-v3")

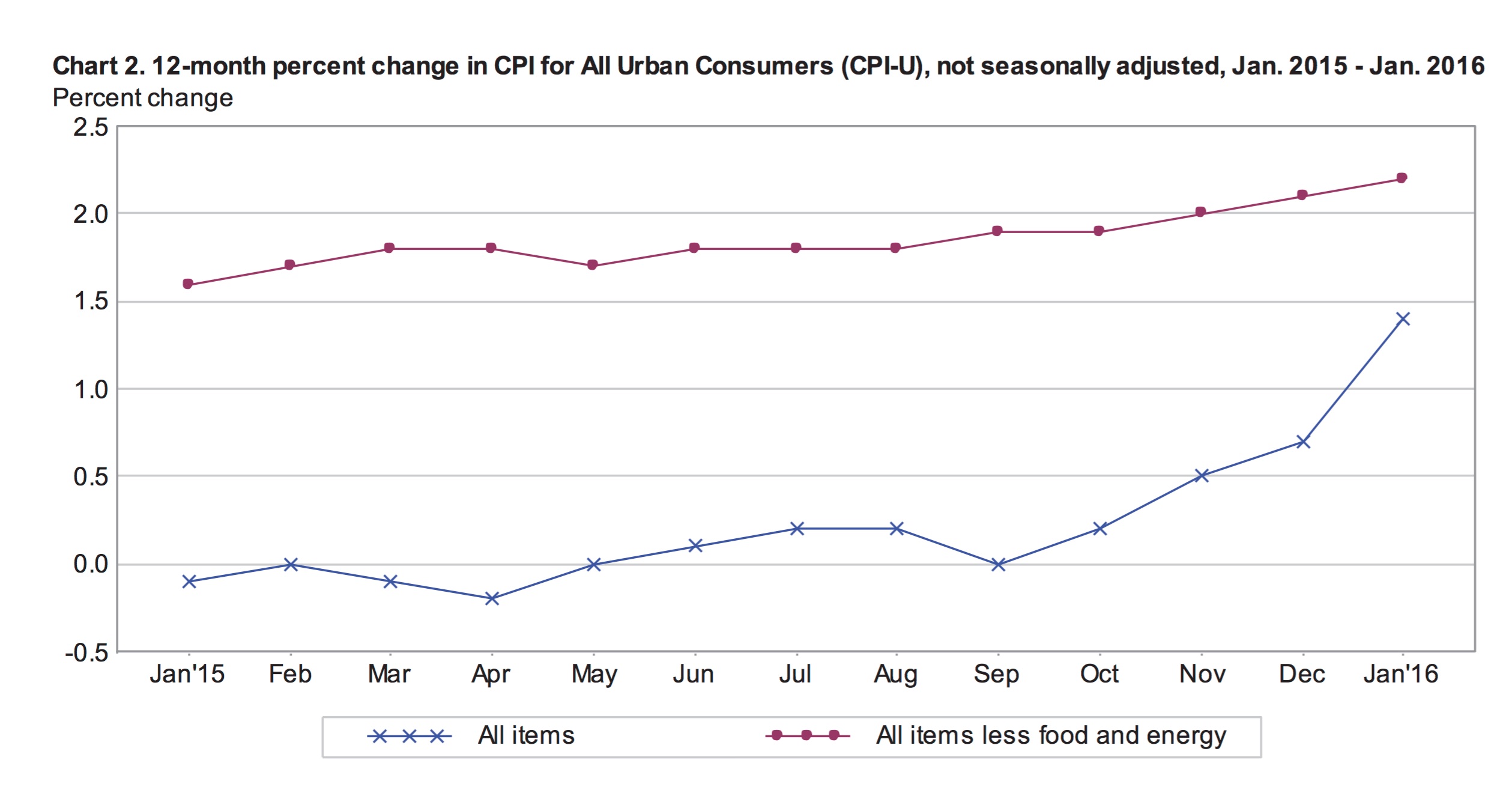

According to the Bureau of Labor Statistics, consumer price levels, measured by the Consumer Price Index for All Urban Consumers (CPI-U), increased by 1.4% for the year ending in January compared to 0.7% for the year ending in December. After seasonal adjustments, the CPI-U was flat in January, following a decline of 0.1% in December. Falling energy prices were largely offset by higher shelter costs for the month.  Core inflation, measured by the index for all items less food and energy, climbed 0.3% in January and 2.2% for the year ending in January. This is marginally higher than the consensus expectations of 0.2% for the month and 2.1% for the year. January’s expectations were in line with December’s inflation numbers. The surprise acceleration in core price levels may reflect some underlying economic strength.

Core inflation, measured by the index for all items less food and energy, climbed 0.3% in January and 2.2% for the year ending in January. This is marginally higher than the consensus expectations of 0.2% for the month and 2.1% for the year. January’s expectations were in line with December’s inflation numbers. The surprise acceleration in core price levels may reflect some underlying economic strength.

Annual Inflation

For the year ending in January, inflation was boosted by higher prices for shelter, medical services and transportation services. At the same time, sliding energy prices kept overall inflation levels relatively tame. The energy index was down 6.5% for the year ending in January and every component of the index declined. Year over year, fuel oil prices fell 28.7% and the gasoline index dropped 7.3%. The index for all items less energy climbed 2% for the year ending in January.

The food index inched up 0.8% for the year masking volatility within the index. The price of food at home slid 0.5% while food away from home was 2.7% more expensive. The price for food at employee sites and schools spiked 5.2% year over year. At the grocery store, meat prices fell 4.9%; milk was 7.2% cheaper; and the price of eggs increased by 6.8%. Fresh fruits and vegetables were 3.3% more expensive compared to a year earlier.

The cost of shelter, which accounts for approximately one third of the CPI-U, climbed 3.2% for the year ending in January and was the largest driver of overall inflation. The index for all items less shelter only grew by 0.5% year over year. Rental prices for primary residences were 3.7% higher in January compared with a year earlier. Over the same period, the index for health insurance jumped 4.8% and motor vehicle insurance climbed 5.4%.

Seasonally Adjusted Monthly Inflation

Every component of the energy index fell in January for the second month in row. Overall the energy index slipped 2.8% in January, including a 4.8% decline in the price of gas. These rates are identical to the changes in the energy and gas indexes in December. Energy and gas prices recorded marginal increases in October and November but appear to have resumed their downward path.

The food index was flat in January with all but one of the six major grocery store groups showing lower prices compared to the previous month. Fruits and vegetables cost 1.3% more in January versus December as tomato prices skyrocketed by 15.3%. The price of eggs tumbled 8.4% in January. Meat prices, particularly prices for beef and pork, also declined significantly over the month.

Shelter costs were 0.3% higher in January and helped balance falling energy prices. Other significant monthly growth was recorded for the medical care index, which climbed 0.5%. Medical insurance prices were up 1.1%. Apparel prices reversed their downward trend and rose 0.6% in January. The index for new vehicles increase by 0.3% while the index for used vehicles gained only 0.1%.

Outlook

The unexpected strength in January’s core inflation increases the likelihood that the Federal Reserve will raise interest rates sooner rather than later. Slow global growth and particularly slow growth in China, cheap oil and low domestic inflation have created skepticism about rate hikes this year. However, January’s annual core inflation rate of 2.2% is the highest recorded since June 2012 and is above the Federal Reserve’s target inflation rate of 2%.

Core inflation is considered to be a better gauge of underlying economic growth because the volatile, short-term price fluctuations within the energy and food components are eliminated. However, there is debate within the Federal Reserve regarding the true path of inflation and economic growth in the United States. A strong dollar drives down the price of imports, depressing inflation and higher rates will further lift the U.S. dollar. This would burden emerging economies and dampen global growth, which will impact the U.S. economy.

The Fed meets on March 15th and 16h to discuss monetary policy. It is unlikely that they will raise rates at that meeting. The futures markets are predicting that the chance of a rate hike this year is less than 40%.

Emily is a Canadian financial blogger with multiple degrees in economics and extensive professional experience as a financial analyst. She was formerly a Ph.D. candidate at the University of Guelph's School of Agricultural Economics. Before that, she received an MA from the University of San Francisco in International Development Economics. She also has a BA in Math with a minor in Economics.