Not sure a debt management plan is your best move? Nonprofit counseling like MMI works brilliantly for some situations and not at all for others. Our free quiz compares DMPs, settlement, consolidation and bankruptcy against your actual numbers.

Take the Free Debt Relief Quiz

Company Snapshot

- Official Name: Money Management International (MMI)

- Official Website: www.moneymanagement.org

- Headquarters: Stafford, Texas

- Founded: 1997 (merging prior credit counseling groups dating back to 1958)

- Type: 501(c)(3) Nonprofit

- Service Area: Nationwide online; in-person branches in ~25 states, over 100 physical locations

Legitimacy, Ratings & Reviews

MMI is a highly reputable nonprofit credit counseling organization with multiple accreditations and top marks for transparency and client satisfaction.

- BBB Rating: A+, BBB accredited since 1994

- TrustPilot: 4.9 to 4.8 out of 5 (Thousands of positive reviews)

- Forbes/Bankrate Score: Highly rated for nonprofit counseling and debt management plans

- Certifications: NFCC, FCAA, HUD-approved, COA accredited

Clients often praise MMI’s helpful staff, clear advice, flexible payment structures, and educational support.

Services Offered by MMI

- Debt Management Plans (DMPs): Consolidated monthly payment to MMI, which negotiates lower interest rates and elimination of late fees with creditors.

- Debt Resolution Plans: Similar to settlement plans, MMI negotiates lump settlements, and refunds are available if unsatisfied

- Credit Counseling & Credit Report Review: Free one-on-one advice and analysis of credit reports.

- Specialized Counseling: Services for student loans, bankruptcy, disaster recovery, homebuying, reverse mortgage, military families. Fees vary or may be free.

- Financial Education & Tools: Workshops, webinars, podcasts, budgeting tools, and more.

Pros 👍

- Nonprofit with high trust: No motive to upsell, focus on consumer benefits.

- Low, transparent fees: For DMPs, setup ranges $33–$75; monthly fees $25–$59.

- Helps reduce interest, not just restructure debt: Clients may save significantly over time.

- Wide range of services: Beyond debt, includes housing, student loans, disaster counseling.

Cons 👎

- Does not reduce principal: You still pay all your debt, albeit at lower interest.

- Long program duration: DMPs typically last 3 to 5 years. :contentReference

- Limited in-person branches: Brick-and-mortar locations exist in about 25 states only.

Debt Types They Can Help With

MMI primarily assists with unsecured debts, including:

- Credit Card Debt

- Medical Bills

- Personal Loans

- Collections

They do not cover secured loans, federal student loans, or IRS obligations under standard programs, though they do offer some student loan counseling and specialized foreclosure/bankruptcy counseling.

Final Thoughts

Money Management International stands out as a trusted nonprofit offering affordable, structured debt support. They are a smart starting point if you want to repay your debt in full with lower interest and comprehensive guidance. If, however, you are looking for a settlement option where you pay less than you owe with no upfront fees, then we recommend

Comparing your options? We ranked 24 debt relief companies side by side, nonprofits and settlement firms alike, with fees, minimums and ratings for each.

See All 24 Companies Ranked

Frequently Asked Questions About Money Management International

1. Is Money Management International a legitimate company?

Yes, they are. In my research, I found that MMI is one of the largest nonprofit credit counseling agencies in the United States. They have been around in some form since the 1950s and officially became Money Management International in 1997 after several nonprofit agencies merged. They are accredited by the National Foundation for Credit Counseling (NFCC) and approved by the Department of Housing and Urban Development for housing counseling. That credibility matters a lot when you are looking for trustworthy help with debt.

2. How does MMI’s debt management program work?

The process is fairly straightforward. You begin with a free consultation where a counselor reviews your income, expenses, and debts. If you qualify, they may recommend a debt management plan. With a DMP, you make one monthly payment to MMI and they send those funds to your creditors. In most cases, they are able to secure lower interest rates and get late fees waived. You still pay back everything you owe, but under more manageable terms. Most programs run between three and five years.

3. How much does it cost to enroll in a debt management plan with MMI?

Fees vary by state regulations, but generally there is a one-time setup fee between $33 and $75 and a monthly fee between $25 and $59. Because MMI is a nonprofit, these fees are modest compared to what for-profit companies charge. They also sometimes reduce or waive fees for people with financial hardship. I like that their pricing is very transparent compared to some competitors.

4. What kinds of debt does MMI help with?

MMI mainly focuses on unsecured consumer debts. This includes credit cards, medical bills, personal loans, and accounts in collections. They also provide counseling for student loans, though they do not consolidate federal loans into their DMPs. They will not be able to help you with secured debts like mortgages or auto loans, and they do not provide relief for IRS tax debt.

5. Will enrolling with MMI hurt my credit score?

This is a common question. In my experience reviewing credit counseling agencies, enrolling in a DMP can cause a short-term dip in your credit score, mainly because some creditors will mark accounts as “managed by a credit counseling agency.” However, since you continue paying down your balances, your score often improves over time. I have seen people finish a program in a stronger position than when they started. The key is that unlike settlement companies, MMI helps you pay off your debt in full, which usually leaves a better long-term credit profile.

6. How is MMI different from debt settlement companies?

The main difference is that MMI does not try to reduce your principal balance. Settlement companies will negotiate with creditors to accept less than you owe, often requiring you to stop payments to build leverage. That approach can save you money but can also damage your credit in the short term. MMI, on the other hand, focuses on lowering interest and fees so you can pay off your debt in full. I see them as more of a safe and steady option, while settlement can be more aggressive and risky.

7. Is MMI available nationwide?

Yes, their counseling services are available across the United States online or by phone. They also have physical branch offices in about 25 states, with over 100 locations in total. This is a plus if you prefer face-to-face counseling. I found that even people in states without branches can still work with them through remote counseling.

8. How long will it take to complete a program with MMI?

Most debt management plans last between three and five years. The exact timeline depends on how much debt you have and how much you can pay each month. From what I have seen, people who commit to the program and make consistent payments often finish faster than expected. The structure of the plan makes it easier to stay on track compared to juggling multiple bills on your own.

9. What do clients say about MMI?

When I looked at reviews across BBB, TrustPilot, and other platforms, I noticed a lot of praise for the professionalism of the counselors and the sense of relief people feel after enrolling. Clients often mention lower interest rates, reduced stress, and steady progress toward being debt free. A smaller number of negative reviews tend to focus on the length of the programs or the fact that you still pay back the full balance, which some consumers may not expect if they were hoping for a settlement-style discount.

10. Is MMI the best option for debt relief?

I would say it depends on your situation. If you are committed to repaying what you owe and you want a nonprofit organization that focuses on education and affordable repayment, MMI is a strong option. Whatever you choose, compare at least two providers from our rankings first. Both approaches have their place, but they serve different needs.

Money Management International FAQ

Is Money Management International legit?

Very much so. MMI is a 501(c)(3) nonprofit with roughly 60 years of history, membership in the NFCC and FCAA, Council on Accreditation approval, and HUD certification for housing counseling. It is one of the largest nonprofit counseling agencies in the country.

How much does MMI charge?

Most counseling and education is free. Debt management plans carry modest setup and monthly fees that vary by state, and MMI notes that reduced or waived fees are available for qualifying clients. You will get exact figures in your free initial session.

Is MMI a debt settlement company?

No, and that matters. MMI is a nonprofit credit counselor: on a debt management plan you repay everything you owe at reduced interest rates. Settlement companies negotiate to pay less than you owe, with heavier credit damage and fees. Different tools for different situations.

Will an MMI debt management plan hurt my credit?

Far less than settlement. Accounts are typically closed when they enter the plan, which can ding your score at first, but consistent on-time plan payments usually rebuild credit during the 3 to 5 year program.

What if a DMP is not enough for my debt?

If your budget cannot cover full repayment even at reduced rates, look at settlement or bankruptcy. Take our free quiz to compare all four paths against your numbers, or browse our rankings of 24 debt relief companies.

![Take Charge America: We Review This Nonprofit Credit Counseling Agency [2026 Update]](https://cpiinflationcalculator.com/wp-content/uploads/2025/02/TakeChargeAmericaHomepage-1080x675.jpg)

by Amine Rahal | Jul 29, 2026 | Debt Relief Wondering if Take Charge America is a good option for debt settlement or debt relief? In this review of the company, we’ll look at their reviews and ratings from across the web, and we’ll break down their services when it comes to managing and decreasing debt.

Wondering if credit counseling is your best move? Nonprofits like Take Charge America shine for some situations and fall short for others. Our free quiz compares counseling, settlement, consolidation and bankruptcy against your actual numbers.

Take the Free Debt Relief Quiz

Who is Take Charge America?

Take Charge America (TCA) is a nonprofit credit counseling agency that provides debt management, financial education, and housing counseling services. Founded in 1987, TCA has helped thousands of individuals regain financial stability through structured debt relief programs and personalized financial counseling.

- Headquarters: Phoenix, Arizona

- States Covered: Nationwide (Available in most U.S. states)

- Founded in: 1987

- Website: www.takechargeamerica.org

- Phone: 1-866-750-9634

Services Offered:

- Free Credit Counseling

- Debt Management Plans (DMPs)

- Budget Planning & Financial Education

- Housing Counseling (HUD-approved)

- Student Loan Counseling

- Bankruptcy Counseling

February 2025 Update: As per a recent press release, Take Charge America has expanded its free housing counseling and mortgage assistance services to California, thanks to a $250,500 grant from the California Housing Finance Agency (CalHFA). This initiative allows the nonprofit agency to provide confidential support to homeowners and renters struggling with delinquency, foreclosure risk, or navigating the homebuying process. The services include rental and mortgage delinquency assistance, reverse mortgage counseling, pre-purchase and post-purchase guidance, and rental counseling for first-time or low-income renters. As a nonprofit, Take Charge America remains committed to offering free, unbiased advice tailored to each client’s financial situation. Residents can schedule a virtual appointment by visiting TakeChargeAmerica.org or calling (866) 987-2008.

Minimum Requirements to Qualify:

- Minimum Debt: No strict minimum, but best suited for those with $5,000+ in unsecured debt

- Income Minimum: Must have verifiable income to support a repayment plan

Visit Take Charge America →

Take Charge America Ratings & Reviews:

Take Charge America is known for its commitment to consumer financial education, transparent practices, and effective debt relief solutions. Here’s how they are rated across major platforms:

- BBB Rating: A+ (Accredited Business)

- BBB Reviews: 4.7/5 Stars

- Trustpilot: 4.8/5 Stars

- Google Reviews: 4.6/5 Stars

- Consumer Affairs: 4.5/5 Stars

- Investopedia Rating: 4.3/5 Stars

- Accreditations: Member of the National Foundation for Credit Counseling (NFCC), HUD-approved housing counseling agency

Key Features & Benefits:

1. Free Credit Counseling

Take Charge America provides a free, confidential financial review to help clients explore available debt relief options and develop a customized financial plan.

2. Debt Management Plans (DMPs)

- TCA works with creditors to reduce interest rates and eliminate late fees.

- Clients make one consolidated monthly payment to TCA, which is then distributed to creditors.

- Most DMPs last 36 to 60 months, depending on the debt amount.

3. Nonprofit & Transparent Fee Structure

- As a nonprofit agency, TCA offers low-cost solutions with fees regulated by state laws.

- Fees typically range from $0 to $50 for enrollment and $25 to $75 monthly.

4. Housing & Bankruptcy Counseling

- Provides HUD-approved housing counseling for mortgage assistance and foreclosure prevention.

- Offers pre-bankruptcy counseling and debtor education, as required by federal law.

5. Financial Education & Resources

- Free online courses, budgeting guides, and financial tools.

- Personalized coaching to help clients develop better financial habits and avoid future debt.

Limitations & Considerations:

While Take Charge America has many benefits, here are some potential downsides:

- Debt management plans require consistent payments – If you miss a payment, you may lose program benefits.

- Not all debts qualify – Secured debts like mortgages and auto loans are not eligible.

- State restrictions apply – Some services may not be available in all states.

Customer Support Review:

Take Charge America receives high marks for customer service and program transparency. Many clients praise the easy enrollment process and supportive financial counselors.

Here’s what a customer named Jessica had to say:

“Take Charge America helped me lower my credit card interest rates and develop a realistic repayment plan. Their team was professional, patient, and always available to answer my questions. I highly recommend them!”

Frequently Asked Questions (FAQ)

What types of debt does Take Charge America handle?

TCA specializes in unsecured debts, such as credit card debt, medical bills, personal loans, and collections. They do not handle secured debts like auto loans or mortgages.

How does Take Charge America’s debt management plan work?

A DMP consolidates all your eligible debts into one monthly payment. TCA negotiates with creditors to lower interest rates and waive fees, helping you pay off debt faster.

Are there any upfront fees?

TCA’s fees vary by state, but they do not charge high upfront fees like for-profit debt relief companies. Many clients qualify for low-cost or waived fees.

Will using a debt management plan affect my credit score?

DMPs may initially impact your credit score, but as you make consistent payments and reduce your debt, your score is likely to improve over time.

How long does a debt management plan take?

Most DMPs take 3 to 5 years to complete, depending on the amount of debt enrolled.

Is Take Charge America available in all U.S. states?

TCA operates in most states, but some services may not be available in all locations. Check their website or call for details.

Does Take Charge America offer student loan assistance?

Yes, TCA provides guidance on student loan repayment options but does not offer direct consolidation services.

What qualifications do I need to enroll in a debt management plan?

You must have verifiable income to ensure you can make consistent monthly payments.

What should I expect during the free consultation?

During the consultation, a financial counselor will review your debt situation, discuss repayment strategies, and outline your best options.

How do I get started with Take Charge America?

Final Thoughts: Is Take Charge America Right for You?

Take Charge America is a trusted nonprofit credit counseling agency that provides debt management plans, financial education, and personalized counseling. Their low fees, nonprofit status, and strong industry reputation make them an excellent choice for individuals struggling with credit card debt and looking for a structured path to financial stability.

If you’re seeking a reputable debt management program, Take Charge America is a solid option.

Check if you qualify

Visit Website

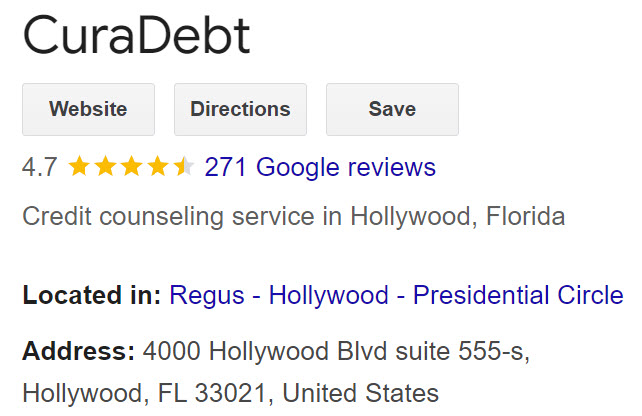

by Amine Rahal | Jul 11, 2026 | Debt Relief  Credit: CuraDebt.com

Quick Answer: Is CuraDebt Legit?

Yes. CuraDebt is a legitimate debt relief company operating since 1996 — one of the oldest in the industry — headquartered in Hollywood, Florida, and accredited by the AADR and IAPDA. What sets them apart: they handle both consumer debt settlement and tax/IRS debt relief under one roof, and they act as a matching platform that can route you to the program that fits your situation. No upfront fees for settlement, per FTC rules. Main limitations: not available in every state, and like all debt settlement, the process can hurt your credit score while negotiations are underway.

CuraDebt (https://www.curadebt.com/) is a debt relief company that has been in business since 1996 (according to their website), making it one of the oldest in the industry. They offer debt settlement and relief services for various types of unsecured debt, including credit card debt, personal loans, medical bills, and tax debt. Based on our review, CuraDebt has generated a lot of positive reviews for its debt relief services, particularly for its ability to help clients reduce their debt through negotiations with creditors. Where applicable, CuraDebt also operates as a referral and matching platform: if you don’t qualify for their settlement program, they may route you toward tax relief, business debt assistance, or other debt-management options instead of simply turning you away.

Want to see what CuraDebt can offer for your situation?

Their initial consultation is free, with no upfront fees for settlement. Every case is different — fees, terms, and program details are disclosed during the consultation before you commit to anything.

See Available Options →

CuraDebt is an affiliate partner — we may earn a commission if you use them, at no extra cost to you. This doesn’t affect our ratings.

Who is CuraDebt?

As we said earlier, CuraDebt is a debt settlement company that specializes in negotiating with creditors on behalf of consumers to reduce their overall debt. They work with individuals who are struggling to manage their credit card debt, tax debt, medical bills, or other unsecured debts.

| Headquarters |

Hollywood, Florida |

| Founded |

1996 (in Irvine, California) |

| States NOT Covered |

Connecticut, Georgia, Illinois, Kansas, Maine, Nevada, New Hampshire, Oregon, South Carolina, Vermont, West Virginia, and Puerto Rico |

| Website |

https://www.curadebt.com/ |

| Phone |

1-877-850-3328 Ext. 400 |

| Minimum Debt |

Generally $10,000 in unsecured debt for the settlement program (historically they’ve advertised lower minimums, and smaller cases may be routed to other programs — ask during the consultation) |

| Minimum Age |

21+ years old |

| Income Requirement |

No minimum, but must have verifiable regular income and be experiencing genuine financial hardship |

Company Legitimacy, Ratings & Reviews

As we covered earlier, this company has been operating in the debt settlement space since 1996, which makes it one of the oldest in the industry. In our view, the company’s longevity speaks volumes about its professionalism and customer service.

| Platform |

Rating |

Review Count |

| BBB (A+ Rating) |

4.7/5 |

~23 reviews |

| Google Reviews |

4.8/5 |

~271 reviews |

| TrustPilot |

3.3/5 |

~12 reviews |

| Yelp |

4.6/5 |

~12 reviews |

| Volume-Weighted Average |

4.73/5 |

~306 (BBB + Google + TrustPilot) |

Accreditations: Member of the American Association for Debt Resolution (AADR); Certified by the International Association of Professional Debt Arbitrators (IAPDA)

Two honest notes on the numbers. First, CuraDebt’s total review base is small compared to national giants — a few hundred reviews versus tens of thousands for the biggest settlement brands — so the averages carry less statistical weight. Second, the Trustpilot score (3.3/5) lags the other platforms, though it’s based on only about a dozen reviews. You can see exactly how CuraDebt stacks up against 21 competitors in our volume-weighted ranking of the best debt settlement companies, where they currently sit at #12.

CuraDebt BBB  CuraDebt Investopedia Rating  CuraDebt Google Rating CuraDebt Key Services & Features

💬 Debt Settlement & Negotiation

Their core program: negotiating with creditors to settle unsecured debts for less than the full balance. No fees until a settlement is reached and accepted.

🏛️ Tax Debt Relief

A rarity among settlement companies: their team includes tax professionals who can work with the IRS on back taxes, penalties, and liens.

🏢 Business & MCA Debt

Assistance with business debt and merchant cash advance obligations — another niche most consumer settlement firms don’t touch.

🔀 Free Counseling & Matching

A free consultation reviews your situation and routes you to the program that fits — including consolidation through partner lenders (watch the rates if you choose this path!).

- Fee structure: No upfront fees for settlement; a fee is charged only after a debt is successfully settled and you accept the offer. Exact fees vary by program and individual circumstances and are fully disclosed during the consultation — industry sources generally cite the 15–25% of enrolled debt range for settlement programs. Get your exact fee in writing before enrolling.

- Strategy: Utilizes various strategies, such as creditor violations (e.g., FDCPA, TCPA) to negotiate better terms for clients

- Limitations: services are not available in all U.S. states (see the excluded list above).

One of the key advantages of CuraDebt is that it does not charge upfront fees for settlement, meaning you only pay once a debt settlement has been successfully negotiated — this is required by FTC rules. CuraDebt is also known for its ability to identify creditor violations, which can sometimes lead to additional savings or settlements for the client.

⚠️ Know the Trade-Offs Before You Enroll

Debt settlement can negatively impact your credit score, as the process often involves stopping payments to creditors while negotiations are underway — and creditors can pursue collections or lawsuits during that window. Forgiven debt can also create a tax bill. And no company can guarantee a specific savings percentage: outcomes depend on your creditors, your hardship, and your ability to fund the settlement account. If someone quotes you a guaranteed result before reviewing your file, treat it as a red flag — at any company. Our complete debt relief guide walks through all the alternatives, including lower-risk options like nonprofit credit counseling.

Customer Support Review

They seem to have responsive customer support through their live chat feature. We tested it ourselves: we asked their support team to explain their services, and an agent named Genesis walked us through the model clearly — you make monthly deposits into a dedicated account instead of paying creditors directly, and as the balance accumulates, CuraDebt negotiates settlements with each creditor. When an offer comes in, they contact you to present it, and the funds only move once you accept. The agent cited typical savings figures during the chat, but treat any savings numbers you hear during sales conversations as marketing estimates, not promises — your actual results depend entirely on your creditors and your situation.

How CuraDebt Compares to Other Debt Relief Companies

CuraDebt’s superpower is breadth: consumer settlement, tax debt, and business/MCA debt under one roof. Pure-play settlement firms like New Era Debt Solutions and Pacific Debt Relief don’t touch IRS debt, and neither do the big national brands like Accredited Debt Relief, Beyond Finance, or National Debt Relief. Meanwhile, dedicated tax firms like Tax Relief Advocates and Five Star Tax Resolution don’t negotiate credit card debt. If your debt problem spans both worlds, CuraDebt is one of the very few single-consultation options.

The trade-off is scale: companies like TurboDebt and Freedom Debt Relief carry review bases in the tens of thousands, while CuraDebt’s footprint is a few hundred reviews. Longevity partially offsets that — very few companies in this industry have survived since 1996.

Not sure settlement is even your best move?

Depending on your numbers, consolidation, nonprofit counseling, or even bankruptcy may fit better than settlement. Our 60-second quiz compares all of them honestly before you talk to any company.

Take the Free Debt Relief Quiz →

🔑 Key Takeaways

- CuraDebt is legitimate and one of the industry’s oldest firms: operating since 1996, BBB A+, AADR member, IAPDA certified.

- Unique breadth: consumer debt settlement, tax/IRS debt relief, and business/MCA debt help under one roof.

- No upfront fees for settlement; exact fees vary by program and are disclosed during the free consultation — get them in writing.

- Settlement generally requires ~$10,000 in unsecured debt and genuine hardship; smaller or different cases may be routed to other programs.

- Not available in CT, GA, IL, KS, ME, NV, NH, OR, SC, VT, WV, or Puerto Rico.

- Settlement hurts your credit while underway — compare it against counseling and consolidation before enrolling.

Final Thoughts

CuraDebt earns its place on our radar through longevity, breadth, and a results-based fee model. It’s a particularly strong consideration if your debt picture includes tax debt or business debt alongside credit cards — almost nobody else handles all three. If you’re a straightforward credit-card-settlement case with a large balance, also compare the bigger-volume providers in our full ranking before deciding. And if your debt is still manageable, this first-person guide on how to reduce debt in 2026 or our bankruptcy vs. debt relief comparison may help you avoid a formal program altogether.

Ready to explore your options with CuraDebt?

The consultation is free, and they’ll tell you which of their programs (if any) fits your situation — settlement, tax relief, or an alternative path.

Explore Options with CuraDebt →

CuraDebt is an affiliate partner — we may earn a commission if you use them, at no extra cost to you. This doesn’t affect our ratings.

Frequently Asked Questions About CuraDebt

What types of debt does CuraDebt handle?

CuraDebt specializes in settling unsecured debts, including credit card debt, personal loans, medical bills, and private student loans — plus tax debts and business/MCA debt, which most settlement companies won’t touch. They do not typically handle secured debts like mortgages or auto loans, although it’s worth asking during the free consultation.

How does the CuraDebt debt settlement process work?

The process begins with a free consultation to assess your debt situation and see if you qualify. If you enroll, you make monthly deposits into a dedicated savings account instead of paying creditors directly. As funds accumulate, CuraDebt negotiates with each creditor to reduce what you owe; when an offer comes in, they present it to you, and the money moves only after you accept. The typical timeframe is 24 to 48 months.

Does CuraDebt charge upfront fees?

No. CuraDebt does not charge upfront fees for debt settlement — this is required by FTC rules. Fees are charged only after a settlement is successfully reached and you accept it. Exact fees vary by program and individual circumstances and are disclosed during the consultation; industry settlement fees generally run 15–25% of enrolled debt. Get your specific fee structure in writing before enrolling.

Will using CuraDebt affect my credit score?

Yes. Participating in a debt settlement program can negatively impact your credit score, since the process often involves stopping payments to creditors while negotiations are underway. The goal is to settle debts for less than what’s owed, which may improve your overall financial situation long-term, and the credit impact is generally less severe than bankruptcy — but the short-term damage is real. Weigh it against alternatives like counseling and consolidation first.

How long does the CuraDebt settlement process take?

The debt settlement process with CuraDebt typically takes between 24 and 48 months, depending on the amount of debt and how quickly you can accumulate funds in your dedicated savings account for settlements. Larger balances and slower funding stretch the timeline.

Is CuraDebt available in all U.S. states?

No. As of 2026, CuraDebt’s services are not available in Connecticut, Georgia, Illinois, Kansas, Maine, Nevada, New Hampshire, Oregon, South Carolina, Vermont, West Virginia, or Puerto Rico. If you live in an excluded state, you’ll need an alternative — our state guides, like Georgia debt relief options and debt solutions for Illinois, cover providers and programs that do operate there.

Does CuraDebt offer tax debt relief?

Yes. CuraDebt offers tax debt relief services, with tax professionals who can work with the IRS on your behalf to resolve back taxes, penalties, and liens. This is one of their biggest differentiators — most debt settlement companies won’t touch IRS debt at all, forcing you to hire a separate tax firm.

What are the qualifications to use CuraDebt’s services?

For the debt settlement program, you generally need at least $10,000 in unsecured debt, must be at least 21 years old, have verifiable regular income, and be experiencing a financial hardship that makes full repayment difficult. There is no maximum debt limit. CuraDebt has historically advertised lower minimums, and cases that don’t fit settlement may be routed to their tax relief, business debt, or other programs — so it’s worth doing the free consultation even if you’re near the threshold.

What happens if I don’t qualify for CuraDebt’s settlement program?

You won’t simply be turned away. CuraDebt operates partly as a matching platform: depending on your situation, they may point you toward tax relief services, business/MCA debt assistance, or alternative debt-management options. That said, always compare any recommendation against the full menu of options yourself — our free debt relief quiz gives you an independent read on whether settlement, consolidation, counseling, or bankruptcy fits your numbers.

What should I expect during the free consultation?

During the free consultation, a CuraDebt counselor reviews your financial situation and discusses your options for debt relief. They should explain the potential savings, timeline, risks, and fees involved — all program details are disclosed before any commitment. Come prepared with your balances, creditors, and monthly budget, and ask for everything in writing before you decide.

How do I get started with CuraDebt?

by Amine Rahal | Jul 8, 2026 | Debt Relief

Quick Answer: Is Five Star Tax Resolution Legit?

Yes. Five Star Tax Resolution is a legitimate, BBB-accredited (A+) tax relief firm founded in 2007 and headquartered in Pasadena, California, serving all 50 states. They put licensed tax attorneys, CPAs, and IRS Enrolled Agents on your case, require a minimum of $10,000 in tax debt, and offer a money-back guarantee if they can’t resolve your case. The trade-offs: premium pricing (fees start around $3,500 and average about $7,500 per Forbes) and a small third-party review footprint compared to bigger competitors.

When readers ask me about tax relief companies, I look for the same basics every time: who is actually doing the work? What services do they offer? How much do they charge? What are their reviews and ratings? Five Star Tax Resolution is a firm in the “tax problem solving” space, and my goal here is to explain how to evaluate them, what to expect from the process, and the questions I would ask before signing anything. Tax debt sits in its own corner of the debt relief world, with different rules, different negotiators, and different scams to avoid.

Is tax debt your only problem — or part of a bigger one?

If credit cards, personal loans, or medical bills are piling up alongside your IRS balance, a tax firm alone won’t fix it. Take our 60-second quiz to see which type of debt relief actually fits your full situation.

Take the Free Debt Relief Quiz →

Company Snapshot

| Official Name |

Five Star Tax Resolution Inc. |

| Headquarters |

Pasadena, California |

| Founded |

2007 |

| Service Area |

All 50 states |

| Minimum Tax Debt |

$10,000 |

| Fees |

Flat fee by phase; reported starting around $3,500, average ~$7,500 (Forbes) |

| Guarantee |

Full refund if they can’t resolve your case (per their BBB profile) |

| Team Credentials |

Tax attorneys, CPAs, IRS Enrolled Agents; NATP, NAEA, CTEC affiliations |

Legitimacy, Ratings & Reviews

Five Star Tax Resolution is a legitimate, BBB-accredited firm. Their consultations are free, they quote binding flat-rate fees, and unusually for this industry, they back the work with a money-back guarantee. Here is where their third-party ratings stand:

| Platform |

Rating |

Review Count |

| BBB (A+ Accredited) |

~4.76/5 |

Small base |

| TrustPilot |

~4.0–4.4/5 |

~23 reviews |

| Accreditations |

BBB, NATP; team certs from NAEA and CTEC |

My honest read: the ratings are good, but the review footprint is tiny for a firm operating since 2007. Compare that to a company like Tax Relief Advocates, which carries thousands of reviews across BBB and Google. A small review base isn’t disqualifying, but it means each individual review tells you less, and it makes the free consultation and written engagement letter more important, not less. One industry reviewer also noted the firm works with a reputation management company, which may partly explain the scarcity of negative feedback online. Take the star averages with a grain of salt and judge them on the specifics they put in writing for your case.

What Five Star Tax Resolution Does

Like other popular tax resolution firms (such as Tax Relief Advocates who you probably hear continuously on radio ads), the core menu typically includes:

🛡️ Protection & Relief

Wage garnishment releases, bank levy releases, and revenue officer assistance when collections are already active.

📋 Compliance Cleanup

Filing or amending missing returns — the IRS won’t negotiate anything until you’re current.

💰 Payment Solutions

Installment agreements, Currently Not Collectible status for genuine hardship, and Offers in Compromise when you qualify.

⚖️ Representation

Penalty abatement requests, audit defense, and payroll tax problem representation before the IRS.

The real differentiator is not the list. It is the quality of the people doing the work and how they communicate with you from week to week.

Five Star Tax Resolution VS Your Other Options

Let’s compare some of the most popular options when it comes to dealing with high tax debt:

| Feature |

Five Star Tax Resolution

Pro Service |

DIY with IRS

Lowest Cost |

Local CPA / EA

Hands-On |

Big National Firm

High Volume |

| Who handles your case |

Named EA/CPA/attorney as lead; dedicated case manager |

You handle calls, forms, deadlines |

Licensed practitioner; often the person you meet runs the file |

Varies; large teams, work may be distributed |

| Typical services |

Transcripts, filings, levy/garnishment relief, Installment Agreement, CNC, OIC, penalty abatement, audit defense |

Online payment plans, amended/late filings, hardship requests, phone appeals |

Same as left, plus ongoing bookkeeping/tax prep if needed |

Full menu; strong at processing volume quickly |

| Estimated fees |

Flat fee by phase; reported ~$3,500 to $7,500+ — premium end, backed by money-back guarantee |

$0 fee to IRS for basic plans; your time is the cost |

Hourly or fixed; varies by market and complexity |

Wide range; can be higher for sales-driven models |

| Best for |

Balances with active collections, missing returns, need for structured representation |

Smaller balances, straightforward plans, comfortable self-advocates |

Personalized attention, local meetings, combined tax prep + resolution |

Multi-year, multi-state, high-volume processing needs |

| Pros |

Dedicated licensed rep; transparent plan; money-back guarantee; secure document portal |

Cheapest; fastest for simple cases; full control |

Direct access to practitioner; can pair with ongoing planning/tax filing |

Extended hours; deep process staff; national footprint |

| Cons |

Premium pricing; small review footprint; outcome depends on your financials and compliance |

Steeper learning curve; time on hold; easier to miss deadlines |

Availability/pricing vary; some cases exceed a solo practice’s bandwidth |

Communication can feel impersonal; sales pressure at some firms |

| Speed to action |

Quick transcript pull and protection steps once onboarded; cases reportedly run 1 week to ~120 days |

Depends on your time and IRS phone queues |

Generally prompt, especially for local emergencies |

Intake is fast; negotiations can be assembly-line style |

| Communication |

Scheduled updates via portal/phone/email; single point of contact |

You manage all IRS communication |

Direct line to practitioner; in-person possible |

Ticket-based; multiple contacts over the life of the case |

| Transparency |

Written plan and flat fee by scope; clear what’s included |

Full control, but you must learn the rules and forms |

Usually straightforward; ask for engagement letter and deliverables |

Varies by brand; ask about cancellations and refund terms |

| Bottom line |

Balanced choice for guided, professional resolution without losing visibility into your case |

Best if the balance is small and you’re comfortable managing forms and deadlines |

Great for personalized attention and ongoing tax planning if the case fits their capacity |

Useful for complex, high-volume needs; evaluate communication quality before committing |

One more comparison worth making: if your debt problem is mostly credit cards and personal loans with some tax debt mixed in, a hybrid provider may serve you better than a pure tax firm. CuraDebt is one of the few companies we’ve reviewed that handles both consumer debt settlement and tax/IRS cases under one roof, and our full ranking of debt relief companies tags each provider by type so you can see who does what at a glance.

Does a Tax Lawyer or Attorney Help?

If you are planning to work with Five Star Tax Resolution, ask exactly who will represent you in front of the IRS. A solid tax lawyer or attorney firm will center the case around licensed professionals such as:

- Enrolled Agents (EAs) who deal with the IRS every day

- CPAs with tax controversy experience

- Tax attorneys when legal complexity or litigation risk is present

I prefer firms that name the lead practitioner on my file and give me direct contact details. If you only interact with sales staff and cannot meet the EA, CPA, or attorney assigned to you, that is a yellow flag. The same logic applies if you’re weighing legal help for consumer debts — our guide to debt consolidation lawyers and attorneys uses the exact same screening criteria.

Now, on their website, it shows Victor A. Latham as the Senior Tax Attorney. Ask if you are going to receive his services if you work with them.

Victor Latham, Senior Tax Attorney. The Process You Should Expect

- Discovery and transcripts

The firm should pull your IRS transcripts with a signed authorization, confirm balances and deadlines, and give you a written game plan.

- Compliance first

The IRS will not negotiate until all required returns are filed. Expect a push to get current on filings and withholding or estimated payments.

- Financial analysis

A proper analysis uses IRS Collection Financial Standards to model what you can afford. This drives your eligibility for an installment plan, hardship status, or an Offer in Compromise.

- Resolution submission

The firm files the chosen path, responds to IRS notices, and handles back-and-forth until you have a written agreement or determination.

- Follow-through

Good firms set reminders for future filings and estimated payments so you do not default your agreement.

Pricing and How to Think About It

Most tax resolution work is quoted as a flat fee based on complexity. Typical industry ranges for individual cases are often $2,000 to $6,000+, with payroll tax and multi-year or audit cases costing more. Five Star sits at the premium end of that range: Forbes reports their fees start around $3,500, with average cases running about $7,500 — roughly double what some leading competitors charge. The counterweights are the binding flat-rate quote, payment plans, and the money-back guarantee if they can’t resolve your case. Many firms phase the work:

- Investigation phase to pull transcripts and map options

- Resolution phase to prepare and negotiate your case

- Compliance or monitoring phase if needed

What I ask for:

- A written engagement letter with scope, deliverables, timelines, and total cost

- Clarity on refund policies and what happens if you disengage

- A list of what is not included so there are no surprises

⚠️ Red Flag: Guaranteed Offers in Compromise

Be wary of anyone — at any firm — who guarantees an Offer in Compromise or quotes a fee before pulling transcripts and doing a real financial analysis. Only the IRS decides who qualifies, and the FTC has taken enforcement action against multiple tax relief firms for deceptive claims. Before paying anyone, run your numbers through the IRS’s own free Offer in Compromise Pre-Qualifier. If a salesperson promises “pennies on the dollar” before seeing your transcripts, walk away.

Strengths I Look For With a Firm Like This

- Clear point of contact and updates on a set cadence

- Licensed staff who will be the ones speaking to the IRS

- Education first mindset with realistic expectations

- Document portal and secure ways to share sensitive files

- Written plan that matches IRS standards rather than sales talking points

Potential Drawbacks to Weigh

- Upfront cost can feel high if the balance is small or the fix is simple — and Five Star’s fees run above industry average

- Outcome uncertainty because the IRS decision depends on your true financials and compliance history

- Time to resolution can stretch for months, especially for offers or complex payroll cases

- Small review footprint means less independent evidence than bigger firms provide

✅ Five Star Might Be a Good Fit If…

- You owe a meaningful balance ($10,000+) and are facing active collections

- You have missing returns and need both filing and negotiation help

- Your situation involves payroll tax or a prior defaulted agreement

- You want a licensed professional to speak to the IRS for you — and value the money-back guarantee enough to pay premium fees

🚫 You Might Not Need a Firm If…

- You owe a small balance and can set up a standard online payment plan yourself

- You are fully compliant and simply need a short-term extension or more time to pay

- You are comfortable using the IRS’s self-service tools and calling the agency directly

Questions I Would Ask Five Star Tax Resolution

- Who will be my licensed representative and how do I reach them directly

- Can I see a written scope of work and a total flat fee by phase

- What are realistic outcomes for my case using IRS standards

- How often will you update me and through which channel

- What happens if the IRS rejects the first proposal

- What exactly triggers your money-back guarantee — and can I get the refund terms in writing

- How will you help me stay compliant so I do not default the agreement

Documents to Gather Before You Talk

- All IRS and state notices

- Last two years of filed returns and any unfiled years list

- Recent pay stubs, bank statements, and a monthly expense breakdown

- Proof of extraordinary expenses that might matter for financial standards

- Any existing installment agreements or prior IRS correspondence

Not sure a tax firm is even the right move?

Depending on your full debt picture, settlement, consolidation, counseling, or even bankruptcy may make more sense than paying a resolution firm. Our quiz compares them all honestly, in about a minute.

Find Your Best Debt Relief Option →

🔑 Key Takeaways

- Five Star Tax Resolution is legitimate: BBB A+ accredited, founded 2007, licensed attorneys/CPAs/EAs on staff, serving all 50 states.

- Premium pricing: fees reportedly start ~$3,500 and average ~$7,500 — but they offer a binding flat-rate quote and money-back guarantee.

- $10,000 minimum tax debt; consultations are free.

- Their third-party review base is small — put extra weight on the written engagement letter, not the star averages.

- If your tax debt is small and you’re compliant, try the IRS’s free self-service tools before paying any firm.

Bottom Line

Five Star Tax Resolution offers the standard suite of tax relief services, which isn’t the same as debt settlement companies who focus on credit card debt — providers like Americor or JG Wentworth explicitly do not touch IRS debt. The value you get will depend on the caliber of the licensed professional who handles your file and the firm’s willingness to set realistic expectations. If you decide to interview them, go in with transcripts, a clear picture of your finances, and the questions above. A good firm will welcome that level of preparation, give you a sober assessment, and put everything in writing.

I always recommend speaking with more than one provider and comparing fees, scope, and who will actually represent you. If your balance and case are straightforward, consider whether you can resolve it directly with the IRS. If your situation is complex or urgent, a strong practitioner can be worth the cost by protecting your rights, preventing costly mistakes, and saving you time. And if the tax bill is just one piece of a wider debt problem, our bankruptcy vs. debt relief comparison and this first-person guide on how to reduce debt in 2026 will help you see the whole board before you commit to anything.

👉 Take the Free Debt Relief Quiz 👉 Read Our Complete Debt Relief Guide

Frequently Asked Questions About Five Star Tax Resolution

Is Five Star Tax Resolution a legitimate company?

Yes. Five Star Tax Resolution is a legitimate, BBB-accredited tax relief firm founded in 2007 and headquartered in Pasadena, California. They employ licensed tax attorneys, CPAs, and IRS Enrolled Agents — all federally authorized to represent taxpayers before the IRS — and hold affiliations with the NATP, NAEA, and CTEC. Legitimate doesn’t automatically mean right for you, though: compare fees, scope, and who will actually handle your file before signing.

How much does Five Star Tax Resolution cost?

Five Star doesn’t publish pricing, but Forbes reports fees starting around $3,500 with average cases running about $7,500 — the premium end of the industry, where typical individual cases run $2,000 to $6,000+. They provide a binding flat-rate quote after a free consultation, accept payment plans, and back the work with a money-back guarantee if they can’t resolve your case. Always get the total fee, scope, and refund terms in a written engagement letter.

What is the minimum tax debt Five Star requires?

Five Star Tax Resolution requires a minimum of $10,000 in tax debt, which is standard for the industry. If you owe less than that, you’re usually better off using the IRS’s free self-service tools: online installment agreements, penalty abatement requests, and the Offer in Compromise Pre-Qualifier all cost nothing but your time.

Does Five Star Tax Resolution offer a money-back guarantee?

Yes. According to their BBB profile, Five Star’s policy is to provide a full refund if they cannot resolve your case — a rarity in this industry. That said, “resolve” can be defined loosely, so ask exactly what triggers the guarantee and get the refund conditions in writing before you pay anything.

How long does Five Star take to resolve a tax case?

Reported timelines range from about one week to 120 days depending on complexity, with the negotiation phase typically running two to three months. Offers in Compromise and multi-year payroll cases take longer. You can speed things up by submitting requested documents quickly and staying current on filings while the case is open.

Can Five Star guarantee my tax debt will be reduced?

No — and to their credit, they don’t claim to. Only the IRS or your state tax agency decides whether you qualify for an Offer in Compromise, penalty abatement, or hardship status, based on your actual financials and compliance history. Any firm that guarantees a specific reduction before pulling your transcripts is showing you a red flag, not a feature.

Is Five Star Tax Resolution the same as a debt settlement company?

No. Tax resolution firms like Five Star negotiate with the IRS and state tax agencies under formal programs (installment agreements, Offers in Compromise, penalty abatement). Debt settlement companies negotiate with private creditors over credit cards, personal loans, and medical bills — and most won’t touch tax debt at all. Our ranked list of debt relief companies tags each provider by type; CuraDebt is one of the few that handles both.

Can I resolve my IRS tax debt without hiring a firm?

Often, yes. If your balance is modest and your returns are filed, the IRS lets you set up payment plans online for free, request penalty relief by phone, and check Offer in Compromise eligibility with their free Pre-Qualifier tool. A firm earns its fee when collections are already active (garnishments, levies), returns are missing, payroll tax is involved, or you simply want a licensed professional handling every IRS conversation for you.

What if I have credit card debt on top of my tax debt?

You’ll likely need two different strategies, because tax firms don’t negotiate consumer debt and most settlement companies don’t touch the IRS. Start by mapping your full picture: our free debt relief quiz compares settlement, consolidation, counseling, and bankruptcy based on your numbers, and our complete debt relief guide explains how each path treats tax debt differently.

Is Five Star Tax Resolution available in my state?

Yes — Five Star serves clients in all 50 states, handling both IRS and state tax agency matters. Keep in mind that state tax rules and consumer debt protections vary considerably; if you’re weighing your broader options locally, our state guides such as California debt relief programs (Five Star’s home state) cover the state-specific landscape.

|

![ClearOne Advantage: We Review This Debt Relief Company [2026 Update]](https://cpiinflationcalculator.com/wp-content/uploads/2025/02/clearonehomepagescreen.jpg)