by Andrew | Jul 17, 2015 | BLS, CPI, Definitions, In the news, Inflation, Monthly CPI Updates

U.S. consumer prices increased for the fifth consecutive month in June, led higher by a rebounding price of gasoline, although there was nothing in the latest release which should pose any immediate alarm for markets or consumers at large. The latest report from the BLS reported an overall increase in headline inflation of 0.3% month on month – an increase that was inline with nearly all economists polled prior to the announcement. Looking at the headline number on an annualized basis, inflation rose 0.1 percent In the 12 months through June, following an unchanged reading for the month of May.

Gasoline prices rose 3.4% month on month, following a 10.4 percent surge in May. Given the recent volatility in crude oil prices and inventory data in July, there could be scope for the influence of rising gas prices to subside in coming months. Oil is currently trading within the $50-60 / bbl range, well below the levels seen in May and June.

Core CPI, which excludes food and energy related costs, increased 0.2 percent month on month following a rise of 0.1% previously. On an annualized basis, core CPI has now risen 1.8 percent.The June reading continues to highlight just how tame the inflationary environment is within the US economy at present. The strong dollar is helping to keep a lid on inflation by reducing the price of imports and wholesale costs. The strong US dollar has been been spurred partly by a flight to safety due to concerns in Europe and China, and partly by the market’s anticipation of a Fed rate hike later this year. We should expect to start hearing comments regarding the damaging effects of the stronger dollar by Fed officials in the weeks and months ahead should this trend continue.

The food index posts largest increase since September 2014

The price of food increased 0.3% in June, largely to an ongoing shortage in wholesale eggs which has caused a sharp jump in retail egg prices across the nation. Egg prices jumped 18.3% in June, the largest monthly gain since August 1973. Elsewhere, the index for meats, poultry, fish, and eggs rose 1.4 percent in June, with the beef index rising 0.9 percent. Food prices are likely to remain elevated in the coming months as the aftermath of the bird flu epidemic works its way through the supply chain. Wholesale food costs have been consistently increasing in PPI surveys, and these costs are likely to make their way down to the consumer in the weeks and months ahead.

Medical Price Inflation starting to cool off

Medical related inflation cooled in June which will be a welcome deviation from the overall trend in 2015. The price for Medical Care Services fell -0.2% in June and the prices for Medical Care Commodities remained unchanged month on month. Health care costs have been one of the largest contributors to inflation over the past 12 months, with both indices rising 2.3 percent and 3.3 percent respectively.

Rent Prices continue to Climb Higher

The shelter index climbed 0.3% in June, and 3% on an annualized basis as the supply of housing continues to shrink in key regions. Rent increases are also amongst the largest contributors to overall inflation in the United States within the past 12 months.

Outlook for Rates

This month’s CPI data contains no surprises, and the relatively tame reading in the core number on the back of the strong US dollar will likely stick in the minds of Fed officials in the weeks ahead. Globally, sentiment continues to wane dramatically given the continued turmoil in Greece, and increasingly China. While Greece appears to be on the verge of some sort of political settlement, the headline risk remains. In China’s case, there is a very real danger of investor sentiment turning, which could spell disaster for emerging markets overall. Latin American and South East Asian markets look at particular risk, especially on the currency front. The fate of these regions would be sealed in no uncertain terms should the Fed raise rates, and it is for this reason that it appears increasingly unlikely that the Fed will raise by year end, despite all of their rhetoric and expressed intention to do so.

by Andrew | Jul 10, 2015 | In the news, Inflation

Rising tensions within global financial markets were the dominant concerns among Fed officials according to minutes just released from their June policy meeting, leading to yet another delay in the Fed’s widely anticipated normalization of interest rate policy. Uncertainty surrounding the future of Greece and ongoing market weakness in China triggered a cautious tone among most members, although signs of continued strength in the domestic economy, especially the labor and housing markets provided enough signs encouragement for other members to favor a rate hike in the near future.

The tug of war between these two forces will be the dominant theme for Fed watchers going forward, and signs of either beginning to dominate in the weeks ahead should offer some more concrete insight into the timing of the Fed’s next move.

In the Fed’s own words:

“Many participants emphasized that, in order to determine that the criteria for beginning policy normalization had been met, they would need additional information indicating that economic growth was strengthening, that labor market conditions were continuing to improve, and that inflation was moving back toward the Committee’s objective.”

The Fed is essentially adopting a “wait and see” approach before pulling the trigger on a rate hike which might seem premature in hindsight.

The Good – Labor Market Continues to Pick Up

On a positive note, job creation and improved employment prospects according to official figures has buoyed the Fed’s expectations for wage growth to pick up for the rest of the year. Recent consumer confidence surveys echo the Fed’s optimism, with average consumers hopeful of real wage increases in the coming months. Increased wage growth would help boost the domestic economy going forward, and the Fed will likely keep monitoring the retail sales data and employment figures closely in the weeks and months ahead for signs of a solid platform of growth emerging.

The Bad and The Ugly – Greece Weighs on Fed Outlook

Dissecting the June minutes in more detail reveals the Fed’s growing concern about the disruptive influence of overseas market turmoil arriving on domestic shores. Greece clearly weighed on policy makers minds, with particular focus on the contagion “Grexit” would cause for European financial institutions, and the domino effect this could have on US banks.

The Fed didn’t mince any words in this regard.

“[M]any participants expressed concern that a failure of Greece and its official creditors to resolve their differences could result in disruptions in financial markets in the euro area, with possible spillover effects on the United States.”

An important point to note is that the June FOMC policy meeting took place well before the most recent turmoil in Greece really flared up. It’s almost certain that the Fed would be adopting even softer language surrounding Greece given recent events. The Chinese stock market has also imploded in recent weeks, and is likely to overshadow even Greece in the near future as the biggest threat to worldwide economic stability. In recent weeks China has employed a variety of increasingly desperate measures to help slow the stock market decline, but neighboring countries in the Asia Pacific region will be looking on anxiously for signs of contagion in the near future.

Inflation continues to remain below target

On the inflation front, the minutes identified stabilizing oil prices as a potential boost to inflationary pressures within the economy in the coming months. The Fed expects increased energy costs combined with a tightening labor market to help push inflation back towards its target of 2% by the end of year – current levels are well below target.

Summing up the inflation environment and economic picture in the Fed’s own words:

“The information reviewed for the June 16-17 meeting suggested that real gross domestic product (GDP) was increasing moderately in the second quarter after edging down in the first quarter. Labor market conditions improved somewhat further in recent months. Consumer price inflation continued to run below the FOMC’s longer-run objective of 2 percent and was restrained significantly by earlier declines in energy prices and decreases in prices of non-energy imports. Survey measures of longer‑run inflation expectations remained stable, while market-based measures of inflation compensation were still low.”

In summary, it is clear there is growing sense of frustration within the Fed with regards to its inability to start normalizing rates which have been set near zero percent since the onset of the 2008 crisis. With ongoing stress in world financial markets, the Fed knows a premature hike in rates would be enough to send many nations over the edge into a full blown recession. Upcoming domestic data will be key in the coming weeks, should there be a deterioration in the domestic economic picture, then all bets for any form of rate hike this year would certainly be off.

by Ryan Barnes | Mar 25, 2015 | CPI, Definitions, gold, Inflation

The U.S. economy got a little economic boost today with a stronger-than-expected CPI reading for February, and a strong Purchasing Manager’s Index (PMI) that continued to project GDP growth.

Headline CPI and core CPI both came in 0.2% higher than January, as slight price hikes at the pump for refined products balanced out a general breather in the declines in some of the base commodities. The headline numbers had been tracking negative for the past three months, which everyone was pretty much ok with chalking up to crude oil. Just so long as GDP growth came in respectably, there wasn’t any reason to panic.

But core CPI (ex-food and energy costs) was already lagging behind Fed goals of around 2%, and already in the midst of sending deflationary ripples up the global goods chain, into…well, just about everything.

Muddled Waters for First Rate Hike

It’s created a tense chess match between investors and the Fed the past few weeks. It started just after the stellar (as in +295,000) February jobs report last month, when the consensus started to form that the Fed would have to act sooner rather than later in creating a interest rate normalization cycle.

The key first step of that cycle is getting us off the floor of zero percent rates – a stance that doesn’t befit a growing economy and presents what Yellen herself has called an “asymmetrical risk”.

U.S. Definitely Growing…But How Much?

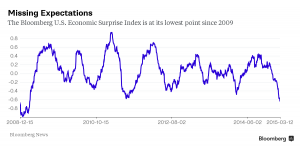

Just as soon as we seemed to have some headway into a summer rate increase, nearly every economic indicator in the U.S. started been printing well below analyst estimates. In fact, the depth of our misses has hit a multi-year high, according to Bloomberg analysis:

In light of this reversal, both investors and the Fed have had to take stock of things. First quarter GDP estimates continue to be ratcheted down – from the 2.5% – 3.0% level I highlighted last month (a number that was freshly lowered at the time) to an average Q1 GDP estimate of about 1.5% today.

Cranky Markets are Volatile Markets

It’s why we’ve seen a spike in volatility around every asset class – fixed income, forex, commodities, and equities have all been bumping around trying to align their compass to the next clear trend line. Would the Fed remove “patient” in the March FOMC meeting? Was September the new June (for the first rate hike)? Was 2015 off the table entirely?

Answering these questions is challenging enough in isolation, but it’s been exacerbated by the stunning rise the the USD index, which alters true price action in commodities and long bonds. The surging U.S. dollar is a de facto rate hike. It lowers the cost of imports dramatically (a deflationary force), and it makes our exports more expensive overseas.

And while the realities of pricier U.S. exports certainly hurt some companies more than others, the simple fact is that close to 50% of the total revenues of the S&P 500 member companies is derived in a currency other than the U.S. dollar.

2014, Part Deux?

It’s quite astonishing how much the first quarter of this year is looking like the first quarter of last year. Tick by tick, indicator by indicator, we seem to be replicating that market environment.

This time last year we were watching interest rates hit new lows, but convinced the party had to end any moment – inflation was coming, and we needed to position ourselves away from fixed income and into equities, gold, and other commodities. Fixed income turned out to deliver stronger returns than even equities did.

GDP looked to be on track for a good start to the year, but then a bout of really bad whether caused us to actually contract as an economy in Q1. Most of the top analysts said “don’t worry, we’ll be strong in the back half of the year”, and sure enough we were. The U.S. turned in over 4.5% growth in the next two quarters.

Looking around today, it’s much the same setup – so far. The key differences between then and now are this:

1) the unemployment rate is lower than last year; we have clearly moved close enough to full unemployment in the Fed’s eyes that it’s no longer an impediment to a rate increase. That box is checked off.

2) the USD is much stronger (10-20% or more) against every major global currency. As I’ve discussed, this move alone is the equivalent of a 25-50 bps rate hike.

In fact, if the dollar hadn’t been zooming so hard the past six months, there’s a chance the Fed would’ve put a token 25bp hike out there last week. Instead, Yellen reminded us that the Fed isn’t there to make things easy for investors, saying the Fed “can’t provide and shouldn’t provide” certainly to markets when it comes to the timing of rate hikes.

We don’t seem to be in any danger of that.

by Andrew | Mar 6, 2015 | BLS, CPI, Inflation

Inflation is one of the most important economic indicators for everyone, especially for investors, businesses, retirees, and policymakers. It affects the cost of groceries, rent, mortgage rates, wages, savings accounts, bond yields, retirement planning, and even the way the Federal Reserve thinks about interest rates.

But here is the part many people miss: there is not just one way to measure inflation.

On this site, we focus heavily on the CPI inflation calculator because the Consumer Price Index is one of the most widely recognized inflation measures in the United States. But CPI is only one part of the bigger picture. Economists, investors, journalists, and the Federal Reserve also look at PPI, PCE, Core CPI, Core PCE, Chained CPI, wage growth, commodity prices, and other indicators.

I have been writing about financial and investment-related topics for more than two decades, and one lesson I have learned is that inflation data can tell different stories depending on the measure you use. That does not mean one number is “fake” and another is “real.” It means each measure has a different purpose, a different method, and a different weakness.

Quick Answer: What Is the Best Way to Measure Inflation?

Honestly, there is no single perfect inflation measure. CPI is useful for understanding consumer price changes. PCE is closely watched by the Federal Reserve. PPI can show price pressure before it reaches consumers. Core inflation strips out volatile food and energy prices. The best approach is to understand what each measure is designed to show, then use them together.

The Bureau of Labor Statistics describes CPI as a measure of the average change over time in prices paid by urban consumers for a representative basket of consumer goods and services. The Bureau of Economic Analysis says the PCE Price Index captures inflation or deflation across a wide range of consumer expenses and reflects changes in consumer behavior. The Federal Reserve’s 2% longer-run inflation goal is measured using the annual change in the PCE Price Index, not CPI.

Why Inflation Is Measured in Different Ways

Inflation sounds simple: prices go up, and money buys less. But measuring inflation across a large, complex economy is not simple at all.

Different people spend money differently. A retiree, a renter, a homeowner, a student, a family with young children, and a small business owner may all experience inflation in very different ways. One person may feel food inflation most. Another may feel rent, insurance, healthcare, or gasoline more sharply.

That is why different inflation measures exist. Each one answers a slightly different question.

| Inflation Measure |

What It Measures |

Why It Matters |

| CPI |

Prices paid by urban consumers for a basket of goods and services. |

Commonly used by consumers, media, contracts, and inflation calculators. |

| PPI |

Prices received by domestic producers for goods and services. |

Can show inflation pressure before it reaches consumers. |

| PCE |

Prices paid for goods and services consumed by people in the U.S. |

The Federal Reserve’s preferred inflation measure. |

| Core CPI / Core PCE |

Inflation excluding food and energy. |

Helps show underlying inflation trends without the noisiest categories. |

| Chained CPI |

Consumer inflation adjusted for substitution behavior. |

Can reflect how consumers change purchases when prices shift. |

| Alternative indicators |

Gold, commodities, wages, rents, market expectations, and private estimates. |

Can provide context, but should not replace official inflation data. |

Official Government Inflation Measures: CPI and PPI

The Bureau of Labor Statistics has the difficult job of collecting and publishing several major U.S. inflation measures. Two of the most widely followed are the Consumer Price Index and the Producer Price Index.

Consumer Price Index: CPI

The Consumer Price Index, or CPI, measures the average change over time in prices paid by consumers for a representative basket of goods and services. It is probably the inflation measure most people recognize because it appears in news headlines, wage discussions, cost-of-living adjustments, and many personal finance calculations.

The CPI includes major categories such as food, housing, apparel, transportation, medical care, recreation, education, and other goods and services. If you want a deeper explanation of the method, we have a guide on what the Consumer Price Index is and how it is calculated.

One reason CPI matters so much is that it gives consumers a practical way to understand changes in purchasing power. When CPI rises, the same dollar generally buys less than it did before. You can see this clearly by comparing historical prices with our historical CPI tables.

The image above shows why the CPI is sometimes described as a “basket of goods” measure. In simple terms, the BLS tracks a representative mix of consumer spending categories and uses that basket to estimate how prices are changing over time. You can read more about this concept in our guide to what a basket of goods means.

Best use of CPI: CPI is useful when you want to understand consumer-facing inflation, cost-of-living changes, or how much purchasing power has changed over time.

Producer Price Index: PPI

The Producer Price Index, or PPI, measures price changes from the producer side of the economy. According to the BLS, PPI measures the average change over time in selling prices received by domestic producers for goods and services.

PPI matters because producer prices can sometimes move before consumer prices. If businesses pay more for raw materials, labor, energy, shipping, or wholesale goods, those higher costs may eventually show up in consumer prices.

That does not always happen immediately. Some companies absorb higher costs to stay competitive. Others pass costs on quickly. The result depends on demand, competition, pricing power, profit margins, and the broader economy.

Still, PPI is worth watching because it can provide an early signal of inflation pressure inside the production pipeline.

Best use of PPI: PPI is useful when you want to understand inflation pressure before it fully reaches consumers. It can be especially helpful for investors, business owners, and analysts watching supply chains and profit margins.

PCE Inflation: The Fed’s Preferred Measure

The Personal Consumption Expenditures Price Index, usually called the PCE Price Index, is another major inflation measure. It is produced by the Bureau of Economic Analysis rather than the Bureau of Labor Statistics.

PCE is especially important because it is the Federal Reserve’s preferred inflation measure. The Federal Reserve says it seeks inflation of 2% over the longer run as measured by the annual change in the PCE Price Index.

One reason economists like PCE is that it can better reflect changes in consumer behavior. For example, if beef prices rise sharply and consumers buy more chicken instead, PCE is designed to capture this kind of substitution more flexibly than traditional CPI.

PCE also covers a broader range of expenditures, including some purchases made on behalf of consumers, such as certain healthcare costs paid by employers or government programs.

| CPI |

PCE |

| Produced by the Bureau of Labor Statistics. |

Produced by the Bureau of Economic Analysis. |

| Focuses on out-of-pocket prices paid by urban consumers. |

Covers a broader range of consumption expenditures. |

| Often used in media, contracts, calculators, and cost-of-living discussions. |

Preferred by the Federal Reserve for its inflation target. |

| May show a different inflation rate than PCE. |

Can better reflect substitution and changing spending patterns. |

For everyday consumers, CPI is often easier to understand. For monetary policy, PCE is often more important. If you are trying to understand what the Fed may do with interest rates, you should pay attention to PCE and Core PCE as well as CPI.

Core Inflation: Why Food and Energy Are Often Excluded

Core inflation usually refers to inflation excluding food and energy. At first, this can sound strange. Food and energy are not optional for most households. Anyone who buys groceries or fills up a car knows these prices matter.

So why exclude them?

The reason is not that food and energy are unimportant. The reason is that food and energy prices can swing sharply from month to month because of weather, wars, supply disruptions, seasonal changes, oil markets, and other temporary shocks. By removing those categories, economists try to get a cleaner view of the underlying inflation trend.

Core CPI and Core PCE are both widely watched. The BEA notes that Core PCE, which excludes food and energy, is closely watched by the Federal Reserve as it conducts monetary policy.

In my view, consumers should look at both headline and core inflation. Headline inflation shows what people are actually paying across the full basket. Core inflation helps show whether inflation pressure is becoming more deeply embedded in the economy.

How to Think About Headline vs. Core Inflation

- Headline inflation includes food and energy, so it can better reflect what households feel month to month.

- Core inflation excludes food and energy, so it may better reflect the underlying trend.

- Both matter because consumers live with headline inflation, while policymakers often focus closely on core inflation.

Chained CPI: Measuring Substitution Behavior

Chained CPI is another inflation measure that tries to account for changes in consumer behavior. When prices rise, people often substitute cheaper products for more expensive ones. For example, if one type of meat becomes much more expensive, a household might buy a different protein instead.

Traditional CPI measures price changes based on a basket of goods and services. Chained CPI adjusts more directly for the way consumers shift spending when relative prices change.

This can make Chained CPI grow more slowly than traditional CPI in some periods. Supporters argue that it reflects real consumer behavior more accurately. Critics argue that it may understate the pressure felt by households that cannot easily substitute away from rising costs like rent, healthcare, insurance, or utilities.

That is a key theme across inflation measurement: every method has tradeoffs.

Median CPI and Trimmed Mean Inflation

Some economists use inflation measures that remove extreme price movements, not just food and energy. Two examples are Median CPI and trimmed mean inflation.

The idea is simple. In any given month, a few categories can jump or fall dramatically. Those outliers can distort the headline number. Median and trimmed mean measures try to show the middle of the inflation distribution by reducing the influence of extreme categories.

The Federal Reserve Bank of Cleveland has also explained how CPI and PCE differ, including why the Fed’s preferred measure is PCE. Regional Federal Reserve banks often publish useful inflation research, including measures such as median CPI and trimmed mean inflation.

These measures are more technical, but they can be helpful when headline inflation is being distorted by one-time spikes in categories like energy, used cars, airline fares, or shelter.

Wage Inflation and Labor Costs

Inflation is not only about consumer prices. Wages and labor costs also matter.

If wages rise faster than productivity, businesses may raise prices to protect margins. On the other hand, if consumer prices rise faster than wages, households lose purchasing power. That is why wage growth and inflation are often discussed together.

For consumers, the practical question is simple: is your income rising faster than your cost of living?

A 4% raise does not feel like a raise if your personal cost of living rises 6%. This is one reason many households can feel financially squeezed even when the official economy looks stable.

To understand why inflation affects households so differently, it helps to read our guide on how CPI affects inflation.

Commodity Prices, Gold, and Market-Based Inflation Signals

Some investors also watch commodity prices, including oil, copper, agricultural products, and gold, for clues about inflation. These indicators can be useful, but they need to be handled carefully.

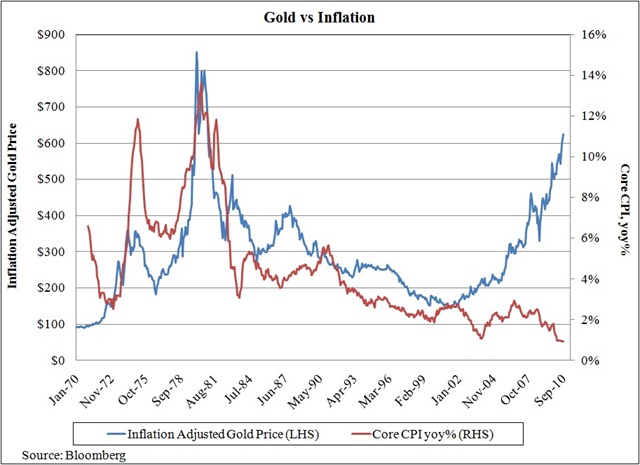

Gold has historically been seen by many investors as a store of value and a hedge against currency weakness, inflation risk, and financial stress. When investors lose confidence in paper currencies, central banks, or the broader financial system, gold may attract more attention.

The chart above reflects the older version of this article’s discussion around gold and inflation. I still think gold is worth watching, but I would not treat it as a clean inflation measure. Gold prices can be influenced by real interest rates, the U.S. dollar, central bank buying, geopolitical risk, investor fear, and long-term demand for hard assets.

That means gold can provide useful context, but it should not replace CPI, PCE, or other official inflation data. If you are interested in that topic, we have a dedicated article on whether gold is a good inflation hedge, as well as an inflation-adjusted gold return calculator.

Investor note: Gold, oil, copper, and other commodities can provide signals about inflation pressure, but they also react to many non-inflation factors. I view them as context, not replacements for official inflation indexes.

Private and Alternative Inflation Estimates

Some investors and analysts are skeptical of official inflation statistics and prefer to track alternative estimates. This skepticism has existed for a long time, especially among people who believe CPI does not fully capture the cost pressures they feel in daily life.

I understand the frustration. Official inflation data can feel disconnected from your household experience if your rent, insurance, groceries, or healthcare costs are rising faster than the national average.

At the same time, I would be careful about treating private inflation estimates as automatically more accurate. Official statistics have limitations, but they also use transparent methodologies, large datasets, and long historical series. Private estimates can be useful as a second opinion, but they may also use assumptions that produce very different results.

The better approach is not to rely blindly on any single number. Look at multiple indicators and understand what each one is measuring.

Why Your Personal Inflation Rate May Differ From CPI

One of the most important points in this article is that the official inflation rate may not match your personal inflation rate.

CPI is based on average spending patterns. But your household is not average. Your budget might be heavily weighted toward rent, childcare, gasoline, insurance, healthcare, or food. If those categories rise faster than the overall CPI, your personal inflation rate may feel much higher.

| Household Type |

Inflation They May Feel Most |

| Renter |

Rent increases, utilities, insurance, transportation. |

| Homeowner |

Property taxes, insurance, repairs, maintenance, utilities. |

| Retiree |

Healthcare, food, insurance, utilities, fixed-income pressure. |

| Commuter |

Gasoline, auto insurance, repairs, financing costs. |

| Family with children |

Food, childcare, housing, education, clothing, medical costs. |

This is why I usually recommend looking at both official inflation and your own budget. The CPI tells you what is happening broadly. Your bank statement tells you what is happening personally.

How Investors Can Use Different Inflation Measures

Investors should pay attention to inflation because it affects interest rates, bond yields, stock valuations, commodity prices, real estate, cash returns, and retirement planning.

For example:

- CPI helps investors understand consumer-facing inflation and purchasing power.

- PPI can show cost pressure on companies before it reaches consumers.

- PCE matters because the Fed uses it for its inflation target.

- Core inflation helps show whether inflation pressure is broad and persistent.

- Commodity prices can offer market-based clues, especially around energy and materials.

- Wage growth can show whether consumers are keeping up with price increases.

If you are building a portfolio, inflation matters because what counts is your real return, not just your nominal return. A 5% investment return looks good until inflation is 4%. In that case, your real return before taxes is only about 1%.

For more on that topic, read our guide to investing during inflation and deflation or our article on inflation-resistant investment ideas.

How Consumers Can Use Inflation Data

You do not need to be an economist to use inflation data. For regular households, inflation data can help with budgeting, wage negotiations, retirement planning, debt decisions, and savings goals.

Here are a few practical ways to use it:

- Use CPI to understand how prices have changed over time.

- Compare your wage growth with inflation to see whether your real income is rising.

- Review your savings rate against inflation to understand your real return.

- Use inflation assumptions when estimating future retirement expenses.

- Watch PCE and Core PCE if you are trying to understand the Federal Reserve’s likely policy direction.

- Track CPI release dates using our CPI release schedule.

Inflation can also connect to broader economic cycles. If you want to understand the relationship between inflation, slowdowns, and contractions, read our explainer on inflation vs. recession vs. depression.

Which Inflation Measure Should You Trust?

The honest answer is that you should not rely on one measure alone.

CPI is useful for understanding consumer prices. PCE is important for Federal Reserve policy. PPI can provide early warnings about business cost pressures. Core inflation can help identify underlying trends. Gold and commodities can provide market context. Your personal budget tells you what inflation feels like in your real life.

If I had to simplify it, I would say this:

My Practical Inflation Dashboard

- For household purchasing power: CPI and your own monthly spending.

- For Federal Reserve policy: PCE and Core PCE.

- For business cost pressure: PPI.

- For underlying trend: Core CPI, Core PCE, median CPI, and trimmed mean measures.

- For market sentiment: gold, oil, commodities, bond yields, and inflation expectations.

No measure is perfect. But together, they can give you a much more complete picture of inflation than any single headline number.

Final Thoughts: Cover All Bases

There is no single inflation measure that tells the whole story. CPI, PPI, PCE, Core PCE, Chained CPI, commodities, wages, and private estimates all provide different pieces of the inflation puzzle.

The important thing is to understand what each measure is good at and where it falls short.

For most consumers, CPI is the easiest inflation measure to understand. For monetary policy, PCE is crucial. For investors and business owners, PPI and core inflation can help reveal pressure building beneath the surface. For your own household, your personal budget may be the most important inflation measure of all.

That is why I believe the best approach is to cover all bases. Follow the official numbers, understand their limitations, and compare them with your real-life spending. Inflation is not just a government statistic. It is something you feel every time your money buys less than it used to…