by Amine Rahal | May 17, 2026 | Debt Relief

Learning how to stop spending money is not really about becoming cheap, miserable, or obsessed with every dollar. It is about getting back in control. If your money keeps disappearing before the end of the month, or you keep promising yourself you will “start saving next month,” the problem is usually not a lack of intelligence. It is a lack of structure.

Struggling With Debt Because of Overspending?

If overspending has already turned into credit card debt, personal loans, or missed payments, it may help to compare your options before things get worse. Our debt relief quiz can help you think through settlement, consolidation, credit counseling, bankruptcy, and other possible next steps.

Take the Debt Relief Quiz

I have been writing about personal finance, inflation, debt, and consumer products for more than two decades, and I have noticed something important: most people do not overspend because they are careless. They overspend because modern life makes spending incredibly easy. One-click checkout, food delivery apps, subscriptions, credit cards, social media ads, inflation, and “limited-time” deals all work together to make your money leave faster than you realize.

The good news is that you can fix this without turning your life into a punishment. Below, I’ll walk through a practical, realistic system for spending less, saving more, and feeling less stressed about money.

How to Stop Spending Money: Start With the Real Problem

Before you cut anything, you need to understand where your money is actually going. Many people build budgets based on what they think they spend. That rarely works. The Consumer Financial Protection Bureau recommends checking your bank statements carefully to see whether your budget reflects reality, not what you wish your spending looked like.

That is the right place to start. Pull your last 30 to 90 days of transactions and sort your spending into categories. You do not need fancy software. A spreadsheet, budgeting app, notebook, or printed bank statements can all work.

| Spending Category |

Examples |

Question to Ask |

| Needs |

Rent, mortgage, utilities, groceries, insurance, basic transportation |

Is this necessary, and can I reduce the cost? |

| Wants |

Restaurants, shopping, entertainment, travel, upgrades |

Does this still feel worth it after the moment passes? |

| Leaks |

Unused subscriptions, impulse orders, delivery fees, bank fees |

Would I miss this if it disappeared tomorrow? |

| Debt |

Credit cards, personal loans, buy-now-pay-later payments |

Is past spending now limiting my present choices? |

Do this before making big emotional decisions. You may discover that the problem is not your occasional coffee. It may be food delivery, car payments, insurance, subscriptions, Amazon orders, credit card interest, or lifestyle creep.

1. Create a “No-Judgment” Spending Audit

The first step is not to shame yourself. It is to collect the facts. A spending audit should feel like looking at a map, not standing in front of a judge.

Go through your last three months of spending and highlight anything that surprises you. I like this exercise because it separates real problems from imagined ones. I have seen people feel guilty over small purchases while ignoring hundreds of dollars in recurring charges they barely use.

Simple exercise: Circle every transaction you would not choose again today. That is your first list of spending cuts. You are not cutting joy. You are cutting regret.

Look especially for:

- Subscriptions you forgot about

- Food delivery and convenience fees

- Impulse shopping from social media ads

- Multiple small purchases that add up

- Bank fees, overdraft fees, and late fees

- Credit card interest from balances you carry

- Duplicate services, apps, insurance, or memberships

If inflation is making your budget tighter, you may also want to use our CPI inflation calculator to see how much purchasing power has changed over time. Rising costs can make an old spending pattern much harder to maintain.

2. Separate “I Want This” From “I Want Relief”

A lot of spending is emotional. That does not make it bad. It just means you need to understand what the purchase is really doing for you.

Sometimes you buy something because you genuinely want it. Other times, you buy because you are tired, stressed, bored, lonely, underpaid, overworked, or looking for a quick reward. The purchase becomes a small hit of relief. The problem is that relief fades, but the credit card bill stays.

Before making a non-essential purchase, ask yourself:

- Do I want the item, or do I want the feeling of buying it?

- Would I still want this tomorrow morning?

- Is this purchase solving a real problem?

- Will I be glad I bought this in 30 days?

- Am I spending because I feel behind compared to other people?

This is where I think many budgeting articles miss the point. People do not need another lecture about “discipline.” They need a pause between the trigger and the purchase.

3. Use the 24-Hour Rule for Impulse Purchases

If you want to stop spending money impulsively, add friction. For any non-essential purchase over a set amount, wait 24 hours before buying. For bigger purchases, wait 7 days.

This one rule can save a surprising amount of money because most impulse purchases lose their power once the moment passes.

| Purchase Amount |

Waiting Period |

Best Use |

| Under $25 |

Pause for 10 minutes |

Snacks, apps, small online purchases |

| $25 to $100 |

Wait 24 hours |

Clothes, gadgets, small home items |

| $100 to $500 |

Wait 3 days |

Electronics, furniture, travel upgrades |

| Over $500 |

Wait 7 days |

Major purchases and financing decisions |

During the waiting period, put the item in a note on your phone instead of your shopping cart. If you still want it later and it fits your budget, you can buy it with less regret.

4. Delete the Triggers That Make Spending Too Easy

Willpower is overrated. Environment matters more.

If your phone is filled with shopping apps, saved credit cards, delivery apps, and promotional emails, you are making spending easy and saving hard. You do not need to “be stronger.” You need fewer traps.

Try this for one week:

- Delete shopping apps from your phone.

- Remove saved credit cards from online stores.

- Unsubscribe from promotional emails.

- Turn off sale notifications.

- Stop browsing stores when you are bored.

- Use a separate browser profile with no saved payment information.

It sounds simple because it is simple. But simple does not mean ineffective. Making a purchase take 60 seconds longer can be enough to stop a lot of unnecessary spending.

5. Build a Budget That Matches Real Life

A budget that only works on paper is not a budget. It is a wish list.

The CFPB describes budgeting as a way to get a handle on debt and work toward savings goals. I agree with that, but I would add one more thing: your budget has to leave room for being human.

If you currently spend $800 a month on restaurants and delivery, do not tell yourself you will spend $0 next month. That may work for a week, then you will probably rebound. A better first goal might be $500, then $350, then $250.

My rule: Do not build a budget around your most disciplined day. Build it around a normal month, then improve it gradually.

A realistic budget should include:

- Fixed bills

- Variable essentials

- Debt payments

- Savings

- Fun money

- Irregular expenses like car repairs, gifts, medical bills, and annual renewals

Irregular expenses are where many budgets break. If you do not plan for them, they become “emergencies” and often end up on a credit card.

6. Give Yourself a Weekly Spending Limit

Monthly budgets can feel too abstract. A weekly spending limit is easier to manage because the timeline is shorter.

After your fixed bills, savings, and debt payments are accounted for, decide how much you can spend each week on flexible categories like restaurants, coffee, clothes, entertainment, rideshares, and personal purchases.

For example, if you can afford $600 per month in flexible spending, give yourself $150 per week. Once the weekly amount is gone, you pause until next week.

This creates a natural boundary without forcing you to track every penny forever.

7. Use Separate Accounts to Protect Your Money From Yourself

One of the most effective ways to stop overspending is to keep all your money from sitting in one checking account. When everything is mixed together, it is easy to mistake bill money or savings money for spendable money.

Consider using separate accounts for:

- Bills

- Emergency savings

- Short-term goals

- Everyday spending

- Debt payoff

When income comes in, move money into the right buckets first. Then you can spend from your everyday spending account without constantly doing mental math.

The FDIC Money Smart program offers financial education resources designed to help people build practical money skills and confidence. That kind of basic structure matters more than most people realize.

8. Stop Using Credit Cards for Problem Categories

Credit cards are not automatically bad. They can offer convenience, fraud protection, rewards, and clean records of spending. But if a credit card makes it easy for you to overspend, it is not helping you.

You do not need to stop using credit cards forever. You can simply stop using them for the categories where you lose control.

For example:

- If you overspend on food delivery, use a debit card only for food apps.

- If you overspend on clothes, remove your credit card from clothing websites.

- If you overspend on nights out, use a cash limit for entertainment.

- If you overspend on Amazon, remove saved payment methods and require a waiting period.

The goal is not perfection. The goal is to stop giving your weakest category unlimited access to borrowed money.

If credit card balances are already becoming difficult to manage, read our broader guide to debt relief options or compare reputable providers in our list of the best debt settlement companies.

9. Identify Your “Expensive Defaults”

Most overspending is not from one dramatic purchase. It is from defaults.

Your default lunch is takeout. Your default evening is delivery and streaming. Your default commute is rideshare. Your default reaction to stress is online shopping. Your default grocery trip includes extras you did not plan to buy.

To stop spending money, you need better defaults.

| Expensive Default |

Better Default |

| Ordering lunch every workday |

Pack lunch 3 days per week and buy lunch 2 days per week |

| Browsing online stores at night |

Keep a wish list and review it once per week |

| Buying groceries without a list |

Plan 3 simple meals before shopping |

| Using credit cards for everything |

Use debit or cash for categories where you overspend |

I like this approach because it does not depend on being perfect. You are simply replacing one habit with another habit that costs less.

10. Cut the Spending That Does Not Improve Your Life

Not all spending is bad. Some spending makes life better. A good meal with someone you love, a gym membership you actually use, a trip you planned responsibly, or tools that help you earn more money can all be worthwhile.

The spending to cut first is the spending that gives you little or no value.

Ask yourself these:

- What do I spend money on but barely enjoy?

- What do I keep paying for out of habit?

- What purchases do I regret most often?

- What spending is mostly about convenience?

- What spending is mostly about impressing other people?

This is where the biggest wins usually come from. You do not need to remove everything fun. You need to remove the spending that does not feel worth it.

11. Build a “Worth It” List

Cutting spending becomes easier when you know what you are protecting.

Create a short list of things that are genuinely worth spending money on. This may include travel, health, family experiences, paying off debt, building an emergency fund, investing, starting a business, or saving for a home.

When you know what matters most, it becomes easier to say no to what matters least.

Example “Worth It” List

- Emergency fund

- Debt freedom

- Health and fitness

- Quality time with family

- One planned vacation per year

- Retirement savings

- Career or business tools that increase income

This turns saving money from a punishment into a tradeoff. You are not just “spending less.” You are redirecting money toward things you actually care about.

12. Watch Out for Lifestyle Creep

Lifestyle creep happens when your spending rises as your income rises. You get a raise, bonus, tax refund, or better job, but instead of getting ahead, you upgrade everything: apartment, car, restaurants, clothes, vacations, subscriptions, and gadgets.

A little lifestyle improvement is fine. You should be able to enjoy some of your progress. The problem is when every raise disappears into new fixed expenses.

Before increasing your lifestyle, decide what percentage of new income will go toward savings, debt payoff, or investing. Even saving 30% to 50% of every raise can make a big difference over time.

Inflation can make lifestyle creep harder to spot because some of your spending increases may be unavoidable. That is why it helps to follow inflation data through our 2026 U.S. inflation rate and CPI data and understand how CPI affects inflation.

13. If Debt Is Driving the Stress, Deal With the Debt Directly

Sometimes the issue is not just spending. It is debt.

If you are carrying high-interest credit card balances, a large part of your monthly cash flow may be going to interest instead of progress. That can make it feel impossible to stop spending because your budget is already under pressure before the month begins.

The Federal Trade Commission says consumers can contact credit card companies directly to ask for a lower interest rate or a payment plan they can afford. You do not always need to pay a company to have that conversation for you.

Depending on your situation, possible options may include:

- Negotiating lower interest rates

- Using a debt payoff strategy

- Credit counseling

- Debt consolidation

- Debt settlement

- Bankruptcy in more serious cases

If you are comparing options, our debt relief quiz can help you think through which direction may make sense. You may also want to read our guide on debt and Chapter 7 bankruptcy if your debt has become unmanageable.

14. Give Yourself a Small Amount of Guilt-Free Spending

This may sound strange in an article about how to stop spending money, but you should probably keep some fun money in your budget.

Why? Because a budget with no room for enjoyment often fails. People can live on restriction for a while, but eventually they snap back. A small, planned amount of guilt-free spending can prevent bigger, unplanned spending later.

The key is to set the amount in advance. Once it is gone, it is gone. That gives you freedom inside a boundary.

15. Use a 30-Day Reset if Spending Feels Out of Control

If your spending feels completely out of control, try a 30-day reset. This is not forever. It is a short-term pause to break the cycle and see what you actually miss.

30-Day Spending Reset

- No non-essential online shopping

- No food delivery unless truly necessary

- No new subscriptions

- No buy-now-pay-later purchases

- No browsing stores for entertainment

- Keep groceries, bills, transportation, healthcare, and planned essentials

- Write down every purchase you wanted to make but skipped

At the end of 30 days, review what you missed and what you forgot about. The things you forgot about were probably not that important. The things you truly missed can be added back in a more intentional way.

How to Stop Spending Money: A Simple Weekly Plan

If you want a simple action plan, start here:

| Week |

Main Goal |

Action Steps |

| Week 1 |

Find the leaks |

Review 90 days of spending, cancel unused subscriptions, identify regret purchases. |

| Week 2 |

Add friction |

Delete shopping apps, remove saved cards, use the 24-hour rule. |

| Week 3 |

Create boundaries |

Set a weekly spending limit and separate bill money from spending money. |

| Week 4 |

Redirect money |

Move saved money toward debt, emergency savings, or another clear goal. |

Final Thoughts: Spend Less Without Hating Your Life

The best way to stop spending money is not to shame yourself into a strict budget you cannot maintain. It is to build a system that makes good decisions easier and impulsive decisions harder.

Start with your real spending. Identify the leaks. Add friction to impulse purchases. Separate your accounts. Give yourself a weekly limit. Keep some guilt-free spending. Then redirect the money you save toward something that actually improves your life.

In my experience, people do not usually need a perfect budget. They need a budget that survives real life.

And if rising prices are part of why your budget feels tighter, spend some time learning how inflation affects your money. Our guides on different ways of measuring inflation, inflation vs. recession vs. depression, and predatory lending and interest rate caps can help you make better financial decisions in a higher-cost environment.

Frequently Asked Questions About How to Stop Spending Money

How do I stop spending money so quickly?

Start by reviewing your last 30 to 90 days of transactions. Look for spending leaks like subscriptions, food delivery, impulse shopping, fees, and purchases you regret. Then add friction by deleting shopping apps, removing saved credit cards, and using a 24-hour rule before buying non-essential items.

Why can’t I stop spending money?

Many people overspend because spending is emotional, easy, and often automatic. Stress, boredom, social pressure, convenience, and saved payment methods can all lead to overspending. The solution is usually not more guilt. It is better systems, fewer triggers, and clearer spending limits.

What is the 24-hour rule for spending?

The 24-hour rule means waiting at least one full day before making a non-essential purchase. This gives the impulse time to fade and helps you decide whether you actually want the item or just wanted the feeling of buying it.

How do I stop impulse buying?

To stop impulse buying, remove saved credit cards, delete shopping apps, unsubscribe from promotional emails, avoid browsing stores when bored, and keep a wish list instead of buying immediately. Review the wish list once per week and only buy what still feels worth it.

Should I stop using credit cards if I overspend?

You may not need to stop using credit cards completely, but it can help to stop using them in categories where you overspend. For example, you might use debit or cash for restaurants, clothes, delivery apps, or entertainment while keeping credit cards for planned bills only.

How can I save money when everything is expensive?

When prices are high, focus first on spending leaks and flexible categories. Review subscriptions, food delivery, insurance, phone plans, bank fees, grocery habits, and debt interest. You may not be able to cut every expense, but small repeated savings can free up meaningful cash flow over time.

What should I cut first when trying to spend less?

Cut spending that gives you the least value first. This usually includes unused subscriptions, impulse purchases, excessive delivery fees, bank fees, duplicate services, and purchases you regularly regret. Avoid cutting everything enjoyable at once, because overly strict budgets are harder to maintain.

How do I stop spending money on food delivery?

Delete food delivery apps for 30 days, remove saved payment methods, keep easy backup meals at home, and set a weekly restaurant budget. You do not have to eliminate takeout forever. The goal is to stop using delivery as the default answer every time you are tired or busy.

How do I stop spending money online?

To stop online overspending, remove saved cards, delete shopping apps, unsubscribe from store emails, block shopping sites during vulnerable times, and use a waiting period before buying. Keeping a wish list instead of a shopping cart can also reduce impulse orders.

What if I already have debt from overspending?

If overspending has already created debt, focus on both the habit and the debt balance. Review your spending, stop adding new debt, contact creditors if payments are becoming hard to manage, and compare options such as budgeting, credit counseling, consolidation, settlement, or bankruptcy depending on your situation.

by Amine Rahal | Apr 21, 2026 | Debt Relief

If you are trying to pay off $20,000 in credit card debt, I want to start with this: it is a serious amount of debt, but it is not automatically a financial death sentence. I have covered personal finance and debt-related topics for more than two decades, and one thing I have noticed is that people often make things worse by panicking, choosing the wrong strategy too fast, or pretending the problem will somehow solve itself. The smarter move is to get clear on your numbers, cut through the noise, and choose the option that actually fits your situation.

Not sure whether consolidation, settlement, counseling, or bankruptcy makes the most sense?

Take our quick debt relief quiz before you commit to anything. It can help you narrow down which path may fit your situation best.

Take the Debt Relief Quiz

In plain English, paying off $20,000 of credit card debt usually comes down to one of five paths: a do-it-yourself payoff plan, a balance transfer, a consolidation loan, a debt management plan through nonprofit credit counseling, or a more aggressive option like debt settlement or bankruptcy. The right answer depends on your income, your credit score, your interest rates, and whether you are still current on your payments.

If you are brand new to this topic, it may also help to start with our broader guide to debt relief in the U.S. so you can see where this article fits into the bigger picture.

Quick answer

If your income is stable and you can still make real progress each month, start with a payoff plan. If your interest rates are the main problem, compare consolidation and nonprofit credit counseling. If you are already falling behind and cannot realistically repay the full balance, then it may be time to look harder at settlement or even bankruptcy instead of forcing a strategy that clearly is not working.

At a glance: your main options

| Option |

Best for |

Main benefit |

Main drawback |

| DIY payoff plan |

Stable income and enough room in your budget |

No third-party fees |

Requires discipline and consistency |

| Balance transfer |

Good credit and a realistic payoff timeline |

Can reduce interest for a limited period |

Transfer fees and promo periods can catch people off guard |

| Consolidation loan |

Good credit and a lower-rate loan offer |

One fixed payment may be easier to manage |

Can backfire if the rate is not much better |

| Debt management plan |

Mostly credit card debt, need structure and lower rates |

One payment and possible rate concessions |

You are still usually repaying what you owe |

| Debt settlement |

Serious hardship and little chance of full repayment |

May reduce the total balance |

Credit damage, fees, and collection risk |

| Bankruptcy |

Debt is no longer realistically manageable |

Can provide stronger legal relief |

Long-term credit impact and formal legal process |

How much do you need to pay each month?

Before you pick a strategy, I think it helps to make the debt feel concrete. Too many people tell themselves they will “pay it off soon” without doing this basic math.

- 24 months: about $833 per month before interest

- 36 months: about $556 per month before interest

- 48 months: about $417 per month before interest

Those numbers do not include interest, so your real monthly payment may need to be meaningfully higher unless you reduce your rate. In my experience, this is the moment where people either realize they can attack the debt head-on or admit they need a more structured form of help.

Step 1: Stop making the balance worse

Before you worry about the perfect payoff tactic, stop the bleeding first.

- Pause new card spending if at all possible

- Cut subscriptions and recurring charges you forgot about

- Call your card issuer and ask about hardship options or rate reductions

- Build a stripped-down monthly budget based on essentials first

- Set up automatic minimum payments if you are still current

This is not glamorous advice, but it matters. I have seen people spend hours researching debt companies while continuing to use the same maxed-out card for takeout, impulse buys, and little things that add up fast. That usually turns a manageable problem into a much uglier one.

Step 2: Choose the right payoff path

1. A DIY payoff plan

If your income is steady and you can carve out real extra cash every month, this is usually the cheapest route. The two classic methods are:

- Debt avalanche: focus extra money on the highest-interest card first

- Debt snowball: focus extra money on the smallest balance first for faster wins

I generally like the avalanche method more because the math is stronger, but I also know that real life is not a spreadsheet. If you need quick psychological wins to stay motivated, snowball can be a perfectly reasonable choice.

If high inflation has been one of the reasons your monthly budget got squeezed in the first place, our article on how inflation affects personal finances gives useful context.

2. A balance transfer card

A balance transfer can work well if your credit is still in good enough shape to qualify for a strong promotional offer. The idea is simple: move the debt to a card with a temporary low or zero percent intro APR, then pay it down aggressively before the promo period ends.

This option works best for people who:

- still have decent credit

- have not fallen far behind yet

- can realistically pay down a large chunk during the intro window

This option works worst for people who use the breathing room as an excuse to avoid making real progress.

3. A debt consolidation loan

Debt consolidation loans can make sense when you qualify for a lower fixed rate and want one predictable monthly payment instead of juggling multiple cards. But I would be careful here. A consolidation loan is not automatically a win just because it sounds cleaner. If the rate is still high, the fees are meaningful, or the repayment term is stretched too far, the loan may just disguise the problem rather than solve it.

If you want a deeper dive into one corner of this space, we also have a page on debt consolidation lawyers and attorneys.

4. Nonprofit credit counseling and debt management plans

This is the path I think many people overlook. A nonprofit credit counselor can review your budget, explain your options, and sometimes place you into a debt management plan, often called a DMP. That usually means one monthly payment, with the agency sending funds to your creditors. In some cases, creditors may agree to reduce interest rates or waive certain fees.

This can be especially useful when your biggest problem is not reckless spending but high interest combined with a tight budget. I have seen this path make a lot more sense than settlement for people who are still earning income and want to repay what they owe in a more structured way.

If you want to compare one nonprofit-style provider with other approaches, you may also want to read our review of Money Management International.

You can also browse our broader list of best debt relief companies and services if you want to compare multiple categories in one place.

5. Debt settlement

Debt settlement is very different from counseling or consolidation. Instead of repaying the full balance under better terms, settlement aims to negotiate your debt down for less than what you owe. That sounds attractive, and sometimes it is the most realistic path, but it comes with real trade-offs.

- Your credit can take a hit

- You may face collections or lawsuit risk along the way

- Not every creditor will cooperate

- Fees matter, and promises should be viewed carefully

I think settlement makes the most sense when the debt is already becoming unmanageable and full repayment just is not realistic anymore. If you are still comparing providers, you can review our rankings of the best debt settlement companies, or dig into individual reviews like TurboDebt and Accredited Debt Relief.

Feeling stuck between too many options?

Use our quiz to narrow down whether your situation looks more like a consolidation case, a counseling case, a settlement case, or a bankruptcy case.

Find Your Best Debt Option

6. Bankruptcy

Bankruptcy is often the option people fear most, but sometimes it is the one that deserves the most honest attention. If your debt is not just stressful but fundamentally unpayable, dragging things out for another year can do more damage than facing the issue directly. Chapter 7 and Chapter 13 work differently, and the right fit depends on your income, your assets, and your overall financial picture.

If you want to go deeper, read our article on how much debt you need to file Chapter 7 and our guide on whether bankruptcy can clear tax debt.

What I would do in four common situations

You have decent income and are still current

I would usually start with a DIY payoff plan, rate negotiation, and maybe a balance transfer or lower-rate consolidation loan.

You are current, but interest is crushing you

I would look hard at nonprofit credit counseling and debt management plans before I jumped to settlement.

You are behind and cannot catch up

I would stop romanticizing the idea of a perfect payoff plan and compare settlement and bankruptcy more seriously.

You are overwhelmed and frozen

I would focus first on clarity. Frozen people often make expensive decisions because they say yes to the first salesperson who sounds confident.

A practical 7-day action plan

- List every card: balance, APR, minimum payment, and due date.

- Calculate your honest monthly surplus: not your optimistic one, your real one.

- Stop new spending: at least temporarily while you stabilize.

- Call your issuers: ask about hardship support or lower APR options.

- Compare two or three realistic paths: not ten.

- Read the fine print before signing anything.

- Commit to one strategy for the next 60 to 90 days.

Red flags I would avoid

- Anyone promising to erase debt quickly with little downside

- Anyone rushing you before reviewing your actual numbers

- Anyone charging fees before doing the work they claim they will do

- Anyone pretending that settlement, counseling, and consolidation are all basically the same

- Anyone using shame, urgency, or fear to pressure you into signing today

Bottom line

If you are trying to pay off $20,000 in credit card debt, the real question is not whether you should “get serious.” You already know that. The real question is whether your situation calls for discipline, lower interest, structured help, or legal relief.

In my view, people waste the most time when they choose the solution they wish matched their situation instead of the one that actually does. If you still have income and room to move, a strong payoff plan may be enough. If interest is the main villain, a debt management plan or a better-rate loan may do the trick. If your finances are breaking down, settlement or bankruptcy may be the more honest conversation to have.

The smartest move now is not panic. It is clarity.

For added perspective, I also recommend reviewing guidance from the Consumer Financial Protection Bureau on credit counseling, the FTC’s debt payoff guidance, and the U.S. Courts overview of bankruptcy basics.

Frequently asked questions about paying off $20,000 in credit card debt

How long does it take to pay off $20,000 in credit card debt?

That depends on your payment amount, your interest rates, and whether you keep adding to the balance. As a rough principal-only guide, it takes about $833 a month to clear $20,000 in 24 months, about $556 a month over 36 months, and about $417 a month over 48 months. Interest usually raises the real amount you need to pay.

Is $20,000 in credit card debt a lot?

Yes, for most households it is a meaningful amount of unsecured debt. That said, what really matters is your cash flow. For one person, $20,000 may be difficult but manageable. For another, it may already be a crisis.

Should I use debt snowball or debt avalanche?

If you want the strongest mathematical approach, avalanche is usually better because it attacks the highest-interest debt first. If you need motivation and quicker wins, snowball may be easier to stick with. The best strategy is the one you will actually follow consistently.

Can I pay off $20,000 in credit card debt without a settlement company?

Absolutely. Many people do it with budgeting, higher monthly payments, a balance transfer, a lower-rate consolidation loan, or a debt management plan through nonprofit credit counseling. A settlement company is not the default answer.

Is a debt management plan better than debt settlement?

Not always, but they are very different. A debt management plan is usually better for someone who can still repay their debt with structure and possibly lower interest. Debt settlement is typically considered when full repayment is no longer realistic and hardship is more severe.

Will debt consolidation hurt my credit?

It can have some short-term impact, especially if you apply for new credit, but it is often less damaging than missed payments or charge-offs. Long term, a well-managed consolidation strategy may help if it lowers utilization and helps you stay current.

Should I stop paying my cards so I can save up for settlement?

This is a risky move and not something to do casually. Missed payments can damage your credit, lead to fees and collection pressure, and increase legal risk. That choice should only be weighed after you understand the trade-offs clearly.

When should I think seriously about bankruptcy?

If you cannot keep up with minimum payments, your balances are not realistically repayable, and other options look like temporary patches rather than real solutions, bankruptcy may deserve a closer look. For some people, it is a cleaner reset than dragging out a losing battle for years.

What is the smartest first step if I feel overwhelmed?

Write down your balances, APRs, minimum payments, and true monthly surplus. That simple exercise brings clarity fast. Once the numbers are in front of you, the realistic options usually become much easier to spot.

Still not sure what to do next?

Take our internal quiz and get a clearer sense of whether your debt situation points more toward counseling, consolidation, settlement, or bankruptcy.

Start the Debt Relief Quiz

by Amine Rahal | Apr 10, 2026 | Debt Relief

If you’re searching for answers about debt and Chapter 7 bankruptcy, one of the biggest questions on your mind is probably this: how much do you have to be in debt to file Chapter 7? The short answer is simpler than most people expect: there is no official minimum debt amount required to file Chapter 7 bankruptcy. I’ve been writing about debt relief, bankruptcy, consolidation, and settlement for a long time, and this is one of the most common misconceptions I see. A lot of people assume you need to be buried in six figures of debt before Chapter 7 is even on the table. That is not how it works.

Not sure whether Chapter 7 is actually your best move?

Before you assume bankruptcy is the answer, take our quick debt quiz. It can help you compare settlement, consolidation, counseling, and bankruptcy side by side.

Take the Debt Relief Quiz

What really matters is not hitting some magic debt number. What matters is whether you qualify, whether Chapter 7 would actually help, and whether it makes financial sense compared with other options. Over the years, I’ve noticed that people often ask the wrong first question. They ask, “Do I have enough debt?” when the better question is usually, “Is my debt bad enough, and is my income low enough, that Chapter 7 makes sense?”

Do you need a minimum amount of debt to file Chapter 7?

No. There is no fixed minimum debt amount written into the law for Chapter 7. In other words, you do not need to owe $20,000, $50,000, or $100,000 before you are allowed to file. The U.S. Courts explains that, subject to the means test, relief under Chapter 7 is available regardless of the amount of the debtor’s debts. If you want to read the official overview, the U.S. Courts’ Chapter 7 basics page is one of the best starting points.

That said, just because there is no official minimum does not mean filing over a small amount of debt is always a smart move. In real life, most people only consider Chapter 7 when the debt is large enough that repayment feels unrealistic or when collections, lawsuits, garnishment risk, or constant financial stress are making life unmanageable.

So what actually matters more than the debt amount?

In my view, these are the questions that matter more than the raw number:

- Is most of your debt unsecured debt, like credit cards, personal loans, or medical bills?

- Is your income low enough to qualify under the means test?

- Do you own assets that could be at risk in a Chapter 7 case?

- Are you behind on payments with no realistic way to catch up?

- Would another path like settlement, consolidation, or counseling be less damaging?

That is why I rarely like answering this topic with a single number. It is not really a number problem. It is more of a qualification and strategy problem. If you want a broader overview before zeroing in on bankruptcy, our main debt relief guide is a good place to start.

What kinds of debt can Chapter 7 erase?

Chapter 7 is usually best known for wiping out many types of unsecured debt. That can include:

- Credit card debt

- Personal loans

- Medical bills

- Old utility bills

- Certain collection accounts

- Some judgments tied to unsecured debt

That is one reason Chapter 7 comes up so often in conversations about debt settlement and debt relief. A lot of people comparing bankruptcy with negotiated settlement end up looking at pages like our ranking of the best debt settlement companies, our review of National Debt Relief, our review of Accredited Debt Relief, or our review of Beyond Finance because they are trying to figure out whether a negotiated approach is more realistic than a court-based one.

However, Chapter 7 does not erase everything. Some debts are harder or impossible to discharge, such as many student loans, child support, alimony, and some tax debts. The discharge rules themselves are laid out in 11 U.S. Code § 523 and 11 U.S. Code § 727. If taxes are a big part of your problem, you should also read our article on whether bankruptcy clears tax debt.

How much debt is “worth it” for Chapter 7?

This is where personal judgment comes in. Even though there is no minimum debt requirement, filing Chapter 7 over a relatively small debt load may not always be the best move because bankruptcy has consequences. It can affect your credit, stay on your credit report for years, and may not be the right fit if your issue is temporary.

| Debt Level |

Chapter 7 worth considering? |

My general view |

| Under $10,000 |

Sometimes, but less often |

Usually only if income is very low and collections are severe |

| $10,000 to $25,000 |

Possibly |

Can make sense if repayment is unrealistic and other options have failed |

| $25,000 to $50,000 |

Often |

This is where Chapter 7 becomes much more common in my experience |

| $50,000+ |

Very often |

Especially if most of it is unsecured debt and income is limited |

This table is not a legal rule. It is just a practical way to think about when bankruptcy starts to become more understandable as a serious option.

The means test matters more than the debt total

In the U.S., Chapter 7 eligibility often turns on the means test. In plain English, the means test looks at your income and certain allowed expenses to determine whether you qualify for Chapter 7 or whether the filing may be presumed abusive. That is why someone with $20,000 in debt and very low income may be a better Chapter 7 candidate than someone with $60,000 in debt but much higher disposable income.

If your income is above your state’s median for a household of your size, the means test becomes especially important. This is one of the biggest reasons I tell readers not to focus only on debt size. You could owe a lot and still have qualification issues. Or you could owe less than you think is “bankruptcy-worthy” and still be a perfectly reasonable candidate because your cash flow has completely collapsed.

If you are trying to compare bankruptcy with other debt paths, I would also look at our guide to debt consolidation lawyers and attorneys, since some readers are really deciding between a legal route and a negotiated or structured payoff route.

When Chapter 7 tends to make more sense

In my opinion, Chapter 7 becomes much more worth discussing when several of these are true:

- You have mostly unsecured debt

- You are behind and cannot realistically catch up

- Your income is low enough to qualify

- You are facing collection pressure, lawsuits, or garnishment risk

- You do not have many non-exempt assets to protect

- You need a clean reset more than a long repayment plan

That last point is important. Some people need a reset. Others just need structure. Those are not the same thing. If tax liabilities are part of the mix, pages like our guide to tax debt lawyers and attorneys, our review of Tax Relief Advocates, and our review of Five Star Tax Resolution can also help you understand how tax-specific help compares with bankruptcy.

When Chapter 7 may not be the best fit

I do not think Chapter 7 should automatically be treated as the first answer for every debt problem. It may not be the best fit if:

- Your debt load is manageable with a lower-interest payoff strategy

- Your income is too high for Chapter 7 qualification

- Most of your debt is non-dischargeable

- You are trying to protect assets that may be exposed

- A settlement or consolidation path would solve the issue with less long-term fallout

That is why I usually suggest people compare it against other options before making a final decision. For example, someone exploring negotiated settlement might also want to read our reviews of TurboDebt and Debt Clear USA, especially if they are still trying to figure out whether bankruptcy is too aggressive for their situation.

Bankruptcy is not the only option

If you’re unsure whether your debt level really points to Chapter 7, use our quiz before making assumptions. Sometimes the better answer is settlement, consolidation, or counseling instead.

See Your Best Debt Relief Path

What if your debt is small but you still can’t pay it?

This is an important point that people sometimes feel embarrassed about. A debt problem does not have to look huge on paper to feel crushing in real life. A person with $12,000 of debt and almost no disposable income may be in a worse position than someone with $40,000 of debt and a strong salary.

I’ve always thought this is where internet advice can be misleading. People throw around numbers without context. But context is everything. The right question is not whether your debt sounds “big enough” to impress someone online. The right question is whether it is unpayable for you.

If your debt is more state-specific and you want to compare local options, your site also has location-based guides like North Carolina debt relief and Florida debt relief programs, which can help readers think through alternatives in a more localized way.

My bottom line

So, how much do you have to be in debt to file Chapter 7?

There is no minimum debt amount required. You do not need to hit a certain number first. What matters more is whether your debt is truly unmanageable, whether most of it is the kind Chapter 7 can erase, whether your income allows you to qualify, and whether Chapter 7 is smarter than the alternatives.

If you are buried in unsecured debt and cannot see a realistic payoff path, Chapter 7 may absolutely be worth exploring. But I would not choose it based on debt amount alone. I would compare it against every realistic option first, especially if your case is not straightforward.

Still unsure whether your debt level justifies Chapter 7?

Take our quick quiz and get pointed toward the debt relief path that may fit your situation best.

Start the Debt Quiz

Frequently Asked Questions

What is the minimum debt to file Chapter 7?

There is no official minimum debt amount required to file Chapter 7 bankruptcy. The bigger issues are eligibility, the type of debt you have, and whether Chapter 7 makes practical sense for your situation.

Can I file Chapter 7 with only $10,000 in debt?

Possibly, yes. There is no rule stopping you based on that number alone. But whether it is worth filing depends on your income, other options, legal costs, and whether the debt is truly unmanageable.

Do I need six figures of debt to qualify for Chapter 7?

No. You do not need to be in massive debt to qualify. There is no six-figure requirement. What matters more is your ability to repay and whether you pass the means test.

Is income more important than debt amount for Chapter 7?

In many cases, yes. Income is a major factor because Chapter 7 often depends on passing the means test. A lower-income filer with moderate debt may be a stronger candidate than a higher-income filer with more debt.

What debt does Chapter 7 usually wipe out?

Chapter 7 commonly wipes out unsecured debts such as credit card debt, personal loans, medical bills, and collection accounts. Some debts, such as many student loans, child support, and certain taxes, are much harder to discharge.

Is Chapter 7 better than debt settlement?

It depends on the case. Chapter 7 can be more final and powerful for someone who truly cannot repay, while debt settlement may make more sense for someone who wants to avoid bankruptcy and has enough income to fund negotiated settlements.

Can Chapter 7 stop debt collectors and lawsuits?

Filing Chapter 7 usually triggers an automatic stay, which can pause many collection actions. That can be one of the biggest immediate benefits for people facing intense creditor pressure.

by Amine Rahal | Apr 10, 2026 | Debt Relief

When readers ask me, “Does bankruptcy clear tax debt?”, my honest answer is: sometimes, yes, but only in specific situations. I’ve been writing about debt relief, tax debt, settlement, consolidation, and bankruptcy-related topics for a long time, and one mistake I see over and over is people assuming all IRS debt gets wiped out the same way credit card debt might. It’s not always the case. Tax debt follows its own rules, and the timing matters a lot.

Not sure whether bankruptcy is the best path for your tax debt?

Take our quick debt quiz first. It’s one of the fastest ways to narrow down which direction may make the most sense before you spend hours researching the wrong solution.

Take the Debt Relief Quiz

In general, bankruptcy can erase some older income tax debt, but it usually does not wipe out every kind of tax bill. If the debt is too recent, tied to payroll taxes, connected to fraud, or based on late or unfiled returns, the odds get much worse. The IRS bankruptcy guidance, IRS Publication 908, and the bankruptcy priority rules under 11 U.S. Code § 507 all point in the same direction: some tax debt can be discharged, but only if the facts line up.

My quick answer

If you want the short version, here it is:

- Yes, bankruptcy may clear some tax debt

- No, it does not automatically clear all tax debt

- Older income tax debt has the best chance

- Recent tax debt, payroll tax debt, and fraudulent tax debt usually survive

I’ve seen people wait too long to get help because they assumed “nothing can be done” with IRS debt. I’ve also seen people rush toward bankruptcy thinking it would magically clean everything up, only to learn later that the tax debt they cared most about would still be there. That is why I think this is one of the most important debt topics to understand properly before you file anything.

When bankruptcy may clear tax debt

In the U.S., bankruptcy is usually most helpful for older income tax debt. A lot of professionals refer to this informally as the 3-2-240 rule. It is a shortcut way of thinking about whether a tax debt might be dischargeable.

| Rule |

What it usually means |

Why it matters |

| 3-year rule |

The tax return due date was at least 3 years before the bankruptcy filing |

Recent tax debt usually gets priority treatment and is harder to discharge |

| 2-year rule |

You filed the tax return at least 2 years before filing bankruptcy |

Late-filed returns can create major problems |

| 240-day rule |

The tax was assessed at least 240 days before the filing date |

A recent assessment can prevent discharge |

Even if those timing rules look good, the debt still generally needs to be income tax debt, not payroll tax debt or a fraud-related obligation. On top of that, things can get more complicated if you had an offer in compromise, a prior bankruptcy, or other events that can affect the clock.

Tax debts that usually do not get wiped out

This is where I think readers need to be especially careful. Bankruptcy is not a universal eraser for every tax problem. It usually does not clear:

- Recent income tax debt

- Payroll tax debt and trust fund taxes

- Tax debt linked to fraudulent returns

- Tax debt tied to willful tax evasion

- Some debt from late or unfiled returns

- Post-petition tax liabilities

If your debt is mostly credit cards, personal loans, or collections, you may also want to compare this question against our broader guide to debt relief options in America. A lot of people assume “tax debt problem” and “overall debt problem” are the same thing, but they often are not.

Chapter 7 vs. Chapter 13 for tax debt

One thing I’ve noticed over the years is that people talk about “bankruptcy” as if it were one single strategy. It isn’t. The chapter matters.

Chapter 7

Chapter 7 bankruptcy is the form most people think of when they imagine wiping out debt and getting a fresh start. For tax debt, Chapter 7 can sometimes discharge older qualifying income taxes. But it is not automatic, and not every filer qualifies for Chapter 7 in the first place.

If someone has old income tax debt that checks the right boxes, Chapter 7 may be the more direct route. But if the debt is newer, partially priority debt, or part of a larger cash-flow problem, Chapter 13 may be more realistic.

Chapter 13

Chapter 13 works more like a court-supervised repayment plan. In my view, it can be more useful for people who need time and protection rather than a full wipeout. Some tax debt may still be paid through the plan, while some older qualifying debt may eventually be discharged.

That is one reason I often tell readers not to focus only on “Can I erase this?” Sometimes the better question is, “Can I stop the pressure, stay protected, and create a payment structure I can actually survive?”

Does bankruptcy stop IRS collections?

Usually, filing bankruptcy triggers an automatic stay, which can temporarily stop many collection actions. That can include collection pressure from the IRS. But this does not mean the tax debt is permanently gone. It just means the collection activity may pause while the bankruptcy case moves forward.

If your main goal is breathing room, that pause can be meaningful. If your main goal is full elimination of the tax balance, then you need to look much more closely at the exact age and type of the tax debt.

Before you jump into bankruptcy, compare your options

If you are also dealing with unsecured debt like credit cards, medical bills, or personal loans, take our quiz first. In some cases, bankruptcy is the right move. In other cases, a different route may be more practical.

Compare Your Debt Relief Options

What about state tax debt?

State tax debt can also be affected by bankruptcy, but the exact treatment can vary, and state collection practices can be different. I would be very careful about assuming the IRS rules tell the full story for state income tax departments. The broad framework may be similar, but local details matter.

If your tax problem is more specialized and you are trying to understand tax-resolution-style help instead of consumer debt relief, you may also want to read our reviews of Tax Relief Advocates and Five Star Tax Resolution. They are not substitutes for legal advice, but they can help you understand how the tax relief side of the market works.

A simple example

Let’s say someone owes federal income taxes for a return that was due more than 3 years ago. They filed the return more than 2 years ago. The IRS assessed the tax more than 240 days ago. There was no fraud, and no willful evasion.

That person may have a path to discharge that debt in bankruptcy.

Now let’s change one detail. Maybe they filed the return late. Maybe the tax was assessed recently. Maybe the debt is for payroll taxes. Maybe the tax year is too recent. Suddenly, the answer can flip from “possibly dischargeable” to “probably not.”

That is why I never like ultra-simplified headlines on this topic. They may get clicks, but they can mislead people badly.

When I think bankruptcy is worth discussing seriously

In my opinion, bankruptcy becomes much more worth discussing when some or all of the following are true:

- You cannot realistically repay the debt in a reasonable timeframe

- The tax debt is old enough that discharge may be possible

- You are also carrying large unsecured debts on top of the tax balance

- Collections are becoming aggressive

- You need court protection and a real reset, not just another temporary arrangement

On the other hand, if the tax debt is recent and your income is stable, bankruptcy may not be the first place I would look. In that case, you may want to compare other options too, including our guide to the best debt settlement companies and our review of debt consolidation lawyers and attorneys, especially if you are trying to weigh legal help against non-legal debt relief programs.

My bottom line

So, does bankruptcy clear tax debt?

Yes, sometimes. But usually only certain older income tax debts that meet strict timing and filing rules. It is much less likely to wipe out recent tax debt, payroll taxes, or tax debt linked to fraud, evasion, or filing issues.

If you are overwhelmed and not sure where your case falls, I honestly think the smartest first step is not guessing. Map out the type of debt, the tax years involved, when the returns were filed, and whether the debt is really tax debt only or part of a bigger consumer debt problem. Once you do that, the right next step gets much easier to see.

Still unsure what to do next?

Use our debt quiz to compare bankruptcy, settlement, consolidation, and other common paths based on your situation.

Start the Debt Quiz

Frequently Asked Questions

Can Chapter 7 wipe out IRS tax debt?

Sometimes. Chapter 7 may discharge certain older income tax debts, but not every IRS debt qualifies. Timing, filing history, and the type of tax all matter.

Does bankruptcy clear payroll tax debt?

Usually no. Payroll taxes and trust fund taxes are generally much harder, and often impossible, to discharge in bankruptcy.

What is the 3-2-240 rule for tax debt in bankruptcy?

It is a shorthand way to evaluate whether some older income tax debt may be dischargeable. Broadly, the return due date usually needs to be at least 3 years old, the return needs to have been filed at least 2 years before bankruptcy, and the tax generally must have been assessed at least 240 days before filing.

If I filed my tax return late, can bankruptcy still clear the debt?

Maybe, but late filing can create serious problems. In some cases, a late-filed return can prevent discharge entirely. This is one of the biggest reasons I think people should review the timeline carefully before filing.

Does bankruptcy stop the IRS from collecting right away?

It often triggers an automatic stay that pauses many collection actions, at least temporarily. But that does not mean the tax debt disappears forever. The question of discharge is separate.

Is tax debt forgiven after bankruptcy taxable?

In general, debt canceled in bankruptcy is not treated as taxable income the way ordinary canceled debt can be. That said, tax consequences can still be technical, so it is smart to review your full situation with a qualified professional.

Should I file bankruptcy just because I owe the IRS?

Not automatically. I would first look at the age and type of the tax debt, whether you are current on filing, what other debts you have, and whether bankruptcy is solving the actual problem or just part of it. For many people, the right answer only becomes clear after comparing a few legitimate paths side by side.

by Amine Rahal | Mar 23, 2026 | Debt Relief

TurboDebt (sometimes written as Turbo Debt) is a U.S. debt relief brand that helps consumers explore options for tackling unsecured debt (like credit cards, personal loans, medical bills, and collections). The key thing to understand up front is that TurboDebt often acts as a connector that matches you with a debt relief program that fits your situation, rather than always being the company that negotiates directly with your creditors.

TurboDebt (sometimes written as Turbo Debt) is a U.S. debt relief brand that helps consumers explore options for tackling unsecured debt (like credit cards, personal loans, medical bills, and collections). The key thing to understand up front is that TurboDebt often acts as a connector that matches you with a debt relief program that fits your situation, rather than always being the company that negotiates directly with your creditors.

PS: Want a fast, personalized starting point before you call anyone? Take our quick quiz here: Debt Relief Quiz (settlement vs consolidation vs bankruptcy).

Are you sure TurboDebt is right for you?

Debt settlement has its downsides! Don’t jump in without comparing different options. Take our quick Debt Relief Quiz to get a better sense of whether debt settlement, consolidation, counselling or bankruptcy may be the smarter direction for your situation.

Why start with the quiz

- Helps narrow down your best-fit option

- Useful if you are torn between multiple debt solutions

- Fast, simple, and more personalized than guessing

Quick reminder

- Every debt situation is different

- The right option depends on your budget, goals, and urgency

- Use the quiz as a smart starting point before committing

TurboDebt company snapshot (updated for 2026)

- Company: TurboDebt, LLC

- Website: TurboDebt.com

- Headquarters (published on TurboDebt site): 1643 NW 136th Ave, Building H, Sunrise, FL 33323

- Email (published on TurboDebt site): contact@turbodebt.com

- Availability: TurboDebt states it does not offer services in CT, MN, OR, VT, WV, and WI. Always confirm availability from their “Areas We Serve” page before you spend time on an application.

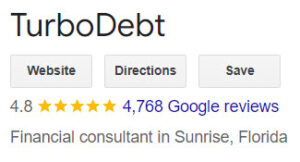

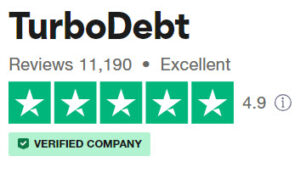

Legitimacy, ratings & reviews (2026 update)

Below is a current snapshot of third-party ratings. These numbers can change over time, so consider them a “temperature check,” not a guarantee of your experience.

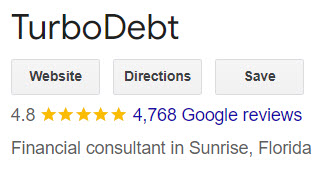

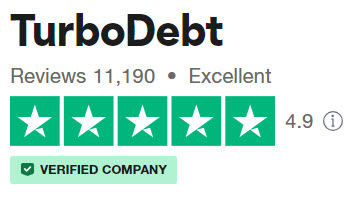

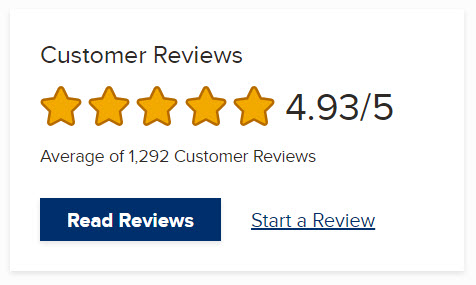

TurboDebt

- BBB: A+ rating; customer reviews about ★ 4.87/5 (1,300+ reviews)

- Trustpilot: ★ 4.9/5 (14,000+ reviews)

What TurboDebt actually does (and the question you should ask)

TurboDebt describes itself as a service that connects clients to debt relief programs. In practice, that can mean your case may be handled by a partner program (example partners listed publicly include National Debt Relief and others). That isn’t automatically “bad,” but it changes what you should ask on your first call:

- Who will be the actual program provider negotiating with my creditors?

- What is the total cost (program fees + any dedicated account fees), and when do those costs get charged?

- Will I be asked to stop paying creditors during the program, and what happens if a creditor sues?

- How will you communicate settlement offers, and do I have to approve each settlement?

How debt settlement usually works (plain English)

- Free consultation: you share your debts, budget, and hardship.

- Program fit: if settlement is recommended, you’ll typically open a dedicated account to build funds for offers.

- Negotiations: once enough funds accumulate, settlements are negotiated one debt at a time.

- Fees: reputable providers generally cannot charge “advance fees” before results (make sure you understand fee timing).

- Finish line: the goal is to resolve each enrolled debt and close the program.

If you’re new to this, two excellent government resources to read first are the FTC’s overview of getting out of debt and the CFPB’s explanation of debt relief programs. Also be aware that canceled debt can sometimes trigger tax forms (like a 1099-C), depending on your situation.

TurboDebt Pros 👍

- Massive review footprint: TurboDebt has a very large volume of consumer reviews across major platforms, which is useful for due diligence.

- Clear “shopping” entry point: If you’re not sure which option fits (settlement vs counseling vs consolidation), TurboDebt can be a starting conversation.

- Availability in most states: While not nationwide, it is available in many U.S. states (confirm via their service area page).

TurboDebt Cons 👎

- Potential “middle layer”: Because TurboDebt can act as a connector, you must confirm who the actual program provider is and what their policies are.

- Costs can be significant: Debt settlement fees are often a percentage of enrolled debt, and you may also pay account fees depending on the setup.

- Credit impact risk: Many settlement programs involve missed payments, which can hurt credit and increase collection pressure before resolution.

Not sure whether settlement, consolidation, or bankruptcy makes more sense?

Before you commit to any company or program, take our quick quiz. It can help you figure out which debt relief path may fit your situation best.

Take the debt relief quiz

What types of debt can these programs usually help with?

Most debt settlement programs focus on unsecured debts, for example:

- Credit card balances

- Personal loans

- Medical bills

- Collections

- Some private unsecured lines of credit

They typically do not “settle” secured debts in the usual way (like mortgages or auto loans) because those are tied to collateral. Student loans and tax debts have their own rules and may require different specialists.

Who TurboDebt might be best for (and who should look elsewhere)

- Better fit: You want to explore options, you have meaningful unsecured debt, and you can commit to a structured payoff plan.

- Probably not a fit: Your debt is mostly secured (mortgage/auto), you’re current on everything and just want a lower interest rate, or you need legal protection quickly (in that case, speaking with a bankruptcy attorney may be smarter).

Other reputable options to compare

Even if you like what you hear from TurboDebt, I would still compare a few other providers before making any decision. Debt relief is not one-size-fits-all. Some companies are better for straightforward unsecured debt, some are stronger for tax debt, and some may be a better fit if you want a more legal-heavy approach.

Here are several alternatives you can review on our site:

- CuraDebt review – a well-known name that can be worth a look if you want to compare a more established debt relief brand.

- Oak View Law Group review – a useful option to compare if you prefer a law-firm-style approach or want help with more complex debt situations.

- JG Wentworth Debt Relief review – worth reviewing if you want to compare another major brand with broad consumer awareness.

- National Debt Relief review – one of the biggest names in the space, and a smart benchmark when comparing fees, process, and reputation.

- Freedom Debt Relief review – another large provider that is useful to compare if you want to see how a major national company stacks up.

- Pacific Debt Relief review – a good one to look at if your focus is mainly unsecured debt like credit cards, loans, collections, or medical bills.

- Accredited Debt Relief review – worth comparing if you want to look at a provider that may offer both settlement and consolidation-style options through partners.

- CreditAssociates review – another option to compare if you want a broader sense of how different programs structure their process and fees.

If you want a broader shortlist instead of reviewing companies one by one, here is our full rankings page: Best debt settlement companies ranked by ratings & reviews.

And if you are still not sure whether debt settlement is even the right route for you, I would take our Debt Relief Quiz before speaking with any company. It can help you think through whether settlement, consolidation, or even bankruptcy may be the better fit for your situation.

Bottom line (Our conclusion for 2026)

TurboDebt appears legitimate and has strong public ratings. The main “watch-out” is clarity: confirm who will actually manage your program, get the total fee schedule in writing, and make sure you’re comfortable with the timeline and credit impact.

Ready to see which debt relief option may fit you best?

Take our quick debt relief quiz to compare paths like settlement, consolidation, and bankruptcy before you decide what to do next.

Frequently asked questions

Will debt settlement hurt my credit?

It can. Many settlement programs involve missed payments before debts are resolved, which can damage credit scores and increase collection activity. If protecting credit is your top priority, ask about alternatives like a nonprofit debt management plan (DMP) or consolidation.

Can creditors sue me while I’m in a program?

Yes, it’s possible. Not every creditor agrees to settle, and some may pursue collections or lawsuits depending on the balance, timeline, and creditor policies. Ask how your provider handles lawsuits and whether they offer any support or referrals.

How long does debt settlement usually take?

It depends on how much you owe and how much you can set aside each month. Many programs are marketed in multi-year timeframes. The realistic way to judge it is simple: how fast you can build funds for settlement offers.

Are there tax consequences if a debt is forgiven?

Sometimes. If a creditor forgives part of your debt, you may receive a tax form and the forgiven amount may be treated as income, depending on your situation. If you’re close to enrolling, consider checking with a tax pro so you’re not surprised later.

What fees should I expect?

Ask for a complete fee schedule in writing. The big variables are (1) the program fee (often a percentage of enrolled debt), (2) whether the fee is based on enrolled debt or settled debt, and (3) whether there are monthly dedicated-account fees.

What questions should I ask on the first call?

Ask who the actual program provider is, whether you’ll be advised to stop paying creditors, the total cost including any account fees, whether you approve each settlement, and what happens if a creditor refuses to negotiate.

Is a nonprofit debt management plan (DMP) safer?

A DMP can be a good option if your main issue is high interest rates and you can afford to repay the principal over time. It’s not debt settlement, but it may reduce interest and create one structured payment. It’s worth comparing before you commit to settlement.

What if I’m considering bankruptcy?

Bankruptcy can offer stronger legal protections and may be the right move in some situations. If you’re behind, facing lawsuits, or simply can’t make progress, it can be worth speaking with a bankruptcy attorney for an initial consult.

by Brandi Marcene | Mar 9, 2026 | Debt Relief

North Carolina combines both relatively low living costs and an ongoing influx of people moving in from other parts of the country. While average housing costs, food costs, utility bills, and everyday living expenses can still come in below those of many other states, that does not mean residents are immune to financial pressure and high debt.

Not sure which debt relief option fits your situation?

Take our quick quiz to compare debt settlement, consolidation, nonprofit programs, and bankruptcy in a more practical, side-by-side way.

Take the Debt Relief Quiz

In larger metro areas like Charlotte, Raleigh, and Durham, many households are now dealing with expensive rental markets, rising home prices, and broader increases in day-to-day expenses. For some families, the gap between income and the true cost of living has become harder to absorb than it used to be.

At the same time, many North Carolinians are trying to manage unsecured debts such as credit cards, medical bills, and personal loans. When those balances start piling up while living costs continue to rise, even people with steady income can begin to feel stuck.

Because of this, there are now more options than ever for people seeking debt relief in North Carolina. These may include credit counseling, debt management plans, debt consolidation, debt settlement, and in some cases legal discharge through bankruptcy. If you want a broader national overview before choosing a path, you can also explore our guide to debt relief options across the U.S., which provides a helpful starting point.

Common debt types

Credit cards, medical bills, personal loans, and other unsecured balances are among the most common issues people are trying to resolve.

Why people fall behind

Rising rent, higher housing costs, and inflation can quickly make minimum payments harder to manage month after month.

Main relief paths

Counseling, DMPs, consolidation, settlement, and bankruptcy each fit different levels of financial stress and repayment ability.

What Debt Relief Looks Like in North Carolina

Credit Counseling and Budget Review — A Low-Risk First Step

When debt feels overwhelming and you want to avoid taking drastic action, nonprofit credit counseling is often one of the safest places to begin. A counselor may be able to analyze your debts, review your income and monthly expenses, help create a workable budget, and recommend a repayment strategy for you to consider.

In North Carolina, many agencies offer these services statewide and often provide support online or by phone. For people who still have income coming in and mainly need structure, education, and a realistic game plan, this can be a smart first step.

Debt Management Plans (DMPs) — Simplifying Payments Over Time

A debt management plan gathers certain unsecured debts into one monthly payment, most often credit card balances. In some cases, creditors may agree to reduce interest rates or waive certain fees, which can make repayment more manageable over time.

For North Carolinians with stable income who are falling behind mainly because of interest charges and too many separate accounts, a DMP can offer structure without requiring a brand new loan. It usually works best for people who still have the ability to repay what they owe, but need a simpler system and more breathing room.

Debt Consolidation Loans — One Loan Instead of Many Payments

If you qualify for a reasonable personal loan rate, often through a credit union, bank, or online lender, consolidating several debts into one loan may lower your overall interest cost and make your finances easier to manage.

This path tends to work best for people whose credit has not already deteriorated too badly and who can stay disciplined with repayment. The key is that the new loan truly needs to improve your situation.

If the new rate is not clearly lower than what you are already paying, or the repayment term ends up increasing your total cost, consolidation may only rearrange the problem instead of solving it. If you are looking more closely at this category, you may also want to review our guide to the top debt consolidation lawyers and attorneys.

Debt Settlement — Negotiating Down What You Owe

For people carrying significant unsecured debt and struggling to keep up with minimum payments, debt settlement can sometimes offer meaningful relief. The goal is to negotiate with creditors so they accept less than the full amount owed.

That said, this approach has to be handled carefully in North Carolina. Residents should be very cautious of companies asking for large upfront fees. Settlement services are generally expected to be performance-based, which means fees should only be earned after actual progress is made.

There are also real trade-offs to understand. Accounts may become delinquent while negotiations are taking place, which can hurt your credit score. Collection efforts may continue during the process, and depending on the amount forgiven, there may sometimes be tax consequences as well.

If you want to compare providers that operate in this space, see our ranked guide to the best debt settlement companies. If you want a deeper look at our top-ranked option, you can also read our full New Era Debt Solutions review.

Short-Term Tools: Balance Transfers and Promotional Offers

If you have good credit and a smaller balance, a 0% balance transfer card or short-term promotional loan can buy you some time to pay debt down faster. In the right case, this can absolutely help.

Still, it usually works best as a short-term tool rather than a full debt relief strategy. For people dealing with larger balances or longer-term hardship, it often just moves debt around without reducing it in a meaningful way.

Bankruptcy — Legal Relief When No Other Option Feels Viable

When an individual is dealing with unsustainable debt, especially if lawsuits, wage garnishment, repossession threats, or foreclosure concerns are part of the picture, bankruptcy may need to be part of the conversation. In most personal cases, that means looking at Chapter 7 or Chapter 13.

For some North Carolinians, bankruptcy can discharge a large portion of unsecured debt and create a genuine reset. For others, it may not be necessary if a less severe option can still work.

Because exemptions, asset protections, eligibility rules, and case strategy can vary, it is generally wise to speak with a qualified attorney or legal aid resource before filing.

Top North Carolina Debt Relief Companies and Services

Best for: Larger unsecured debt balances

Fees: No upfront fees; performance-based model

Coverage: Nationwide, including North Carolina

More info: Read our full review

Money Management International (MMI)

Best for: Nonprofit counseling and debt management plans

Fees: Often free consultation or modest enrollment fees

Coverage: Nationwide, serving North Carolina

Freedom Debt Relief

Best for: Larger settlement cases

Fees: Performance-based fees

Coverage: Nationwide, including North Carolina

National Debt Relief

Best for: Large-scale debt settlement

Fees: Performance-based fees

Coverage: Nationwide, including North Carolina

More info: Read our review

InCharge Debt Solutions

Best for: Counseling and structured repayment help

Fees: Free consultation; monthly fees may apply for plans

Coverage: Nationwide, including North Carolina

North Carolina Debt Relief Company Highlights

New Era mainly focuses on negotiating unsecured debts and tends to be most relevant for people dealing with larger balances. North Carolina residents looking into settlement without major upfront costs often compare it early in their research.

Money Management International (MMI)

MMI is a nonprofit option focused on credit counseling and debt management plans. It may be a better fit for North Carolinians who still have stable income and want a structured way to repay debt rather than settle it.

Freedom Debt Relief