by Sarah Bauder | Feb 13, 2020 | CPI, Definitions

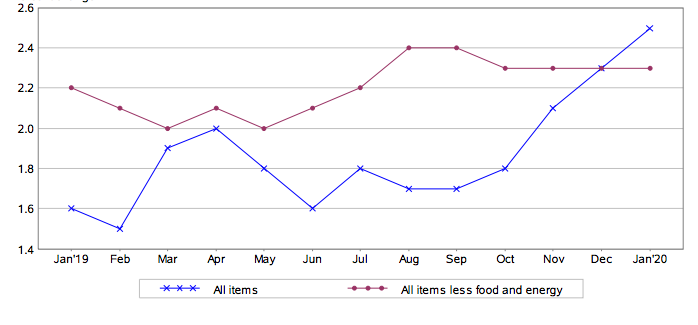

The US Bureau of Labor Statistics (BLS) reported today, that in January, the Consumer Price Index for All Urban Consumers (CPI-U) increased 0.1% on a seasonally adjusted basis. The all items index has risen 2.5% before seasonal adjustment, over the past year.

Based upon the data provided by the BLS, the shelter index was the largest component, which attributed to the rise in the seasonally adjusted all items index. In addition, the medical care and food indexes also increased. Conversely, the energy index dropped in January.

(Source: US Bureau of Labor Statistics)

Energy Index

In January, the index for energy decreased by 0.7%. This is in contrast to December when the energy index edged up 1.6%. The price of gasoline dropped 1.6% in January, compared to the 3.1% rise the previous month. The electricity index edged up 0.4%, as did the natural gas index, with an increase of 1.0%.

Overall, over the past 12-month period, the energy index rose 6.2%. The price of gasoline soared up 12.8% since January 2019. The index for electricity edged up 0.5%, while the natural gas index dropped 3.2%.

Food Index

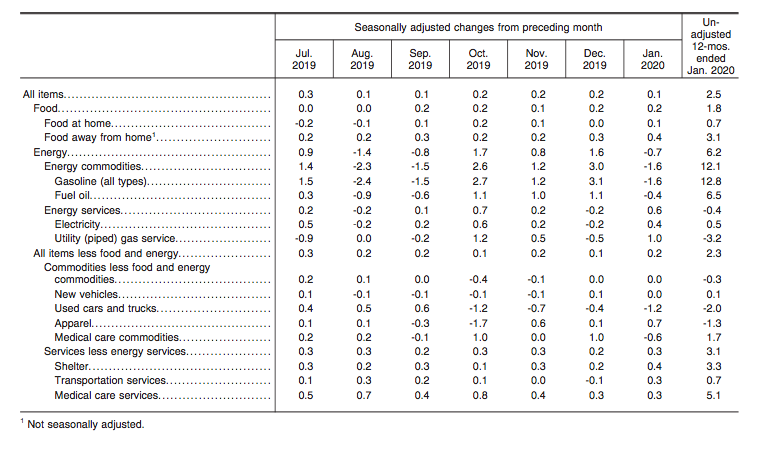

Similarly to December, the index for food rose 0.2%. The food at home index also increased 0.1% in January. The food away from home index also edged up 0.4%.

Since January 2019, the food at home index rose 0.7%. Likewise, the food away from home index also increased 3.1% over the past 12 months.

(Source: US Bureau of Labor Statistics)

All Items Less Food And Energy Index

In January, the index for all items less food and energy rose 0.2% – December saw an increase of 0.1%. As mentioned, the shelter index increased 0.4%. The owners’ equivalent rent index saw a 0.3% increase, and the index for rent rose 0.4%.

The index for medical care also increased by 0.2%, as did the hospital services index, which rose 0.8%.

Over the last 12 months, the all items less food and energy index increased 2.3%. Since January 2019, the index for shelter edged up 3.3%. The medical care index also saw an increase over this same period, rising 4.5%. Over the past 12 months, there have been few indexes that decreased in this category.

Source cited: https://www.bls.gov/news.release/archives/cpi_02132020.htm

by Emily Cross Leon | Apr 15, 2017 | Definitions

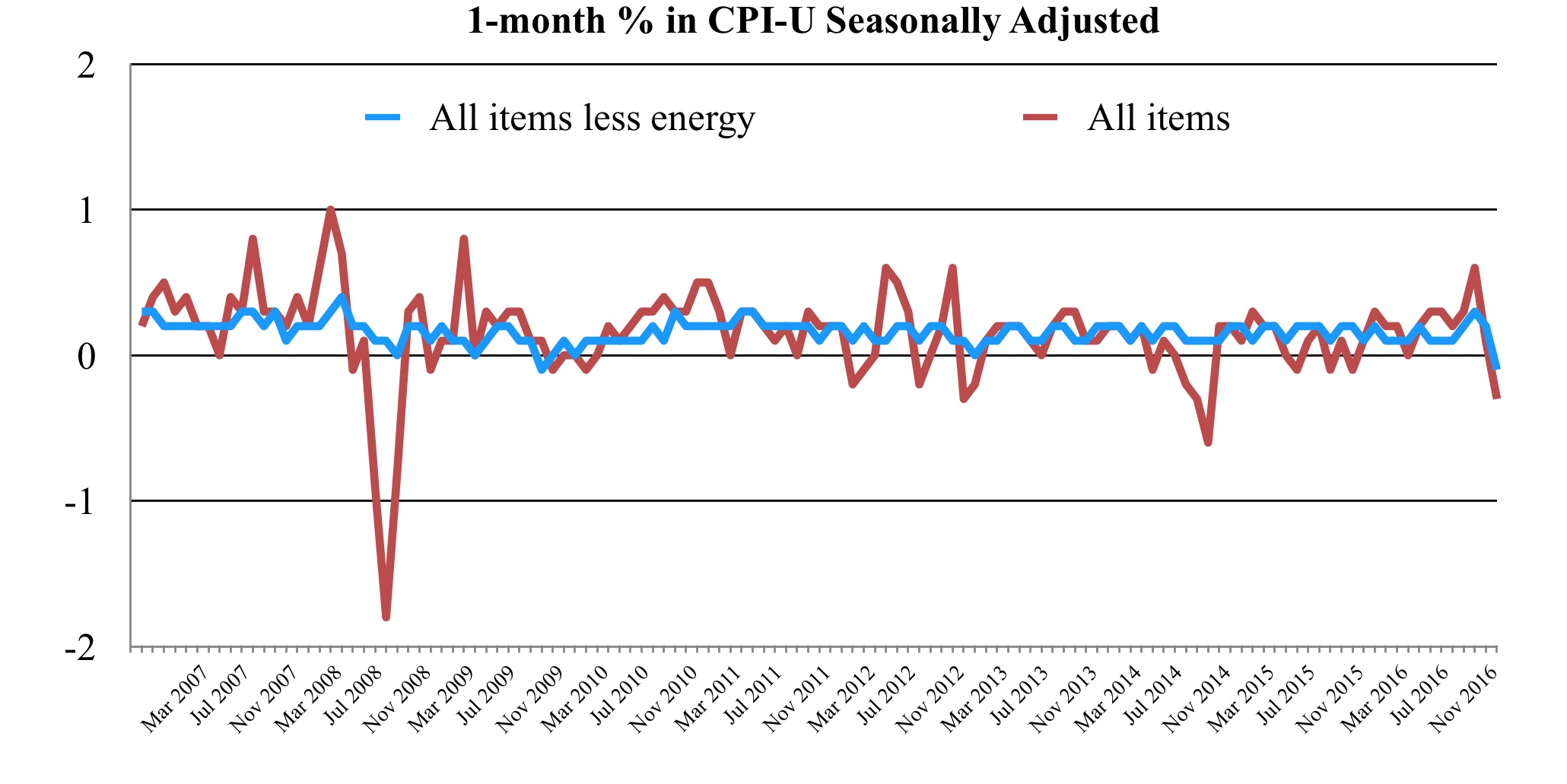

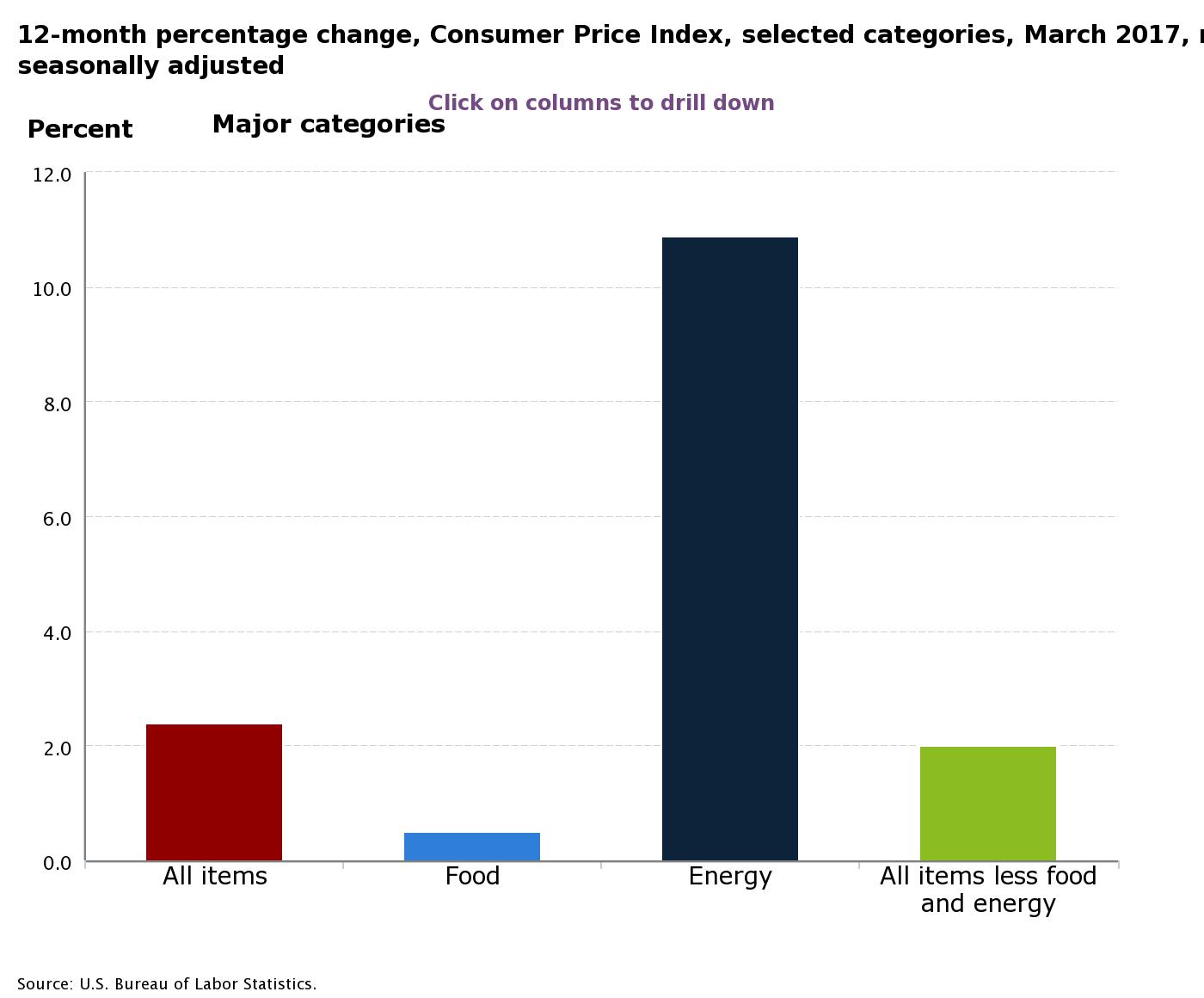

Inflation seemingly took a breath in March. According to Friday’s report from the Bureau of Labor Statistics, prices climbed 2.4% over the 12-months ending in March. Markets had expected an annual rate of 2.6% after February’s five-year peak at 2.7%. For the month, consumer prices inched up 0.1% in March. However, with seasonal adjustments the CPI-U posted a 0.3% decline, the largest one month drop since January 2015, when the all items index fell 0.6% with seasonal adjustments. Only two month ago, monthly inflation was at its highest level since February 2013.

Whether the decline in March represents a temporary blip on the radar or true underlying economic weakness remains to be seen. It is worth noting that when energy is excluded, the CPI-U has grown at a relatively stable rate over the past decade (represented by the blue line in the chart above). Gasoline represents roughly 3.3% of the CPI-U and half of the energy index; it has increased in price by nearly 20% over the past year, despite a 6.2% decline in March. Extreme volatility in the energy index, has been, and continues to be the dominant force impacting headline monthly inflation. Interestingly, March’s monthly decline (excluding energy) is the sharpest in the past 10 years.

March Monthly Prices

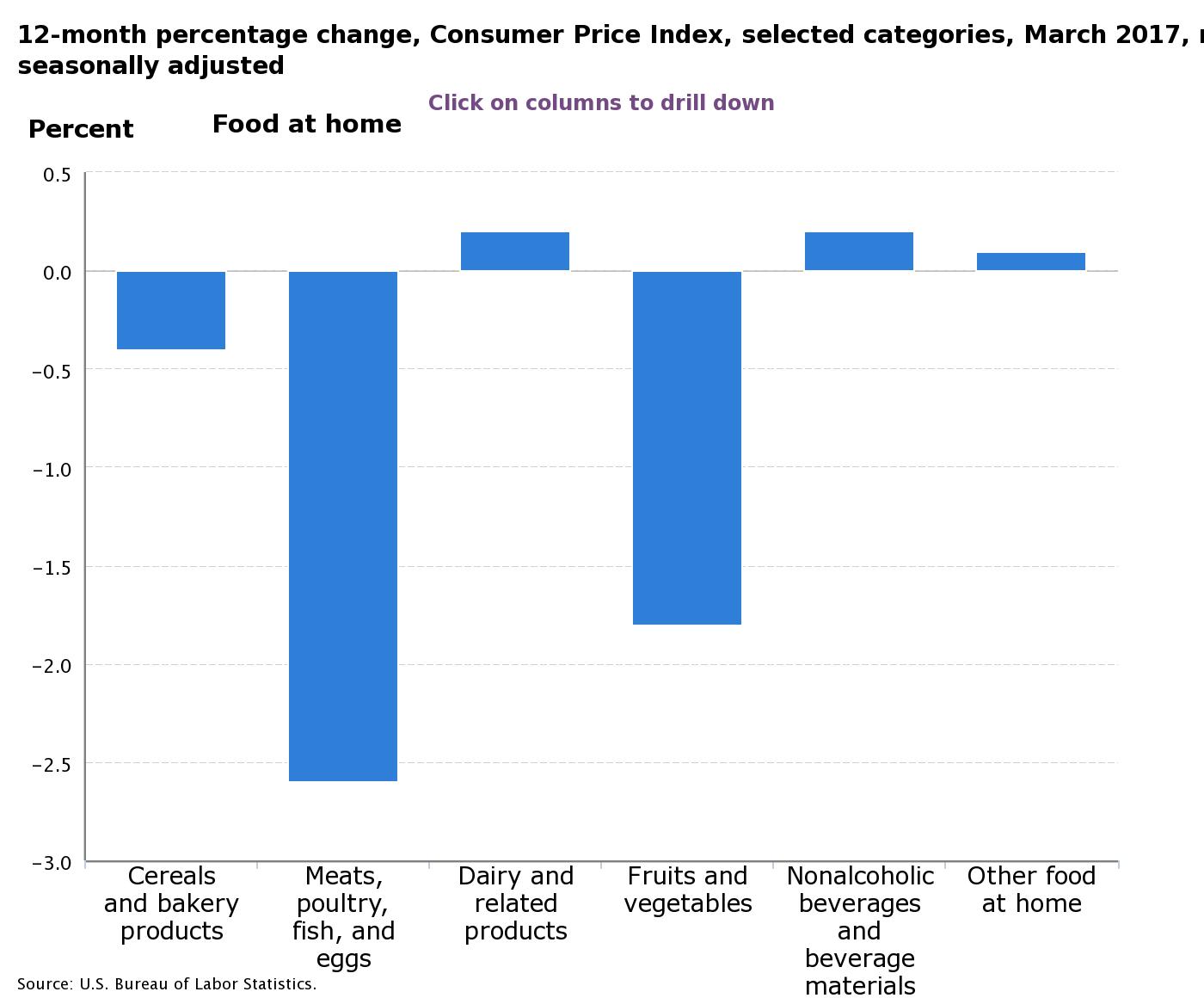

Core prices (excluding food and energy) dropped 0.1% with seasonal adjustments in March, after increasing 0.2% in February. March was the first month that seasonally adjusted core inflation dropped below zero since January 2010. Outside of the core index, food prices climbed 0.3% to more than offset a larger decline in the energy index, which fell 3.2%. Food accounts for around 14% of the all-items index, nearly twice the weight of energy.

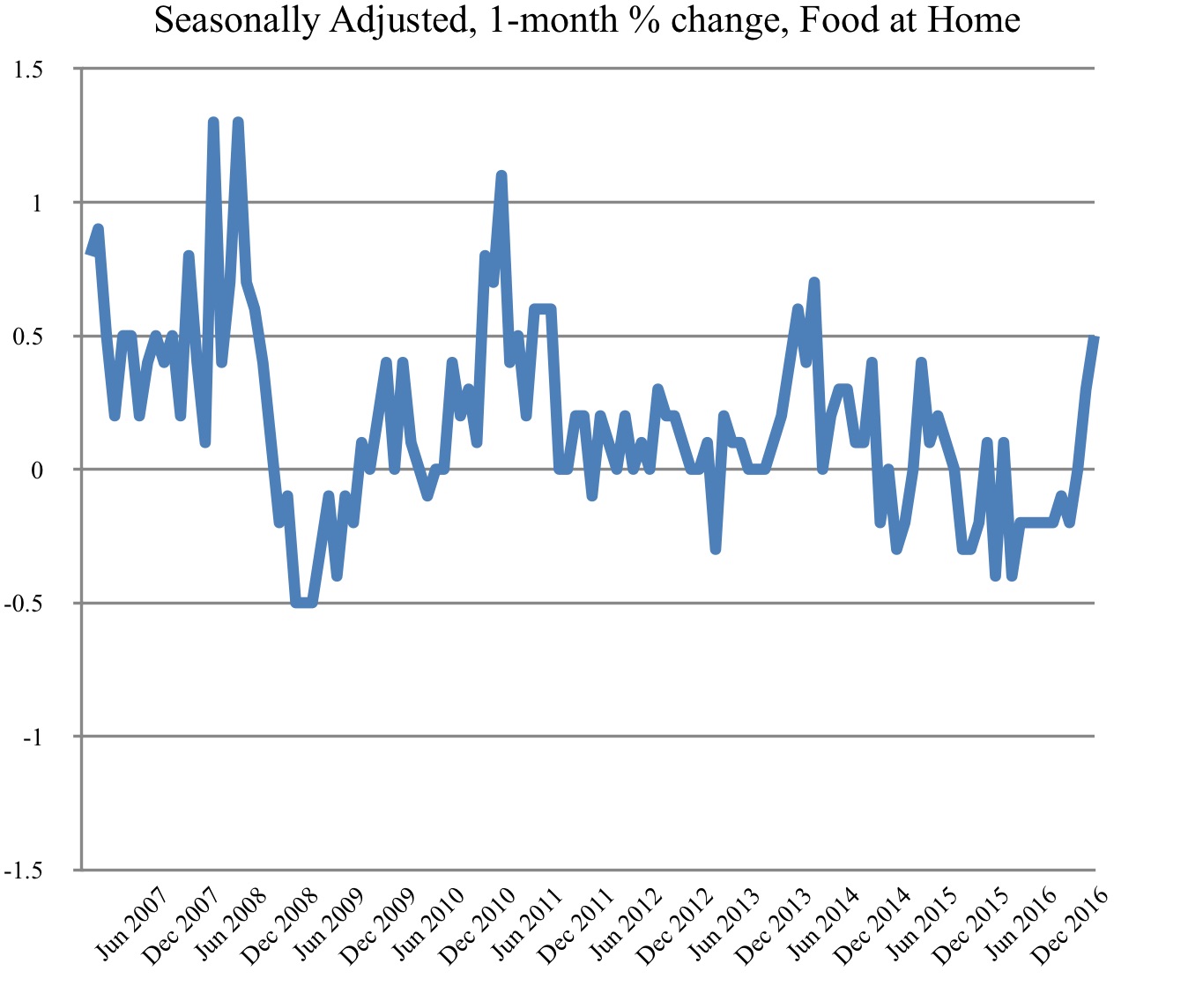

Grocery store prices were up 0.5% in March. Prices were higher in four of the six major grocery store components; the index for other food at home slipped 0.1% and the index for dairy and related products fell 0.6%. The chart below illustrates the volatility of food prices since 2007; even with seasonal adjustments this index fluctuates drastically each month. Since 2014, the index for food at home has posted more months of declines than growth. In recent months, grocery store prices have clearly spiked.

Within the core index, shelter is by far the largest component of consumer spending. The index for shelter added 0.1% in March and 0.3% in February with seasonal adjustments. The price of medical care services was also up 0.1% in March; higher costs for hospital services (up 0.3%) were offset by lower costs for physician services (down 0.4%). The seasonally adjusted price of new vehicles fell for the second month in March, down 0.3% compared to 0.2% in February. Similarly, the index for used cars and trucks fell 0.9% in February adding to declines in both January and February.

Annual Inflation

Core prices climbed 2.0% year-over-year in March, slightly less than the all items index. Meanwhile, energy prices shot up 10.9% as energy commodities (mostly gasoline) surged 19.8% and energy services were up a more modest 3.4% annually. The food index inched up 0.5% over the 12-months ending in March. Grocery store prices fell 0.9% over the year, but this was offset by higher prices for food away from home; that index climbed an annual 2.4%.

Core commodity prices (commodities less food and energy commodities) slumped over the year ending in March, down 0.6%. This includes a 4.7% decline in the index for used cars and trucks. Apparel prices were up just 0.6% year-over-year. On the other hand, the medical care commodities index posted a 3.9% increase.

Over the year, the price of shelter rose 3.5%. Shelter is categorized as a service and service prices were up overall on an annual basis in March. The transportation and medical care service indexes were both higher, up 3.8% and 3.4% respectively. Within the transportation services index, motor vehicle insurance prices jumped 8.0% compared to a year earlier. However, declines in the price of wireless telephone services were the largest on record. That index fell 11.4% year-over-year.

Economic Outlook

The Fed has increasingly expressed their intention to continue raising interest rates, citing positive economic news and burgeoning inflation. The Fed aims to maintain an annual inflation rate close to 2% and they are generally more interested in the core index. When prices are rising faster than their target, higher interest rates prevent the economy from overheating. On the other hand, sluggish inflation is a sign of weak consumer demand and discourages current investment. Friday’s negative report may force the fed to reconsider the pace of rate hikes going forward. Inflation is not the Fed’s only mandate, they also aim to maintain stable and full employment.

by Emily Cross Leon | Mar 16, 2017 | Definitions

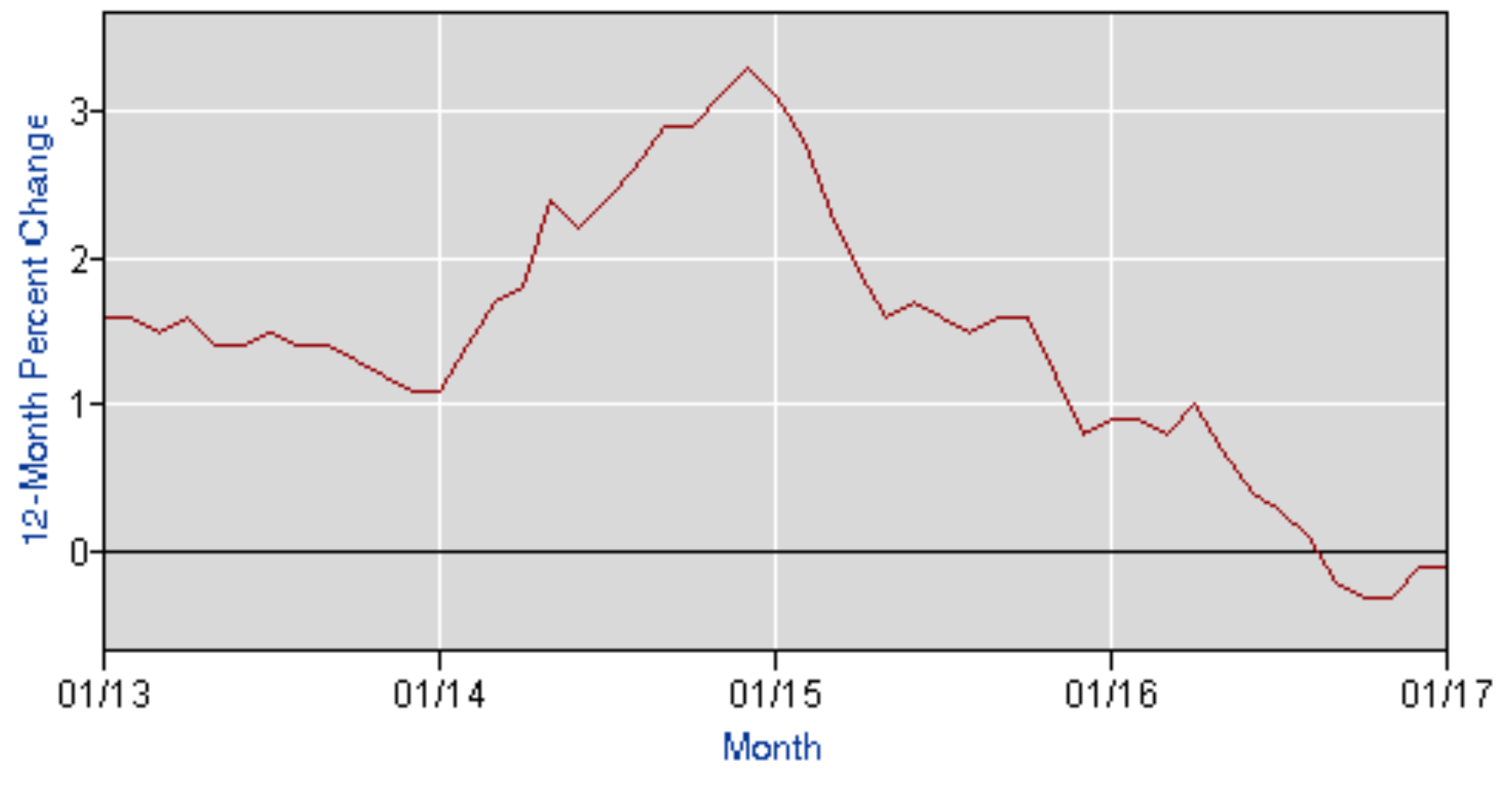

According to today’s report from the Bureau of Labor Statistics, consumer prices grew a modest 0.3% in February, down considerably from 0.6% in January. On an annual basis, the all-items index (CPI-U) was up 2.7% in February and 2.5% in January. These are the highest annual rates in nearly five years (see graph below). Excluding food and energy, consumer prices were up 0.4% in February and 2.2% over the 12-months ending in February. These were the numbers analysts had expected.

Annual Inflation

Year-over-year, the price of food was flat in February despite plenty of volatility in grocery store prices. The price of meat declined significantly, including uncooked ground beef, down 6% and ham, down 3.9%. The price of eggs reportedly dropped 23.6% over the same 12-month period. The index for fresh vegetables fell 7.2% and fruit prices were down 4.3%. These declines were somewhat offset by higher prices for fish and seafood, up 3.4% for the year. Overall, the grocery store index fell 1.7% on an annual basis, while the index for food away from home added 2.4%.

For the year ending in February, the energy index advanced 15.2%. The soaring price of energy commodities was tempered by more modest growth in the price of energy services. Energy commodities, which account for roughly half of the energy index, were 29.8% more expensive in February compared to a year earlier. This is largely the result of higher prices at the pump; the gasoline index grew 30.7% year-over-year. Over the same period, the index for energy services (which includes electricity and utility piped gas) was up 3.5%.

There was a downward trend in the price of many retail commodities over the relevant year. The index for household furnishing and supplies fell 1.7%, while the apparel index inched up just 0.4% and prices for recreational commodities dropped 3.3%. Transportation commodities, which do not include motor fuel, posted a 1.2% annual decline in prices. While the price of new vehicles was up 0.5%, the index for used vehicles dropped 4.3%.

The index for transportation services grew 3.6% annually despite declines in the cost of car and truck rentals, reportedly down 1.7%. Over the same period, the index for motor vehicle maintence and repairs added 2.5%. The major reason for higher transportation service costs was a 7.6% spike in motor vehicle insurance rates. Intercity train fairs also jumped a notable 5.4%.

The price of medical care commodities appreciated significantly over the year. That index was up 4.1%, mostly the result of a 5.2% annual increase in prices for prescription drugs. Similarly, medical care services recorded a 3.4% year-over-year increase. The price for physician services was 3.6% higher compared to a year earlier while the index for hospital services was up 4.3%.

Shelter is the largest component of the all-items index, accounting for over a third of its total. The shelter index, up 3.5% over the year ending in February, is mostly comprised of rental costs including owners equivalent of rent, which is a reflection of home values. The index measuring owners equivalent of rent climbed 3.5% while those renting their primary residence saw costs rise 3.9%.

Inflation in February

In February, the price of food gained 0.2% with both the index for food at home and food away from home rising at that same rate. Three of the six components of grocery store consumption increased by 0.2% over the month; cereals and bakery products, meats poultry fish and eggs and fruits and vegetables.

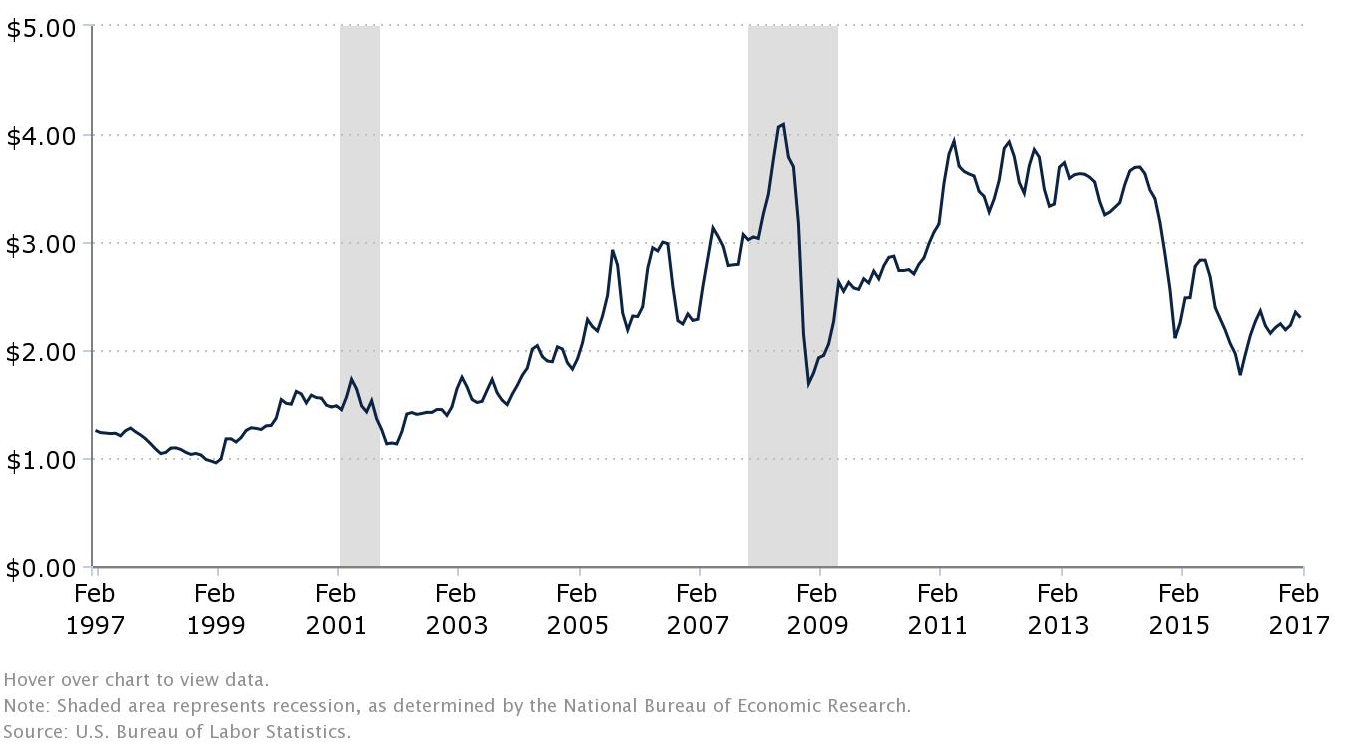

The energy index declined on a monthly basis, down 0.7% in February. Although energy service prices added 0.5%, a 2.0% decline in the the energy commodity index more than offset the rise. Volitile gas prices were once again responsible for changes in the energy index. Prices at the pump dropped 2.1% in February. Gasoline accounts for roughly 3.4% of the all-items index and nearly half the energy index. The graph below illustrates the average price of regular unleaded gasoline per gallon over the past decade.

The apparel index, which includes clothing, footwear and accessories, jumped 2.4% in February. However, with seasonal adjustments, the apparel index was up 0.6%, following a 1.4% seasonally adjusted increase in February. The index for transportation commodities increased 0.2% in February, including 0.4% growth in the price of used vehicles. The transportation services index added a more significant 0.8% in February. The price to lease a car or truck was 2.0% higher for the month and the index measuring the cost of public transportation increased by 2.3%. Medical care was more expensive in February. Medical care commodity prices grew 0.5% as prescription drug costs were 0.6% higher. The medical care service index was also up 0.6% as the price of hospital outpatient services shot up 1.3% in February.

Economic Outlook

Inflation appears to have rebounded despite February’s low monthly rate. The CPI-U has surpassed the Fed’s annual 2% target after remainingy stubbornly low throughout 2015 and most of 2016. Along with higher inflation, employment and economic growth numbers support today’s decision by the Federal Reserve to raise interest rates. The optimism reflected in the stock market also indicates the economy may need to be reigned in. Today, interest rates were increased by 0.25% to a range of 0.75% to 1.0%. Higher rates make borrowing harder for business and consumers but also keep prices from growing to quickly, which is good for the consumer. The Fed did not alter their outlook for 2017, two more rate hikes are expected this year.

Inflation appears to have rebounded despite February’s low monthly rate. The CPI-U has surpassed the Fed’s annual 2% target after remainingy stubbornly low throughout 2015 and most of 2016. Along with higher inflation, employment and economic growth numbers support today’s decision by the Federal Reserve to raise interest rates. The optimism reflected in the stock market also indicates the economy may need to be reigned in. Today, interest rates were increased by 0.25% to a range of 0.75% to 1.0%. Higher rates make borrowing harder for business and consumers but also keep prices from growing to quickly, which is good for the consumer. The Fed did not alter their outlook for 2017, two more rate hikes are expected this year.

by Emily Cross Leon | Feb 16, 2017 | Definitions

Consumers paid more for almost everything in January compared to a month earlier. Headline inflation hit 0.6% for the month after posting a decline in November and no change in December. Inflation in January was well above 2016’s average monthly rate of 1.5%. Year-over-year, consumer prices were up 2.5% in January, slightly more than analysts expected and the highest annual rate since March 2012.

Today’s report from the Bureau of Labor Statics supports the Fed’s case for raising interest rates. However, the CPI-U is not the their preferred measure of inflation. They focus more on the personal consumption expenditure index (PCE), which remains below the 2% target. January’s strong consumer price report coincides with positive retail and employment data – more indications that it’s time to move towards less accommodative monetary policy.

Prices in January

The food index added 0.4% in January as both the index for food at home and the index for food away from home climbed 0.4%. Grocery store prices increased across the board; the index for dairy and related products was up the most, climbing 0.9% and the index for cereals and bakery products ticked up 0.6% month-over-month. Fruits and Vegetables was the only component of grocery store spending to decline, down a monthly 0.1% which becomes a much larger decline of 1.7% after seasonal adjustments. The seasonally adjusted food index inched up 0.1% after remaining flat for most of 2016. Similarly, seasonally adjusted grocery store prices were flat in January, ending a series of declines.

The energy index climbed 3.3% in January, which is a seasonally adjusted 4.0%. Within the the sector, the price of gasoline drove much of the month-over-month growth. Gas prices were reportedly up 5.3% or a seasonally adjusted 7.8%.

Core inflation, which excludes food and energy, was up 0.4% in January. With seasonal adjustments, core inflation was 0.3%. Within the core index, the price of new vehicles increased 1.1%, while prices for used cars and trucks fell 0.1%. Used cars and trucks was the only major expenditure category in the core CPI–U to decline over the month. Core commodity prices were up 0.5% and core services were up 0.3%. The service indexes for both medical care and transportation added 0.4%. Also notable, Airline fares spiked 1.4% in January.

The shelter index, which accounts for roughly one third of the all-items indexed, was 0.3% higher in January. With seasonal adjustments, growth in the price of shelter slowed in January, to 0.2% from 0.3% in both November and December.

Annual inflation

Although energy prices surged over the year ending January, core inflation was also strong, up 2.3% year-over-year. Stagnating food prices countered the impact of higher energy costs within the all-items index. Food prices fell an annual 0.2% in January while the price of gasoline pushed 20.3% higher. The graph below shows the 12-month change in the food and beverage index falling throughout 2015 and 2016. Overall grocery store prices were down 1.9% for the year ending January and the cost of food away from home reportedly climbed 2.4%.

The jump in the energy index was caused by higher gas and fuel oil prices. Energy commodities represent roughly half of the energy index, which is close to 7% of the all-items indexed. A 20% spike in the energy commodity index contributed nearly 0.7% to overall inflation for the year. Energy services, on the other hand only added 2.9% over the 12-month ending in January.

Within the core index commodity prices slid 0.2% over the year, largely the result of a 3.7% decline in the price of used cars and trucks. In general, commodity prices were up for the year, with medical Medicare commodities rising the most, up 4.7% annually.

Shelter prices were significantly higher year-over-year; that index was up 3.5%, including 3.9% growth in the index for rent. Medical care and transportation services were also more expensive, up 3.6% and 3.2% respectively. Despite spiking in January, Airline fares fell 3.3% for the year.

Economic Outlook

Addressing congress this week, Chairman of the Federal Reserve, Janet Yellen spoke of the possibility of rate hikes as soon as next month. She also warned of the dangers of waiting too long to raise rates and potential damage if it became necessary to raise rates quickly. Yellen also stressed the importance of sticking to the Fed’s dual mandate – stable inflation and full employment. While generally positive in her outlook for the US economy, Yellen noted the high level of uncertainty that exists in today’s political environment. Earlier this month the FOMC opted to ‘maintain the target range for the federal funds rate at 0.5% to 0.75% percent [and keep] the stance of monetary policy accommodative.’

by Emily Cross Leon | Feb 1, 2017 | Definitions

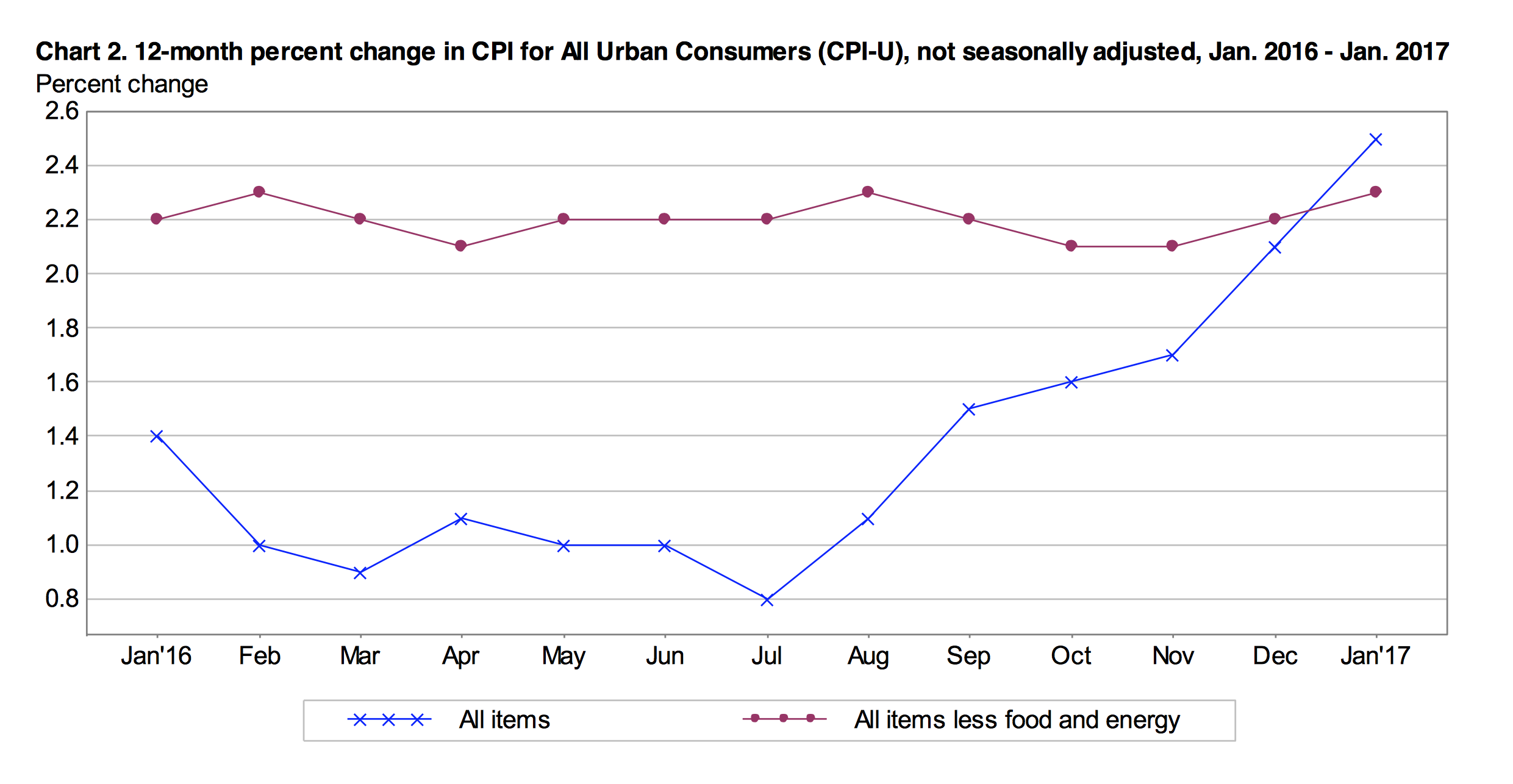

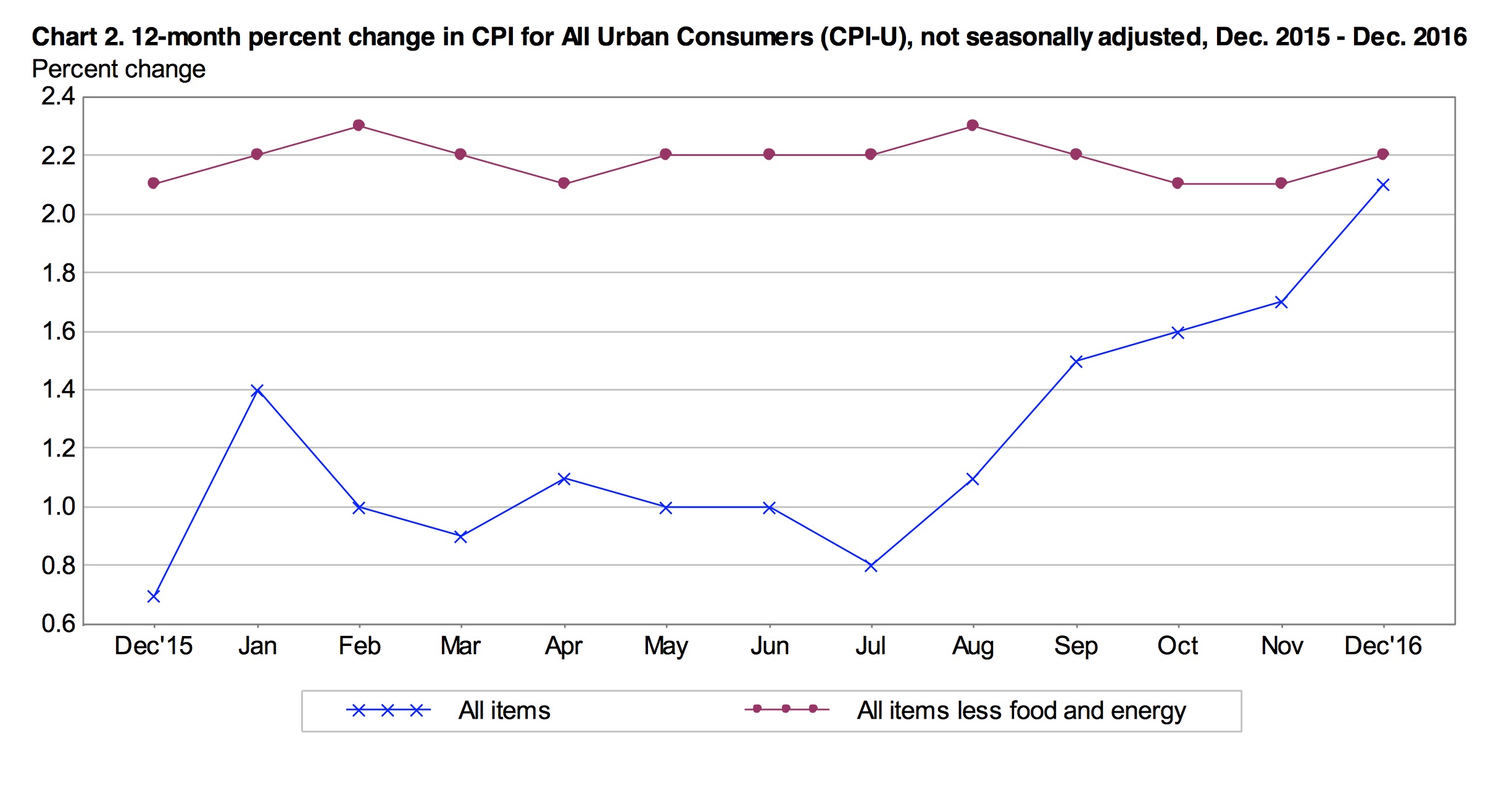

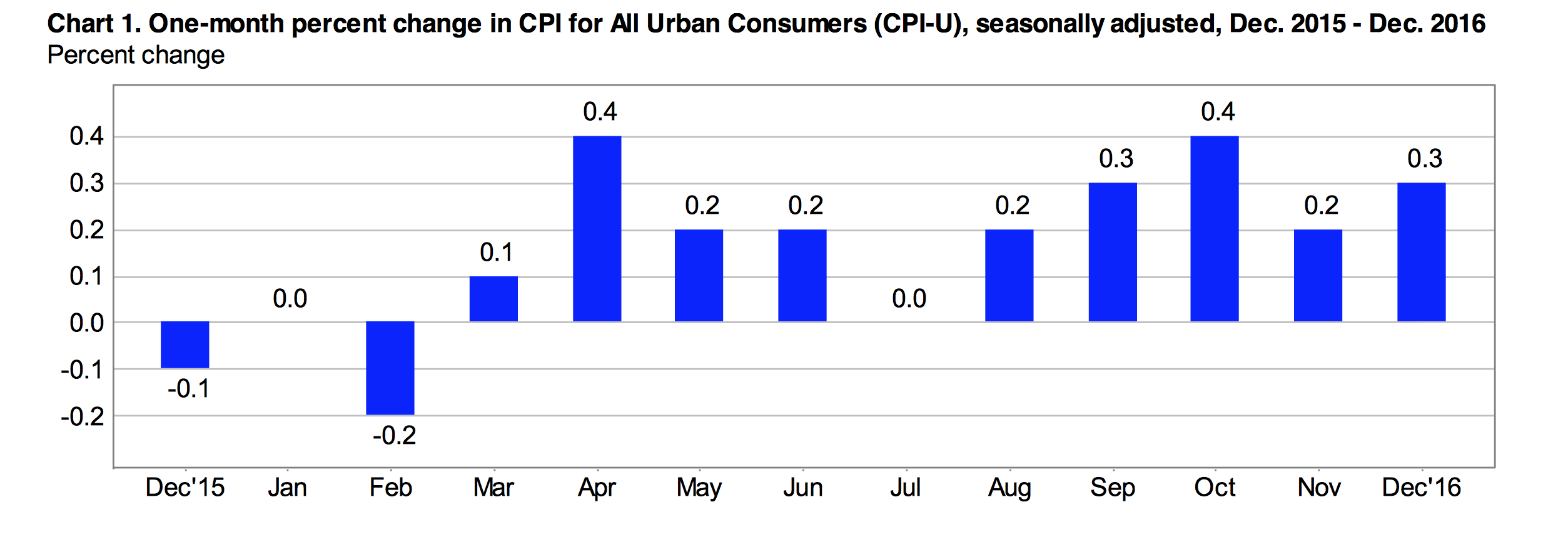

Inflation climbed above the Fed’s 2.0% target rate to round out 2016 with the highest year-over-year rate since June 2014. December’s inflation report from the Bureau of Labor Statistics did not surprise markets, that expected the data to reflect growing strength in the economy. Headline inflation, as measured by the consumer price index for all urban consumers (CPI-U), was up 2.1% year-over-year in December, the highest annual (December to December) rate in five years and significantly above the 10-year average of 1.8%.

Annual inflation spiked from 1.7% in November and has been accelerating since July. The all items index also continued to move closer to the core index as food and energy prices move in opposite directions. The core index (all items less food and energy), which is designed to be less volatile, was up 2.2% in December.

The CPI-U was unchanged on a monthly basis in December, after dropping 0.2% in November. However, with seasonal adjustments, consumer prices were up for the fifth consecutive month, adding 0.3% in December and 0.2% in November. Core inflation was up a seasonally adjusted 0.2% in December.

December Inflation Breakdown

Seasonally adjusted food prices were flat in December. Prices at the grocery store fell 0.2% while the cost of food away from home increased 0.2%. The index for meats, poultry, fish and eggs declined by 0.8%, while dairy and related products posted a 0.5% price increase for the month. On a seasonally adjusted basis, the food index has been flat since July and the index for food at home has declined for 8 consecutive months. The chart below shows the seasonally adjusted rates of inflation within the food index for December.

Energy prices were up a seasonally adjusted 1.5% in December, largely because of a 3.0% spike in prices at the pump, measured by the gasoline index. The price of fuel oil also jumped 0.6%. Excluding food and energy, the all items index was up a monthly 0.2% to match the rate in November. Within this core index, the price of used cars and trucks added 0.5% and the index for transportation services grew by 0.6%. The price of shelter continued its steady climb, adding 0.3% month-over-month. Medical care prices also inched up with medical care service costs increasing 0.1% and medical care commodity prices up 0.4%. Balancing some of this growth, the price of apparel reportedly dropped 0.7% in December following a 0.5% decline in November.

Annual Inflation

Over the year, the price of food slipped 0.2% as prices at the grocery store continued t0 decline. The index measuring the price of food at home fell 2.0% in 2016 with prices at the grocery store were down in all six major categories. The index for fruits and vegetables declined 2.4% year-over-year in December. At the same time, the index for meat, poultry fish and eggs dropped 5.4% and dairy prices were down 1.3%. The index for food away from home moved in the opposite direction, up 2.3% year-over-year. The net result was a marginal decline in the food index as food at home accounts for a larger share of the food index compared to food away from home.

After falling in 2014 and 2015, the energy index spiked 5.4% in 2016 including a 9.1% increase in prices at the pump. The price of fuel oil increased 12.7% in 2016. Electricity bills posted a 0.7% increase over the relevent year, while piped gas utility service costs were up 7.8%.

Excluding food and energy, core inflation was a healthy 2.2% in 2016, marginally higher than 2015’s core rate of 2.1%. Core inflation was led by growing shelter prices, up 3.6% year-over-year as rent prices climbed 4.0%. Medical costs also contributed to higher overall prices for the year, up 4.1%, largely the result of a 6.2% jump in prescription drug costs.

Market Outlook

December’s inflation report potentially points to the end of a long period of slow inflation and hesitation about raising interest rates. Although there is an unprecedented amount of uncertainty in the markets, the economy appears to be strengthening. Inflation has been the missing piece in the Fed’s criteria to raise rates, which have remained stubbornly low for roughly four years.

After raising the benchmark overnight interest rate by 0.25% to a range of 0.50% to 0.75% in November, the Federal reserve expects they will need three rate hikes in 2017 to keep the economy from overheating. If inflation continues to accelerate, the fed will likely be raising rates more than anticipated this year.

by Emily Cross Leon | Dec 15, 2016 | Definitions

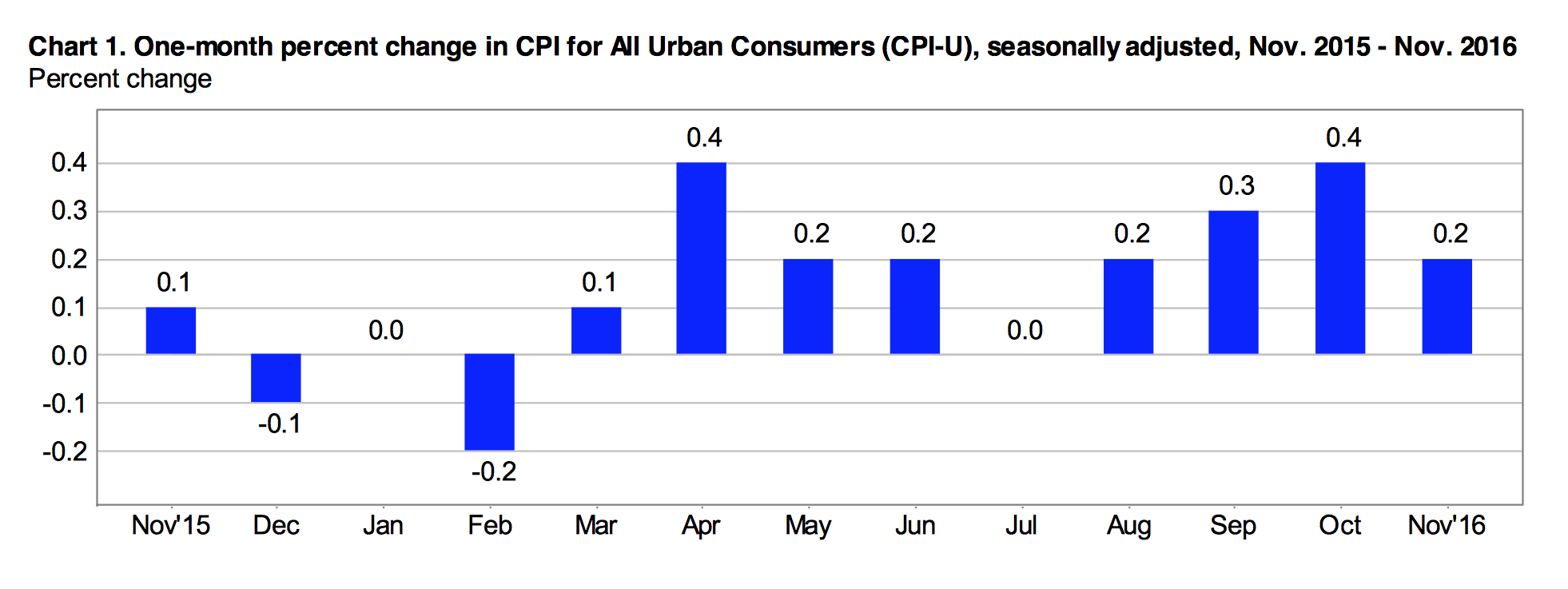

This morning the Bureau of Labor Statistics released consumer price data for November that was marginally ahead of expectations. For the year, prices measured by the Consumer Price Index for All Urban Consumers (CPI-U) climbed 1.7%, compared to an anticipated 1.6%. This is good news for the US economy as inflation has remained stubbornly low while jobs and other economic indicators have been more positive. Today’s report comes in the shadow of yesterday’s much anticipated FOMC decision to tighten monetary policy by raising rates by 0.25%.

The 0.2% decline in prices in November reflects a seasonal phenomena, which when corrected for, yields a 0.2% increase in the all items index. In October, seasonally adjusted prices climbed 0.4%. Core inflation, which excludes food and energy, was flat in November but after seasonal adjustments, rose 0.2%, compared to 0.1% in October. Over the relevant year, the core index climbed a healthy 2.1%.

Monthly Inflation

The 0.2% seasonally adjusted increase in the all items index in November can be largely attributed to a 1.2% jump in the energy index. The price of gas rose 2.7% in November on a seasonally adjusted basis. Prior to adjustments, prices were down 2.4% at the pump. Energy service prices fell 1% year-over-year, while energy commodity prices were 2.5% higher.

Food prices (seasonally adjusted) were flat for the month including a 0.1% dip in prices at the grocery store, adding to a streak of declines over the previous six months. The cost of meat declined 0.1% in November, following a 0.7% decline in October. Also significant, a 1.1% decline in the price of milk in November after falling a 0.9% in October. The price of fruits and vegetables slipped 0.2% in November canceling out an equal gain in October. Meanwhile, the index for food away from home inched up 0.1% in November.

Shelter, which accounts for 33.5% of the all items indexed, was 0.4% more expensive in November as rent prices grew 0.3% and the index for owners equivalent of rent was up 0.4%. Medical care commodities added 0.6% on a seasonally adjusted basis in November and the price of medical care services reportedly added 0.3 to match October’s growth. The index for airline fares slid a notable 1.3% in November after also diving 2.2% in October.

Annual Inflation

The core index, up 2.1% for the year ending in November was greatly impacted by increasing rental prices. The shelter index posted 3.6% annual growth, with the subindex for rent of primary residence growing 3.9% year-over-year (the shelter index accounts for over 42% of the core index). Medical care costs also climbed through the year as the index for medical care commodities added 4.3% and the indexed for medical care services was up 3.9%. The most significant change was in the price of hospital services, up 4.3% annually.

The transportation services index reportedly added 2.5% for the year. Within this index, motor vehicle insurance prices were 6.7% higher while Airline fares declined 6.6%.

Weighting on annual inflation numbers, the price of food fell 0.4% over the relevant year. At the grocery store prices were down 2.2% and lower in every component of grocery store spending. The most significant decline was posted by the index for meat, poultry, fish and eggs, down an annual 6% in November.

The energy index increased 1.1% over the 12-months ending in November, including higher costs for both energy commodities and energy services, up 0.8% and 1.5% respectively. At the pump, consumers paid 1% more for gas in November compared to November of 2015.

Regional Inflation

Monthly inflation was strongest in the Northeast where prices remained flat prior to seasonal adjustments compared to a 0.2% decline for the country as a whole. Prices were most sluggish in the Midwest, down 0.3% for the month. Also, inflation was most robust in larger cities, those with populations over 1.5 million posted a net monthly decline of only 0.1%.

On an annual basis, inflation was also highest in bigger cities. In Western urban areas the all items index climbed 2.3% compared to a national average of 1.7%. Prices growth was slower in the Midwest and the South, up only 1.2% and 1.6% annually.

Economic Outlook

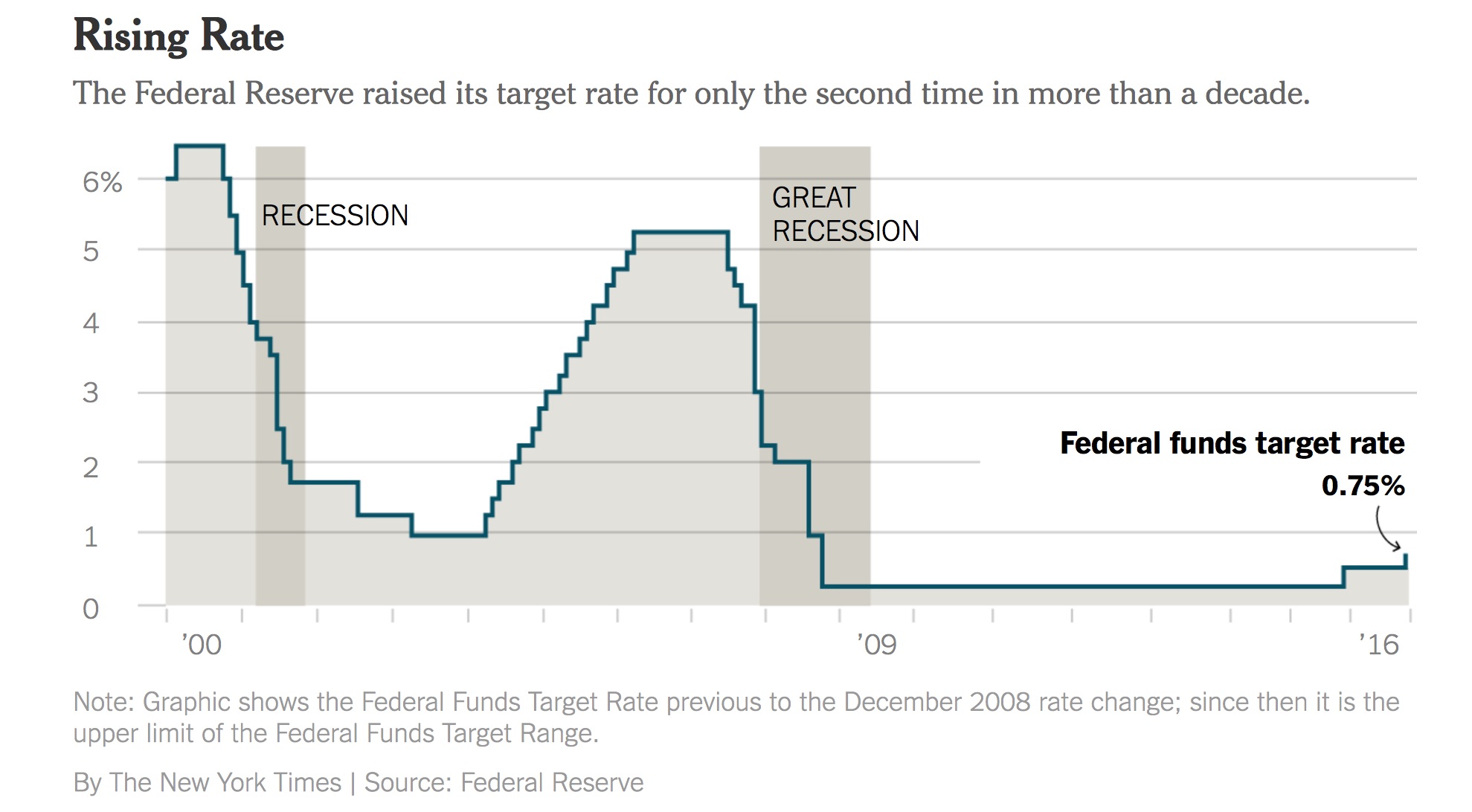

On Wednesday, the Federal Reserve upped its benchmark interest rate by 0.25% to 0.5%-0.75%, recognizing the “considerable progress” the economy has made in terms of job growth and price stability. The Fed voted unanimously to raise rates, marking the second hike since the financial crisis of 2008.

Expectations are for continued economic growth and for inflation rise t0 2% over the next couple of years – which is their target rate. Although, the cloud of uncertainty that surrounds the political environment and the potential for large policy shifts in the near future make the path of interest rates and the direction of the economy highly unpredictable. As of Wednesday, the fed anticipates three rate hikes in 2017.