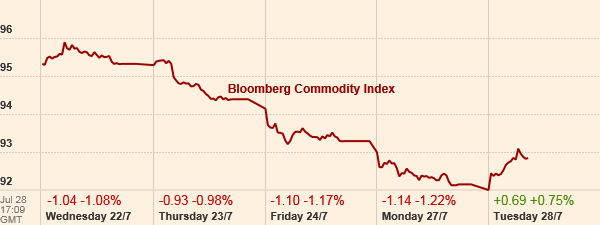

Commodity prices have been plunging in recent weeks, with the Bloomberg commodities index falling to an 11-year low, a drop of nearly 42 per cent since its peak in 2008. Plunging prices for natural resources are stoking real concerns that the deflationary conditions which plagued the US economy during the first quarter of 2015 could return with a vengeance in the months ahead. Commodity markets have been under pressure for most of the year on expectations of an imminent rate hike by the Federal Reserve, but the rout has been accelerating viciously in recent weeks due to ongoing concerns with a broad based economic slowdown in China. While the Chinese stock market has been grabbing headlines for the past few months, the real danger lies with problems bubbling under the surface of the country’s “real” economy. Recent Purchasing Manager Index data from China has been abysmal, with the latest figures showing PMI at a 15 month low. Growing signs of stress amongst Chinese purchasing managers does not bode well for the world at large. Slowing demand worldwide combined with an oversupply of inventory due to excessive production in China is likely to trigger another wave of deflation in the coming months – which should, all else being equal, curtail any potential rate hike by the Fed.

Central Banks are EASING Globally

Compounding the situation at the Fed is a scramble amongst central banks across the world to increase their monetary stimulus packages to help contain the economic carnage which has been unleashed in their respective nations due to interest rate differential expectations in some cases, and plunging commodity based revenues on the other. Canada was the first country to concede “all is not well”, with the central bank cutting interest rates and lowering its GDP forecast for the rest of the year due to falling oil sector investment. Both Australia and New Zealand have followed suit, with both countries looking increasingly vulnerable to any potential slowdown in China. The currencies of both countries have fallen sharply in value in recent months – with no sign of relief in the near future.

In the case of China, it is estimated that the country experienced $224 billion of capital outflows in the second quarter, an eye watering number which has forced the PBOC to tap into its foreign reserves in order to defend the Yuan. If China is having to resort to such measures to defend its currency, what chance do more vulnerable emerging markets have? Nations like Brazil, South Africa, Indonesia, are all seeing severe currency crises which in some cases could spark into full blown regional banking crises should the current financial conditions persist.

So where does this leave the Fed? In no uncertain terms, an increase in rates by the Fed any time soon will push the vast majority of the world over the proverbial edge, and it wouldn’t take long for the ramifications of such economic pain to begin reverberating within the US economy itself.

The Fed’s hands are tied… again

The unfolding commodity carnage will start to impact wall street GDP forecasts and earnings estimates in the days and weeks ahead as analysts begin to digest the implications of slowing demand worldwide. Downward revision to GDP forecasts will be the death knell for rising rates, and will eclipse any positive data which may be appearing on the employment front. Once again the Fed will find itself trapped between seemingly “improving” signs domestically, and full scale carnage internationally. The long run implications of this dilemma are worrying. Should deflationary pressures increase dramatically in the coming months, there will be an expectation on the Fed to embark upon the same easing measures which have led to the current situation in the first place. China undergoing a period of market turmoil as a direct result of the zero interest rate policies being implemented by central banks all over the world. The inflation which failed to show up in developed economies, was unleashed with a vengeance in Chinese financial assets. The market may very well expect and demand another round of QE, and they may very well even get it, but the question has to be asked, will it matter any more? And if it doesn’t matter, what comes next? The answer to that looks increasingly like a breakdown in faith in central banks, as they fight wearily on against increasingly frequent financial storms.

Andrew McCarthy is an expert in all things inflation. He has a Bachelors in Economics and has been working in the finance industry for over two decades.