by Amine Rahal | May 3, 2025 | Debt Relief

Is Freedom Debt Relief Legit? Here’s an honest look at one of America’s largest debt settlement companies. This review follows reviews we have done of other similar companies such as New Era Debt, Family Credit Management, Cura Debt and Turbo Debt. Ultimately, all these debt relief companies offer similar services, so we recommend that you shop around and check the rates you get from different companies. Don’t just pick the first one.

Overview of the Company

Freedom Debt Relief (FDR) is one of the most established debt settlement firms in the U.S., helping clients resolve over $15 billion in debt since 2002. Headquartered in San Mateo, CA, it serves clients nationwide (excluding a few states) and focuses on unsecured debt such as credit card balances and medical bills.

- Founded: 2002

- Headquarters: San Mateo, CA

- Website: www.freedomdebtrelief.com

- Minimum Debt: $10,000

- Fees: 15%–25% of enrolled debt

- Accreditations: AADR, IAPDA, BBB A+

Key Services Offered

- Free debt consultation

- Custom settlement plans

- Creditor negotiation

- Online dashboard

- Dedicated support team

Pros & Cons

| Pros |

Cons |

| ✅ One of the most experienced firms |

❌ Credit score may drop during program |

| ✅ No upfront fees |

❌ Not available in every state |

| ✅ Strong client support & dashboard |

❌ May receive frequent sales calls |

| ✅ Accredited by major associations |

❌ Not suitable for secured or tax debt |

Ratings & Reviews Summary

| Source |

Rating |

Highlights |

| BBB |

A+ / 4.47★ |

Strong transparency record |

| TrustPilot |

4.6★ (42,000+) |

Customer service and results praised |

| Google Reviews |

4.7★ |

Generally positive, some delays noted |

Please check the most current ratings from these review sites as they may have changed since we wrote this review.

How It Works

- Start with a free consultation

- Enroll in a custom settlement plan

- Deposit monthly into a secure account

- FDR negotiates with creditors on your behalf

- You approve and pay reduced settlements

- Graduate after debts are resolved (24–48 months)

Is It Right for You?

Great for:

- Anyone with $10k+ in unsecured debt

- People seeking a big, reputable brand

- Those needing hands-on guidance and a support team

Not ideal for:

- Consumers with secured debt or IRS tax issues

- People living in restricted states

- Anyone seeking a DIY or consolidation loan approach

💬 Frequently Asked Questions About Freedom Debt Relief

1. What does Freedom Debt Relief do?

Freedom Debt Relief helps consumers settle unsecured debts—primarily credit card balances—by negotiating directly with creditors to reduce the total amount owed. They create customized programs based on your debt, income, and hardship.

2. Is Freedom Debt Relief legit?

Yes. Freedom Debt Relief has been operating since 2002 and is accredited by the American Association for Debt Resolution (AADR) and certified by the International Association of Professional Debt Arbitrators (IAPDA). They’ve helped over 850,000 people resolve more than $15 billion in debt.

3. What kind of debt can Freedom help with?

They handle unsecured debts, including:

They do NOT work with:

-

Mortgages

-

Auto loans

-

IRS tax debt

-

Federal student loans

4. What is the minimum debt required?

You typically need at least $7,500–$10,000 in unsecured debt to qualify for their program.

5. How does the debt settlement process work?

-

You stop paying your creditors.

-

You deposit funds monthly into a dedicated settlement account.

-

Freedom negotiates with your creditors after enough funds accumulate.

-

They settle the debt for less than what you owe.

-

You approve the settlement before payment is released.

The process usually takes 24–48 months depending on your ability to save.

6. How much can I save with Freedom Debt Relief?

On average, clients who complete the program reduce their enrolled debt by 45–60% before fees. After fees, net savings may be 20–30% depending on your specific case.

7. What fees does Freedom charge?

Freedom charges 15% to 25% of the enrolled debt amount, but only after a successful settlement is reached. No upfront fees are charged (in compliance with FTC rules).

8. Will this hurt my credit score?

Yes, debt settlement typically causes a temporary drop in your credit score because you stop making payments to creditors. However, many clients see gradual recovery after completing the program and resolving debts.

9. Does Freedom Debt Relief guarantee success?

No. Results vary by client. Some creditors may not agree to settle, and you must remain consistent with your monthly deposits. However, Freedom has thousands of successful settlements documented.

10. Can I cancel the program if I change my mind?

Yes. You are not locked in. You can cancel at any time without penalty. However, if you cancel after a debt has already been settled, you will still owe the associated settlement fee.

11. Is this service available in all 50 states?

No. Freedom is currently available in 40+ U.S. states. They do not operate in:

12. What happens to interest and late fees during the program?

While enrolled, creditors may still charge interest and late fees until a settlement is reached. These costs are factored into settlement negotiations.

13. Is the forgiven debt taxable?

Yes, in most cases the IRS considers forgiven debt taxable income. Freedom recommends speaking with a tax advisor to understand your obligations.

14. What happens if I miss a monthly payment?

Missing payments can delay settlements or cause your account to be removed from the program. Consistency is critical to success.

15. Can I still use my credit cards during the program?

No. You must stop using credit cards that are enrolled in the program. Using them can jeopardize your eligibility.

16. Will I receive collection calls?

Yes. Because you’re not paying creditors directly, you may receive calls or notices. However, Freedom provides advice and support to help manage communications.

17. Can Freedom Debt Relief stop lawsuits or wage garnishment?

No, not directly. Debt settlement may reduce the chance of being sued, but it doesn’t guarantee protection. If you’re facing legal action, consult an attorney.

18. Who should avoid debt settlement?

You should probably avoid debt settlement if:

-

You’re not behind on payments

-

You can pay off your debt in under 2 years with budgeting

-

You need to protect your credit score at all costs

-

You primarily have secured debt (mortgage, auto loans)

Final Verdict

Freedom Debt Relief is a trusted, experienced player in the debt relief industry. With no upfront fees, a solid negotiation team, and thousands of satisfied clients, it’s a solid option for those struggling with unsecured debt. While it may not be the most boutique or personal solution, it’s certainly one of the most proven.

Check Eligibility at FreedomDebtRelief.com

![ClearOne Advantage – We Review This Debt Relief Company [2025]](https://cpiinflationcalculator.com/wp-content/uploads/2025/02/clearonehomepagescreen.jpg)

by Amine Rahal | May 2, 2025 | Debt Relief

Seeking debt relief and wondering whether ClearOne Advantage is a good choice? Look no further. In this article, we’ll review the company, its debt relief services, its reviews and ratings and we’ll break down their services and costs as well when it comes to debt settlement, debt consolidation, credit counselling and other similar services they may offer.

#1 Rated Debt Relief Company in 2025?

Are you looking for the #1 Rated Debt Relief & Settlement Company in 2025? See our New Era Debt review. New Era Debt has received the highest number of positive reviews amongst all the 20 companies we researched.

> Check if you qualify

> Visit Website

|

What is ClearOne Advantage?

ClearOne Advantage is an American debt relief company specializing in debt settlement services. Founded in 2008 and headquartered in Baltimore, Maryland, ClearOne Advantage has helped thousands of clients reduce their unsecured debts through negotiation with creditors. The company offers customized debt relief programs designed to help individuals regain financial stability without resorting to bankruptcy.

- Headquarters: Baltimore, Maryland

- States Covered: Available in most U.S. states (check their website for state-specific availability)

- Founded in: 2008

- Website: www.clearoneadvantage.com

- Phone: 1-888-340-4697

👍 Pros of ClearOne Advantage

- No upfront fees – you basically pay only when debts are settled

- Free consultation with customized relief plan

- Online portal to track progress 24/7

- Highly rated across BBB, Google, Trustpilot

- Member of AADR and IAPDA certified

- Dedicated customer support team

👎Cons of ClearOne Advantage

- Only available in select U.S. states

- May negatively impact your credit score short-term

- Does not assist with secured debt (e.g. mortgages, car loans) like many other debt settlement companies.

- No services for IRS/tax debt (CuraDebt may be better for tax debt.)

- Not all creditors may agree to settlements

ClearOne Advantage Application Process

- Free Consultation: Speak with a debt specialist to evaluate your situation

- Enrollment: If you qualify, you’ll be enrolled in a tailored debt settlement plan

- Build Savings: Start making monthly deposits into your settlement account

- Negotiation Phase: ClearOne negotiates with creditors to reduce total debt

- Debt Settlement: Pay reduced balances as settlements are reached

- Graduation: Once all debts are settled, you complete the program

This process typically spans 24 to 48 months, depending on your balance and savings rate.

Services Offered by ClearOne

- Free Debt Analysis

- Debt Settlement & Negotiation

- Customized Debt Reduction Plans

- Financial Education & Budgeting Support

- Upfront Fees (Performance-Based Fees)

- Dedicated Client Portal for Account Management

Minimum Requirements:

- Minimum Debt: $10,000 in unsecured debt

- Income Minimum: No strict requirement, but must demonstrate the ability to make monthly program payments

Who Should Consider ClearOne Advantage?

ClearOne Advantage is best suited for:

- Individuals with $10,000 or more in unsecured debt such as credit cards and some loans.

- Those struggling to make minimum payments

- People seeking an alternative to bankruptcy

- Clients looking for hands-on guidance and a modern digital experience

- Consumers in qualifying U.S. states with moderate to strong income

ClearOne may not be ideal for:

- Consumers with secured debt like mortgages or auto loans

- Individuals needing tax debt or federal student loan help

- Those unwilling to take a short-term hit to their credit score

ClearOne Advantage Ratings & Reviews:

ClearOne Advantage has built a strong reputation for its transparency, customer service, and ability to help clients settle their debts. Here’s how they are rated across major platforms:

- BBB Rating: A+ (Accredited Business)

- BBB Reviews: 4.72/5 Stars (Over 1,500 Reviews)

- Trustpilot: 4.8/5 Stars (Over 3,000 Reviews)

- Google Reviews: 4.6/5 Stars

- Consumer Affairs: 4.7/5 Stars

- Investopedia Rating: 4.1/5 Stars

- Accreditations: Member of the American Association for Debt Resolution (AADR), Certified by the International Association of Professional Debt Arbitrators (IAPDA)

ClearOne Advantage VS Others

Here is a brief overview of how this company compares with other popular competitors in the debt settlement space…

| Company |

Avg. Rating |

Fees |

Min. Debt |

BBB Rating |

| ClearOne Advantage |

4.37 / 5 |

20% – 25% |

$10,000 |

A+ |

| New Era Debt Solutions |

4.9 / 5 |

14% – 23% |

$10,000 |

A+ |

| TurboDebt |

4.9 / 5 |

15% – 25% |

$10,000 |

A+ |

| Freedom Debt Relief |

4.59 / 5 |

15% – 25% |

$10,000 |

A+ |

| Pacific Debt Relief |

4.85 / 5 |

15% – 35% |

$10,000 |

A+ |

Key Features & Benefits:

1. Free Consultation & Customized Plan

ClearOne Advantage provides a free initial consultation to assess your financial situation and determine if you qualify for their debt relief program. Each plan is tailored to the client’s financial needs, ensuring a manageable path toward debt resolution.

2. No Upfront Fees

Unlike some competitors, ClearOne Advantage does not charge upfront fees. Instead, their fee structure is performance-based, meaning they only charge a percentage of the settled debt once a negotiation is successfully completed.

3. Debt Reduction Through Negotiation

The company negotiates with creditors to reduce the total amount owed. Many customers have reported savings of 40% to 60% on their original debt balances before fees.

4. Online Client Portal

ClearOne Advantage offers an online portal where clients can monitor their progress, track payments, and communicate with their dedicated support team.

5. Strong Customer Support

With a team of debt specialists available via phone, email, and chat, ClearOne Advantage ensures clients receive guidance throughout the entire settlement process.

Limitations & Considerations:

While ClearOne Advantage has many benefits, it’s essential to be aware of potential downsides:

- Debt settlement can negatively impact your credit score because creditors may report missed payments before settlements are reached.

- Not all creditors agree to settlements, which means some debts may still need to be repaid in full.

- State restrictions apply, and the service is not available in all U.S. states.

Customer Support Review:

ClearOne Advantage has received positive feedback for its customer service and transparency. Many clients praise the company for providing clear information about the settlement process and offering responsive support.

Here’s what a customer named Mark had to say about his experience:

“ClearOne Advantage helped me settle my credit card debts when I was drowning in payments. Their team was transparent, and I saved almost 50% on my total debt. The online portal made tracking everything easy. Highly recommend!”

Frequently Asked Questions (FAQ)

1. What types of debt does ClearOne Advantage handle? ClearOne Advantage specializes in unsecured debt, including credit card debt, personal loans, medical bills, and some private student loans. They do not handle secured debts like mortgages or auto loans. They don’t help with IRS or tax debt either.

2. How does ClearOne Advantage’s debt settlement process work? Clients enroll in a customized debt settlement program where they make monthly deposits into a special account. Once enough funds are accumulated, ClearOne negotiates with creditors to reduce the total debt amount. The process typically takes 24-48 months.

3. Are there any upfront fees? No. ClearOne Advantage follows a performance-based fee structure, meaning they only charge fees after successfully negotiating a debt settlement.

4. Will using ClearOne Advantage affect my credit score? Yes, debt settlement can impact your credit score. Since you stop making payments to creditors during negotiations, your credit score may drop. However, successfully settling debts can help you avoid more severe financial consequences like bankruptcy.

5. How long does the debt settlement process take? The process generally takes between 24 and 48 months, depending on the amount of debt and the client’s ability to make payments into the settlement account.

6. Is ClearOne Advantage available in all U.S. states? No, ClearOne Advantage is not available in all states. Check their website to see if they operate in your state.

7. Does ClearOne Advantage offer tax debt relief? No, ClearOne Advantage specializes in unsecured debt relief and does not offer services for IRS tax debt.

8. What qualifications do I need to enroll in ClearOne Advantage’s program? To qualify, clients generally need at least $10,000 in unsecured debt and must demonstrate a financial hardship that prevents them from repaying debts in full.

9. What should I expect during the free consultation? During the consultation, a debt specialist will review your financial situation and discuss potential savings, risks, fees, and timelines for debt relief.

10. How do I get started with ClearOne Advantage? Visit www.clearoneadvantage.com or call 1-888-340-4697 to schedule a free consultation.

Final Thoughts: Is ClearOne Advantage Right for You?

ClearOne Advantage is a legitimate and highly-rated debt settlement company that offers customized relief programs with no upfront fees. While debt settlement may impact your credit score, ClearOne Advantage has a strong track record of helping clients reduce their overall debt burden.

If you’re struggling with unsecured debt and considering settlement, ClearOne Advantage is worth exploring.

Check if you qualify Visit Website

by Amine Rahal | Feb 5, 2025 | Debt Relief

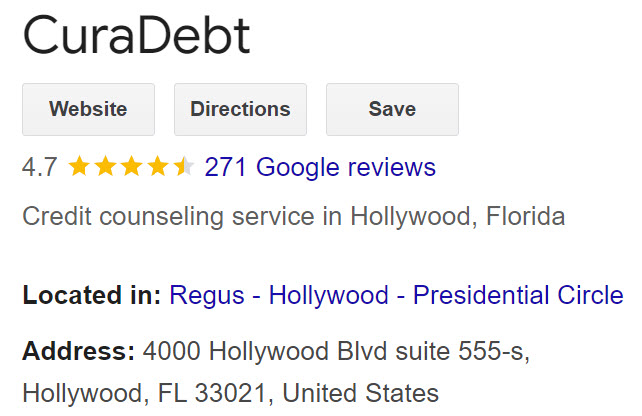

Credit: CuraDebt.com

CuraDebt (https://www.curadebt.com/) is a debt relief company that has been in business since 1996 (according to their website), making it one of the oldest in the industry. They offer debt settlement and relief services for various types of unsecured debt, including credit card debt, personal loans, medical bills, and tax debt. Based on our review, CuraDebt seems to have generated a lot of positive reviews for its debt relief services, particularly for its ability to help clients reduce their debt significantly through negotiations with creditors.

#1 Rated Debt Relief Company in 2025?

Are you looking for the #1 Rated Debt Relief & Settlement Company in 2025? See our New Era Debt review. New Era Debt has received the highest number of positive reviews amongst all the 20 companies we researched.

> Check if you qualify

> Visit Website

|

Who is CuraDebt?

As we said earlier, CuraDebt is a debt settlement company that specializes in negotiating with creditors on behalf of consumers to reduce their overall debt. They work with individuals who are struggling to manage their credit card debt, tax debt, medical bills, or other unsecured debts.

- Headquarters: Hollywood, Florida.

- States Covered: All states EXCEPT: Connecticut, Georgia, Kansas, New Hampshire, South Carolina, Vermont, and West Virginia

- Founded in: 1996 in Irvine.

- Website: https://www.curadebt.com/

- Phone: 1-877-850-3328 Ext. 400

- Services Offered:

- Free Debt Counselling

- Negotiation With Creditors

- Debt settlement

- Tax debt relief

- Debt consolidation (through partner lenders – watch out for the rates if you choose this path!)

- Minimum debt: $5,000

- Minimum Age: Must be at least 21+ years old.

- Income Minimum: No minimum but must have verifiable regular income

Company Legitimacy, Ratings & Reviews

As we covered earlier, this company is operating in the debt settlement space since 1996, which makes it one of the oldest in the industry. In our view, the company’s longevity speaks volumes about its professionalism and customer service.

- BBB Rating: A+ (best)

- BBB Reviews: 4.74/5 Stars (27 Reviews)

- Google Reviews: 4.8/5 Stars (304 Reviews)

- Investopedia: 3.9/5 Stars

- Yelp: 4.6/5 Stars (12 Reviews)

- TrustPilot: 4.7/5 Stars (30 Reviews)

- BankRate: 4.6/5 Stars

- Accreditations:

- Member of the American Association for Debt Resolution (AADR)

- Certified by the International Association of Professional Debt Arbitrators (IAPDA)

CuraDebt BBB

CuraDebt Investopedia Rating

CuraDebt Google Rating

CuraDebt Key Services & Features

- Free Consultation: They provide a free initial consultation to discuss your debt situation and see whether you qualify for their services and what debt relief program is best for you.

- List of Services Offered:

- Debt Settlement

- Debt Relief (Personal and Business)

- Debt Negotiation

- Debt Consolidation Program

- Tax Debt Relief

- Fee structure: No upfront fees; charges a fee only after successful debt settlement. Typically 20% of the settled debt

- Strategy: Utilizes various strategies, such as creditor violations (e.g., FDCPA, TCPA) to negotiate better terms for clients

- Limitations: services are not available in all U.S. states. Fill out the form to see if you qualify.

One of the key advantages of CuraDebt is that it does not charge upfront fees, meaning you only pay once a debt settlement has been successfully negotiated. The company’s fee structure is typically around 20% of the settled debt, which is in line with industry standards. CuraDebt is also known for its ability to identify creditor violations, which can sometimes lead to additional savings or settlements for the client.

However, it’s important to note that debt settlement can negatively impact your credit score, as the process often involves stopping payments to creditors while negotiations are underway. Additionally, CuraDebt’s services are not available in all U.S. states, and there have been some mixed reviews about customer service and transparency.

Customer Support Review

They seem to have a responsive customer support through their live chat feature. In fact, we asked their support team to explain their services briefly, and here is what one of their support agents named Genesis had to say:

“I’m going to explain a bit about our company and how we will assist you with your debt. Since 2000, we have been working nationwide, directly with clients’ creditors, to negotiate savings of 40 to 60 percent. Instead of making individual monthly payments to creditors, we create a plan for you where a portion of your funds is deposited into an account. As this amount accumulates, we negotiate agreements with your creditors on your behalf to eliminate your debt more quickly.

Here’s how it works: We will negotiate with each of your creditors to reduce the total amount you owe. For example, if you owe Capital One $800, and we negotiate it down to $300, you would pay $300 instead of $800. This $300 will come from your monthly payments into the account. Whenever we receive an offer, we will contact you to present it. Once you accept the offer, the money will be sent to the creditor.”

CuraDebt FAQ

What types of debt does CuraDebt handle?

CuraDebt specializes in settling unsecured debts, including credit card debt, personal loans, medical bills, private student loans, and tax debts. The company does not typically handle secured debts like mortgages or auto loans, although you should probably ask them to find out.

2. How does the CuraDebt debt settlement process work?

The process begins with a free consultation to assess your debt situation and see if you qualify for their services. If you enroll, CuraDebt will negotiate with your creditors to reduce the amount you owe. You’ll make monthly deposits into a dedicated savings account, which will be used to settle the negotiated debts. The typical time frame for settlement is 24 to 48 months.

3. Are there any upfront fees?

No, CuraDebt does not charge any upfront fees. You only pay a fee (usually 20% of the settled debt) after a successful settlement is reached and accepted.

4. Will using CuraDebt affect my credit score?

Yes, participating in a debt settlement program can negatively impact your credit score. The process often involves stopping payments to creditors, which can lead to a drop in your credit score. However, the goal is to eventually settle the debts for less than what is owed, which may help improve your financial situation in the long run. Also, note that the impact on your credit score isn’t as bad as a consumer proposal or bankruptcy.

5. How long does the debt settlement process take?

The debt settlement process with CuraDebt typically takes between 24 and 48 months, depending on the amount of debt and how quickly you can accumulate funds in your savings account for settlement.

6. Is CuraDebt available in all U.S. states?

No, CuraDebt’s services are not available in all states. It operates in 26 states and the District of Columbia. If you live in a state where CuraDebt does not operate, you’ll need to look for alternative debt relief options.

7. Does CuraDebt offer tax debt relief?

Yes, CuraDebt offers services to help with tax debt relief. Their team includes tax professionals who can negotiate with the IRS on your behalf to resolve tax debts, penalties, and liens.

8. What are the qualifications to use CuraDebt’s services?

To qualify for CuraDebt’s services, you must have a minimum of $5,000 in unsecured debt, be at least 21 years old, and have verifiable income. There is no maximum debt limit for their services.

9. What should I expect during the free consultation?

During the free consultation, a CuraDebt counselor will review your financial situation and discuss your options for debt relief. They will explain the potential savings, timeline, risks, and fees involved in the process. This consultation helps you decide if debt settlement is the right choice for you.

10. How do I get started with CuraDebt?

To get started, you can visit CuraDebt’s website to request a free savings estimate or call their customer service line. If you decide to enroll, you’ll be assigned a debt counselor who will guide you through the entire settlement process.

![Take Charge America – We Review This Debt Settlement Firm [2025 Update]](https://cpiinflationcalculator.com/wp-content/uploads/2025/02/TakeChargeAmericaHomepage-1080x675.jpg)

by Amine Rahal | Jan 5, 2025 | Debt Relief

Wondering if Take Charge America is a good option for debt settlement or debt relief? In this review of the company, we’ll look at their reviews and ratings from across the web, and we’ll break down their services when it comes to managing and decreasing debt.

#1 Rated Debt Relief Company in 2025?

Are you looking for the #1 Rated Debt Relief & Settlement Company in 2025? See our New Era Debt review. New Era Debt has received the highest number of positive reviews amongst all the 20 companies we researched.

> Check if you qualify

> Visit Website

|

Who is Take Charge America?

Take Charge America (TCA) is a nonprofit credit counseling agency that provides debt management, financial education, and housing counseling services. Founded in 1987, TCA has helped thousands of individuals regain financial stability through structured debt relief programs and personalized financial counseling.

- Headquarters: Phoenix, Arizona

- States Covered: Nationwide (Available in most U.S. states)

- Founded in: 1987

- Website: www.takechargeamerica.org

- Phone: 1-866-750-9634

Services Offered:

- Free Credit Counseling

- Debt Management Plans (DMPs)

- Budget Planning & Financial Education

- Housing Counseling (HUD-approved)

- Student Loan Counseling

- Bankruptcy Counseling

February 2025 Update: As per a recent press release, Take Charge America has expanded its free housing counseling and mortgage assistance services to California, thanks to a $250,500 grant from the California Housing Finance Agency (CalHFA). This initiative allows the nonprofit agency to provide confidential support to homeowners and renters struggling with delinquency, foreclosure risk, or navigating the homebuying process. The services include rental and mortgage delinquency assistance, reverse mortgage counseling, pre-purchase and post-purchase guidance, and rental counseling for first-time or low-income renters. As a nonprofit, Take Charge America remains committed to offering free, unbiased advice tailored to each client’s financial situation. Residents can schedule a virtual appointment by visiting TakeChargeAmerica.org or calling (866) 987-2008.

Minimum Requirements to Qualify:

- Minimum Debt: No strict minimum, but best suited for those with $5,000+ in unsecured debt

- Income Minimum: Must have verifiable income to support a repayment plan

Take Charge America Ratings & Reviews:

Take Charge America is known for its commitment to consumer financial education, transparent practices, and effective debt relief solutions. Here’s how they are rated across major platforms:

- BBB Rating: A+ (Accredited Business)

- BBB Reviews: 4.7/5 Stars

- Trustpilot: 4.8/5 Stars

- Google Reviews: 4.6/5 Stars

- Consumer Affairs: 4.5/5 Stars

- Investopedia Rating: 4.3/5 Stars

- Accreditations: Member of the National Foundation for Credit Counseling (NFCC), HUD-approved housing counseling agency

Key Features & Benefits:

1. Free Credit Counseling

Take Charge America provides a free, confidential financial review to help clients explore available debt relief options and develop a customized financial plan.

2. Debt Management Plans (DMPs)

- TCA works with creditors to reduce interest rates and eliminate late fees.

- Clients make one consolidated monthly payment to TCA, which is then distributed to creditors.

- Most DMPs last 36 to 60 months, depending on the debt amount.

3. Nonprofit & Transparent Fee Structure

- As a nonprofit agency, TCA offers low-cost solutions with fees regulated by state laws.

- Fees typically range from $0 to $50 for enrollment and $25 to $75 monthly.

4. Housing & Bankruptcy Counseling

- Provides HUD-approved housing counseling for mortgage assistance and foreclosure prevention.

- Offers pre-bankruptcy counseling and debtor education, as required by federal law.

5. Financial Education & Resources

- Free online courses, budgeting guides, and financial tools.

- Personalized coaching to help clients develop better financial habits and avoid future debt.

Limitations & Considerations:

While Take Charge America has many benefits, here are some potential downsides:

- Debt management plans require consistent payments – If you miss a payment, you may lose program benefits.

- Not all debts qualify – Secured debts like mortgages and auto loans are not eligible.

- State restrictions apply – Some services may not be available in all states.

Customer Support Review:

Take Charge America receives high marks for customer service and program transparency. Many clients praise the easy enrollment process and supportive financial counselors.

Here’s what a customer named Jessica had to say:

“Take Charge America helped me lower my credit card interest rates and develop a realistic repayment plan. Their team was professional, patient, and always available to answer my questions. I highly recommend them!”

Frequently Asked Questions (FAQ)

1. What types of debt does Take Charge America handle? TCA specializes in unsecured debts, such as credit card debt, medical bills, personal loans, and collections. They do not handle secured debts like auto loans or mortgages.

2. How does Take Charge America’s debt management plan work? A DMP consolidates all your eligible debts into one monthly payment. TCA negotiates with creditors to lower interest rates and waive fees, helping you pay off debt faster.

3. Are there any upfront fees? TCA’s fees vary by state, but they do not charge high upfront fees like for-profit debt relief companies. Many clients qualify for low-cost or waived fees.

4. Will using a debt management plan affect my credit score? DMPs may initially impact your credit score, but as you make consistent payments and reduce your debt, your score is likely to improve over time.

5. How long does a debt management plan take? Most DMPs take 3 to 5 years to complete, depending on the amount of debt enrolled.

6. Is Take Charge America available in all U.S. states? TCA operates in most states, but some services may not be available in all locations. Check their website or call for details.

7. Does Take Charge America offer student loan assistance? Yes, TCA provides guidance on student loan repayment options but does not offer direct consolidation services.

8. What qualifications do I need to enroll in a debt management plan? You must have verifiable income to ensure you can make consistent monthly payments.

9. What should I expect during the free consultation? During the consultation, a financial counselor will review your debt situation, discuss repayment strategies, and outline your best options.

10. How do I get started with Take Charge America? Visit www.takechargeamerica.org or call 1-866-750-9634 for a free consultation.

Final Thoughts: Is Take Charge America Right for You?

Take Charge America is a trusted nonprofit credit counseling agency that provides debt management plans, financial education, and personalized counseling. Their low fees, nonprofit status, and strong industry reputation make them an excellent choice for individuals struggling with credit card debt and looking for a structured path to financial stability.

If you’re seeking a reputable debt management program, Take Charge America is a solid option.

Check if you qualify

Visit Website

by Amine Rahal | Aug 30, 2024 | Debt Relief

In the U.S., interest rate caps—especially when it comes to protecting consumers from predatory lending—are largely regulated at the state level. This means that the maximum interest rates lenders can charge vary depending on which state you live in and the type of loan we’re taking out. Let’s break down how this works across different states.

What Qualifies as a “Predatory Loan”?

First, let’s compare a traditional loan you would get from a bank versus a “predatory loan” you would get from an alternative lender:

| Feature |

Traditional Bank Loan |

Predatory Loan |

| Interest Rate |

Low to moderate (typically 3% to 12% APR) |

Very high (can exceed 50% APR, sometimes 300%+) |

| Loan Terms |

Fixed terms (usually 1 to 30 years) |

Short terms (often 2 weeks to a few months) |

| Repayment Structure |

Monthly payments, often with amortization |

Lump-sum payment or frequent, high payments |

| Fees and Charges |

Transparent, disclosed upfront |

Hidden fees, high fees, or penalties |

| Borrower Qualification |

Strict requirements (credit score, income, etc.) |

Minimal qualification (often no credit check at all) |

| Regulatory Oversight |

Highly regulated by federal and state laws |

Often operates in regulatory gray areas |

| Purpose of Loan |

Typically for major purchases (homes, cars, education) |

Often for emergency or short-term needs |

| Impact on Credit Score |

Positive impact if paid on time, reported to credit bureaus |

Negative impact, often not reported positively to credit bureaus |

| Borrower Rights |

Strong consumer protections, recourse available |

Limited recourse, predatory practices common |

| Rollover/Renewal |

Generally not allowed or unnecessary |

Frequent rollovers, trapping borrowers in cycles |

| Lender’s Intent |

Long-term relationship, repayment is expected |

Profit from borrower’s inability to repay on time |

Essentially, a predatory loan is a type of loan that takes advantage of borrowers in vulnerable and dire financial situations. These loans often come with excessively high interest rates, hidden fees, or deceptive terms that make it difficult for borrowers to repay the loan.

Federal Protections

Before diving into state specifics, it’s worth noting that there is a federal cap in place for certain groups. The Military Lending Act (MLA) caps interest rates at 36% APR for active-duty service members and their dependents on most consumer loans. This law provides a strong layer of protection, but it only applies to military members. You can learn more about the MLA on the Consumer Financial Protection Bureau (CFPB) website.

State-Level Interest Rate Caps

Interest rate caps for everyone else are set by state laws, and these can vary widely:

- California

- Payday Loans: In California, payday lenders can charge up to $15 per $100 borrowed, which can equate to an APR of over 400% depending on the term of the loan.

- Installment Loans: For loans over $2,500, there’s no cap on interest rates.

- More Info: Check out California’s Department of Financial Protection and Innovation for detailed regulations.

- Colorado

- New York

- All Loans: New York has a strict usury law that caps interest rates at 16% for most types of consumer loans. Charging above 25% is considered criminal usury.

- More Info: For more on New York’s laws, the New York State Department of Financial Services is a good resource.

- South Dakota

- Payday Loans: Like Colorado, South Dakota caps payday loan rates at 36% APR. This cap was set after a successful 2016 ballot initiative aimed at protecting consumers from predatory lending practices.

- More Info: Learn more on the South Dakota Division of Banking website.

- Texas

- Payday Loans: Texas doesn’t cap interest rates directly for payday loans, but it does regulate fees. This can still lead to APRs that exceed 400%, depending on the loan’s terms, which is extremely high.

- More Info: The Texas Office of Consumer Credit Commissioner provides more information on lending laws in the state.

- Illinois

- Florida

- Utah

- All Loans: Utah has no cap on interest rates, making it one of the most lender-friendly states in the U.S. This means payday lenders and other high-interest lenders can charge extremely high rates. Beware of Utah-based lenders.

- More Info: For more, see the Utah Department of Financial Institutions.

Know Your Rights & Do Your Due Diligence

These state-specific laws are crucial because they determine how much protection you have against predatory lending practices. In states with strict caps like New York or Colorado, consumers are generally safer from exorbitant interest rates. But in states like Utah or Texas, the lack of caps means consumers need to be extra cautious when taking out loans.

Predatory loans have put many American consumers in dire financial situations, exacerbating their debt and pushing them into bankruptcies. If you are dealing with high debt and are struggling to pay your bills, consider debt settlement instead of requesting another loan which will most likely put you deeper into debt.

Finding Out More

If you’re considering taking out a loan, it’s a good idea to first check what the interest rate caps are in your state. You can usually find this information through your state’s Department of Financial Services or a similar regulatory body. Additionally, the Consumer Financial Protection Bureau (CFPB) offers a wealth of resources on consumer rights and protections.

By understanding these caps, you can better protect yourself from predatory lending practices and make more informed financial decisions.

by Alex Demolitor | Jul 8, 2024 | Debt Relief

If debt problems are mounting and pressure from creditors has become overwhelming, seeking professional help can ease the burden. Instead of forging the difficult path alone, strategizing with experts reduces the economic and psychological strain.

But, is Oak View Law Group the right partner to get you out of debt?

About the Company

- URL: https://www.ovlg.com/

- Phone: 1-800-530-6854

- Email: clientintake@ovlg.com

- Company HQ: Auburn, CA

- Trustpilot Reviews: 4.4/5 stars (15 reviews)

- Google Reviews: 4.4/5 stars (12 reviews)

- Better Business Bureau (BBB) Reviews: 4.7/5 (12 reviews)

Pros and Cons

For a quick breakdown of how Oak View Law Group stacks up, please see the list below:

Pros:

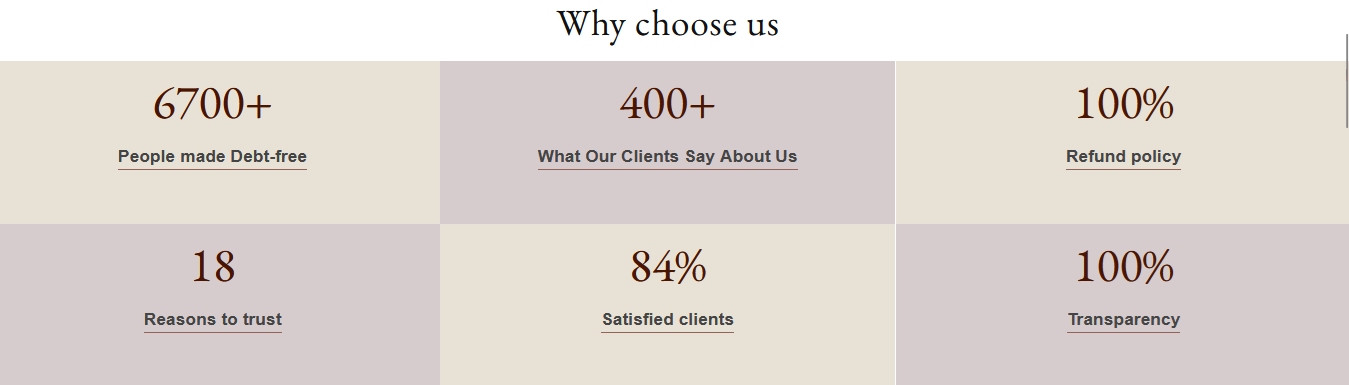

- Has helped more than 6,700 clients become debt-free

- Its team of experts has experience across 15 segments of consumer law

- There is a “No-Questions-Asked Refund Policy”

- Oak View Law Group provides professional guidance and mentorship throughout the debt-relief process

- Oak View Law Group can often settle your debts at 40% to 60% of the outstanding balance

- There are services for auto, medical, and student loan debt

- Highly rated by clients

Cons:

- Fees are federally regulated but can be high in some cases

What is Oak View Law Group?

Helping more than 6,700 clients become debt-free, Oak View Law Group is a consumer law firm headquartered in California. It specializes in debt relief, debt consolidation, and bankruptcy services. The group helps clients save money, avoid lawsuits, and has a team of experts with experience across 15 segments of consumer law. Moreover, Oak View Law Group has a “No-Questions-Asked Refund Policy,” where your fees and trust account balance are reimbursed if you’re unsatisfied with the service.

Some of Oak View Law Group’s services include:

- Debt Consolidation

- Debt Settlement

- Chapter 7 Bankruptcy

- Chapter 13 Bankruptcy

- Payday Loan Consolidation

- Payday Loan Settlement

For more insights on the value of these services, the Federal Trade Commission (FTC) has a helpful guide on How To Get Out of Debt.

How Can Oak View Law Group Help Me?

Working with a credit professional is like having an experienced coach to draw up plays on your behalf. And like any sport, it allows for a clearer strategy to achieve the team’s goals.

Oak View Law Group provides professional guidance, mentorship, and develops an effective debt-relief strategy, similar to a licensed insolvency trustee (LIT). Our partner site has an extensive guide on The Benefits of a LIT, which can help you determine if a consumer proposal or bankruptcy is the best strategy. Some of the differences include:

- You often forfeit more personal assets in bankruptcy

- Bankruptcy has a greater impact on your credit score

- An initial bankruptcy stays on your credit report for six years or more versus three years with a consumer proposal

For more information, please see our partner guide, What Is a Consumer Proposal in Canada and Who Is It For?

Similarly, Oak View Law Group provides parallel guidance to a LIT. By weighing the pros and cons of several scenarios, its team can help improve your financial health by achieving the following:

- Lower monthly payments and interest charges

- Devise a plan for manageable monthly payments

- Reduce or eliminate late fees

- Reduce or eliminate collection calls

What Is Oak View Law Group’s Settlement Program?

When working with Oak View Law Group, its team handles the day-to-day negotiations with creditors. For example, they manage creditor calls, negotiations, bill payments, and ensure you can enjoy your professional and personal lives with minimal disruption.

How Long Does It Take to Become Debt-Free?

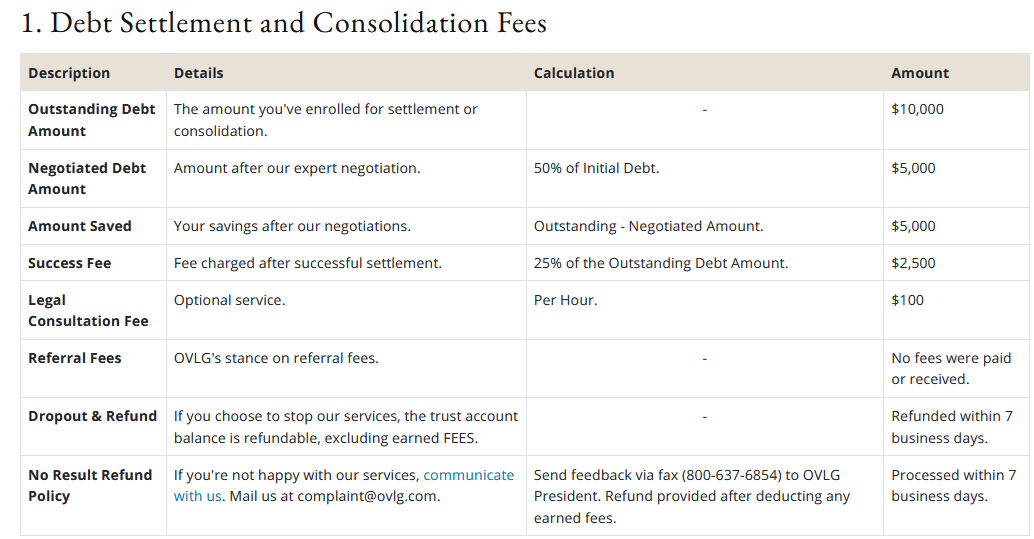

Depending on the amount owed and your excess income, estimates can vary widely. In a nutshell: it often depends on how much funds you want to allocate to debt repayments.

For example, let’s say you have $10,000 in debt and Oak View Law Group negotiates a 50% settlement. You have to pay $5,000 and can choose a lump-sum payment or monthly installments.

The firm notes that “As per the industry trends and our experience, debt can be settled at 40% to 60%, but we always negotiate for the lowest settlement percentage possible to save more for our clients.”

Thus, if you can cut the collection amount in half by working Oak View Law Group, it should greatly enhance the speed at which you become debt-free.

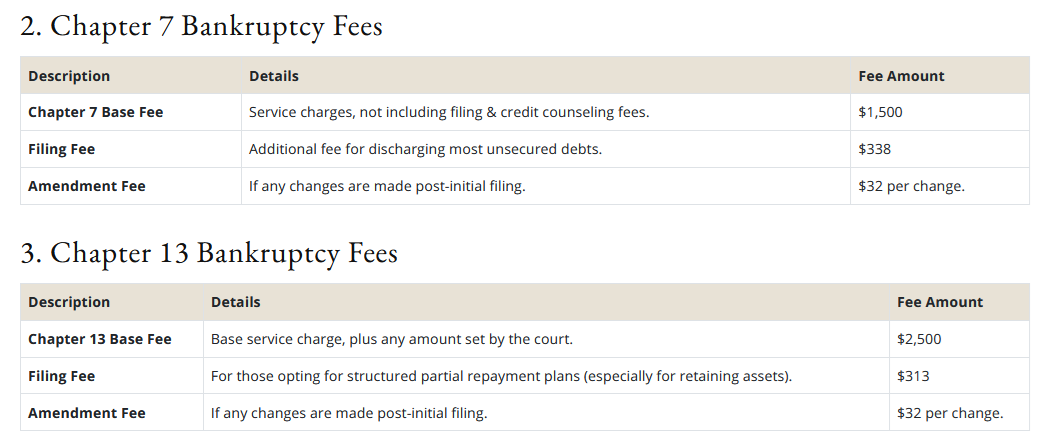

What Does Oak View Law Group Charge In Fees?

Adhering to FTC guidelines, Oak View Law Group’s fees are outlined in the graphics below:

What Other Services Does Oak View Law Group Provide?

If you’re struggling with auto, medical, or student loan debt, Oak View Law Group can assist in these areas too.

- Regarding auto loans, the firm can help if the vehicle has been repossessed, sold, or is being processed by a third-party collection agency.

- For overdue medical bills, the firm notes that healthcare companies “do not provide settlement offers.” Consequently, Oak View Law Group can only help you negotiate a manageable repayment plan.

- Likewise, student loan companies do not provide settlement plans either, and Oak View Law Group can only help if the account has been transferred to collections.

How Do Clients Rate Oak View Law Group?

While the firm doesn’t have a lot of Google or Trustpilot reviews, the vast majority of clients were satisfied with Oak View Law Group’s services. Many cited efficient settlement procedures and noted how Oak View Law Group provided support and guidance throughout the process. A few of the testimonials read:

- Oak View Law Group was able to settle my huge payday loan debts. The staff were very helpful and understanding. I can’t believe how fast and easy they were able to settle my debt. Much respect to Oak View Law Group. Thank you for getting me out of debt.

- OVLG assisted me in resolving three payday loan debts. Mr Sanchez assured me that all debts would settled by the projected date and I would have access to himself, agents, and my account online. The process went just as planned, he communicated with me every step of the way and was patient to answer all my concerns. I would definitely return as well as recommend OVLG.

- I have worked with OVLG, specifically, Diego, and I cannot say enough good things that he and OVLG have done for me. They have helped me so much and are diligent, professional, and understanding. I am truly amazed at how quickly Diego replies. Great company, great assistance. They truly give you hope.

As a result, not only does Oak View Law Group develop strategies for effective debt relief, but it also shows empathy when dealing with difficult situations.

Are We Believers In Oak View Law Group?

Because client testimonials are the best indicator of distinguished service, Oak View Law Group’s reviews speak for themselves. By providing guidance, mentorship, and working with clients every step of the way, the firm has developed a compassionate reputation.

Moreover, if Oak View Law Group can negotiate debt settlements at 40% to 60% of the outstanding balance, the cost savings can greatly outweigh the service fees. On top of that, the “No-Questions-Asked Refund Policy” adds further credibility and reduces your risk if you’re unhappy with the process.

All in all, there is a lot to like about Oak View Law Group, and if your debts have become unmanageable, it may be the right firm for you.

If you want to learn more, visit: https://www.ovlg.com/