencies would continue to appreciate against the dollar. This type of behavior should sound familiar, it is the exact same line of thinking which sparked the Asian financial crisis of the late 1990s. Faced with plunging domestic currencies, the cost of servicing US dollar debt is set to climb sharply for these corporates. Stephen Jen, a prominent analyst who called the Asian currency crisis in the 1990s while working for Morgan Stanley predicts emerging market currencies could fall a further 30 to 50 percent from current levels in response to the declining Yuan. The implications of such a move on these economies would be devastating – a toxic mixture of inflation and widespread corporate insolvency. Many of these nations have been a key driver of global growth in recent years, so weakness in their economies are likely to be felt on a worldwide scale

Faced with plunging domestic currencies, the cost of servicing US dollar debt is set to climb sharply for these corporates. Stephen Jen, a prominent analyst who called the Asian currency crisis in the 1990s while working for Morgan Stanley predicts emerging market currencies could fall a further 30 to 50 percent from current levels in response to the declining Yuan. The implications of such a move on these economies would be devastating – a toxic mixture of inflation and widespread corporate insolvency. Many of these nations have been a key driver of global growth in recent years, so weakness in their economies are likely to be felt on a worldwide scale

Where Does the Federal Reserve Go From Here?

Ongoing weakness in China and emerging markets at large are likely to be felt more acutely in developed economies in the months ahead. The biggest concern amongst many analysts is the potential for a return to the deflationary pressures which dogged sentiment in the US economy in the early part of 2015. These concerns are warranted. Commodity prices have continued to collapse in the past few weeks with the price of crude oil in particular hovering dangerously around the $40 per barrel mark, the lowest price in over 6 years. The low price of oil and energy related costs will have significant ramifications for both the CPI and PPI data in the months ahead, and it seems increasingly likely that a return to negative readings for CPI in particular is a real probability for the August and September data which should be released in the fourth quarter. Armed with the knowledge that these types of headwinds are in the post for the US economy, it seems increasingly unlikely that the Fed will lose its nerve to begin raising rates at its upcoming September meeting. The more cynical among us could even argue that China’s devaluation has been a dream come true for the Fed as it gives it enough cover to delay raising rates due to “external” factors and opens the door for more QE. And more QE at the end of the day is what every wants. The government wants it, the market wants it, emerging markets want it, and it looks increasingly likely that they will get it in the months ahead. The worrying element to all of this is that the current weakness across world markets is systemic – it feels far more dangerous than 2008 and we are now on the eve of a bigger crisis knowing full well that the world’s central banks have no credible policy response to deal with it.

Andrew McCarthy is an expert in all things inflation. He has a Bachelors in Economics and has been working in the finance industry for over two decades.