by Andrew | Jun 18, 2015 | Definitions

May CPI numbers released by the BLS came broadly in line with expectations, with headline inflation posting an increase of 0.4% versus expectations of 0.5%. The core measure, excluding food and energy, rose 0.1% versus consensus estimates of 0.2%.

Rebounding gasoline prices were the biggest contributor to rising prices, with the gasoline index rising 10.4%. Other energy costs were mixed, and medical related costs continued to rise with the medical care commodities index rising 0.4% and the medical care services index rising 0.2%. The CPI data comes on the heels of yesterdays rate decision by the FOMC, and today’s data breathes no new significant life into our argument for rates to continue to remain fixed for the foreseeable future.

Key Highlights from the June FOMC Statement

Yesterday’s rate hike decision was a relatively tame event marketwise, although revisions in some key projections were enough to spur a moderate bout of USD weakness across the board. Delving into the statement, the Fed painted an improving economic picture, noting overall improvements since the first quarter of this year. Signs of improvement in the labor market were given particular mention.

On potential signs of growing unease with the relative strength of the US Dollar versus its peers, the Fed once again reiterated sluggish growth in US exports. While no special mention of the dollar was included in this month’s statement, currency targeting is likely to feature much more on the market’s radar going forward.

Current Conditions In the Fed’s own words:

“Information received since the Federal Open Market Committee met in April suggests that economic activity has been expanding moderately after having changed little during the first quarter. The pace of job gains picked up while the unemployment rate remained steady. On balance, a range of labor market indicators suggests that underutilization of labor resources diminished somewhat. Growth in household spending has been moderate and the housing sector has shown some improvement; however, business fixed investment and net exports stayed soft.”

With regards to inflation, the Fed reiterated its forecast for inflation to normalize towards its 2% target on the back of stabilizing energy prices and tightening labor markets in general.

“Inflation is anticipated to remain near its recent low level in the near term, but the Committee expects inflation to rise gradually toward 2 percent over the medium term as the labor market improves further and the transitory effects of earlier declines in energy and import prices dissipate.”

GDP Projections Downgraded, Unemployment Forecasts Rise

Somewhat surprisingly given the Fed’s upbeat language in its written statements from the June meeting, are the negative forecast revisions for both GDP and unemployment going forward. GDP projections were but from 2.3%-2.7% to 1.8%-2.0% – a fairly sizeable downgrade, and perhaps a growing reflection of the real headwinds facing the economy at present. Continued stress in the energy sector, which has seen sustained layoffs in the first half of this year, is showing signs of of having a wider impact on the economy at large. The Fed’s projections reflect this new reality, with unemployment forecasts for 2015 raised from 5.0%-5.2% to 5.2%-5.3%.

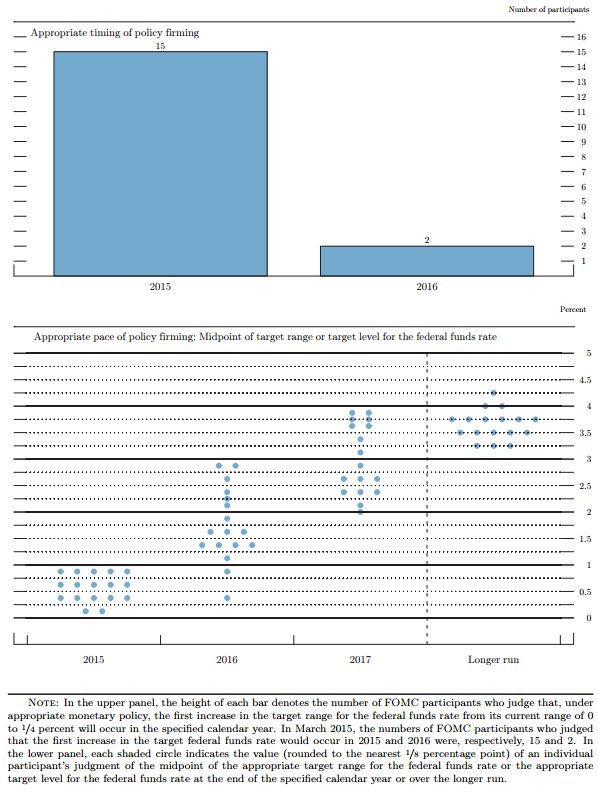

FOMC Members increase dovish stance

Revisions in the Fed’s quantitative forecasts were also backed up by a softening stance in the “dot” surveys of where each member expects the Fed Funds rate to be over the next two years. While the survey is conclusive that FOMC members expect a rate hike at some point this year, the magnitude of the rise is less clear. The overall drop from 1.875% to 1.625% in expectations for the Fed Funds rate in 2016 in many ways highlights the dwindling conviction affecting many FOMC members with regards to the extent of the “upcoming” rate hikes.

In summary, inflation is starting to show signs of stabilizing, with the deflationary month on month trends eradicated for the time being. While not evident in this month’s release, increased input costs on the producer front are likely to stoke higher inflation going forward. Medical inflation is an increasingly worrying trend, and is likely to hurt average Americans in a big way in the near future.

by Andrew | May 22, 2015 | Definitions

CPI for April came in broadly inline with market expectations with core inflation (ex Food and Energy) rising +0.3% MoM vs expectations of +0.2%. Broader CPI rose +0.1% bang inline with market forecasts. Annualized figures show a persistent deflationary trend, declining -0.2% YoY inline with analyst forecasts. Weekly earnings may well draw the Fed’s attention, with the data showing significant signs of improvement rising +2.3%. Combined with the positive jobs numbers of late, the employment situation does seem to be gathering steam.

Energy prices declined across the board, falling -1.3% MoM and -19.4% YoY. Gasoline fell -1.7% and Fuel Oil posted a decline of -8.4% MoM.

In a worrying continuation of last month’s data, medical prices surged +0.7% MoM and was the highest contributor to the Core inflation figure.

The slightly than higher Core CPI numbers are causing a sharp spike in the Dollar Index post announcement, however the relatively benign number combined with the slowdown in nearly all major economic indicators over the past month are likely to reduce the possibility of any potential rate hike at the Fed’s upcoming June policy meeting. Markets are awaiting Fed chief Yellen’s commentary later today for any revised signal in rate expectations.

Economic Indicators have been weak across the board

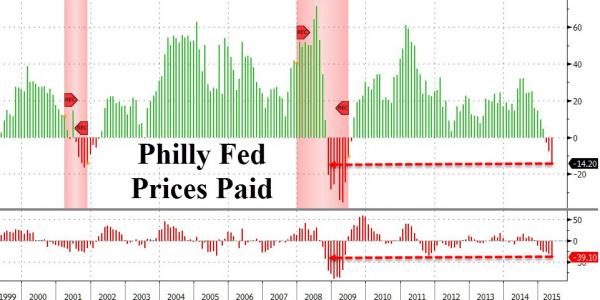

Philly Fed

Recent data from the Philly Fed indicate a slowdown in the manufacturing sector with the index posting further declines in May, posting a 6.7 print versus 8.0 consensus estimates. Despite a brief bounce in April, the index has now missed expectations for 7 out of the past 9 months and is growing reflection of the malaise starting to creep into the real economy. Prices paid for new orders plunged at an alarming pace, with declines also present in the average workweek.

PMI

The Markit US Manufacturing PMI survey released earlier this week reinforces the evidence of further weakness creeping into the manufacturing sector. May PMI data slowed to 53.8 versus expectations of 54.5, and extends the weakness of the April data which registered the biggest miss of expectations on record. Manufacturing PMI is now at it lowest level in over a year when the US was gripped in the middle of severe winter weather. PMI weakness is a growing trend across the world, with European, and Chinese surveys all pointing in a similar direction.

The strong dollar has been attributed with causing most of the headwinds for the manufacturing sector and is likely to be a concern for policy makers going forward. Declining export sales highlight further problems with the strong dollar, with US data falling for the past two consecutive months. April also saw the first rise in input costs for 2015, as the rebounding crude oil price began creeping into production costs.

Given the impact the stronger dollar is having on the broader economy, the Fed is likely to adopt a cautious approach going forward, and will likely increase commentary around the impact the relative strength of the currency is having going forward. Rate hikes in the near future would likely exacerbate problems in the export and manufacturing sector, and the Fed will be keeping this in mind at the June policy meeting.

FOMC Minutes paint a mixed picture for rate hikes going forward

The minutes from the last policy meeting released earlier this week reflected growing concern about current bond market volatility, and over extended valuations in the stock market. Examining the minutes in detail reveals a more proactive stance by the Fed in trying to jawbone the equity markets onto a more sustainable path without having to use the threat of an actual rate hike.

Some of the more noteworthy commentary includes:

In their discussion of financial market developments and financial stability issues, policymakers highlighted possible risks related to the low level of term premiums. Some participants noted the possibility that, at the time when the Committee decides to begin policy firming, term premiums could rise sharply—in a manner similar to the increase observed in the spring and summer of 2013—which might drive longer-term interest rates higher. In this connection, it was suggested that the tendency for bond prices to exhibit volatility may be greater than it had been in the past, in view of the increased role of high-frequency traders, decreased inventories of bonds held by broker-dealers, and elevated assets of bond funds.

A few anticipated that the information that would accrue by the time of the June meeting would likely indicate sufficient improvement in the economic outlook to lead the Committee to judge that its conditions for beginning policy firming had been met. Many participants, however, thought it unlikely that the data available in June would provide sufficient confirmation that the conditions for raising the target range for the federal funds rate had been satisfied, although they generally did not rule out this possibility. Participants discussed the merits of providing an explicit indication, in postmeeting statements released prior to the commencement of policy firming, that the target range for the federal funds rate would likely be raised in the near term. However, most participants felt that the timing of the first increase in the target range for the fed-eral funds rate would appropriately be determined on a meeting-by-meeting basis and would depend on the evo-ution of economic conditions and the outlook. In keeping with this data-dependent approach, some participants further suggested that the postmeeting statement’s description of the economic situation and outlook, and of progress toward the Committee’s goals, provided the appropriate means by which the Committee could help the public assess the likely timing of the initial increase in the target range for the federal funds rate.

On balance, April CPI has gone some way in postponing any imminent rate hike which could have some bearing on the USD in the coming days and weeks. Yellen’s commentary later today will prove crucial for market sentiment. We stay tuned.

by Andrew | May 5, 2015 | Definitions

Financial commentary and analysis is usually heavily peppered with “since Lehman” or “Post-Lehman” comparison statistics and conjecture. 2008 were some of the darkest days ever for financial markets; the losses worldwide were truly staggering and we are still wrestling with the consequences of this epic event to this day.

The world has changed a great deal since Lehman closed its doors – the financial world in particular has changed. The policy response from governments and monetary authorities around the world were amongst the most aggressive monetary policy moves of the modern era. As a result, we are now living in the midst of a giant financial experiment with all the theories, uncertainty, fear, greed and hope associated with finance jostling for equilibrium.

The Federal Reserve and other central banks throughout the world have been engaged in loose monetary policy, quantitative easing, ZIRP, and NIRP without issue despite the dire warnings of opponents who see the surge in the money supply as the precursor to rampant inflation and a hyperinflationary currency collapse. These fears for the most part have not transpired. Inflation has remained subdued through this period, and a lot of head scratching has ensued.

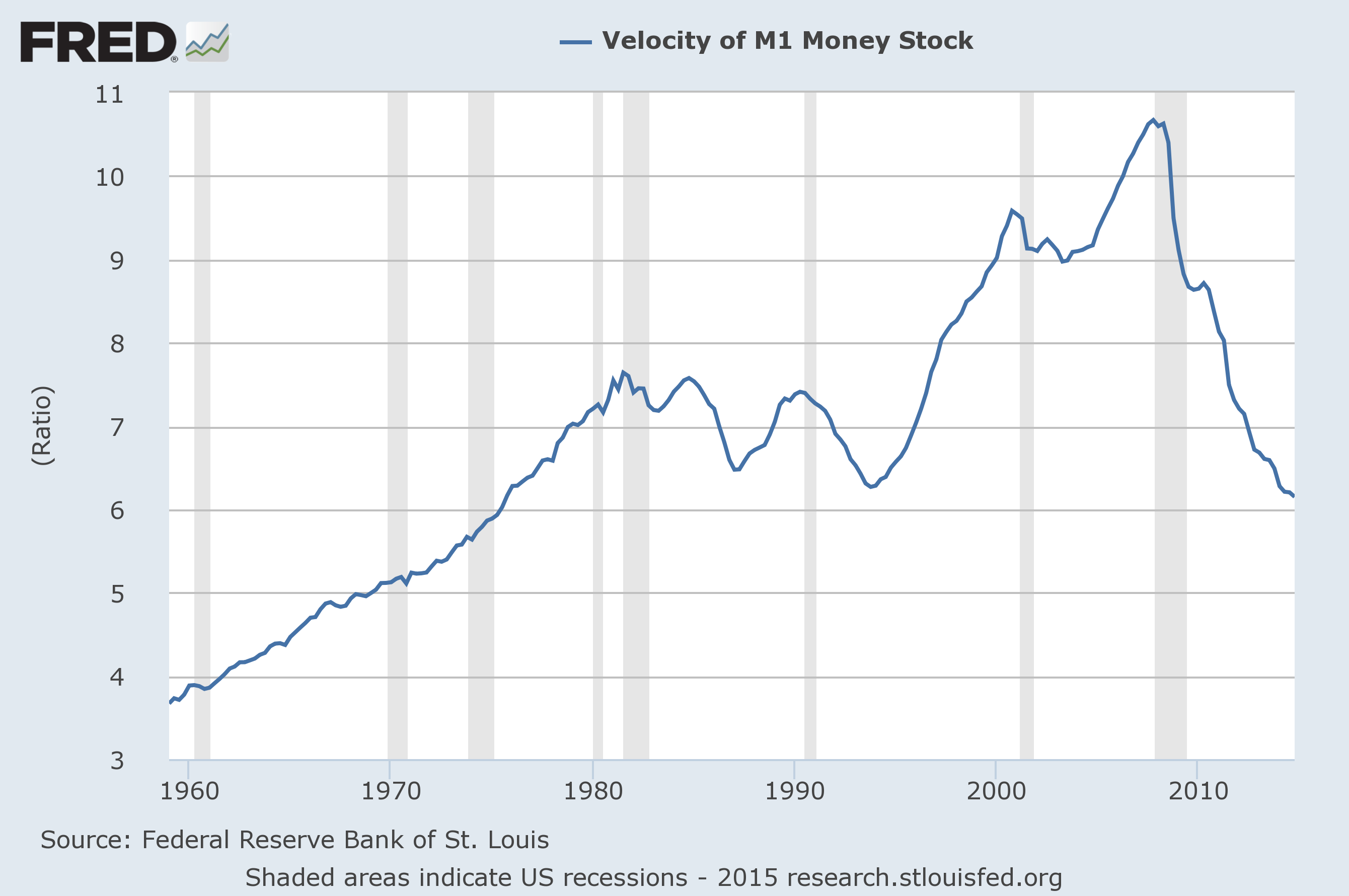

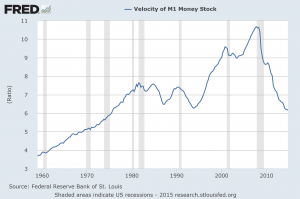

We are in uncharted territory, but there can be no argument about some of the major economic themes that have transpired “Post-Lehman” – the most astounding of which has been a complete collapse in the velocity of money throughout the economy. This metric above all others, helps explain why the expansionary monetary policy regimes throughout the world have managed to avoid triggering bouts of high inflation. The low velocity of money statistics also reveal just how fractured the economic recovery has been in the United States – where the exuberant valuation levels of financial markets are not borne out by developments in the real economy.

What is the velocity of money?

The velocity of money refers to how fast money circulates within the economy from one person to the next. Velocity of money is an important tool for gauging the rate at which money within the economy is used for purchasing goods and services. Analysts will often take the velocity of money as part of their consideration when determining how well the overall economy is performing. A high velocity of money indicates an active economy, and by consequence, is likely performing well. A low velocity of money will usually cause alarm bells to start ringing for economists. Low velocity of money is usually the precursor of slower growth and the onset of deflationary conditions.

Another element we need to take into consideration is the overall money supply of the economy. The money supply has many different measures, but economists usually narrow these down into two distinct measures known as M1 and M2.

The M1 definition refers to the most liquid assets in the economy, namely cash and checking deposits. M2 broadens the definition of the money supply by also including “near cash” assets such as savings deposits, time deposits, and other money market mutual funds which can be converted into cash relatively quickly.

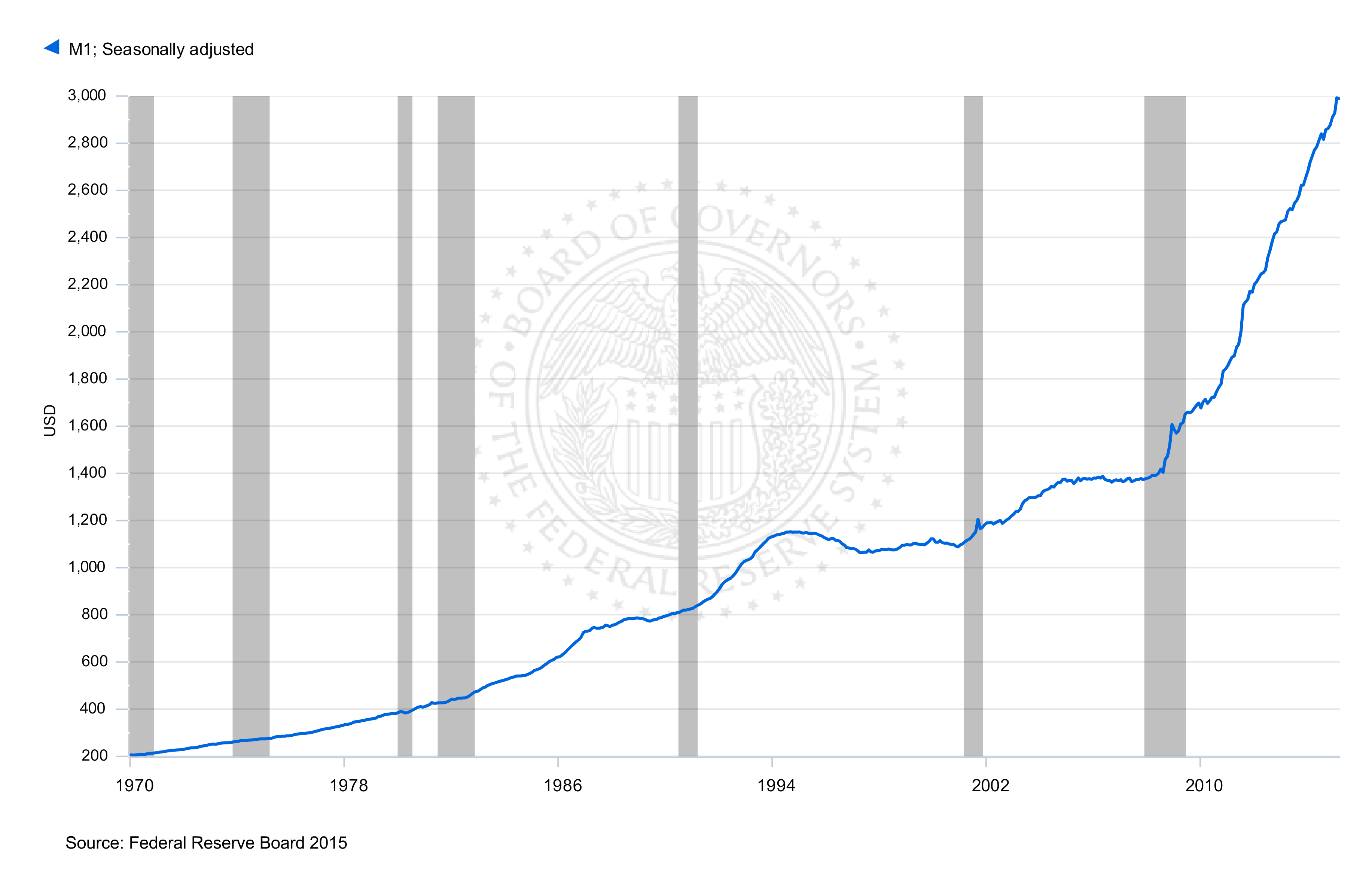

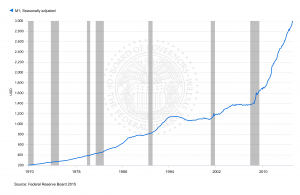

How much has money supply increased since the start of QE?

As a consequence of the Federal Reserve’s QE program, the money supply of the United States as measured by M1 has increased by over 100% since September 2008. Increasing the money supply on this scale has never occurred before – the exponential nature of the M1 chart illustrates this well.

Despite the dramatic increase in the overall money supply – we are still concerned about deflationary pressures within the economy. So what has been happening with all of this extra money? Banks for the large part, have been hoarding this cash as excess reserves within the system. The transmission mechanism through credit growth has been sluggish at best – and therefore the velocity of money has been crashing.

The Velocity of Money has been in freefall since 2008

The velocity of money has crashed “Post-Lehman” – the chart below shows by just how much! The implications of this are obvious. Money has been tied up in the financial sector – banks have been unwilling to lend to the “real sector” and the recovery has been going at a snail’s pace as a consequence. Financial markets by contrast, have been soaring with various markets around the word frequently taking out all time highs.

What happens next?

Looking forward from our current position is difficult. On one hand, the deflationary pressures weighing down the economy are still at large but the massive increase in the money supply has the potential to stoke serious inflationary pressures going forward. Central bank around the world have all squeezed the toothpaste tube and the contents are out. The next chapter in the “Post-Lehman” story will undoubtedly be dominated by how to get the money supply genie back into the bottle. Time will tell.

by Andrew | Apr 20, 2015 | Definitions

Official March inflation data from the BLS was a mixed bag with headline CPI continuing to remain under pressure, but a significant rise in Core CPI ex Food and Energy was enough to trigger knee jerk uncertainty about the outlook for the Fed’s immediate interest rate policy. A weak session across all markets following the release of the data suggests market participants are viewing the recent uptick in prices as a signal for rates to rise quicker than expected.

The Deflationary Camp

On one side, the deflationary environment shows no sign of easing up, with headline CPI coming in weaker than expected – consumer prices rose a modest 0.2% from February versus a consensus call for a 0.3% increase. CPI YoY fell to -0.1%, the third successive monthly decrease. Double digit falls in energy prices YoY continue to keep a lid on consumer prices for the time being with Energy (-18% YoY) and Gasoline in particular (-29% YoY). Food prices fell -0.2% for the first time in six month providing further relief to the consumer.

In a worrying sign for business activity and sentiment going forward, the index for airline fares declined for the fourth time in the last 5 months and there seems to be growing evidence of discounting taking place in the business travel segment across the board.

Core CPI Remains Stubbornly High

On the flip side, Core CPI excluding Food and Energy continues to print at elevated levels, rising to 1.8% YoY versus consensus expectations of 1.7% YoY. Increased Housing (+0.3% MoM, 3% YoY) and Health Care costs (0.4% MoM, 1.9% YoY) were the main contributors. The recent stability in Crude and Energy prices could see Core CPI remain on the high side for the next few months and the market is likely to start paying more attention to energy prices going forward to try and gauge potential sentiment within the Fed.

Wages

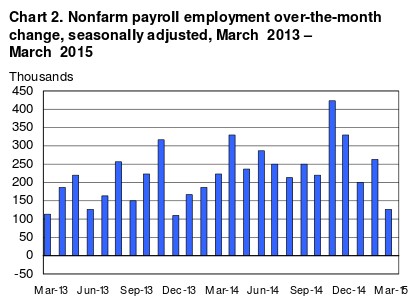

Real average hourly earnings for all employees increased 0.1 percent from February to March with 0.3-percent increase in average hourly earnings just shading the 0.2% increase in CPI. The NFP numbers for the past few months are likely to give the Fed further room to pause – NFP has been on the slide every month since December 2014, and with the potential for increased layoffs coming from the oil, gas, and shale sectors the unemployment numbers might show increasing stress in the coming months.

Market Reaction

Equity markets were a sea of red all day Friday, as a perfect storm of higher than expected Core CPI, increased volatility in China and wider Asian markets, and ongoing drama with Greece triggered a bout of selling from investors trying to reduce exposure going into the weekend.

Selected Market Performances

S&P500 -1.13%

DJIA -1.54%

WTI Crude -1.71%

EURUSD +0.43%

Outlook Going Forward

Rising Core CPI will be a concern for markets, but with increased volatility within China and Emerging Asia equity markets, and heightened geopolitical tensions it appears too early to assume any imminent rate hike from the Fed – if anything these pressures are likely to keep the Fed on hold for the time being in order to get more clarity on world events. Consumer prices continue to remain subdued and policy makers are likely to want to see a pick up on this side before jumping into action.

The dollar will continue to act as proxy for rates in the meantime, and we expect the currency to remain well bid against its major competitors for as long as the current standoff from the Fed continues to playout. The Gold market has been steady all month with the yellow metal hovering around the $1200 mark in fairly tight trading bands. With the ZIRP, and increasingly NIRP world in which we live, the Gold market might still have a role to play this year.

by Ryan Barnes | Mar 25, 2015 | CPI, Definitions, gold, Inflation

The U.S. economy got a little economic boost today with a stronger-than-expected CPI reading for February, and a strong Purchasing Manager’s Index (PMI) that continued to project GDP growth.

Headline CPI and core CPI both came in 0.2% higher than January, as slight price hikes at the pump for refined products balanced out a general breather in the declines in some of the base commodities. The headline numbers had been tracking negative for the past three months, which everyone was pretty much ok with chalking up to crude oil. Just so long as GDP growth came in respectably, there wasn’t any reason to panic.

But core CPI (ex-food and energy costs) was already lagging behind Fed goals of around 2%, and already in the midst of sending deflationary ripples up the global goods chain, into…well, just about everything.

Muddled Waters for First Rate Hike

It’s created a tense chess match between investors and the Fed the past few weeks. It started just after the stellar (as in +295,000) February jobs report last month, when the consensus started to form that the Fed would have to act sooner rather than later in creating a interest rate normalization cycle.

The key first step of that cycle is getting us off the floor of zero percent rates – a stance that doesn’t befit a growing economy and presents what Yellen herself has called an “asymmetrical risk”.

U.S. Definitely Growing…But How Much?

Just as soon as we seemed to have some headway into a summer rate increase, nearly every economic indicator in the U.S. started been printing well below analyst estimates. In fact, the depth of our misses has hit a multi-year high, according to Bloomberg analysis:

In light of this reversal, both investors and the Fed have had to take stock of things. First quarter GDP estimates continue to be ratcheted down – from the 2.5% – 3.0% level I highlighted last month (a number that was freshly lowered at the time) to an average Q1 GDP estimate of about 1.5% today.

Cranky Markets are Volatile Markets

It’s why we’ve seen a spike in volatility around every asset class – fixed income, forex, commodities, and equities have all been bumping around trying to align their compass to the next clear trend line. Would the Fed remove “patient” in the March FOMC meeting? Was September the new June (for the first rate hike)? Was 2015 off the table entirely?

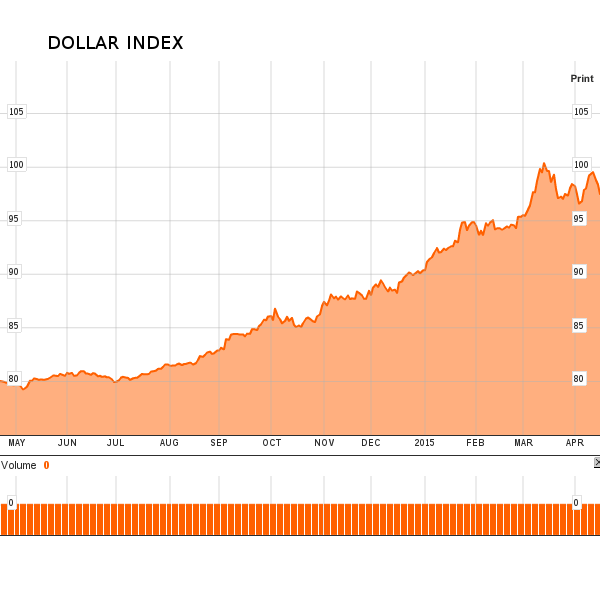

Answering these questions is challenging enough in isolation, but it’s been exacerbated by the stunning rise the the USD index, which alters true price action in commodities and long bonds. The surging U.S. dollar is a de facto rate hike. It lowers the cost of imports dramatically (a deflationary force), and it makes our exports more expensive overseas.

And while the realities of pricier U.S. exports certainly hurt some companies more than others, the simple fact is that close to 50% of the total revenues of the S&P 500 member companies is derived in a currency other than the U.S. dollar.

2014, Part Deux?

It’s quite astonishing how much the first quarter of this year is looking like the first quarter of last year. Tick by tick, indicator by indicator, we seem to be replicating that market environment.

This time last year we were watching interest rates hit new lows, but convinced the party had to end any moment – inflation was coming, and we needed to position ourselves away from fixed income and into equities, gold, and other commodities. Fixed income turned out to deliver stronger returns than even equities did.

GDP looked to be on track for a good start to the year, but then a bout of really bad whether caused us to actually contract as an economy in Q1. Most of the top analysts said “don’t worry, we’ll be strong in the back half of the year”, and sure enough we were. The U.S. turned in over 4.5% growth in the next two quarters.

Looking around today, it’s much the same setup – so far. The key differences between then and now are this:

1) the unemployment rate is lower than last year; we have clearly moved close enough to full unemployment in the Fed’s eyes that it’s no longer an impediment to a rate increase. That box is checked off.

2) the USD is much stronger (10-20% or more) against every major global currency. As I’ve discussed, this move alone is the equivalent of a 25-50 bps rate hike.

In fact, if the dollar hadn’t been zooming so hard the past six months, there’s a chance the Fed would’ve put a token 25bp hike out there last week. Instead, Yellen reminded us that the Fed isn’t there to make things easy for investors, saying the Fed “can’t provide and shouldn’t provide” certainly to markets when it comes to the timing of rate hikes.

We don’t seem to be in any danger of that.

by CPI | Nov 5, 2014 | Definitions

CPI stands for Consumer Price Index, and it is a measure of inflation. It is calculated by measuring the change in a specific group of goods and services over time. The CPI is calculated by the US Bureau of Labor Statistics.

CPI stands for Consumer Price Index, and it is a measure of inflation. It is calculated by measuring the change in a specific group of goods and services over time. The CPI is calculated by the US Bureau of Labor Statistics.

What the CPI Measures

The CPI measures the spending habits for two different groups. The CPI-U measures the spending patterns of all urban consumers. The CPI-W measures the spending patterns of urban wage earners and clerical workers. The spending patterns of people living in rural areas, farmers, members of the armed forces and those institutionalized in prisons or hospitals are not measured. The group of all urban consumers represents about 87 percent of the entire population of the United States. The people who comprise the CPI-W are a subset of the CPI-U.

What the CPI Includes

The CPI includes eight major groups of expenditures. They are:

- apparel, which includes clothing and accessories like jewelry;

- education and communication, which includes school tuition, telephone and internet services, and computer software and accessories;

- food and beverages, which consists of grocery items as well as dining out;

- housing, which includes rent or mortgage payments, utilities and furnishings;

- medical care, including prescriptions, hospital services, doctor’s services, and dental and vision products and services;

- recreation, including admission to spectator sporting events, toys, pets, and sports equipment;

- transportation, comprised of vehicle leases and purchases, gas, insurance, and airplane and train fares; and

- other goods and services, such as personal services like hairdressing, funeral expenses, and tobacco and smoking products.

Taxes on items purchased and excise taxes are included in CPI, as are user taxes like tolls. Income taxes are not included. Investments and savings vehicles are not included.

How the CPI Data is Published

The CPI data is published nationally and by region every month. The regions are the Northeast, Midwest, South and West. The data is also published by metropolitan area. The Chicago, Los Angeles and New York data are published every month. Data for the other 11 metropolitan areas are published every other month. These areas are Atlanta, Boston, Cleveland, Dallas, Detroit, Houston, Miami, Philadelphia, San Francisco, Seattle and Washington DC.

How the CPI is Used

The CPI is used to measure inflation. It is used by government agencies and entities to measure the effectiveness of fiscal and monetary policy, and to determine when that policy needs to be adjusted. It is used by government, private industry, labor unions and individuals to determine how effective current economic policy is.

The CPI is used to determine purchasing power. When you hear the terms ‘in today’s dollars,’ or ‘adjusted for inflation,’ the values discussed have been adjusted by using the CPI in order to reflect true purchasing power, or the amount a dollar will buy, at different times in history.

The CPI is used to adjust Social Security and other income payments, and to adjust the level of income required for eligibility for government programs. Retirees, whether they collect Social Security or a military or civil service pension, recipients of food stamps, and children who receive free or reduced price school lunches are all affected by changes in the CPI.

The Difference Between CPI and a Cost-of-Living Index

The CPI is often referred to as a cost-of-living index, but there is a difference. The CPI reflects what consumers are actually buying, while a cost of living index reflects the amount of income necessary to maintain a certain standard of living.

When consumers have less income, they tend to substitute less expensive versions of the same item in their budgets. Since the CPI reflects the cost of what they actually buy, this measure may drop when substitutions are made. A cost of living index, on the other hand, would reflect the cost of a certain item over time, which will almost always go up.