Andrew

Andrew McCarthy is an expert in all things inflation. He has a Bachelors in Economics and has been working in the finance industry for over two decades.

by Andrew | Aug 14, 2015 | Definitions, Federal Reserve, In the news

The PBOC stunned world markets this week with a series of consecutive devaluations of the Yuan, dropping nearly 5 percent against the US dollar and poised to weaken even further in the days and weeks ahead. The Yuan devaluation is just the latest in long list of policy responses to help stimulate China’s slowing economy, although this latest move is likely to have broad reaching implications for the rest of the world. Chinese monetary authorities increased the currency’s reference rate against the dollar by 1.9% without warning in the early hours of Tuesday morning, and have continued to intervene in the broader currency markets ever since. The biggest move in the CNY prior to Tuesday’s devaluation was a meager 0.15% as the currency remained tightly controlled by the authorities, emphasising just how shocking the 1.9% move on Tuesday has been for investors’ collective psyche. Chinese officials have been justifying the devaluation by pointing to the strength in the US dollar over the past year which has caused the Yuan to appreciate significantly against the Euro and British pound in particular. While the Chinese argument has some merits, many analysts are viewing the move as an escalation of the “beggar thy neighbor” currency wars which have been raging throughout the world since the onset of the financial crisis in 2008. The obvious question world markets are currently having to contend with now that China has officially entered the global currency war, what implications will this latest move have for broader markets including China’s immediate neighbors, the US dollar, and Federal Reserve policy going forward?

Emerging Markets Set to Follow China’s Lead

One of the biggest threats to emerge from the recent Yuan devaluation is a potential full blown currency crisis in emerging world FX rates. Prior to China’s devaluation, many of these countries were already struggling with weak currencies and mounting current account deficit issues. Collapsing commodity prices have placed a significant strain on these countries budgets, and now they face the unenviable task of having to devalue their currencies further in order to keep in step with China. The risk of contagion from this sort of mass currency intervention is clear. Many corporates in Asia and other emerging markets have been borrowing US dollars since the 2008 crisis due to the zero percent interest rates and widespread belief that their own domestic currencies would continue to appreciate against the dollar. This type of behavior should sound familiar, it is the exact same line of thinking which sparked the Asian financial crisis of the late 1990s. Faced with plunging domestic currencies, the cost of servicing US dollar debt is set to climb sharply for these corporates. Stephen Jen, a prominent analyst who called the Asian currency crisis in the 1990s while working for Morgan Stanley predicts emerging market currencies could fall a further 30 to 50 percent from current levels in response to the declining Yuan. The implications of such a move on these economies would be devastating – a toxic mixture of inflation and widespread corporate insolvency. Many of these nations have been a key driver of global growth in recent years, so weakness in their economies are likely to be felt on a worldwide scale

Faced with plunging domestic currencies, the cost of servicing US dollar debt is set to climb sharply for these corporates. Stephen Jen, a prominent analyst who called the Asian currency crisis in the 1990s while working for Morgan Stanley predicts emerging market currencies could fall a further 30 to 50 percent from current levels in response to the declining Yuan. The implications of such a move on these economies would be devastating – a toxic mixture of inflation and widespread corporate insolvency. Many of these nations have been a key driver of global growth in recent years, so weakness in their economies are likely to be felt on a worldwide scale

Where Does the Federal Reserve Go From Here?

Ongoing weakness in China and emerging markets at large are likely to be felt more acutely in developed economies in the months ahead. The biggest concern amongst many analysts is the potential for a return to the deflationary pressures which dogged sentiment in the US economy in the early part of 2015. These concerns are warranted. Commodity prices have continued to collapse in the past few weeks with the price of crude oil in particular hovering dangerously around the $40 per barrel mark, the lowest price in over 6 years. The low price of oil and energy related costs will have significant ramifications for both the CPI and PPI data in the months ahead, and it seems increasingly likely that a return to negative readings for CPI in particular is a real probability for the August and September data which should be released in the fourth quarter. Armed with the knowledge that these types of headwinds are in the post for the US economy, it seems increasingly unlikely that the Fed will lose its nerve to begin raising rates at its upcoming September meeting. The more cynical among us could even argue that China’s devaluation has been a dream come true for the Fed as it gives it enough cover to delay raising rates due to “external” factors and opens the door for more QE. And more QE at the end of the day is what every wants. The government wants it, the market wants it, emerging markets want it, and it looks increasingly likely that they will get it in the months ahead. The worrying element to all of this is that the current weakness across world markets is systemic – it feels far more dangerous than 2008 and we are now on the eve of a bigger crisis knowing full well that the world’s central banks have no credible policy response to deal with it.

by Andrew | Aug 10, 2015 | Federal Reserve, In the news

In what could become be a dry run for the Federal Reserve in the very near future, this month’s inflation report by the Bank of England revealed the growing likelihood that rates in the UK are likely to remain unchanged for the foreseeable future due to the worldwide collapse in commodity prices and a strong value of sterling versus the rest of its major trading peers. Similar to the US market, a rate hike sometime this year was heavily baked into investors assumptions for the UK economy, and these latest minutes are sure to throw the market off guard with regards to both the BoE and Fed’s rate tightening schedule.

Commodity Driven Deflation begins to Accelerate

The BoE’s dovish comments come on the back of slowing inflation in June, with CPI in the UK falling back to 0% on a month over month basis. The BoE’s monetary policy has an inflation targeting policy of 2% as part of its commitment to helping sustain a growing economy and employment picture. In his open letter to the UK chancellor, BoE Governor Mark Carney identified an unusually low contribution from energy and food prices as being the main trigger for the sluggish inflation figures. Carney’s comments reflect the growing reality for the US and UK that the ongoing commodity rout, and relative strength in both nations’ currencies are triggering a return to the deflationary environment which existed in the first quarter of this year.

Carney hinted that the slowing commodity market could lead to a slowdown to global growth, although he maintained the bank’s forecast that growth in advanced economies would accelerate (this seems dubious). In his own words:

“The Committee projects UK-weighted world demand to expand at a moderate pace. Growth in advanced economies is expected to be a touch faster, and growth in emerging economies a little slower, than in the past few years. The support to UK exports from steady global demand growth is expected to be counterbalanced, however, by the effect of the past appreciation of sterling. Risks to global growth are judged to be skewed moderately to the downside reflecting, for example, risks to activity in the euro area and China.”

The Fed looks increasingly likely to follow the BoE cautionary stance

Carney’s comments are likely to increase doubt over the Fed’s ability to raise rates in the coming months. Both the Fed and the BoE are cut from the same cloth, and their similar modelling techniques should result in the same deflationary headwinds beginning to appear in official data in the weeks and months ahead. The Fed is facing an increasingly difficult decision, especially given the backdrop of official economic data coming out of the US which paints a narrative of improving employment within the economy. If the Fed continues to stick to its mantra of being data dependent, then it will risk triggering massive capital flight across world markets as the USD carry trade unwinds in earnest. The Fed will be very well aware of this scenario, and it is for this reason that we are likely to see a more cautionary stance develop amongst the Fed in the weeks ahead. We are already starting to see GDP forecasts come in well short of expectation, with the Atlanta fed predicting a mere 1% increase in GDP in the third quarter, nearly 2% lower than consensus wall street expectations! The Atlanta Fed has been highly accurate with its GDP forecasting this year, so if the trend continues, the outlook for GDP downgrades in the months ahead looks a certainty. The collapse in the shale oil and gas sector alone is likely to see a formidable reduction in capex in the seconf half of 2015 – none of which has been priced into wall street analysts’ expectations. Faced with deflation, a strong US dollar, and deteriorating GDP growth, who would seriously bet on the Fed raising rates in the near future? The funny thing is – the market still is! The likelihood is that we are going to see a very sharp realization that the interest rate expectations for this year are way off the mark. How this realization happens without a complete breakdown in credibility of central banks’s is a discussion for another day, but it seems increasingly likely that if trends around the world continue as they have been in the first half of 2015, we are far more likely to see references to QE4 in mainstream financial press in the very near future.

by Andrew | Jul 31, 2015 | Definitions, Federal Reserve, gold, In the news

The Federal Reserve kept interest rates on hold at its latest policy meeting Wednesday, ensuring interest rates will remain near zero for at least another two months. Fed officials closed ranks voting 10-0 to keep interest rates unchanged, In what was a widely expected move by the broader market. With only three policy meetings remaining in which to make good on Janet Yellen’s signal to raise benchmark interest rates by the end of the year, the Fed faces an increasingly difficult decision on whether to move in September, or delay any change in policy to next year. Given the ongoing volatility in global markets, their decision will not be an easy one.

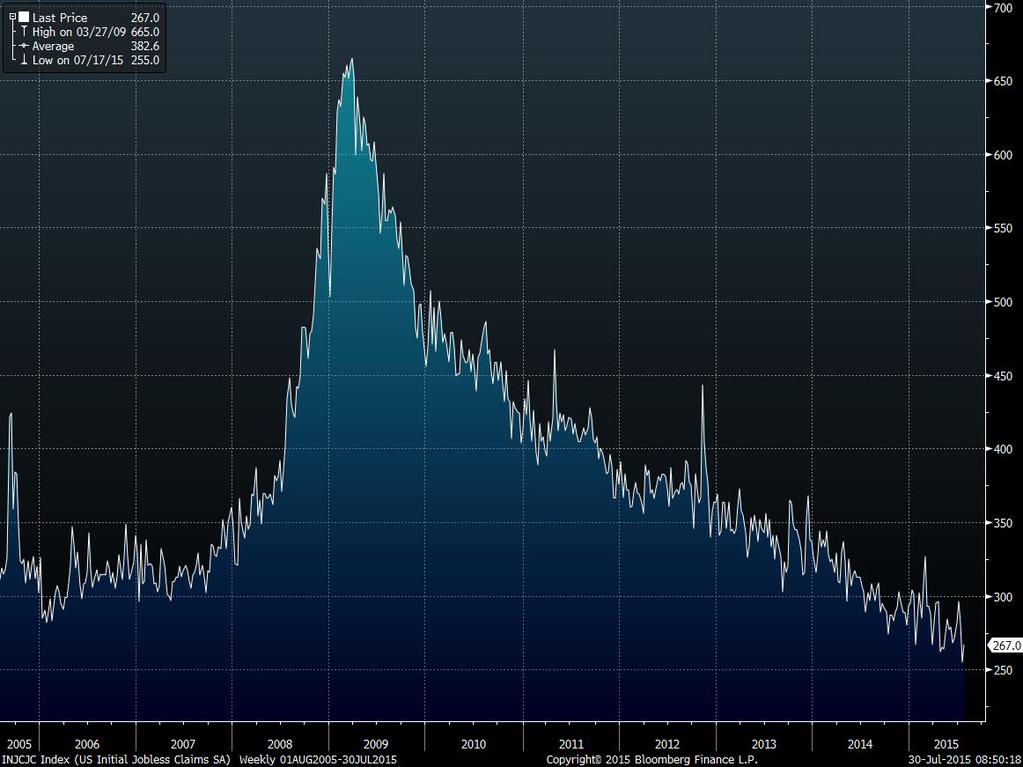

At the heart of the Fed’s dilemma is an improving employment picture, which goes some way to fulfilling the Fed’s mandate of achieving maximum employment, and has been cited on numerous occasions by Fed officials as the reason to start normalizing interest rate policy. Unemployment has fallen from nearly 10% at the height of the financial crisis in 2009, to 5.3% currently, and official month to month data continues to show signs of improvement. The advance reading of initial unemployment claims this week was 255,000, a drop of 26,000 from the previous week. The latest data marks the lowest level of weekly initial unemployment claims in over 41 years. Consensus expectations had been calling for initial claims numbers closer to 278,000. All else being equal, the employment figures would be enough for the Fed to start hiking rates at their September meeting, but everything else is not equal. There are several financial storms raging all across the globe which the Fed will need to ensure they do not exacerbate.

Commodity Price Rout Raises Deflation Concerns

The global rout in commodity markets is of particular concern, and plunging prices could see a return of the deflationary conditions which plagued the US CPI data for the first quarter of this year. Any increased probability of deflation would put

the other half of the Fed’s dual mandate of ensuring price stability in jeopardy, and any uncertainty regarding this half of the equation is likely to instill an increased degree of caution amongst Fed officials when it comes to raising rates.

The potential impact of the recent commodity crash was outlined in a recent report by Deutsche Bank analysts, who found that the current -29% drop in the benchmark CRB commodities index is likely to severely impact headline inflation in the coming months. DB forecasts headline CPI inflation to fall from 01.% currently to -0.9% in the next few months. If they are correct, this would be the biggest year over year drop in inflation since September 2009, and one of the lowest inflation levels on record.

Timing of Fed Hike Continues to be Pushed Out

Market reaction to the Fed’s latest minutes was upbeat, with benchmark US equity indices all posting modest gains. Treasuries rallied with yields falling on the back of increasing signs that a growing segment of investors are starting to discount the probability of any rate rise this year. A broader recognition of this new environment is likely to cement itself in the coming days after wall street analysts continue to digest the ongoing rout in commodity markets, and downward GDP revisions begin to come through. If the Fed fails to hike in September it is very unlikely that it would test the resolve of global markets by hiking in the midst of peak holiday season in December, a period when world wide liquidity is wafer thin and trading desks staffed by fresh faced grads out of college. The reality looks increasingly, as we have been saying all year, that there will be no hike this year – the earliest and most likely timescale for any rike would be mid 2016 at best. By then there should be some clarity on any potential impact from the fallout in China, and if the deflationary trends which were so prevalent at the start of the year reappear. Should deflationary conditions return, there will be virtually no room for the Fed to progress with its normalisation policy – and given the heightened volatility across global markets, it seems increasingly likely that a return to increased QE is likely to occur long before any rise in rates.

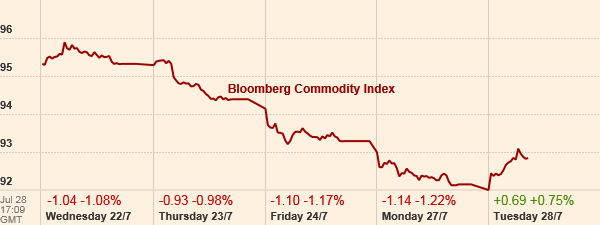

by Andrew | Jul 28, 2015 | In the news, Inflation, inflation measure

Commodity prices have been plunging in recent weeks, with the Bloomberg commodities index falling to an 11-year low, a drop of nearly 42 per cent since its peak in 2008. Plunging prices for natural resources are stoking real concerns that the deflationary conditions which plagued the US economy during the first quarter of 2015 could return with a vengeance in the months ahead. Commodity markets have been under pressure for most of the year on expectations of an imminent rate hike by the Federal Reserve, but the rout has been accelerating viciously in recent weeks due to ongoing concerns with a broad based economic slowdown in China. While the Chinese stock market has been grabbing headlines for the past few months, the real danger lies with problems bubbling under the surface of the country’s “real” economy. Recent Purchasing Manager Index data from China has been abysmal, with the latest figures showing PMI at a 15 month low. Growing signs of stress amongst Chinese purchasing managers does not bode well for the world at large. Slowing demand worldwide combined with an oversupply of inventory due to excessive production in China is likely to trigger another wave of deflation in the coming months – which should, all else being equal, curtail any potential rate hike by the Fed.

Central Banks are EASING Globally

Compounding the situation at the Fed is a scramble amongst central banks across the world to increase their monetary stimulus packages to help contain the economic carnage which has been unleashed in their respective nations due to interest rate differential expectations in some cases, and plunging commodity based revenues on the other. Canada was the first country to concede “all is not well”, with the central bank cutting interest rates and lowering its GDP forecast for the rest of the year due to falling oil sector investment. Both Australia and New Zealand have followed suit, with both countries looking increasingly vulnerable to any potential slowdown in China. The currencies of both countries have fallen sharply in value in recent months – with no sign of relief in the near future.

In the case of China, it is estimated that the country experienced $224 billion of capital outflows in the second quarter, an eye watering number which has forced the PBOC to tap into its foreign reserves in order to defend the Yuan. If China is having to resort to such measures to defend its currency, what chance do more vulnerable emerging markets have? Nations like Brazil, South Africa, Indonesia, are all seeing severe currency crises which in some cases could spark into full blown regional banking crises should the current financial conditions persist.

So where does this leave the Fed? In no uncertain terms, an increase in rates by the Fed any time soon will push the vast majority of the world over the proverbial edge, and it wouldn’t take long for the ramifications of such economic pain to begin reverberating within the US economy itself.

The Fed’s hands are tied… again

The unfolding commodity carnage will start to impact wall street GDP forecasts and earnings estimates in the days and weeks ahead as analysts begin to digest the implications of slowing demand worldwide. Downward revision to GDP forecasts will be the death knell for rising rates, and will eclipse any positive data which may be appearing on the employment front. Once again the Fed will find itself trapped between seemingly “improving” signs domestically, and full scale carnage internationally. The long run implications of this dilemma are worrying. Should deflationary pressures increase dramatically in the coming months, there will be an expectation on the Fed to embark upon the same easing measures which have led to the current situation in the first place. China undergoing a period of market turmoil as a direct result of the zero interest rate policies being implemented by central banks all over the world. The inflation which failed to show up in developed economies, was unleashed with a vengeance in Chinese financial assets. The market may very well expect and demand another round of QE, and they may very well even get it, but the question has to be asked, will it matter any more? And if it doesn’t matter, what comes next? The answer to that looks increasingly like a breakdown in faith in central banks, as they fight wearily on against increasingly frequent financial storms.

by Andrew | Jul 17, 2015 | BLS, CPI, Definitions, In the news, Inflation, Monthly CPI Updates

U.S. consumer prices increased for the fifth consecutive month in June, led higher by a rebounding price of gasoline, although there was nothing in the latest release which should pose any immediate alarm for markets or consumers at large. The latest report from the BLS reported an overall increase in headline inflation of 0.3% month on month – an increase that was inline with nearly all economists polled prior to the announcement. Looking at the headline number on an annualized basis, inflation rose 0.1 percent In the 12 months through June, following an unchanged reading for the month of May.

Gasoline prices rose 3.4% month on month, following a 10.4 percent surge in May. Given the recent volatility in crude oil prices and inventory data in July, there could be scope for the influence of rising gas prices to subside in coming months. Oil is currently trading within the $50-60 / bbl range, well below the levels seen in May and June.

Core CPI, which excludes food and energy related costs, increased 0.2 percent month on month following a rise of 0.1% previously. On an annualized basis, core CPI has now risen 1.8 percent.The June reading continues to highlight just how tame the inflationary environment is within the US economy at present. The strong dollar is helping to keep a lid on inflation by reducing the price of imports and wholesale costs. The strong US dollar has been been spurred partly by a flight to safety due to concerns in Europe and China, and partly by the market’s anticipation of a Fed rate hike later this year. We should expect to start hearing comments regarding the damaging effects of the stronger dollar by Fed officials in the weeks and months ahead should this trend continue.

The food index posts largest increase since September 2014

The price of food increased 0.3% in June, largely to an ongoing shortage in wholesale eggs which has caused a sharp jump in retail egg prices across the nation. Egg prices jumped 18.3% in June, the largest monthly gain since August 1973. Elsewhere, the index for meats, poultry, fish, and eggs rose 1.4 percent in June, with the beef index rising 0.9 percent. Food prices are likely to remain elevated in the coming months as the aftermath of the bird flu epidemic works its way through the supply chain. Wholesale food costs have been consistently increasing in PPI surveys, and these costs are likely to make their way down to the consumer in the weeks and months ahead.

Medical Price Inflation starting to cool off

Medical related inflation cooled in June which will be a welcome deviation from the overall trend in 2015. The price for Medical Care Services fell -0.2% in June and the prices for Medical Care Commodities remained unchanged month on month. Health care costs have been one of the largest contributors to inflation over the past 12 months, with both indices rising 2.3 percent and 3.3 percent respectively.

Rent Prices continue to Climb Higher

The shelter index climbed 0.3% in June, and 3% on an annualized basis as the supply of housing continues to shrink in key regions. Rent increases are also amongst the largest contributors to overall inflation in the United States within the past 12 months.

Outlook for Rates

This month’s CPI data contains no surprises, and the relatively tame reading in the core number on the back of the strong US dollar will likely stick in the minds of Fed officials in the weeks ahead. Globally, sentiment continues to wane dramatically given the continued turmoil in Greece, and increasingly China. While Greece appears to be on the verge of some sort of political settlement, the headline risk remains. In China’s case, there is a very real danger of investor sentiment turning, which could spell disaster for emerging markets overall. Latin American and South East Asian markets look at particular risk, especially on the currency front. The fate of these regions would be sealed in no uncertain terms should the Fed raise rates, and it is for this reason that it appears increasingly unlikely that the Fed will raise by year end, despite all of their rhetoric and expressed intention to do so.