-v3")

TurboDebt (sometimes written as Turbo Debt) is a U.S. debt relief brand that helps consumers explore options for tackling unsecured debt (like credit cards, personal loans, medical bills, and collections). The key thing to understand up front is that TurboDebt often acts as a connector that matches you with a debt relief program that fits your situation, rather than always being the company that negotiates directly with your creditors.

TurboDebt (sometimes written as Turbo Debt) is a U.S. debt relief brand that helps consumers explore options for tackling unsecured debt (like credit cards, personal loans, medical bills, and collections). The key thing to understand up front is that TurboDebt often acts as a connector that matches you with a debt relief program that fits your situation, rather than always being the company that negotiates directly with your creditors.

PS: Want a fast, personalized starting point before you call anyone? Take our quick quiz here: Debt Relief Quiz (settlement vs consolidation vs bankruptcy).

- Helps narrow down your best-fit option

- Useful if you are torn between multiple debt solutions

- Fast, simple, and more personalized than guessing

- Every debt situation is different

- The right option depends on your budget, goals, and urgency

- Use the quiz as a smart starting point before committing

TurboDebt company snapshot (updated for 2026)

- Company: TurboDebt, LLC

- Website: TurboDebt.com

- Headquarters (published on TurboDebt site): 1643 NW 136th Ave, Building H, Sunrise, FL 33323

- Email (published on TurboDebt site): contact@turbodebt.com

- Availability: TurboDebt states it does not offer services in CT, MN, OR, VT, WV, and WI. Always confirm availability from their “Areas We Serve” page before you spend time on an application.

Legitimacy, ratings & reviews (2026 update)

Below is a current snapshot of third-party ratings. These numbers can change over time, so consider them a “temperature check,” not a guarantee of your experience.

TurboDebt

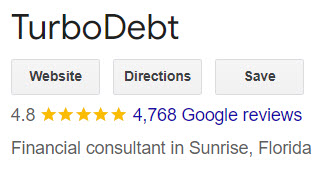

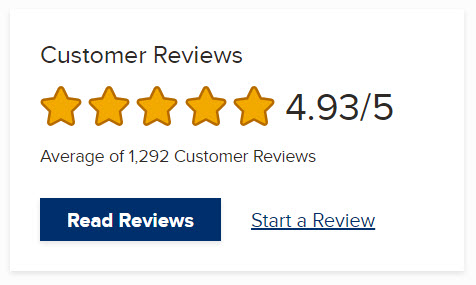

- BBB: A+ rating; customer reviews about ★ 4.87/5 (1,300+ reviews)

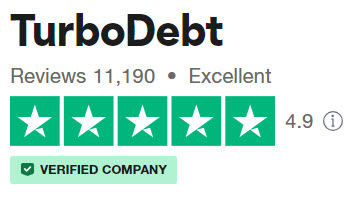

- Trustpilot: ★ 4.9/5 (14,000+ reviews)

What TurboDebt actually does (and the question you should ask)

TurboDebt describes itself as a service that connects clients to debt relief programs. In practice, that can mean your case may be handled by a partner program (example partners listed publicly include National Debt Relief and others). That isn’t automatically “bad,” but it changes what you should ask on your first call:

- Who will be the actual program provider negotiating with my creditors?

- What is the total cost (program fees + any dedicated account fees), and when do those costs get charged?

- Will I be asked to stop paying creditors during the program, and what happens if a creditor sues?

- How will you communicate settlement offers, and do I have to approve each settlement?

How debt settlement usually works (plain English)

- Free consultation: you share your debts, budget, and hardship.

- Program fit: if settlement is recommended, you’ll typically open a dedicated account to build funds for offers.

- Negotiations: once enough funds accumulate, settlements are negotiated one debt at a time.

- Fees: reputable providers generally cannot charge “advance fees” before results (make sure you understand fee timing).

- Finish line: the goal is to resolve each enrolled debt and close the program.

If you’re new to this, two excellent government resources to read first are the FTC’s overview of getting out of debt and the CFPB’s explanation of debt relief programs. Also be aware that canceled debt can sometimes trigger tax forms (like a 1099-C), depending on your situation.

TurboDebt Pros 👍

- Massive review footprint: TurboDebt has a very large volume of consumer reviews across major platforms, which is useful for due diligence.

- Clear “shopping” entry point: If you’re not sure which option fits (settlement vs counseling vs consolidation), TurboDebt can be a starting conversation.

- Availability in most states: While not nationwide, it is available in many U.S. states (confirm via their service area page).

TurboDebt Cons 👎

- Potential “middle layer”: Because TurboDebt can act as a connector, you must confirm who the actual program provider is and what their policies are.

- Costs can be significant: Debt settlement fees are often a percentage of enrolled debt, and you may also pay account fees depending on the setup.

- Credit impact risk: Many settlement programs involve missed payments, which can hurt credit and increase collection pressure before resolution.

Before you commit to any company or program, take our quick quiz. It can help you figure out which debt relief path may fit your situation best.

What types of debt can these programs usually help with?

Most debt settlement programs focus on unsecured debts, for example:

- Credit card balances

- Personal loans

- Medical bills

- Collections

- Some private unsecured lines of credit

They typically do not “settle” secured debts in the usual way (like mortgages or auto loans) because those are tied to collateral. Student loans and tax debts have their own rules and may require different specialists.

Who TurboDebt might be best for (and who should look elsewhere)

- Better fit: You want to explore options, you have meaningful unsecured debt, and you can commit to a structured payoff plan.

- Probably not a fit: Your debt is mostly secured (mortgage/auto), you’re current on everything and just want a lower interest rate, or you need legal protection quickly (in that case, speaking with a bankruptcy attorney may be smarter).

Other reputable options to compare

Even if you like what you hear from TurboDebt, I would still compare a few other providers before making any decision. Debt relief is not one-size-fits-all. Some companies are better for straightforward unsecured debt, some are stronger for tax debt, and some may be a better fit if you want a more legal-heavy approach.

Here are several alternatives you can review on our site:

- CuraDebt review – a well-known name that can be worth a look if you want to compare a more established debt relief brand.

- Oak View Law Group review – a useful option to compare if you prefer a law-firm-style approach or want help with more complex debt situations.

- JG Wentworth Debt Relief review – worth reviewing if you want to compare another major brand with broad consumer awareness.

- National Debt Relief review – one of the biggest names in the space, and a smart benchmark when comparing fees, process, and reputation.

- Freedom Debt Relief review – another large provider that is useful to compare if you want to see how a major national company stacks up.

- Pacific Debt Relief review – a good one to look at if your focus is mainly unsecured debt like credit cards, loans, collections, or medical bills.

- Accredited Debt Relief review – worth comparing if you want to look at a provider that may offer both settlement and consolidation-style options through partners.

- CreditAssociates review – another option to compare if you want a broader sense of how different programs structure their process and fees.

If you want a broader shortlist instead of reviewing companies one by one, here is our full rankings page: Best debt settlement companies ranked by ratings & reviews.

And if you are still not sure whether debt settlement is even the right route for you, I would take our Debt Relief Quiz before speaking with any company. It can help you think through whether settlement, consolidation, or even bankruptcy may be the better fit for your situation.

Bottom line (Our conclusion for 2026)

TurboDebt appears legitimate and has strong public ratings. The main “watch-out” is clarity: confirm who will actually manage your program, get the total fee schedule in writing, and make sure you’re comfortable with the timeline and credit impact.

Take our quick debt relief quiz to compare paths like settlement, consolidation, and bankruptcy before you decide what to do next.

Frequently asked questions

Will debt settlement hurt my credit?

It can. Many settlement programs involve missed payments before debts are resolved, which can damage credit scores and increase collection activity. If protecting credit is your top priority, ask about alternatives like a nonprofit debt management plan (DMP) or consolidation.

Can creditors sue me while I’m in a program?

Yes, it’s possible. Not every creditor agrees to settle, and some may pursue collections or lawsuits depending on the balance, timeline, and creditor policies. Ask how your provider handles lawsuits and whether they offer any support or referrals.

How long does debt settlement usually take?

It depends on how much you owe and how much you can set aside each month. Many programs are marketed in multi-year timeframes. The realistic way to judge it is simple: how fast you can build funds for settlement offers.

Are there tax consequences if a debt is forgiven?

Sometimes. If a creditor forgives part of your debt, you may receive a tax form and the forgiven amount may be treated as income, depending on your situation. If you’re close to enrolling, consider checking with a tax pro so you’re not surprised later.

What fees should I expect?

Ask for a complete fee schedule in writing. The big variables are (1) the program fee (often a percentage of enrolled debt), (2) whether the fee is based on enrolled debt or settled debt, and (3) whether there are monthly dedicated-account fees.

What questions should I ask on the first call?

Ask who the actual program provider is, whether you’ll be advised to stop paying creditors, the total cost including any account fees, whether you approve each settlement, and what happens if a creditor refuses to negotiate.

Is a nonprofit debt management plan (DMP) safer?

A DMP can be a good option if your main issue is high interest rates and you can afford to repay the principal over time. It’s not debt settlement, but it may reduce interest and create one structured payment. It’s worth comparing before you commit to settlement.

What if I’m considering bankruptcy?

Bankruptcy can offer stronger legal protections and may be the right move in some situations. If you’re behind, facing lawsuits, or simply can’t make progress, it can be worth speaking with a bankruptcy attorney for an initial consult.

Amine is an entrepreneur, investor and financial writer that covers the US economy, inflation, alternative investments, cryptocurrencies and more. He has been involved in the space for over a decade.