The Federal Reserve kept interest rates on hold at its latest policy meeting Wednesday, ensuring interest rates will remain near zero for at least another two months. Fed officials closed ranks voting 10-0 to keep interest rates unchanged, In what was a widely expected move by the broader market. With only three policy meetings remaining in which to make good on Janet Yellen’s signal to raise benchmark interest rates by the end of the year, the Fed faces an increasingly difficult decision on whether to move in September, or delay any change in policy to next year. Given the ongoing volatility in global markets, their decision will not be an easy one.

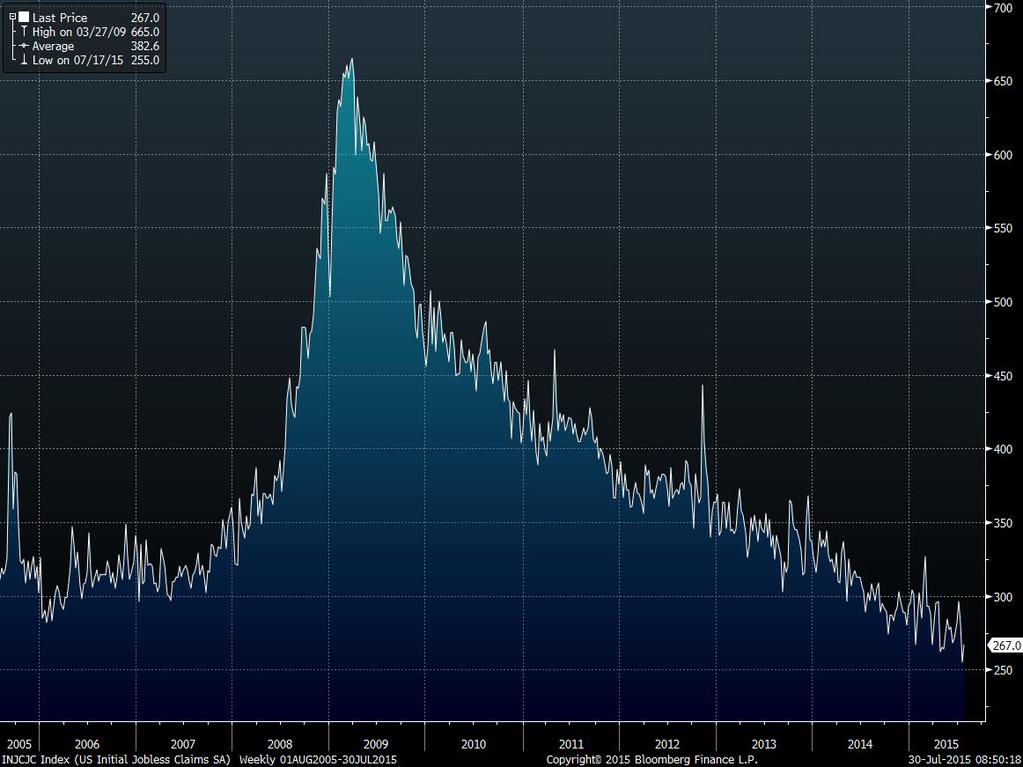

At the heart of the Fed’s dilemma is an improving employment picture, which goes some way to fulfilling the Fed’s mandate of achieving maximum employment, and has been cited on numerous occasions by Fed officials as the reason to start normalizing interest rate policy. Unemployment has fallen from nearly 10% at the height of the financial crisis in 2009, to 5.3% currently, and official month to month data continues to show signs of improvement. The advance reading of initial unemployment claims this week was 255,000, a drop of 26,000 from the previous week. The latest data marks the lowest level of weekly initial unemployment claims in over 41 years. Consensus expectations had been calling for initial claims numbers closer to 278,000. All else being equal, the employment figures would be enough for the Fed to start hiking rates at their September meeting, but everything else is not equal. There are several financial storms raging all across the globe which the Fed will need to ensure they do not exacerbate.

Commodity Price Rout Raises Deflation Concerns

The global rout in commodity markets is of particular concern, and plunging prices could see a return of the deflationary conditions which plagued the US CPI data for the first quarter of this year. Any increased probability of deflation would put

the other half of the Fed’s dual mandate of ensuring price stability in jeopardy, and any uncertainty regarding this half of the equation is likely to instill an increased degree of caution amongst Fed officials when it comes to raising rates.

The potential impact of the recent commodity crash was outlined in a recent report by Deutsche Bank analysts, who found that the current -29% drop in the benchmark CRB commodities index is likely to severely impact headline inflation in the coming months. DB forecasts headline CPI inflation to fall from 01.% currently to -0.9% in the next few months. If they are correct, this would be the biggest year over year drop in inflation since September 2009, and one of the lowest inflation levels on record.

Timing of Fed Hike Continues to be Pushed Out

Market reaction to the Fed’s latest minutes was upbeat, with benchmark US equity indices all posting modest gains. Treasuries rallied with yields falling on the back of increasing signs that a growing segment of investors are starting to discount the probability of any rate rise this year. A broader recognition of this new environment is likely to cement itself in the coming days after wall street analysts continue to digest the ongoing rout in commodity markets, and downward GDP revisions begin to come through. If the Fed fails to hike in September it is very unlikely that it would test the resolve of global markets by hiking in the midst of peak holiday season in December, a period when world wide liquidity is wafer thin and trading desks staffed by fresh faced grads out of college. The reality looks increasingly, as we have been saying all year, that there will be no hike this year – the earliest and most likely timescale for any rike would be mid 2016 at best. By then there should be some clarity on any potential impact from the fallout in China, and if the deflationary trends which were so prevalent at the start of the year reappear. Should deflationary conditions return, there will be virtually no room for the Fed to progress with its normalisation policy – and given the heightened volatility across global markets, it seems increasingly likely that a return to increased QE is likely to occur long before any rise in rates.

Andrew McCarthy is an expert in all things inflation. He has a Bachelors in Economics and has been working in the finance industry for over two decades.