Alex Demolitor

Alex Demolitor is a Canadian financial writer hailing from Halifax, NS. Alex has a Bachelors Degree from King's College and passed the CFA Exam Level III. He specializes in fundamental analysis of the stock, bond, commodity, and FX markets. He also covers US & Canadian economic indicators.

by Alex Demolitor | Feb 13, 2026 | Definitions

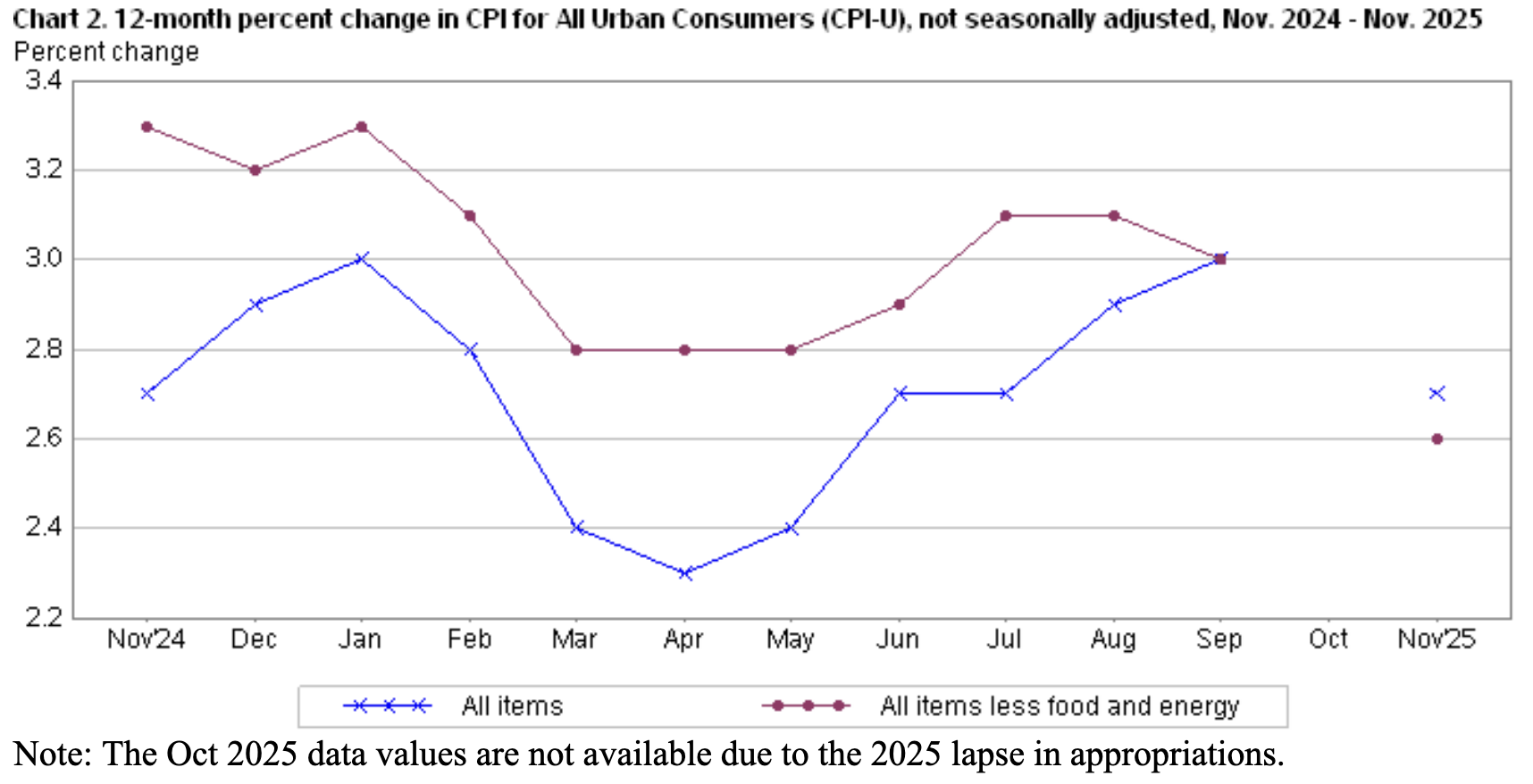

The January 2025 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation increased by 0.2% this month, down from 0.3% in December. These data were released at 8:30 am EST on February 13, 2026, by the Bureau of Labor Statistics (BLS). Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 2.4%, a deceleration from the 2.7% realized in December.

The figures were well behaved and mostly aligned with economists’ consensus estimates. The table below is courtesy of Investing.com. The left column represents January’s figures, while the right column represents forecasters’ expectations. As you can see, the headline figures missed slightly, while the core metrics matched the consensus.

As it stands, a mixed economic outlook has Fed officials leaning in a hawkish direction. Dallas Fed President Lorie Logan said on Feb. 10 that “We will learn in the coming months whether inflation is coming down to our target and whether the labor market will remain stable. If so, this would tell me that our current policy stance is appropriate and no further rate cuts are needed to achieve our dual mandate goals.

“If instead we see inflation coming down but with further material cooling in the labor market, cutting rates again could become appropriate. But right now, I am more worried about inflation remaining stubbornly high.”

Thus, with commodity futures prices rising sharply in January, higher input costs could uplift the CPI over the next few months and keep the Fed on hold.

Food Prices

The food index rose by 0.2% MoM in January, and five of the six major grocery indices increased this month.

- Cereals and bakery products (+1.2%)

- Meats, poultry, fish, and eggs (+0.2%)

- Dairy and related products (+0.8%)

- Fruits and vegetables (+0.1%)

- Nonalcoholic beverages (+0.1%)

- Other food at home (-0.3%)

Surprisingly, the food away from home index only increased by 0.1% (versus 0.7% in December), as restaurant inflation underperformed in January.

Energy Prices

The energy index fell by 1.5% MoM in January, with gasoline prices down by 3.2%, electricity down by 0.1%, and natural gas rising by 1.0%.

Core CPI

The January core CPI rose by 2.5% Y-o-Y, down from 2.6% in December. Below is an itemized breakdown of the various components:

- Shelter index: (+0.2%) [December: +0.4%]

- Rent index: (+0.2%) [December: +0.3%]

- Owners’ equivalent rent: (+0.2%) [December: +0.3%]

- Motor vehicle insurance: (-0.4%) [December: NA]

- Medical care services: (+0.3%) [December: +0.4%]

- Physician services: (+0.3%) [December: +0.3%]

- Hospital services: (+0.9%) [December: +1.0%]

- Airline fares: (+6.5%) [December: +3.8%]

Seasonally Unadjusted CPI

Before seasonal adjustments, the CPI-U for January 2025 increased by 2.4% Y-o-Y to an index level of 325.252. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

From Bad to Good

After months of solid economic data, weakness to start the New Year had recession whispers growing louder.

For example, the BLS reported on Feb. 5 that JOLTS Job Openings retreated in December. The report stated:

“The number of job openings trended down to 6.5 million (-386,000) in December and was down by 966,000 over the year. The job openings rate, at 3.9 percent, changed little over the month. The number of job openings decreased in professional and business services (-257,000), retail trade (-195,000), and finance and insurance (-120,000).”

Moreover, with the metric sinking below its pre-pandemic baseline, a cooling U.S. labor market was on full display.

Next up, the U.S. Census Bureau revealed on Feb. 10 that retail sales were flat in December, which poured cold water on the idea of robust holiday sales. As a result, consumer spending and employment weakness created more uncertainty for investors and policymakers.

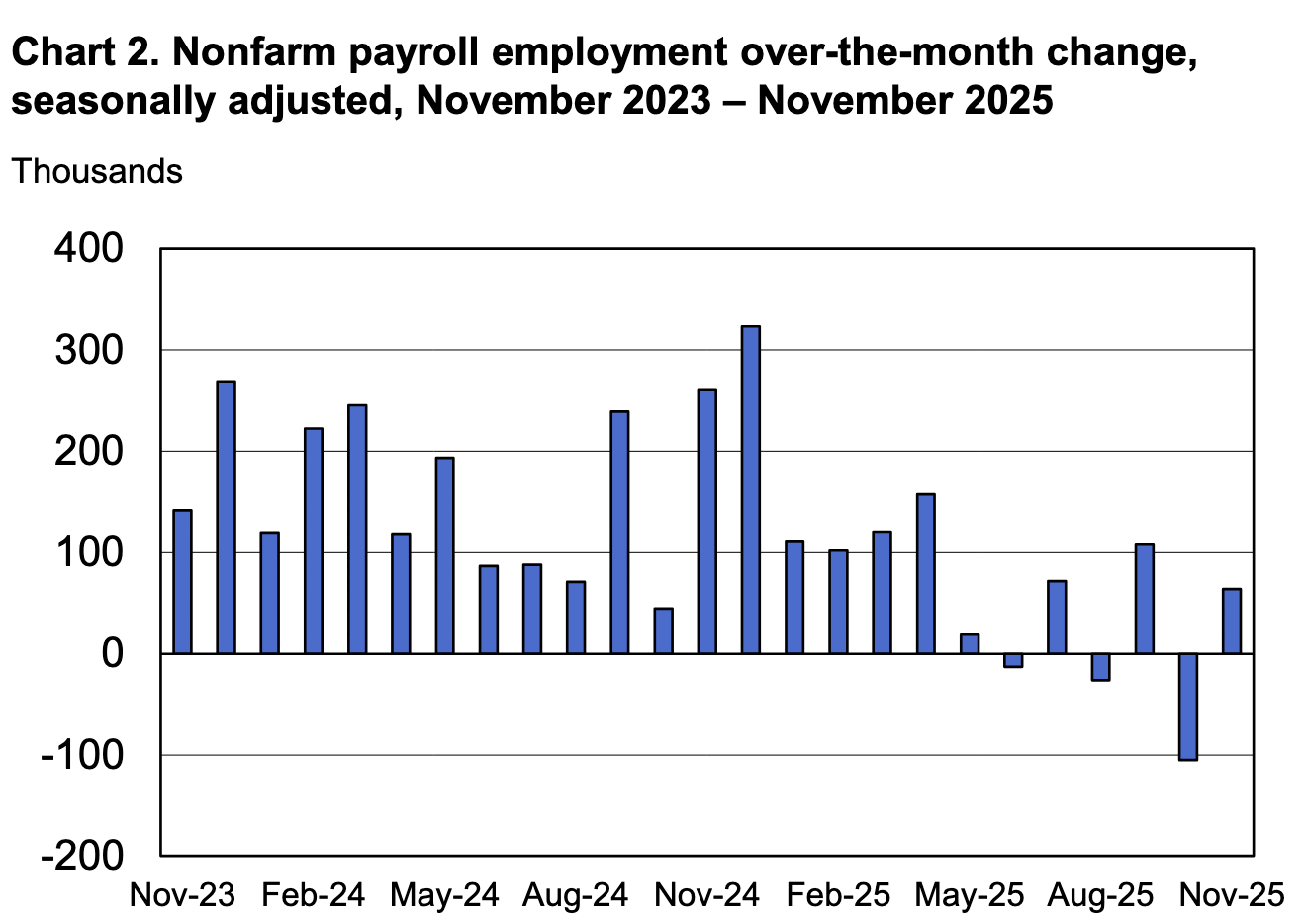

However, while it seemed like the economic outlook could be headed in a negative direction, the BLS reported on Feb. 11 that U.S. nonfarm payrolls rose by 130,000 in January, the largest monthly increase since December 2024.

More importantly, the job gains, wage inflation, and the unemployment rate all outperformed economists’ consensus estimates, offsetting the recession fears that culminated from the weak data above.

Add it all up, and the recent data is still strong enough to keep the FOMC on hold. Higher inflation is likely over the next few months, and the committee is unlikely to expedite rate cuts as long as employment remains solid.

Turning to the financial markets, gold and silver stole the show in January, with rapid rises and intense corrections. And while both have calmed for the time being, volatility could be amplified as their bull markets reach an accelerated phase.

To explain, the blue line above tracks the gold-S&P 500 ratio. If you analyze the left side of the chart, you can see that gold significantly outperformed stocks leading up to, during, and after the global financial crisis.

Therefore, while the surge above $5,000 has garnered plenty of headlines, the level of the ratio on the right side of the chart signals that more upside could be on the horizon, and gold could remain an in-demand asset for the foreseeable future.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Please seek the guidance of a financial advisor before making any investment decision.

Furthermore, if you’ve built a thriving business and are looking to cash in on your success, it’s essential to think from a buyer’s perspective. Our extensive guide covers prep work, valuation, marketing, and provides other useful tips to help you create a professional pitch. We also have more valuation resources to help better understand the key financial metrics that can make or break a deal.

In addition, if you own an HVAC business in Texas, our niche guide is the perfect playbook to help you obtain the best price.

Finally, for creditor solutions, please consult our list of debt management firms for other financial resources in your area.

by Alex Demolitor | Jan 13, 2026 | Definitions

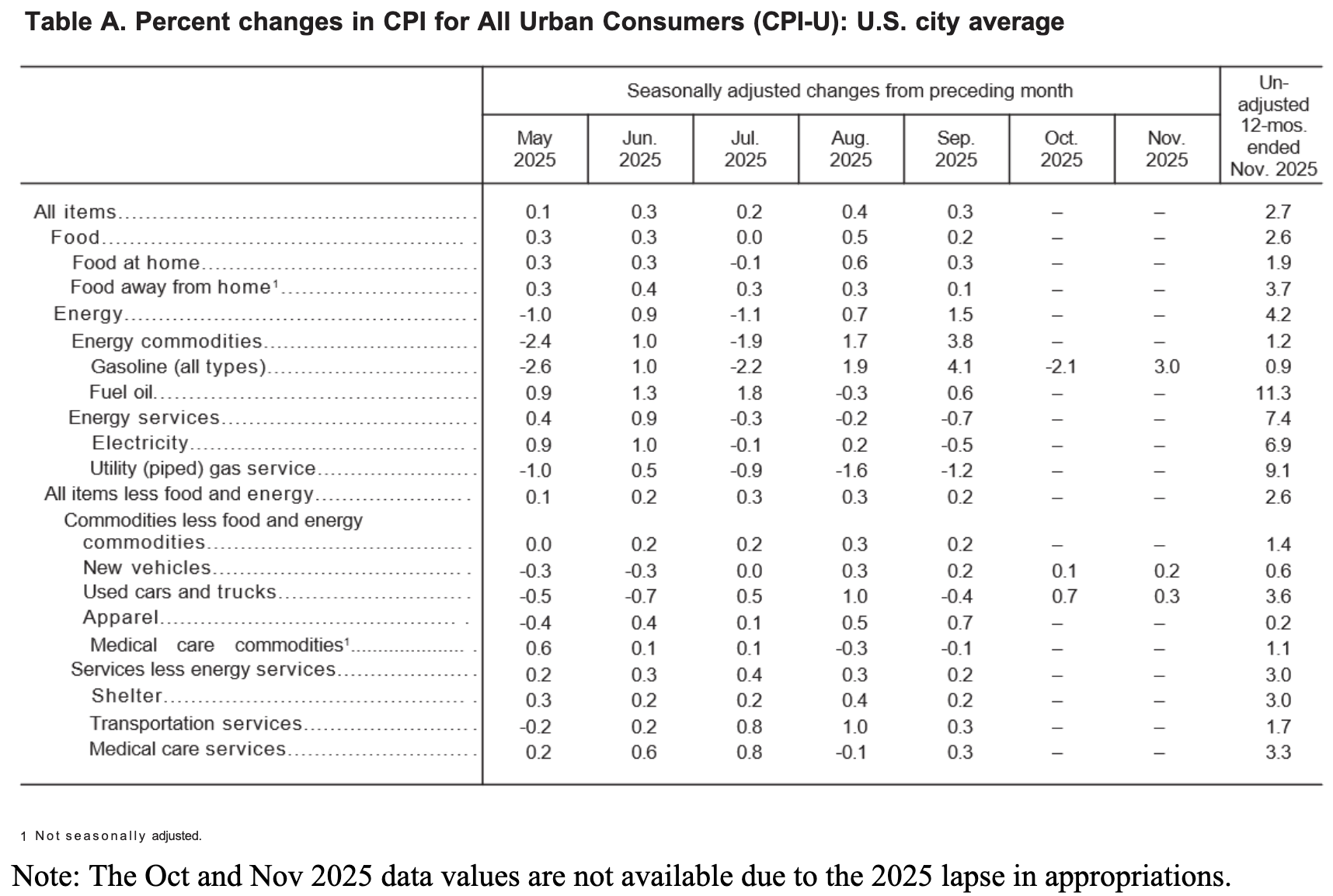

The December 2025 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation increased by 0.3% this month, up from the 0.2% average over the last two months. These data were released at 8:30 am EST on January 13, 2026, by the Bureau of Labor Statistics (BLS). Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 2.7%, matching the recent two-month average.

Today’s core results also missed economists’ consensus estimates. The table below is courtesy of Investing.com. The left column represents December’s figures, while the right column represents forecasters’ expectations. As you can see, the red metrics highlight how core inflation was weaker than anticipated.

With Fed Chairman Jerome Powell still leading the FOMC until his term ends later this year, he reiterated in December that he’s in no hurry to cut rates. And with investors pricing in little to no chance of a rate cut in January, Bloomberg reported on Jan. 9 that “Bond traders maintained an outlook for two rate cuts overall in 2026, with the first seen by mid-year.”

As a result, disappointing economic data will likely be required for accelerated easing over the next few months.

Food Prices

The food index rose by 0.7% MoM in December, and five of the six major grocery indices increased this month.

- Cereals and bakery products (+0.6%)

- Meats, poultry, fish, and eggs (-0.2%)

- Dairy and related products (+0.9%)

- Fruits and vegetables (+0.5%)

- Nonalcoholic beverages (+0.4%)

- Other food at home (+1.6%)

The food away from home index also jumped by 0.7%, as restaurant inflation kept pace with grocery prices in December.

Energy Prices

The energy index increased by 0.3% MoM in December, with gasoline prices down by 0.5%, electricity down by 0.1%, and natural gas rising by 4.4%.

Core CPI

The December core CPI rose by 2.6% Y-o-Y, matching the average figure from the previous two months. As a reminder, the October CPI report was cancelled due to the government shutdown, so the metrics don’t have comparable MoM data from November.

- Shelter index: (+0.4%)

- Rent index: (+0.3%)

- Owners’ equivalent rent: (+0.3%)

- Motor vehicle insurance: (NA)

- Medical care services: (+0.4%)

- Physician services: (+0.3%)

- Hospital services: (+1.0%)

- Airline fares: (5.2%)

Seasonally Unadjusted CPI

Before seasonal adjustments, the CPI-U for December 2025 increased by 2.7% Y-o-Y to an index level of 324.054. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

Let the Good Times Roll

With solid economic data pointing to steady economic activity, the FOMC can continue its wait-and-see approach and not rush further rate cuts.

For example, the BLS released its Employment Situation report on Jan. 9. The U.S. economy added 50,000 net new jobs, and the unemployment rate declined to 4.4%. Furthermore, average hourly earnings (a proxy for wage inflation) increased from 3.6% Y-o-Y in November to 3.8% Y-o-Y in December. Consequently, the labor market remains on solid footing for the time being.

As further evidence, the BLS released its Job Openings and Labor Turnover Summary (JOLTS) on Jan. 7. And with more than seven million job openings still available, the metric (the blue line below) has stabilized near its pre-pandemic baseline. Likewise, layoffs and discharges (the green line below) also remain in a healthy range and highlight how most employers continue to retain staff.

Finally, the Atlanta Fed updated its Q4 GDPNow model on Jan. 9. And while the results can be skewed by fluctuating imports and exports, and the data is lagged, the latest reading pegs growth at 5.1% (the green line below). If realized, the results would be well above 2% trend growth and economists’ consensus estimates (the blue line below).

Add it all up, and the recent data is strong enough to suppress any rate-cut calls, and the FOMC should continue to preach the same message until weaker data forces its hand.

Turning to the financial markets, gold had a tremendous 2025, and the fundamentals support more strength in 2026.

To explain, the orange line above tracks the 5-year rolling percentage change in the gold price, while the blue line above tracks the 5-year rolling percentage change in global military spending. As you can see, the yellow metal lives up to its safe-haven reputation when the geopolitical outlook becomes more treacherous.

To that point, U.S. President Donald Trump has advocated for a 50% increase in the U.S. military budget, in what he called “very troubled and dangerous times.” As a result, the spending trend should continue, and the developments are bullish for gold.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Please seek the guidance of a financial advisor before making any investment decision.

Furthermore, if you’re looking to diversify your portfolio or strategically exit a business, there are several strategies to help realize the best valuation. Our extensive guides for company owners in Illinois, Michigan, and Ohio provide insights into compliance issues, tax plans, demand assessments, and much more.

In addition, please consult our list of debt management firms for other financial services in your area.

by Alex Demolitor | Dec 18, 2025 | Definitions

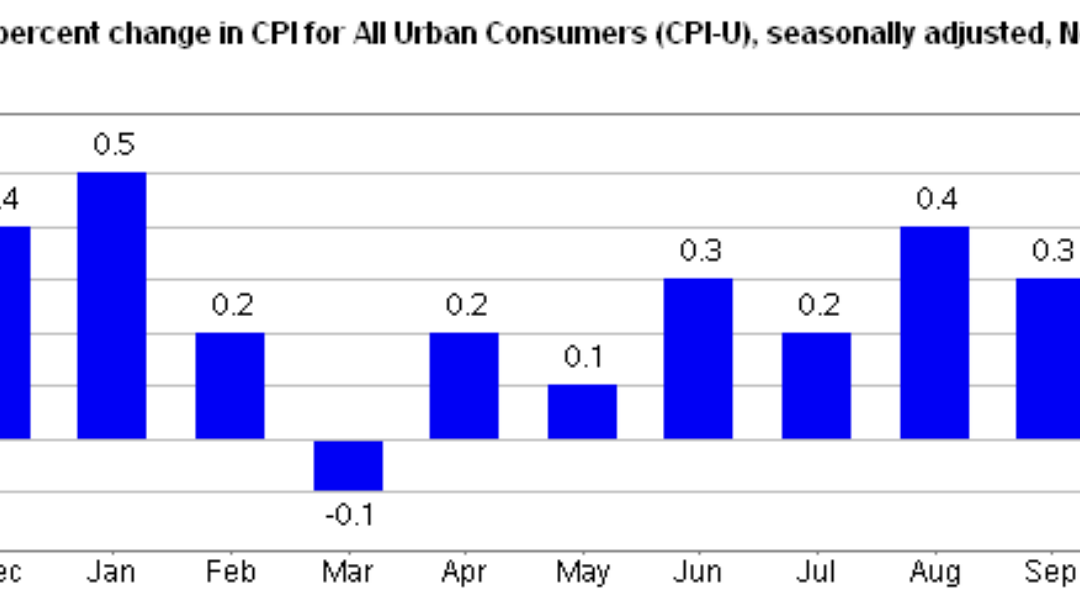

The November 2025 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation increased by 0.2% over the last two months, down from 0.3% in September. These data were released at 8:30 am EST on December 18, 2025, by the Bureau of Labor Statistics (BLS). Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 2.7%, down from 3.0% in September. As a reminder, the October CPI report was cancelled due to the government shutdown, so there are no comparable figures on a MoM basis.

Today’s results also missed economists’ consensus estimates. The table below is courtesy of Investing.com. The left column represents November’s figures, while the right column represents forecasters’ expectations. As you can see, the red metrics highlight how inflation was subdued relative to forecasts.

After cutting interest rates for the second consecutive meeting, Fed Chairman Jerome Powell emphasized on Dec. 10 that “Monetary policy is not on a preset course, and we will make our decisions on a meeting-by-meeting basis.”

“Everyone around the table at the FOMC agrees that inflation is too high and we want it to come down, and agrees that the labor market has softened and that there is further risk…. I’ve said before a couple times, we’re well positioned to wait to see how the economy evolves. We’ll just have to see.”

As such, with the FOMC confronting uncertainty on both sides of its dual mandate, further labor market weakness is likely necessary for more easing in the months ahead.

Food Prices

The food index rose by 2.6% Y-o-Y in November. Again, the monthly changes are neglected due to the missing October report, so the figures below are relative to November 2024.

- Cereals and bakery products (+1.9%)

- Meats, poultry, fish, and eggs (+4.7%)

- Dairy and related products (-1.6%)

- Fruits and vegetables (+0.1%)

- Nonalcoholic beverages (+4.3%)

- Other food at home (+1.3%)

The food away from home index was up by 3.7%, as restaurant inflation continues to outpace grocery prices.

Energy Prices

The energy index rose by 4.2% Y-o-Y in November, with gasoline prices up by 0.9%, electricity by 6.9%, and natural gas by 9.1%.

Core CPI

The November core CPI rose by 2.6% Y-o-Y, down from 3.0% in September. Below is an itemized breakdown of the main Y-o-Y price fluctuations seen in the core CPI reading:

- Shelter index: (+3.0%)

- Rent index: (+3.0%)

- Owners’ equivalent rent: (+3.4%)

- Motor vehicle insurance: (NA)

- Medical care services: (+3.3%)

- Physician services: (+1.7%)

- Hospital services: (+5.7%)

- Airline fares: (-5.4%)

Seasonally Unadjusted CPI

Before seasonal adjustments, the CPI-U for November 2025 increased by 2.7% Y-o-Y to an index level of 324.122. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

Not Bad Enough

With mixed economic data hitting the wire in recent days, there isn’t any concrete evidence that supports the Fed altering its meeting-by-meeting approach.

For example, S&P Global released its U.S. Composite PMI on Dec. 16. And while growth momentum has slowed, the current reading of 53 signals a healthy expansion. An excerpt read:

“The headline S&P Global US PMI ® Composite Output Index fell to 53.0 in December from 54.2 in November, according to the ‘flash’ reading (based on about 85% of usual survey responses). The latest reading was the lowest since June, though continues to indicate robust economic growth….

“Input cost inflation accelerated markedly in December, hitting the fastest since November 2022,” while “increased costs again fed through to higher selling prices, with the overall rate of inflation rising to the steepest since July and therefore amongst the greatest since the pandemic-related price-surge of 2022.”

So, while business activity has softened over the last few months, the modest momentum deceleration is unlikely to induce rate cuts with alternative inflation metrics trending up.

Furthermore, the U.S. Bureau of Labor Statistics revealed on Dec. 16 that the U.S. economy added 64,000 net new jobs in November — a solid increase given the paltry figures realized over the last few months. The report also noted how “Construction employment grew by 28,000 in November, as nonresidential specialty trade contractors added 19,000 jobs,” which highlights decent strength in the interest-rate sensitive sector.

Finally, the U.S. Census Bureau added on Dec. 16 that retail sales remained solid on an annual basis, as consumers continued to spend ahead of the holiday season. An excerpt read:

“Retail trade sales were up 0.1 percent (±0.5 percent)* from September 2025, and up 3.4 percent (±0.5 percent) from last year. Nonstore retailers were up 9.0 percent (±1.2 percent) from last year, while food service and drinking places were up 4.1 percent (±1.8 percent) from October 2024.”

Add it all up, and the recent data is likely good enough to keep the FOMC in wait-and-see mode.

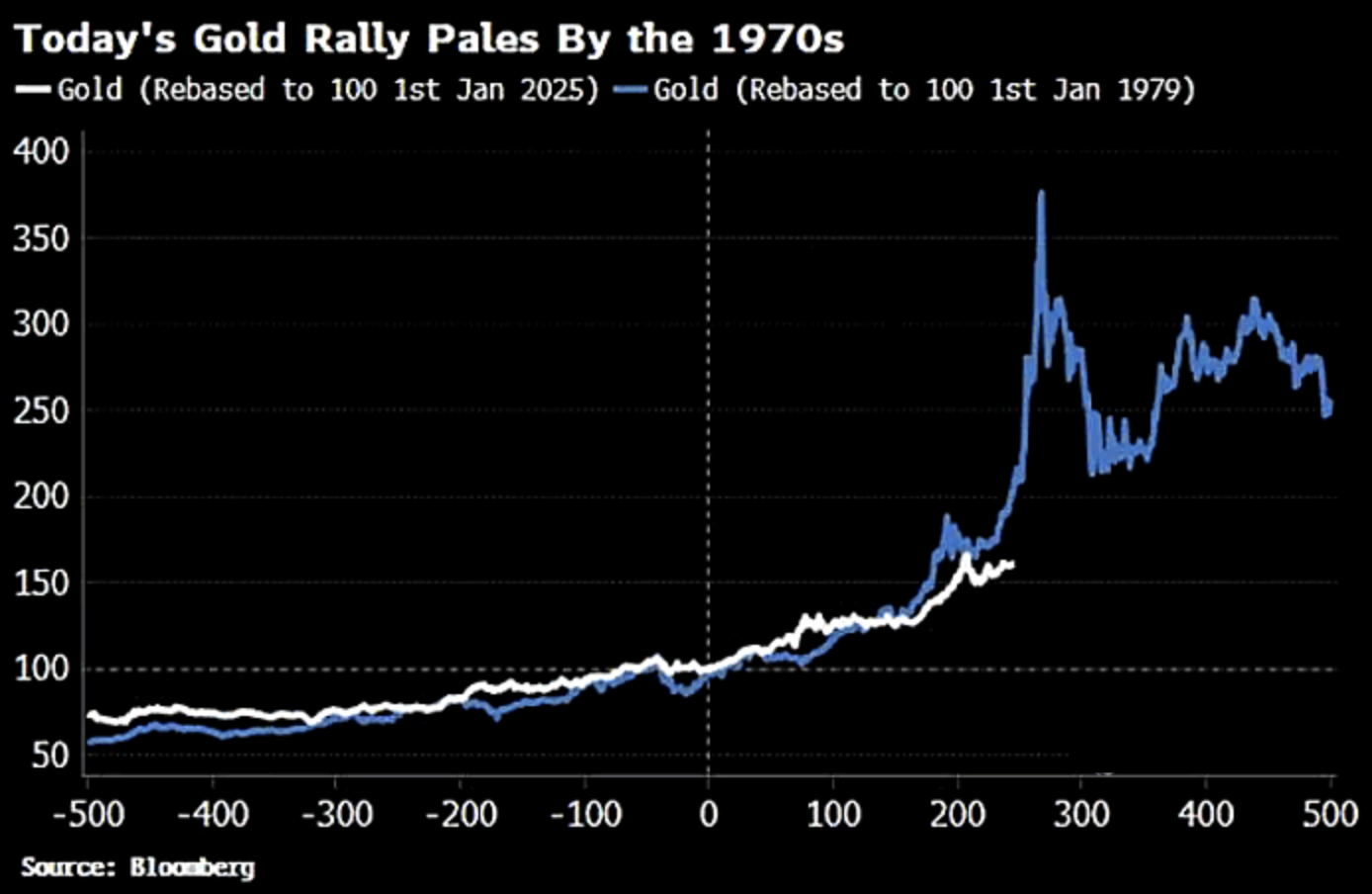

Turning to the financial markets, gold has had an impressive 2025, and further gains could be in store in the months and years ahead.

To explain, the white line above tracks gold’s indexed performance since Jan. 1, 2025, while the blue line above tracks its indexed performance from Jan. 1, 1979. As you can see, the yellow metal had a lot of runway during the historical surge; and given the similar fundamental developments occurring today, gold’s bull market may have plenty of room to run.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Please seek the guidance of a financial advisor before making any investment decision.

Furthermore, if credit concerns have increased alongside the economic uncertainty, residents in Georgia have options at their disposal. Our extensive guide outlines how to approach credit counseling, debt management plans, the different types of loans and financing products, as well as the best companies to help guide you along the way. Similarly, Ohio residents have access to professional solutions, with free and nonprofit assistance also available in the region. Finally, Illinois has several local and nationwide firms that can negotiate with creditors on your behalf, create repayment plans, and help determine if declaring bankruptcy is an appropriate solution.

Remember, speaking with a professional ensures the right products are matched with your needs. For more options across other cities and states, please consult our list of debt management firms that can help keep you on track.

by Alex Demolitor | Oct 24, 2025 | Definitions

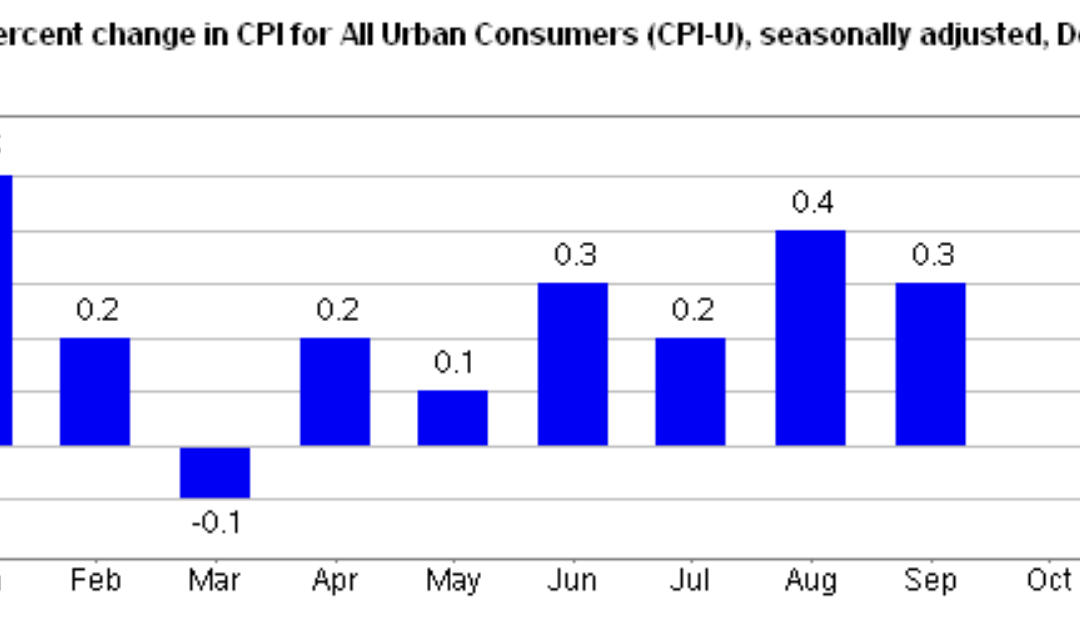

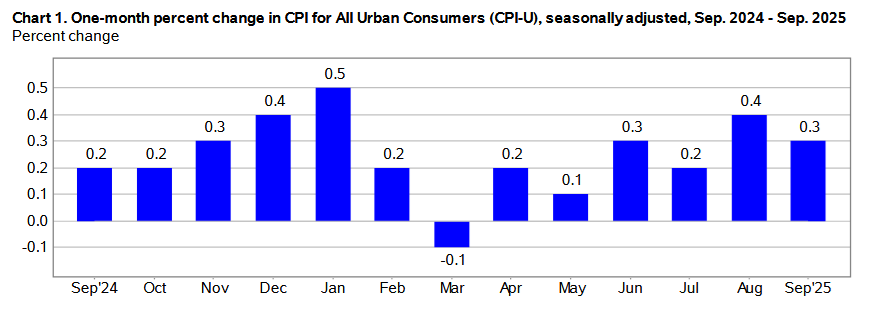

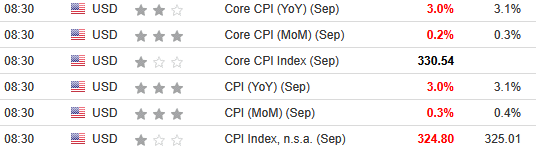

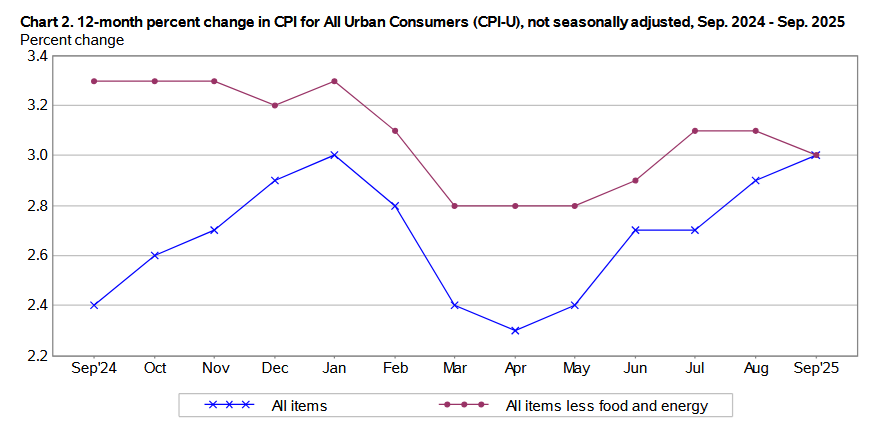

The September 2025 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation increased by 0.3% for the month, down from 0.4% in August. These data were released at 8:30 am EST on October 24, 2025, by the Bureau of Labor Statistics (BLS). Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 3.0%, up from 2.9% in August.

The results missed economists’ consensus estimates. The table below is courtesy of Investing.com. The left column represents September’s figures, while the right column represents forecasters’ expectations. As you can see, the red metrics highlight how inflation was cooler than anticipated.

After cutting interest rates in September, Fed Chairman Jerome Powell noted on Oct. 14 that “Some signs have begun to emerge that liquidity conditions are gradually tightening, including a general firming of repo rates along with more noticeable but temporary pressures on selected dates. The Committee’s plans lay out a deliberately cautious approach to avoid the kind of money market strains experienced in September 2019.”

In other words, with the Fed still selling bonds and liquidity declining in money markets, commercial banks have tapped their reserves to help with short-term funding. The issues could result in the Fed ending quantitative tightening on Oct. 29, which would be another dovish development.

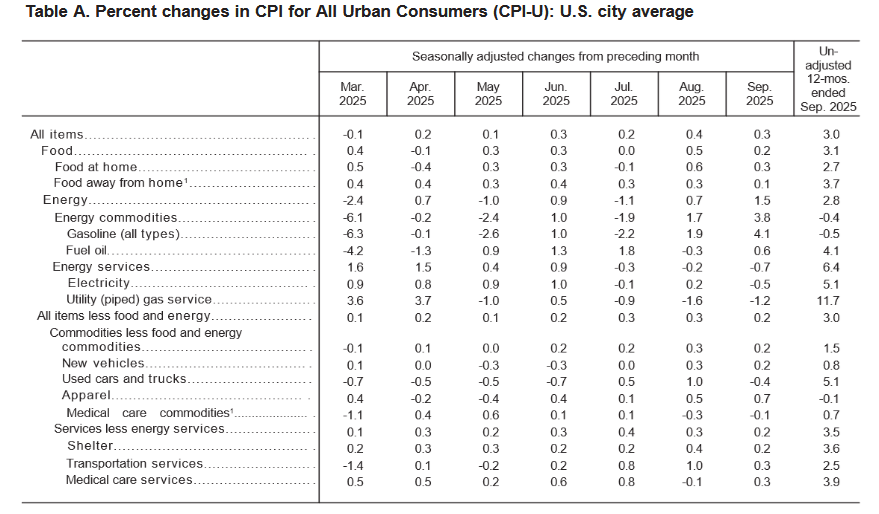

Apparel was the primary outlier in September, rising by 0.7% MoM. Gasoline prices also rose by 4.1% MoM after increasing by 1.9% in August. Core inflation (which excludes the impacts of food and energy), rose by 0.2% in September, slipping from the 0.3% jumps in July and August.

Food Prices

The food index rose by 0.2% MoM in September following a 0.5% rise in August. Four of the six major grocery store food indexes increased, while one was flat, and the other decreased:

- Cereals and bakery products (+0.7%)

- Meats, poultry, fish, and eggs (+0.3%)

- Dairy and related products (-0.5%)

- Fruits and vegetables (+0.0%)

- Nonalcoholic beverages (+0.7%)

- Other food at home (+0.5%)

Surprisingly, the food away from home index rose by 0.1%, which was its lowest reading in several months and signals a slowdown in restaurant inflation.

Energy Prices

The energy index jumped by 1.5% in September following a 0.7% rise in August. Gasoline prices increased by 4.1%, while electricity and natural gas prices fell by 0.5% and 1.2%, respectively.

Core CPI

The September core CPI rose by 0.2% month-over-month and 3.0% Y-o-Y. Below is an itemized breakdown of the main price fluctuations seen in the core CPI reading:

- Shelter index: (+0.2%) [August: +0.4%]

- Rent index: (+0.2%) [August: +0.3%]

- Owners’ equivalent rent: (+0.1%) [August: +0.4%]

- Motor vehicle insurance: (-0.4%) [August: +0.0%]

- Medical care services: (+0.3%) [August: -0.1%]

- Physician services: (-0.1%) [August: +0.3%]

- Hospital services: (+0.3%) [August: +0.0%]

- Airline fares: (+2.7%) [August: +5.9%]

Seasonally Unadjusted CPI

Before seasonal adjustments, the CPI-U for September 2025 increased by 3.0% Y-o-Y to an index level of 324.800. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

Economic Challenges

While the U.S. government shutdown has paused the release of most public economic data, private sources still indicate a deteriorating outlook.

For example, there has been a recent string of bankruptcies among large subprime auto lenders, as consumers fail to make their loan payments. An Oct. 17 article from The Guardian noted:

“Car owners were found to be missing payments at the highest rate in more than 30 years in January, when a Fitch Ratings index monitoring the share of subprime auto borrowers at least 60 days past due on their loans hit 6.5%.” In addition: “Car repossessions surged to their highest level since 2009 last year, according to Cox, with 1.73m vehicles seized, up 16% from the year prior and 43% from 2022.”

Moreover, the situation is even worse now. And with interest rates still relatively elevated and stress beginning to show in riskier areas of consumer credit, problems in the auto loan market could spread if the economy continues to weaken.

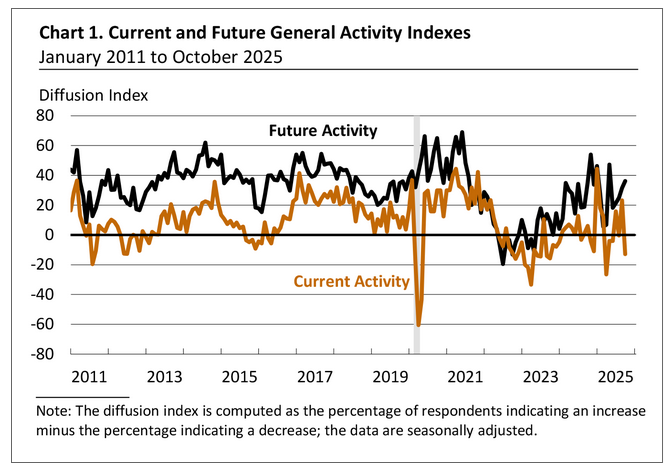

To that point, the Philadelphia Fed released its Manufacturing Business Outlook Survey on Oct. 16. And while sentiment regarding future activity remained positive, “The survey’s index for current general activity fell significantly and turned negative, more than offsetting last month’s increase.”

“The diffusion index for current general activity dropped 36 points to -12.8 in October, its lowest reading since April. Twenty-five percent of the firms reported decreases in general activity this month (up from 17 percent last month), while 12 percent reported increases (down from 40 percent).”

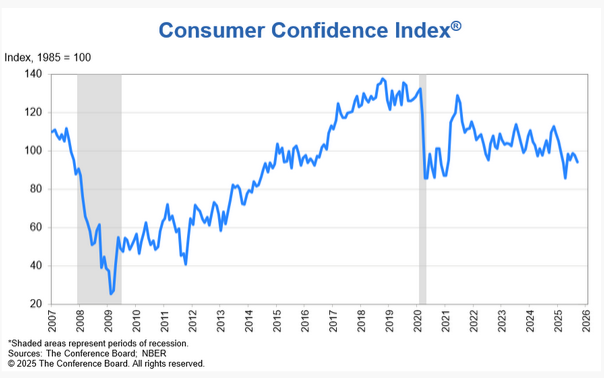

Finally, The Conference Board released its latest Consumer Confidence report on Sep. 30. Stephanie Guichard, Senior Economist, Global Indicators at The Conference Board, said:

“Consumer confidence weakened in September, declining to the lowest level since April 2025. The present situation component registered its largest drop in a year. Consumers’ assessment of business conditions was much less positive than in recent months, while their appraisal of current job availability fell for the ninth straight month to reach a new multiyear low.”

Likewise, “there was a rise in mentions of jobs and employment to a level unseen since August 2024. The comments were mostly negative, especially when referring to the current situation; there were a few positive comments which mostly conveyed hopes that things would get better.”

So, while inflation uncertainty has declined somewhat, the second half of the FOMC’s dual mandate — maximum employment — remains challenged, and could dominate if the recent trends persist. Consequently, lower interest rates may be the path of least resistance until the labor market shows more signs of life.

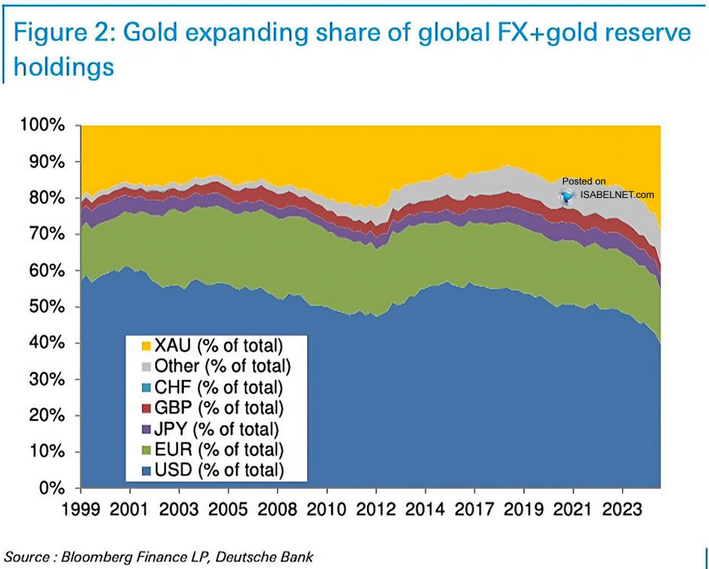

Turning to the financial markets, gold has been on a tear and surpassed $4,000 an ounce. And while volatility has increased, the long-term fundamentals of higher fiscal deficits, inflation, and a weaker U.S. dollar remain in place. Therefore, the theme of global central banks replacing FX reserves with gold should continue for the foreseeable future.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Please seek the guidance of a financial advisor before making any investment decision.

Furthermore, if credit concerns have increased alongside the economic uncertainty, there are solutions. TurboDebt is a debt settlement company that negotiates with creditors on your behalf to help lower your financial obligations. The firm focuses on unsecured claims, and you can book a free consultation to determine if the process is right for you.

For tax-related claims, an accredited lawyer can help guide you in the right direction and determine which services fit your needs. Our extensive guide breaks down how the process works and the options available.

Last, if your business is looking for the right financial partner, Grasshopper Bank is a digital institution providing a full suite of products like high-interest savings accounts, low-fee checking accounts, small business administration (SBA) loans, senior secured loans, lines of credit, and other types of commercial loans.

Remember, speaking with a professional ensures the right products are matched with your needs. For more options, please consult our list of debt management firms that can help keep you on track.

by Alex Demolitor | Sep 11, 2025 | Definitions

The August 2025 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation increased by 0.4% for the month, double the 0.2% rise in July. These data were released at 8:30 am EST on September 11, 2025, by the Bureau of Labor Statistics (BLS). Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 2.9%, up from 2.7% in July.

The results aligned near economists’ consensus estimates. The table below is courtesy of Investing.com. The left column represents August’s figures, while the right column represents forecasters’ expectations. As you can see, core came in as expected, while the monthly headline figure outperformed.

While Fed Chairman Jerome Powell hinted at a potential rate cut later this month, the FOMC has been cautious in its approach to monetary policy. Rather than encourage another round of inflation by cutting rates prematurely, the committee has prioritized price stability, and today’s results did little to eliminate the concerns.

Used cars and trucks were the primary outliers, with both rising by 1.0% MoM. Gasoline prices also rose by 1.9% MoM after declining by 2.2% in July. Core inflation (which excludes the impacts of food and energy), rose by 0.3% in August, matching the 0.3% from July, and slightly outperforming the 0.2% in June.

Food Prices

The food index rose by 0.5% MoM in August following a flat reading in July. All six major grocery store food indexes increased:

- Cereals and bakery products (+0.1%)

- Meats, poultry, fish, and eggs (+1.0%)

- Dairy and related products (+0.1%)

- Fruits and vegetables (+1.6%)

- Nonalcoholic beverages (+0.6%)

- Other food at home (+0.1%)

Maintaining its momentum, the food away from home index rose by 0.3%, mirroring July, and slightly underperforming the 0.4% increase in June.

Energy Prices

The energy index jumped by 0.7% in August after declining by 1.1% in July. Gasoline prices increased by 1.9%, electricity by 0.2%, while natural gas dropped by 1.6%.

Core CPI

The August core CPI rose by 0.3% month-over-month and 3.1% Y-o-Y. Below is an itemized breakdown of the main price fluctuations seen in the core CPI reading:

- Shelter index: (+0.4%) [July: +0.2%]

- Rent index: (+0.3%) [July: +0.3%]

- Owners’ equivalent rent: (+0.4%) [July: +0.3%]

- Motor vehicle insurance: (+0.0%) [July: +0.1%]

- Medical care services: (-0.1%) [July: +0.8%]

- Physician services: (+0.3%) [July: +0.2%]

- Hospital services: (+0.0%) [July: +0.5%]

- Airline fares: (+5.9%) [July: +4.0%]

Seasonally Unadjusted CPI

Before seasonal adjustments, the CPI-U for August 2025 increased by 2.9% Y-o-Y to an index level of 323.976. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

Cuts Coming?

While the U.S. labor market has been weakening for some time, conflicting data had the FOMC preaching patience. However, with several sources converging recently and signaling a slowdown, a September rate cut is likely a done deal.

For example, the BLS released its latest U.S. nonfarm payrolls report on Sep. 5. The economy added 22,000 net new jobs (well below expectations), and the report stated:

“The change in total nonfarm payroll employment for June was revised down by 27,000, from +14,000 to -13,000, and the change for July was revised up by 6,000, from +73,000 to +79,000. With these revisions, employment in June and July combined is 21,000 lower than previously reported.”

Thus, while a 21,000 miscount may not seem like much, the key revelation was that June’s revision to -13,000 was the first net negative print since 2021.

To that point, the BLS reported on Sep. 9 that annual revisions showed the U.S. added 911,000 fewer jobs over the last 12 months than previously reported. An excerpt read:

“The preliminary estimate of the Current Employment Statistics (CES) national benchmark revision to total nonfarm employment for March 2025 is -911,000 (-0.6 percent), the U.S. Bureau of Labor Statistics reported today. The annual benchmark revisions over the last 10 years have an absolute average of 0.2 percent of total nonfarm employment.”

Finally, The Conference Board revealed on Aug. 26 that Americans’ assessment of the labor market continued to deteriorate. Stephanie Guichard, Senior Economist, Global Indicators at The Conference Board, said, “Consumer confidence dipped slightly in August but remained at a level similar to those of the past three months. The present situation and the expectation components both weakened. Notably, consumers’ appraisal of current job availability declined for the eighth consecutive month.”

More importantly, The Conference Board’s ‘labor differential’ metric soared to a new cycle high.

To explain, the gray line above tracks the U.S. unemployment rate, while the red line above tracks the labor differential. When the red line rises, it means that more survey respondents believe that jobs are “hard to get” versus “plentiful.”

Furthermore, with a rising red line often a precursor to a higher unemployment rate, the sharp spike on the right side of the chart should be a cause for concern for the FOMC.

All in all, while inflation uncertainty remains high, the second half of the FOMC’s dual mandate — maximum employment — remains challenged. Therefore, a continuation of the trend should result in more rate cuts in the months ahead.

As the drama unfolds, gold is the clear winner. The yellow metal hit another record high in September, and Goldman Sachs expects more upside in the months and years ahead.

To explain, the blue line above tracks the consolidated gold holdings of global central banks, while the red dashed line above tracks Goldman Sachs’ projection over the next several months.

As you can see, continued demand from the largest buyers should help keep the gold price elevated for the foreseeable future.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Please seek the guidance of a financial advisor before making any investment decision.

In addition, if credit concerns have increased alongside the economic uncertainty, there are solutions. American Debt Relief provides debt settlement services, including negotiating with creditors to help eliminate or reduce the monthly payments on your unsecured debts like credit cards, medical bills, and personal loans. Similarly, Money Management International can help lower your interest rates, remove late payment fees, and negotiate lump sum settlements. Services are also available for student loans, bankruptcy, disaster recovery, homebuying, reverse mortgages, and military families.

Last, CreditAssociates can help you become debt-free in as little as 24–36 months. There are no upfront fees, but the group only provides assistance with unsecured debts and some business loans.

Remember, speaking with a professional can help you avoid bankruptcy and protect your credit score. For more options, please consult our list of debt management firms that can help get you back on track.