July’s Weak Inflation Numbers Mean More Uncertainty Around September Rate Hike

On Wednesday, the Bureau of Labor Statistics released inflation data for July that was slightly below expectations. For the month, the headline number or Consumer Price Index for All Urban Consumers (CPI-U) increased 0.1% compared to a median estimate of 0.2% for analysts polled by Bloomberg.

For the 12-month period ending in July, inflation was only 0.2%. This number includes consistent declines in monthly CPI numbers for October 2014 through January 2015. Year over year, core inflation, which excludes food and energy, climbed 1.8%. This is exactly in line with expectations and equal to the core annual inflation number reported four of the past five months.

July’s CPI numbers follow increases of 0.4% and 0.3% in May and June respectively and point to a loss of momentum. Sluggish inflation means the Federal Reserve may be hesitant to raise rates in September. The Fed’s key interest rate has hovered around zero since December 2008 but a series of rate hikes has been widely anticipated to start as early as next month. Weak inflation coinciding with global economic troubles could indicate that the US economy is not ready for higher interest rates.

Crude Oil Prices Tumble in July

The Energy index fell 14.8% for the year ending in July, despite an increase of 0.1% in July. Crude Oil went from around $58/barrel to below $46/barrel in the month of July alone; such low prices have not been seen since 2009. However, gasoline prices edged higher by 0.9% in July following increases of 3.4% in June and 10.4% in May. Year over year, the gasoline index has still slid 22.3% due to the sharp declines in the second half of 2014. Aside from gasoline, all other major components of the energy index fell in July. Year over year, all components of the energy index are significantly lower with fuel oil posting the largest 12-month decline, down 29.7%.

Declining oil prices have sparked competition among airlines and fares fell a staggering 5.6% in the month of July. Low fuel costs have slowly filtered through to consumers resulting in the largest monthly decline in airline tickets in nearly 10 years. Economists do not expect prices to remain low for long.

Food and Housing Costs on the Rise While Wages Remain Stagnant

The food index climbed 1.6% for the year ending in July, including a 0.2% rise in July alone. All six major grocery store indexes were higher for the month, led by dairy products, up 0.8%. The price of fruits and vegetables rose 0.3% in July. The year ending July saw drastic increases in the price of eggs (24.9%) and beef (10.0%). Compared to a year earlier, food at home is 0.9% more expensive and food away from home is costs 2.7% more

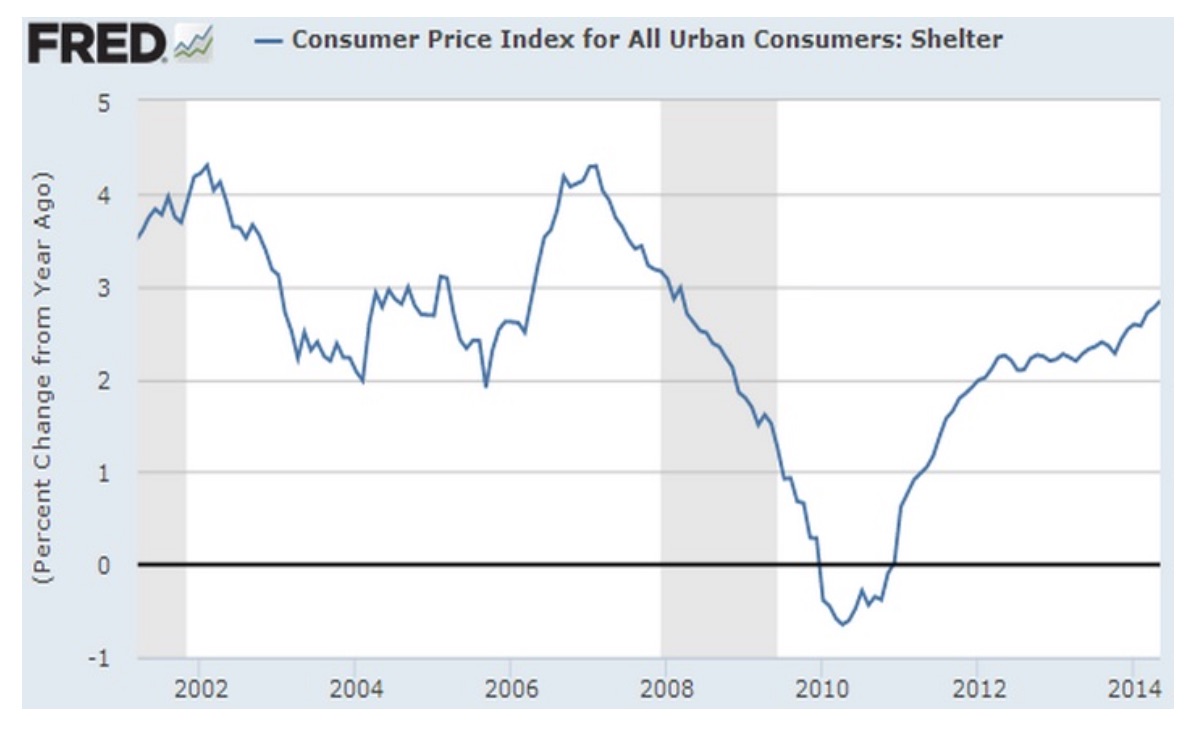

Shelter costs are up significantly (3.1%) year over year. In July, shelter costs posted their largest monthly gain (0.4%) since February 2007. This is largely due to higher rental costs as available housing continues to dwindle. Vacancy rates for rental units are near their 22-year low. The graph below shows that this trend has been consistent since 2010. The problem, according to Diane Swonk, chief economist at Mesirow Financial in Chicago is that “rents are surging and in the face of stagnant wages [which] leaves less for consumers to spend elsewhere in the economy.”

The July jobs report showed a small decline in unemployment, down a marginal 0.02% to 5.26%, which is a 7-year low. Employment growth has been healthy and consistent but wage growth has lagged previous economic recoveries. David Kelly at JP Morgan blames low headline inflation numbers, among other factors, for lacklustre wage growth.

Outlook for the Federal Reserve

Growing concern over the health of the global economy could delay or slow the pace of interest rate hikes at the Federal Reserve. China’s surprise devaluation of the yuan should be a major concern for the US economy. Other emerging markets could potentially follow suit if they wish to remain competitive with China. This could spur global deflation. Import prices will certainly fall in the US. Combined this with drastically dwindling commodity prices and a strong dollar and there is little to support price growth. Although the Fed has stated that they may still raise rates despite low inflation, it is a key factor they will need to consider. Raising rates in a deflationary environment is unlikely.