One of the more interesting sets of data to catch our attention in recent months is the National Association of Credit Managers CMI Index – a broad measure of the underlying credit conditions affecting both the manufacturing and service sectors in the US economy. The CMI has proved to be a valuable leading indicator since its inception in 2002, successfully predicting both the start and the end of the credit crisis in 2007 and 2009 respectively.

Given the important role credit plays in the overall economy, following a gauge of credit conditions on a month to month basis provides an excellent insight into just how healthy the flow of credit is throughout the business sector. From this vantage point, the trend emerging from recent data is worrying on all fronts and could have serious ramifications for the economy in remaining quarters of 2015.

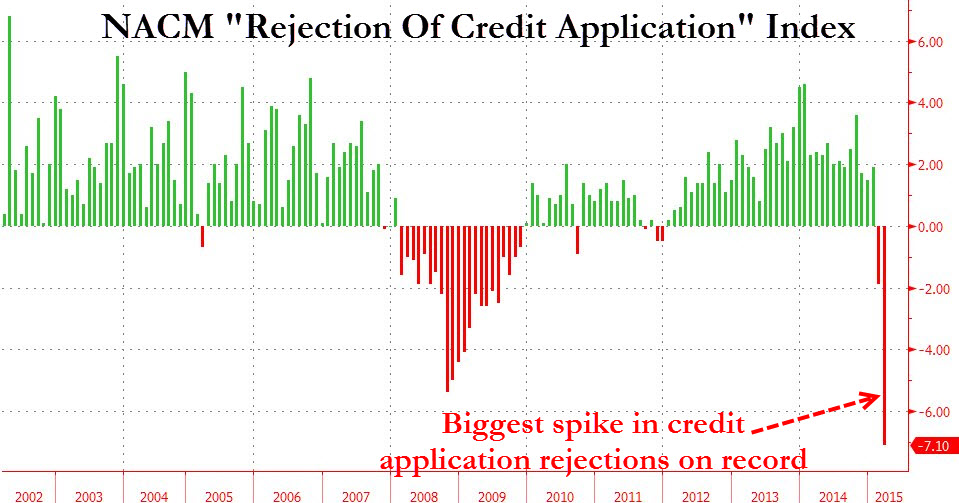

Full Blown Recessionary Signal in March (or is it… )

In March, the CMI data recorded the biggest deterioration of business credit conditions in over 7 years. The fall in the unfavorable factors part of the index, tumbled from 50.5 to 48.5 – the lowest level since the 2008 recession formally ended. The data turned the heads of many analysts due to the severity of the drop. In the NACM’s own words:

“There is quite obviously some serious financial stress manifesting in the data and this does not bode well for the growth of the economy going forward. These readings are as low as they have been since the recession started and to see everything start to get back on track would take a substantial reversal at this stage. The data from the CMI is not the only place where this distress is showing up, but thus far, it may be the most profound”

Thankfully, if not somewhat surprisingly, the NACM made significant revisions to the March data in its April release – with the sharp falls in February and March replaced with less apocalyptic data points. The massive declines in February and March were revised from 52.1 and 46.1 respectively to 60.5 and 60.6, quite an enormous revision, and one which the NACM were rather vague in explaining. Again, in their own words:

“In February and March the CMI seemed to show a drastic drop in the amount of credit extended by companies to those that wanted to buy their machines or commodities and inventory. There was also a big drop in the number of credit applications submitted. Many of the other categories were also in decline, but these were the most dramatic. Upon reviewing the data and assessing some of the additional numbers it seems that there was not quite the drama originally noted.”

So.. credit crunch avoided, but the data has stoked our curiosity about what exactly did occur in February and March. If credit conditions deteriorated so badly during this period, the trend should surely be mirrored in the consumer credit data – we cracked open the Fed’s latest Consumer Credit report to take a look.

Consumer Revolving Credit Slowdown

While the Fed’s consumer credit lags the NACM (the Fed only has data up until March, the NACM CMI is current through the month of April) the data nevertheless appears to confirm the initial view from the CMI – a significant deterioration in credit availability did occur in the first quarter of 2015. From the Fed’s data, revolving credit fell -3.3% in both January and February of this year before rebounding +5.9% in March, signalling a severe slowdown in credit creation in the early part of the first quarter from non government sources. This was the worst month for revolving credit (predominantly credit cards) since December 2010 and paints a worrying picture regarding the health of the US consumer going forward.

Compounding the sluggish consumer, there also seems to be credit aversion occurring throughout the big banks, with the Fed’s data showing outstanding consumer credit held at depository institutions down -2.5% from the fourth Q4 2014 to March 2015. It would appear from this data that the big banks have pulled their horns in with respect to extending credit to both businesses and consumers in the first three months of 2015 as uncertainty reigns supreme with regards to the timing of the Fed’s next rate hike.

Both data sets have certainly caught our interest and we will be monitoring the Fed’s latest credit report scheduled for release on June 7 for signs of how the current trend is progressing. In the meantime, the data clearly shows the economy is in far less robust health than those calling for a rate hike would care to imagine. The recent fall in global PMIs and factory orders in the US are further signs of a slowdown occurring – we have been calling for an extended period of delayed rate hikes for a while, but this current data seals it.

Andrew McCarthy is an expert in all things inflation. He has a Bachelors in Economics and has been working in the finance industry for over two decades.