by Alex Demolitor | Apr 10, 2025 | Definitions

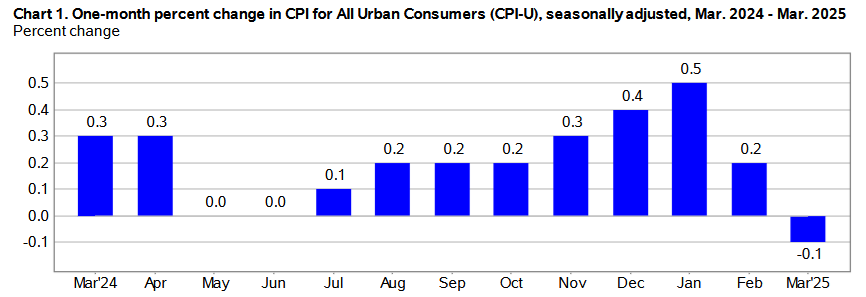

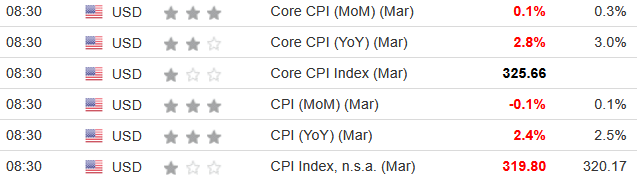

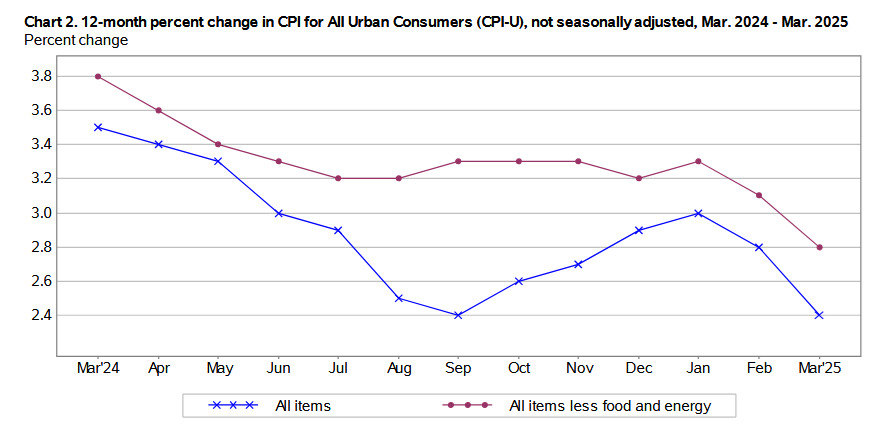

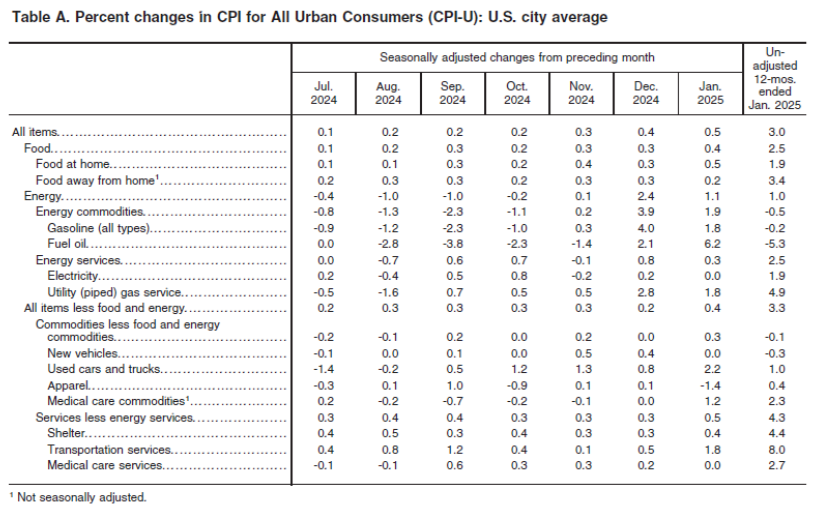

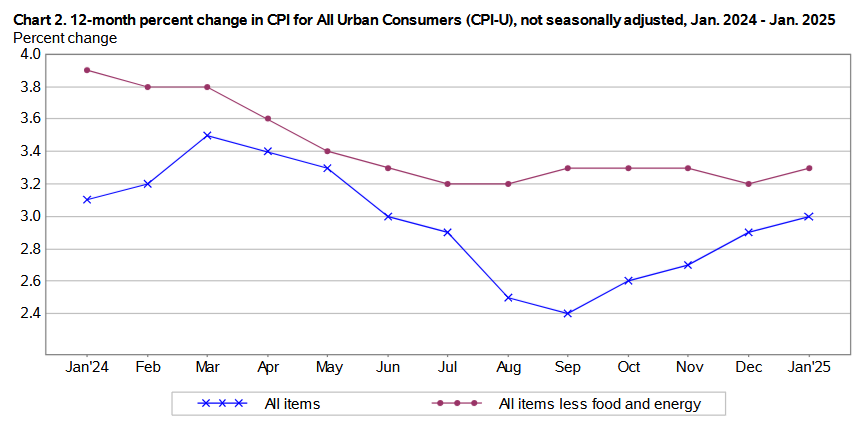

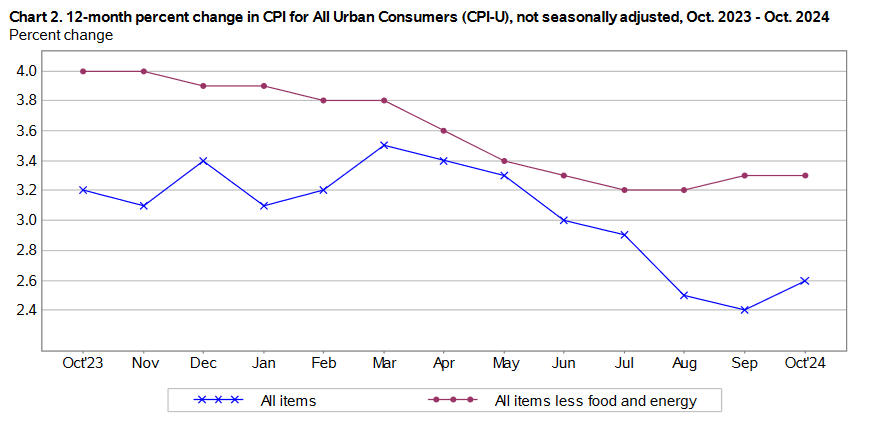

The March 2025 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation declined by 0.1% for the month, reversing February’s 0.2% rise. These data were released at 8:30 am EST on Thursday, April 10, 2025, by the Bureau of Labor Statistics. Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 2.4%, a continued deceleration from 2.8% in February, 3.0% in January, and 2.9% in December.

The downside surprise was more welcome news, as the results missed economists’ consensus estimates. The table below is courtesy of Investing.com. The left column represents March’s figures, while the right column represents forecasters’ expectations. As you can see, the red metrics were weaker than anticipated.

Despite that, Fed Chairman Jerome Powell has maintained a cautious outlook and said on Apr. 4:

“While uncertainty remains elevated, it is now becoming clear that the tariff increases will be significantly larger than expected. While tariffs are highly likely to generate at least a temporary rise in inflation, it is also possible that the effects could be more persistent. We are well positioned to wait for greater clarity before considering any adjustments to our policy stance. It is too soon to say what will be the appropriate path for monetary policy.”

As a result, while the data has cooperated recently, Powell still prefers further evidence of disinflation to warrant more rate cuts.

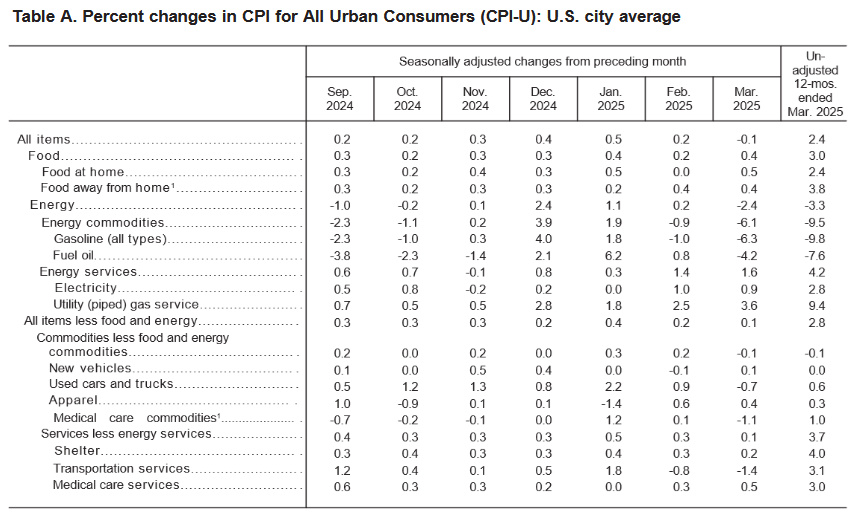

Gasoline, transportation services, and used cars and trucks drove March’s downside momentum, while shelter also slowed to 0.2% MoM.

Core inflation (which excludes the impacts of food and energy), rose by 0.1% in March, down from 0.2% in February and 0.4% in January. The indexes for airline fares, motor vehicle insurance, and recreation were among the primary laggards.

Food Prices

The food index jumped by 0.4% in March, after slowing to 0.2% in February. Although, two of the six major grocery store food indexes realized deflation:

- Cereals and bakery products (-0.1%)

- Meats, poultry, fish, and eggs (+1.3%)

- Dairy and related products (+1.0%)

- Fruits and vegetables (-0.5%)

- Nonalcoholic beverages (+0.6%)

- Other food at home (+0.5%)

Likewise, the food away from home index rose by 0.4%, as restaurant inflation remains resilient.

Energy Prices

The energy index fell by 2.4% in March, after rising by 0.2% in February and 1.1% in January. Gasoline prices sunk by 6.3%, while natural gas and electricity inflation jumped by 3.6% and 0.9%.

Core CPI

The March core CPI rose by 0.1% month-over-month and 2.8% Y-o-Y. Below is an itemized breakdown of the main price fluctuations seen in the core CPI reading:

- Shelter index: (+0.2%) [February: +0.3%]

- Rent index: (+0.3%) [February: +0.3%]

- Owners’ equivalent rent: (+0.4%) [February: +0.3%]

- Motor vehicle insurance: (-0.8%) [February: +0.3%]

- Medical care services: (+0.5%) [February: +0.3%]

- Physician services: (+0.3%) [February: +0.4%]

- Hospital services: (+1.1%) [February: +0.1%]

- Airline fares: (-5.3%) [February: -4.0%]

Seasonally Unadjusted CPI Data for March

Before seasonal adjustments, the CPI-U for March 2025 increased by 2.4% Y-o-Y to an index level of 319.799. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

Who Blinks First?

Although Powell has preached patience when it comes to future rate cuts, the economic backdrop has become more precarious. With trade wars and stock market volatility intensifying, the sour sentiment could weigh on corporations’ investment decisions and eventually result in higher unemployment. As a result, the second half of the Fed’s dual mandate could dominate the longer the uncertainty persists.

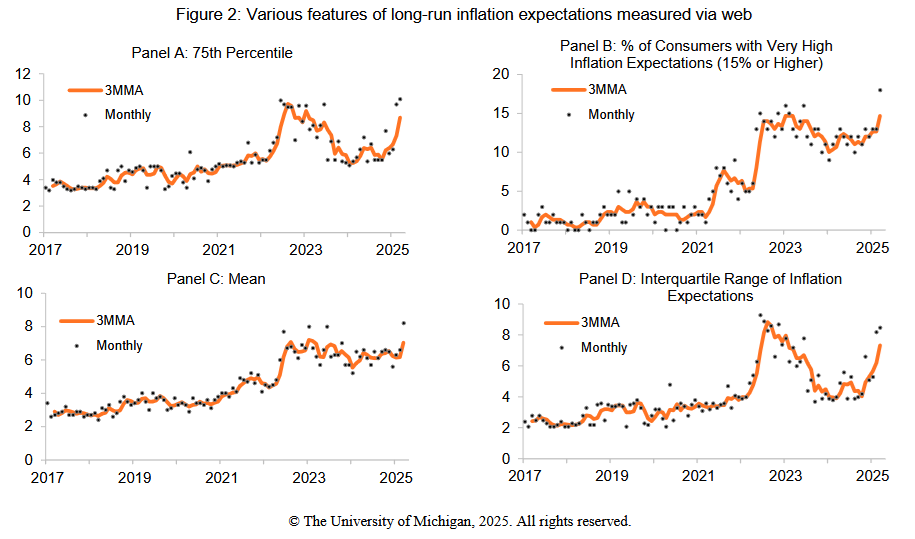

Furthermore, the dichotomy in inflation expectations could have Powell looking in the wrong direction. For example, the University of Michigan’s latest Consumer Sentiment Report showed a material rise in Americans’ inflation fears. An excerpt read:

“As of March 2025, long-run expectations have climbed sharply for three consecutive months and are now comparable to the peak readings from the post-pandemic inflationary episode. They exhibit substantial uncertainty, particularly in light of frequent developments and changes with economic policy.”

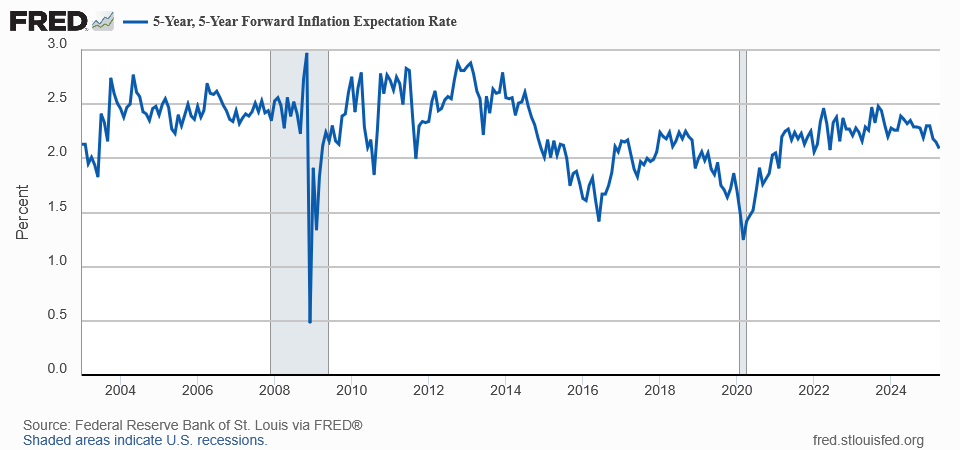

Conversely, the 5y5y tells a different story. For context, the metric measures institutional investors’ five-year inflation expectation five years from today. If you analyze the right side of the chart below, you can see that the 5y5y has declined considerably in 2025 and remains near the Fed’s 2% long-run target.

Add it all up, and Powell has to decide whether he believes consumers or investors assessment of future inflation.

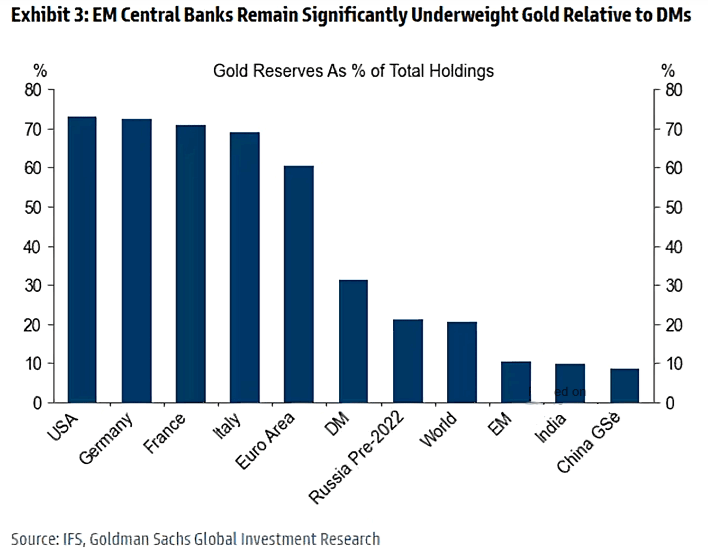

In the meantime, while stocks have gyrated, gold continues to outperform. And while developed-market central banks have large gold reserves, emerging market purchases could be the next catalyst to push prices higher.

The Goldman Sachs chart below shows how EM central banks have relatively small gold holdings. But, if they follow their DM counterparts and increase their allocations, the gold price could shine even brighter in the months ahead.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Remember, seek the guidance of a financial advisor before making any investment decision.

In addition, if debt troubles have increased alongside the economic uncertainty, you’re not alone. Speaking with a professional can help you avoid bankruptcy and protect your credit score. To learn more, consult our list of debt management firms that can help get you back on track.

by Alex Demolitor | Mar 12, 2025 | Definitions

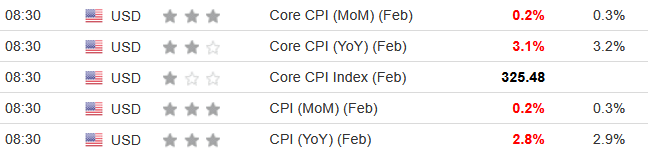

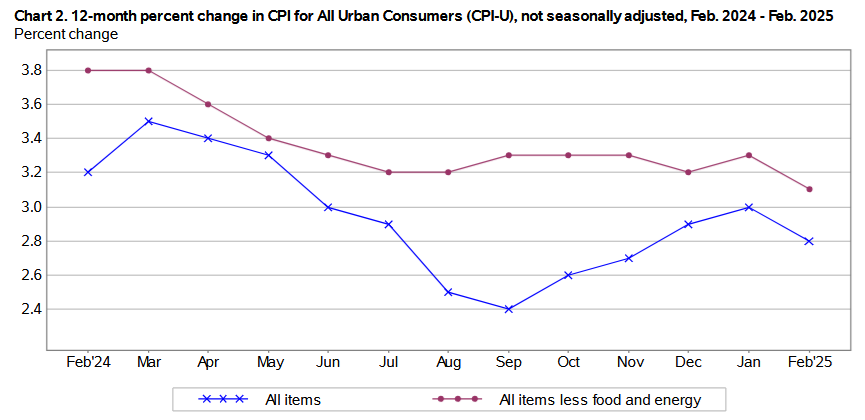

The February 2025 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation increased by 0.2% for the month, a drop from January’s 0.5% rise. These data were released at 8:30 am EST on Wednesday, March 12, 2025, by the Bureau of Labor Statistics. Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 2.8%, falling from 3.0% in January and 2.9% in December.

The downside surprise was welcome news, as the results missed economists’ consensus estimates. The table below is courtesy of Investing.com. The left column represents February’s figures, while the right column represents forecasters’ expectations. As you can see, the red metrics were weaker than anticipated.

Despite that, Fed Chairman Jerome Powell has maintained a wait-and-see approach to rate cuts. On Mar. 7, he said, “The U.S. economy continues to be in a good place. We do not need to be in a hurry and are well-positioned to wait for greater clarity.”

“The path to sustainably returning inflation to our target has been bumpy, and we expect that to continue,” Powell said. “We see ongoing progress in categories that remain elevated, such as housing services and the market-based components of non-housing services.”

As a result, while he noted the “uncertainty” around tariffs and U.S. immigration policy, patience is his preferred approach for the time being.

Used cars and trucks and utility pipelines were primary outliers on the upside this month, while gasoline and transportation services were noticeably weak.

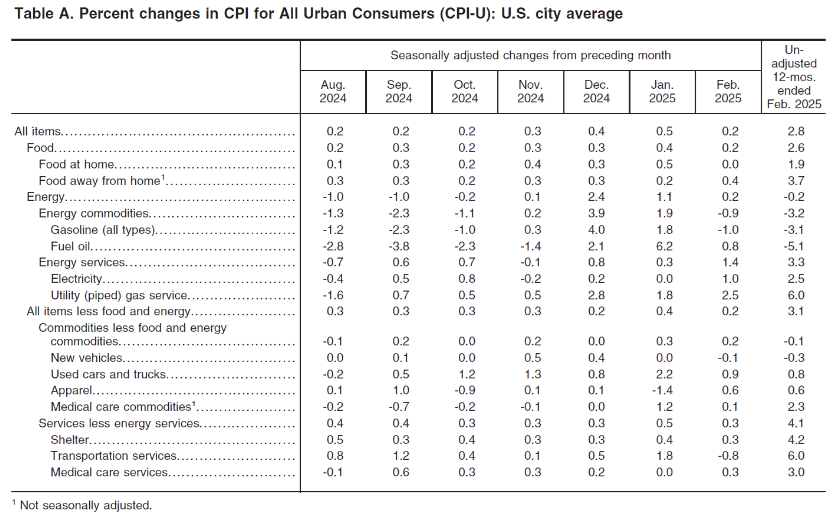

Core inflation (which excludes the impacts of food and energy), rose by 0.2% in February, down from 0.4% in January. And even with the welcome deceleration in shelter — dropping to 0.3% in February from 0.4% in January — the index accounted for “nearly half of the monthly all items increase.”

Food Prices

The food index slowed to 0.2% in February, and four of the six major grocery store food indexes realized deflation:

- Cereals and bakery products (+0.4%)

- Meats, poultry, fish, and eggs (+1.6%)

- Dairy and related products (-1.0%)

- Fruits and vegetables (-0.5%)

- Nonalcoholic beverages (-0.5%)

- Other food at home (-0.5%)

Conversely, the food away from home index rose by 0.4% (surpassing January’s 0.2% rise), as restaurant inflation accelerated in February.

Energy Prices

The energy index rose by 0.2% in February, down from 1.1% in January. Gasoline prices fell by 1%, while natural gas and electricity inflation jumped by 2.5% and 1%.

Core CPI February 2025

The February core CPI rose by 0.2% month-over-month and 3.1% Y-o-Y. Below is an itemized breakdown of the main price fluctuations seen in the core CPI reading:

- Shelter index: (+0.3%) [January: +0.4%]

- Rent index: (+0.3%) [January: +0.3%]

- Owners’ equivalent rent: (+0.3%) [January: +0.3%]

- Motor vehicle insurance: (+0.3%) [January: +2.0%]

- Medical care services: (+0.3%) [January: +0.0%]

- Physician services: (+0.4%) [January: +0.1%]

- Hospital services: (+0.1%) [January: +0.9%]

- Airline fares: (-4.0%) [January: +1.2%]

Seasonally Unadjusted CPI Data for February 2025

Before seasonal adjustments, the CPI-U for February 2025 increased by 2.8% Y-o-Y to an index level of 319.082. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

Behind the Curve?

With the Fed focused on tariffs and U.S. fiscal policy, some analysts believe the Committee’s unwillingness to cut interest rates could backfire in the future. If the economy is weaker than it anticipates, a ‘behind the curve’ Fed implies that interest rates are too high relative to the fundamental backdrop.

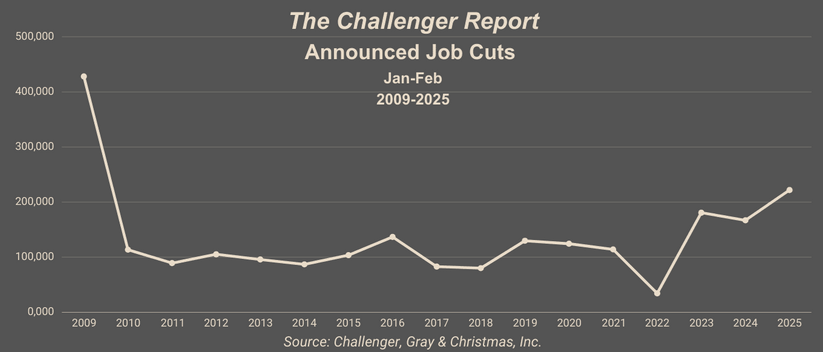

As an unsettling example, Challenger, Gray, and Christmas noted on Mar. 6 that “Job Cuts Surge on DOGE Actions, Retail Woes; Highest Monthly Total Since July 2020.”

The report stated:

“U.S.-based employers announced 172,017 job cuts in February, the highest total for the month since 2009 when 186,350 job cuts were recorded. It is the highest monthly total since July 2020 when 262,649 cuts were announced….

“February’s total is a 245% increase from the 49,795 cuts announced one month prior. It is a 103% increase from the 84,638 cuts announced in the same month last year. So far this year, employers have announced 221,812 job cuts, the highest year-to-date (YTD) total since 2009 when 428,099 job cuts were planned.”

Likewise, Truflation estimates the U.S. CPI is closer to 1.32% Y-o-Y based on its data, and the reading has declined materially in 2025. Thus, if the forecast proves prescient and the labor market weakens, a major shift in rate-cut expectations could unfold in the months ahead.

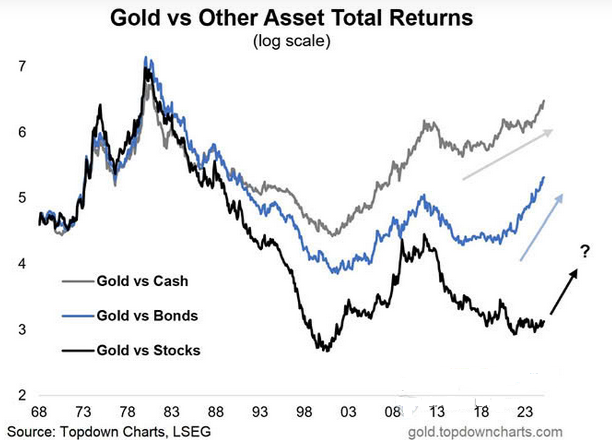

In the meantime, while stocks have been crushed recently, gold continues to shine bright. In fact, after years of underperformance, the yellow metal is now outperforming cash, bonds, and to a lesser degree, stocks. As such, it’s an excellent diversifier during uncertain periods.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Remember, seek the guidance of a financial advisor before making any investment decision.

by Alex Demolitor | Feb 12, 2025 | Definitions

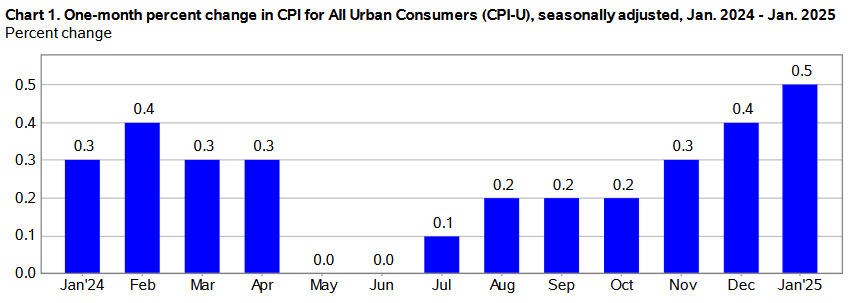

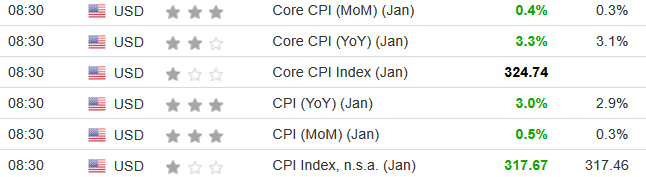

The January 2025 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation increased by 0.5% for the month, surpassing December’s 0.4% rise. These data were released at 8:30 am EST on Wednesday, February 12, 2025, by the Bureau of Labor Statistics. Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 3.0%, up from 2.9% in December and 2.7% and 2.6% in November and October.

The magnitude of the strength was largely unexpected, as the results easily surpassed economists’ consensus estimates. The table below is courtesy of Investing.com. The left column represents January’s figures, while the right column represents forecasters’ expectations. As you can see, the green metrics highlight January’s outperformance.

The data is likely an unwelcome sign for Fed Chairman Jerome Powell, as he’s shifted his stance in a hawkish direction recently. He said on Feb. 11:

“With our policy stance now significantly less restrictive than it had been and the economy remaining strong, we do not need to be in a hurry to adjust our policy stance. We know that reducing policy restraint too fast or too much could hinder progress on inflation.”

Thus, with January’s results amplifying that message, it could be a while before investors receive the rate cuts they desire.

Used cars and trucks were primary outliers again this month, with energy-related items like gasoline, fuel oil, and utilities also recording significant MoM increases. Likewise, food inflation was the highest in five months.

Core inflation (which excludes the impacts of food and energy), rose by 0.4% in January, a jump from December’s 0.2% print. And despite the decline in real-time rents, shelter rose by 0.4% MoM and accounted for “nearly 30 percent of the monthly all items increase.”

Food Prices

The food index hit a five-month high in January, and four of the six major grocery store food indexes increased:

- Cereals and bakery products (-0.4%)

- Meats, poultry, fish, and eggs (+1.9%)

- Dairy and related products (+0.3%)

- Fruits and vegetables (-0.5%)

- Nonalcoholic beverages (+0.9%)

- Other food at home (+0.3%)

In addition, the food away from home index rose by 0.2%, as restaurant inflation slowed in January.

Energy Prices

The energy index rose by 1.1% in January, with gasoline and natural gas up by 1.8%, respectively, while electricity was flat.

Core CPI January 2025

The January core CPI rose by 0.4% month-over-month and 3.3% Y-o-Y. Below is an itemized breakdown of the main price fluctuations seen in the core CPI reading:

- Shelter index: (+0.4%) [December: +0.3%]

- Rent index: (+0.3%) [December: +0.3%]

- Owners’ equivalent rent: (+0.3%) [December: +0.3%]

- Motor vehicle insurance: (+2.0%) [December: +0.4%]

- Medical care services: (+0.0%) [December: +0.2%]

- Physician services: (+0.1%) [December: +0.1%]

- Hospital services: (+0.9%) [December: +0.2%]

- Airline fares: (+1.2%) [December: +3.9%]

Seasonally Unadjusted CPI Data for January 2025

Before seasonal adjustments, the CPI-U for January 2025 increased by 3.0% Y-o-Y to an index level of 317.671. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

Seeking Shelter

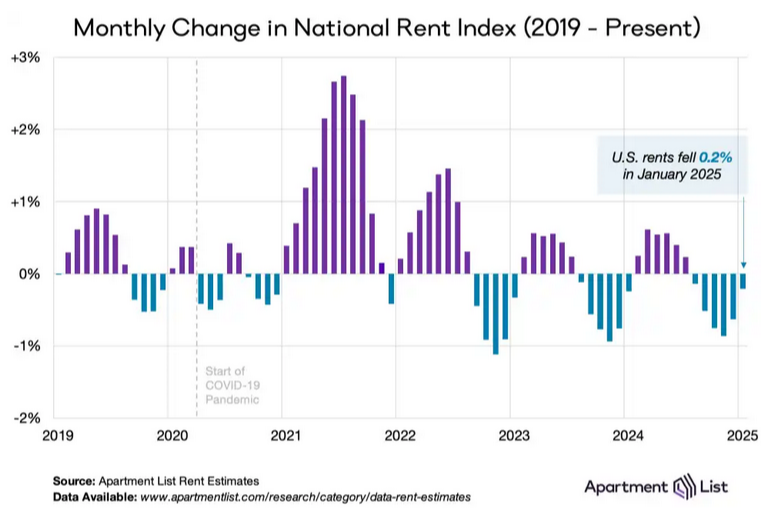

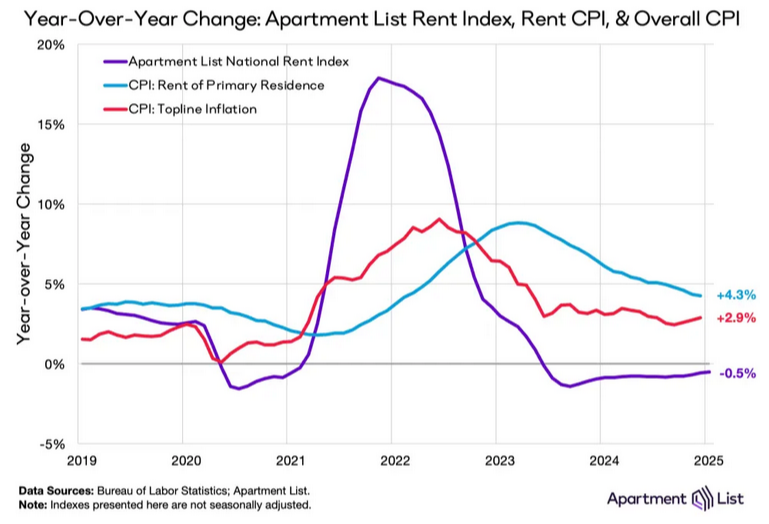

With inflation refusing to recede, the financial markets remain unnerved at the prospect of higher-for-longer interest rates. However, one sign of hope is the eventual decline of rental inflation.

The shelter CPI accounts for more than 30% of the headline CPI’s movement, and Apartment List noted on Jan. 27:

‘Our national rent index started the year with its sixth straight month-over-month decline, falling by 0.2 percent in January. Year-over-year growth also remains negative at -0.5 percent, but is slowly inching back toward positive territory.”

The report added:

“The Apartment List National Rent Index has proven to be a strong leading indicator of the CPI housing and rent components (collectively referred to as “shelter”), since our index captures price changes in new leases, which are only later reflected in price changes across all leases (what the CPI measures)….

“Despite the progress, shelter CPI remains elevated and is one of the key factors continuing to exert upward pressure on topline CPI. In fact, if you strip out shelter, the remainder of the CPI price basket has increased by just 1.9 percent year-over-year as of December, right in line with the Fed’s long-term 2 percent inflation target. As shelter inflation continues to trend down, it will help improve the overall inflation picture.”

Consequently, while January’s CPI print worsened the inflation outlook, there are some positive signs that could flip the script in the months ahead.

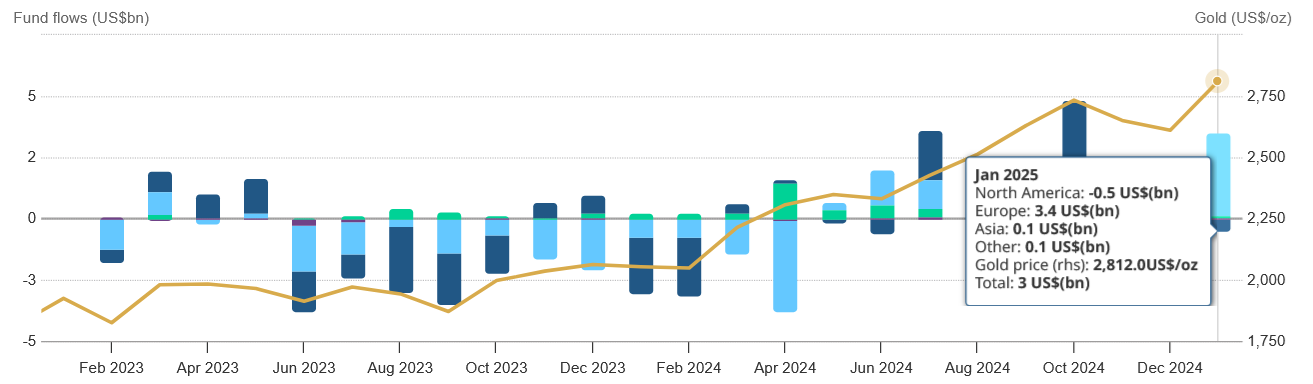

In the meantime, while some assets have suffered recently, as higher interest rates on risk-free assets like Treasury bonds make risky assets like stocks seem less attractive, gold has shined bright. Moreover, the World Gold Council noted on Feb. 10 that gold’s “record-breaking performance attracted investor attention.”

An excerpt read:

“European funds saw their largest monthly inflow since March 2022, adding US$3.4bn during January. UK and Germany dominated inflows. In the UK, government bond yields fell notably during the second half of January as easing inflation pressure and soft economic data prints raised investor expectations for rate cuts from the Bank of England during 2025. Reduced opportunity cost of holding gold, alongside a robust gold price performance, drove local investors into gold ETFs.”

As such, more upside could materialize as inflation, geopolitical uncertainty, and tariff concerns fester throughout 2025.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Remember, seek the guidance of a financial advisor before making any investment decision.

by Alex Demolitor | Jan 15, 2025 | Definitions

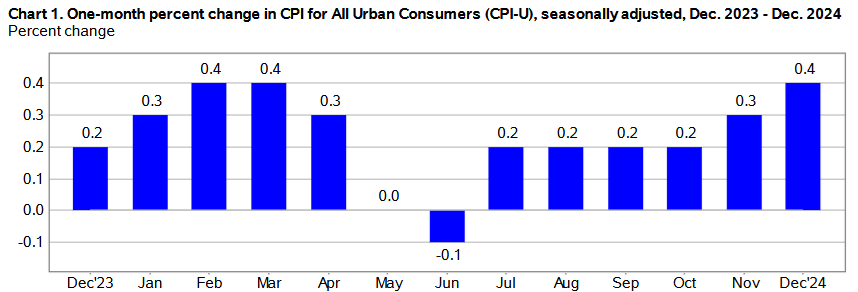

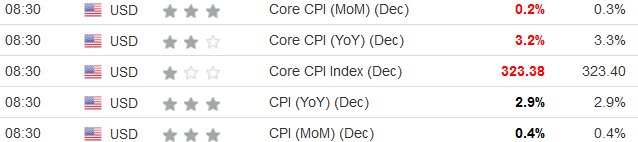

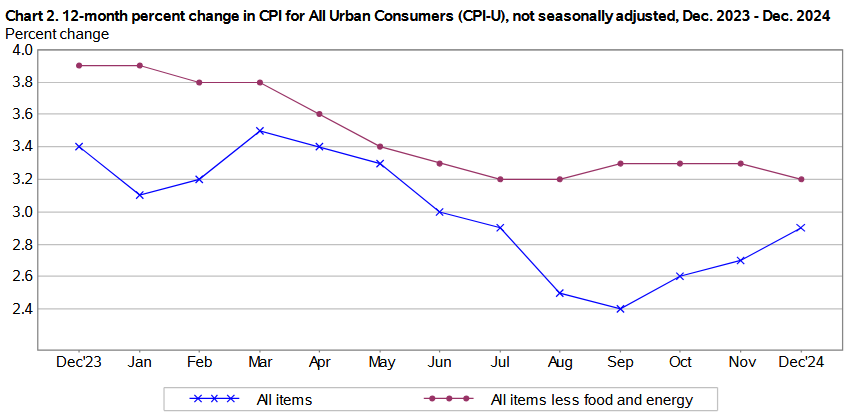

The December 2024 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation increased by 0.3% for the month, surpassing November’s 0.2% rise. These data were released at 8:30 am EST on Wednesday, January 15, 2025, by the Bureau of Labor Statistics. Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 2.9%, a rise from the 2.7% and 2.6% witnessed in November and October.

Despite the monthly acceleration, the results matched or missed economists’ consensus estimates. The table below is courtesy of Investing.com. The left column represents December’s figures, while the right column represents forecasters’ expectations. As you can see, a weaker-than-expected core CPI was the headliner.

The data may be a relief for FOMC Chairman Jerome Powell, as the committee shifted from a dovish labor-market-driven tone to a hawkish inflation-driven tone. He said during his post-meeting press conference on Dec. 18:

“Inflation itself is way down, but people are still feeling high prices. The best we can do for them is to get inflation back down to its target and keep it there so that people are earning, you know, big, real wage increases so that their, their wages are going up, their compensation is going up faster than inflation year upon year upon year. And that’s what will restore people’s good feeling about the economy. That’s what it will take, and that’s what we’re aiming for.”

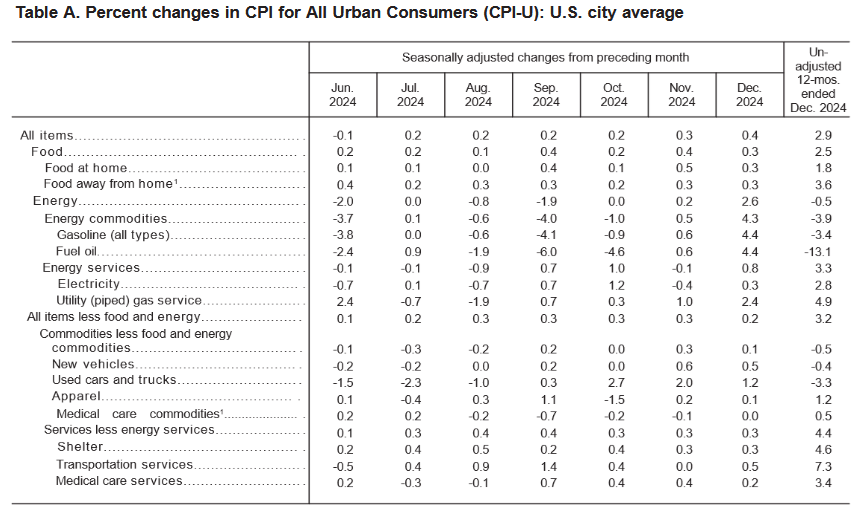

Used cars and trucks were the primary outlier again this month, with the segment rising by 1.2% MoM in December. Similarly, energy-related items like gasoline and utilities recorded significant increases.

Core inflation (which excludes the impacts of food and energy), rose by 0.2% in December, a decline from November’s 0.3% print. Moreover, with real-time rents down sharply on an annual basis, a weaker shelter component should aid the core CPI in the months ahead.

Food Prices

The food index slowed in December, rising by 0.3% versus 0.4% in November. Four of the six major grocery store food indexes increased:

- Cereals and bakery products (+1.2%)

- Meats, poultry, fish, and eggs (+0.6%)

- Dairy and related products (+0.2%)

- Fruits and vegetables (-0.1%)

- Nonalcoholic beverages (-0.4%)

- Other food at home (+0.3%)

In addition, the food away from home index rose by 0.3%, as restaurants priced their products in line with overall food inflation.

Energy Prices

The energy index rose by 2.6% in December, a noticeable jump from the 0.2% recorded in November. Gasoline and natural gas prices rose by 4.4% and 2.4%, respectively, while electricity rose by 0.3%.

Core CPI December 2024

The December core CPI rose by 0.2% month-over-month and 3.2% Y-o-Y. Below is an itemized breakdown of the main price fluctuations seen in the core CPI reading:

- Shelter index: (+0.3%) [November: +0.3%]

- Rent index: (+0.3%) [November: +0.2%]

- Owners’ equivalent rent: (+0.3%) [November: +0.2%]

- Motor vehicle insurance: (+0.4%) [November: +0.1%]

- Medical care services: (+0.2%) [November: +0.4%]

- Physician services: (+0.1%) [November: +0.3%]

- Hospital services: (+0.2%) [November: +0.0%]

- Airline fares: (+3.9%) [November: +0.4%]

Seasonally Unadjusted CPI Data for December 2024

Before seasonal adjustments, the CPI-U for December 2024 increased by 2.9% Y-o-Y to an index level of 315.605. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

Too Hawkish?

With the FOMC shifting its stance in a hawkish direction on Dec. 18, inflation had taken precedence over the labor market. Powell added:

“You saw in the SEP that risks and uncertainty around inflation we see as higher. Nonetheless, we see ourselves as still on track to continue to cut. I think the actual cuts that we make next year will not be because of anything we wrote down today. We’re, we’re going to react to data. That’s just the general sense of what the Committee thinks is likely to be appropriate.”

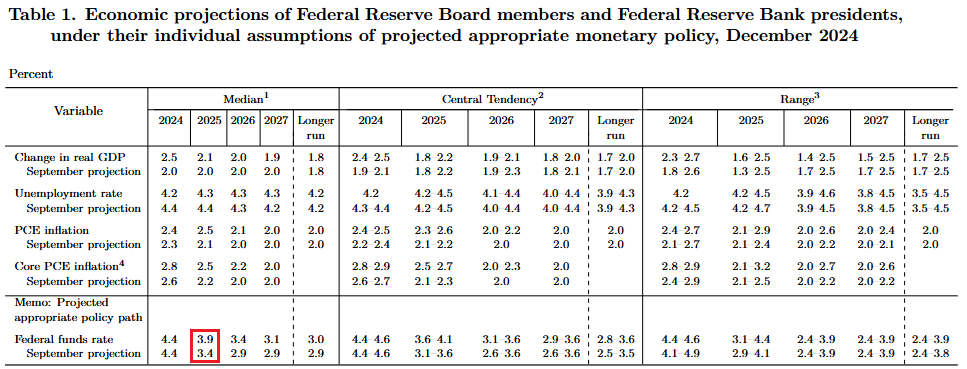

To explain, the FOMC releases its Summary of Economic Projections (SEP) four times per year, and include members’ forecasts for GDP growth, inflation, unemployment, and the federal funds rate (FFR).

If you analyze the red box below, you can see that the consensus estimate was for 100 basis points of rate cuts and a 3.4% FFR in 2025. But, with economic data outperforming, the FFR projection was increased to 3.9%, which means only 50 basis points of rate cuts.

Add it all up, and the hawkish shift implies stricter monetary policy throughout 2025. Yet, with the core CPI data underperforming today, more of the same could lead to a shift back to dovish projections in the months ahead.

In the meantime, asset prices have suffered recently, as higher interest rates on risk-free assets like Treasury bonds make risky assets like stocks, gold, and silver seem less appealing.

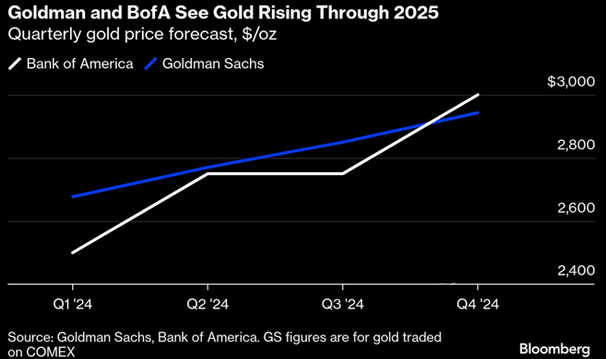

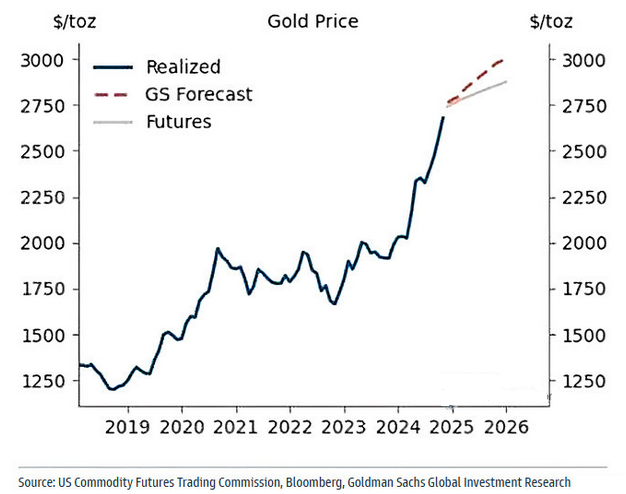

However, Goldman Sachs and Bank of America still expect the yellow metal to exceed $2,800 and post a new record high in 2025. If you analyze the Bloomberg chart below, you can see that both investment banks see gold maintaining its strength throughout the year.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Remember, seek the guidance of a financial advisor before making any investment decision.

by Alex Demolitor | Dec 11, 2024 | Definitions

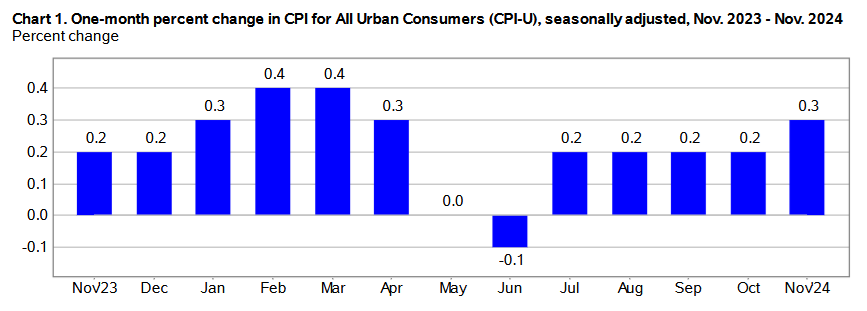

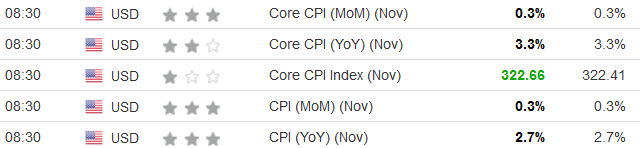

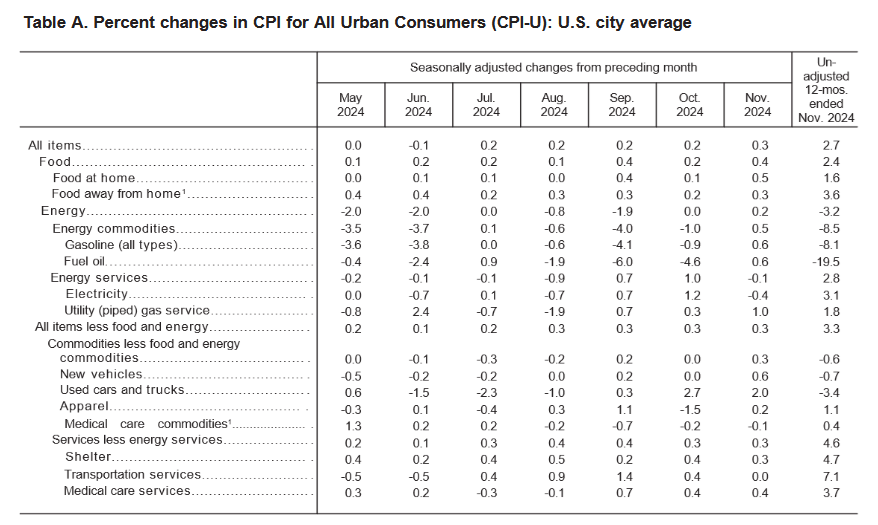

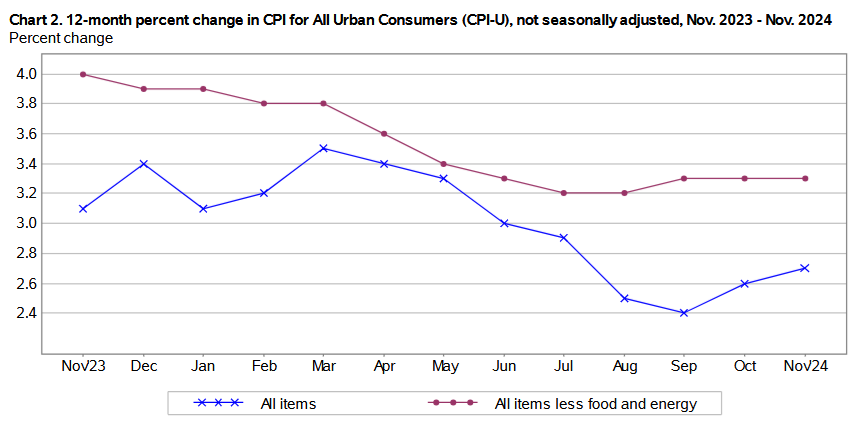

The November 2024 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation increased by 0.3% for the month, outperforming October’s 0.2% rise. These data were released at 8:30 am EST on Wednesday, December 11, 2024, by the Bureau of Labor Statistics. Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 2.7%, a rise from the 2.6% witnessed in October.

Although the CPI data exceeds the FOMC’s 2% target, the results aligned with economists’ estimates. The table below is courtesy of Investing.com. The left column represents November’s figures, while the right column represents forecasters’ expectations. As you can see, most metrics (marked in black) matched consensus predictions.

FOMC Chairman Jerome Powell should welcome the news, as the data supports the committee’s current trajectory. With economic data holding up and inflation behaving, Powell said on Nov. 14, “The economy is not sending any signals that we need to be in a hurry to lower rates. The strength we are currently seeing in the economy gives us the ability to approach our decisions carefully.”

As a result, while the FOMC is widely expected to cut interest rates by 25 basis points at next week’s meeting, Powell may maintain a gradual approach to monetary easing.

Used cars and trucks were the primary outlier this month, with the segment rising by 2% MoM in November. And outside of utilities (up by 1% MoM), no other metric increased by more than 0.6% MoM. Core inflation (which excludes the impacts of food and energy), rose by 0.3% in November, matching August, September, and October’s prints. However, shelter slowed to 0.3% MoM, down from 0.4% MoM in October.

Food Prices

The food index continued its upward trend, rising by 0.4% in November and doubling October’s 0.2% print. Four of the six major grocery store food indexes increased:

- Cereals and bakery products (-1.1%)

- Meats, poultry, fish, and eggs (+1.7%)

- Dairy and related products (-0.1%)

- Fruits and vegetables (+0.2%)

- Nonalcoholic beverages (+1.5%)

- Other food at home (+0.1%)

In addition, the food away from home index rose by 0.3%, a slight uptick from October’s 0.2% result.

Energy Prices

The energy index rose by 0.2% in November after recording a flat performance in October. Gasoline and natural gas prices rose by 0.6% and 1.0%, respectively, while electricity slumped by 0.4%.

Core CPI November 2024

The November core CPI rose by 0.3% month-over-month and 3.3% Y-o-Y. Below is an itemized breakdown of the main price fluctuations seen in the core CPI reading:

- Shelter index: (+0.3%) [October: +0.4%]

- Rent index: (+0.2%) [October: +0.3%]

- Owners’ equivalent rent: (+0.2%) [October: +0.4%]

- Motor vehicle insurance: (+0.1%) [October: -0.1%]

- Medical care services: (+0.4%) [October: +0.4%]

- Physician services: (+0.3%) [October: +0.5%]

- Hospital services: (+0.0%) [October: +0.5%]

- Airline fares: (+0.4%) [October: +3.2%]

Seasonally Unadjusted CPI Data for November 2024

Before seasonal adjustments, the CPI-U for November 2024 increased by 2.7% Y-o-Y to an index level of 315.493. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

No Rush to Cut?

With resilient economic data allowing Powell to take a patient approach to rate cuts, little occurred to disrupt his thesis this week.

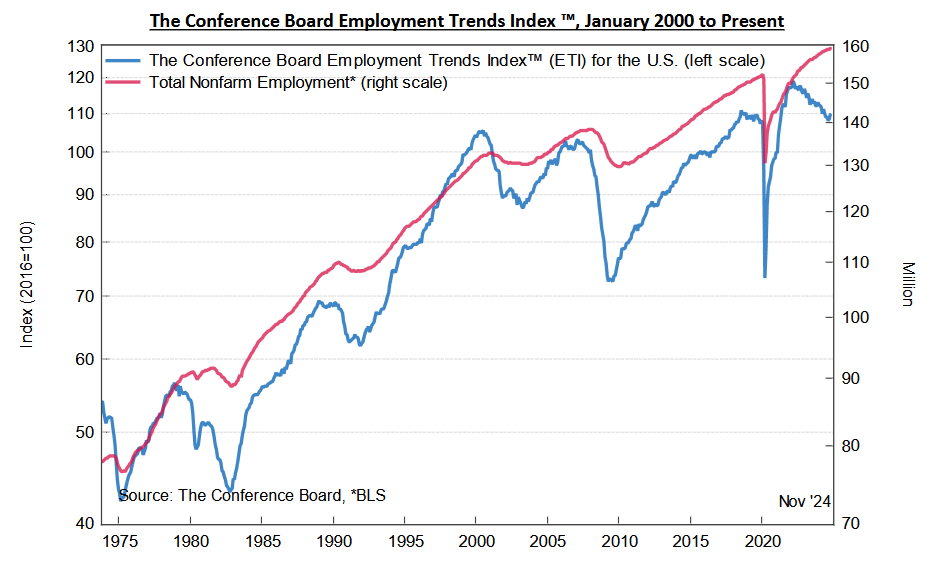

For example, The Conference Board released its Employment Trends Index (ETI) on Dec. 9. Economist Mitchell Barnes noted, “The ETI rose again in November, marking consecutive monthly gains for the first time in 2024. The increases in October and November add up to the largest two-month increase in the ETI since the torrid period of job gains in 2022 coming out of the pandemic.”

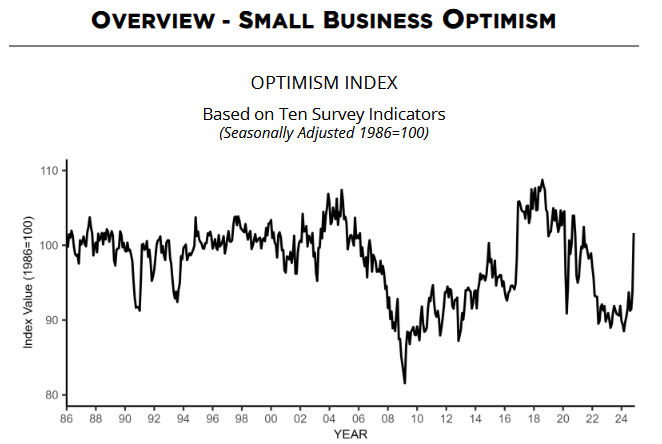

Similarly, the NFIB released its Small Business Optimism Index on Dec. 10. The report stated: “The NFIB Small Business Optimism Index rose by eight points in November to 101.7, after 34 months of remaining below the 50-year average of 98. This is the highest reading since June 2021. Of the 10 Optimism Index components, nine increased, none decreased, and one was unchanged.”

Add it all up, and there aren’t many catalysts to entice the FOMC to accelerate rate cuts. Consequently, interest rates should remain high until the U.S. economy showcases further weakness.

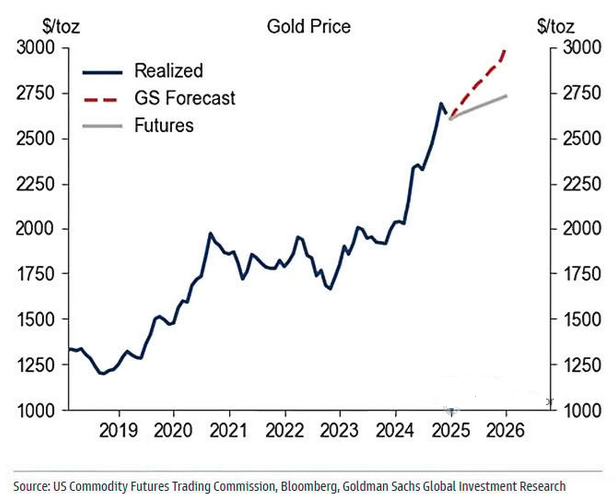

In the meantime, risk assets remain elevated, and gold continues to perform well despite a stronger U.S. dollar and elevated interest rates. On Dec. 2, Goldman Sachs reiterated its year-end 2025 price target of $3,000, with Commodities Strategist Lina Thomas writing, “Since 2022, gold prices have surged 40% even as US interest rates were climbing. That is very strange. Typically, higher interest rates make gold less attractive – because gold doesn’t pay any interest, unlike bonds.”

“That was a wake-up call for central banks worldwide. They began to diversify their reserves away from the dollar and into an asset no one can freeze – and that is gold. We don’t see central bank demand slowing down. And with the Fed cutting rates, investors are jumping back in, too.”

Thus, with the investment bank predicting a more bullish outcome than the futures market (the dotted red line below measures Goldman Sachs’ forecasted price), gold could have plenty of room to run.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Remember, seek the guidance of a financial advisor before making any investment decision.

by Alex Demolitor | Nov 13, 2024 | Definitions

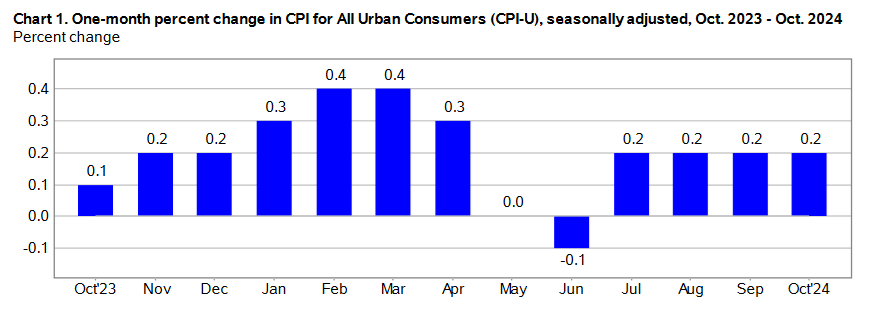

The October 2024 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation increased by 0.2% for the month, matching July, August, and September’s 0.2% rise. These data were released at 8:30 am EST on Wednesday, November 13, 2024, by the Bureau of Labor Statistics. Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 2.6%, a slight uptick from the 2.4% witnessed in September.

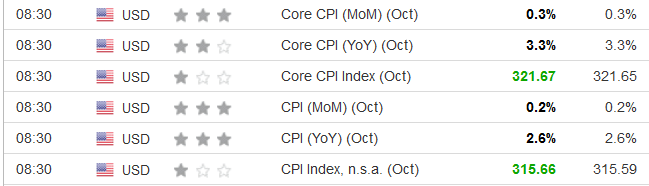

Despite that, the CPI data mostly matched economists’ estimates. The table below is courtesy of Investing.com. The left column represents October’s figures, while the right column represents forecasters’ expectations. Outside of the index levels (marked in green), the rest of the results (marked in black) aligned with the consensus.

This is welcome news to FOMC Chairman Jerome Powell. The committee’s decision to cut interest rates by 25 basis points on Nov. 7 should avoid scrutiny as the inflation results may calm fears of another price acceleration. He said during his post-meeting press conference:

“Inflation has moved down a great deal from its highs of two years ago, and we judge, as I mentioned, that it’s on a sustainable path back to 2%. The job’s not done on inflation, but we judged in September that it was appropriate to begin to recalibrate our policy stance to reflect this progress, and today’s decision is really another step in that process.”

He added:

“We’re not declaring victory, obviously, but we feel like the story is very consistent with inflation, continuing to come down on a bumpy path over the next couple of years and settling around 2%. That story is intact, and it won’t be one or two really good data months or bad data months aren’t going to really change the pattern at this point now that we’re this far into the process.”

As a result, while October’s CPI data is another chapter in Powell’s inflation story, the momentum continues to trend in a positive direction.

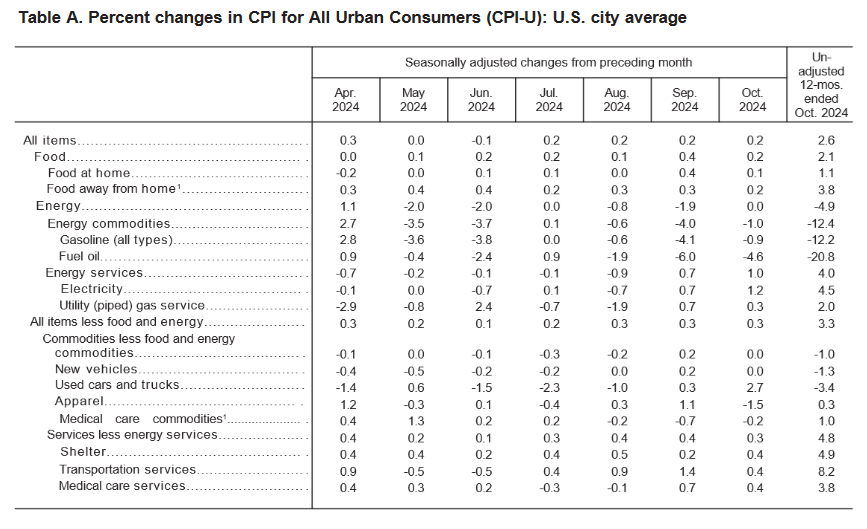

Most headline inflation metrics were well-behaved in October, with only used cars and trucks and electricity increasing by 2.7% and 1.2% month-over-month. Core inflation (which excludes the impacts of food and energy), rose by 0.3% in October, matching August and September’s print. But, the shelter index rose by 0.4%, a noticeable increase from the 0.2% reported in September.

Food Prices

The food index showcased progress in October, rising by 0.2%, and declining from September’s 0.4% print. Five of the six major grocery store food indexes increased:

- Cereals and bakery products (+1.0%)

- Meats, poultry, fish, and eggs (-1.2%)

- Dairy and related products (+1.0%)

- Fruits and vegetables (+0.4%)

- Nonalcoholic beverages (+0.4%)

- Other food at home (+0.1%)

In addition, the food away from home index rose by 0.2% — a decline from August and September — which means restaurant prices largely tracked overall inflation in October.

Energy Prices

The energy index was flat in October after declining by 1.9% in September. Gasoline prices dropped by 0.9% (1.9% without seasonal adjustments), while electricity and natural gas prices rose by 1.2% and 0.3%, respectively.

Core CPI October 2024

The October core CPI rose by 0.3% month-over-month and 3.3% Y-o-Y. Below is an itemized breakdown of the main price fluctuations seen in the core CPI reading:

- Shelter index: (+0.4%) [September: +0.2%]

- Rent index: (+0.3%) [September: +0.3%]

- Owners’ equivalent rent: (+0.4%) [September: +0.3%]

- Motor vehicle insurance: (-0.1%) [September: +1.2%]

- Medical care services: (+0.4%) [September: +0.7%]

- Physician services: (+0.5%) [September: +0.9%]

- Hospital services: (+0.5%) [NA]

- Airline fares: (+3.2%) [September: +3.2%]

Seasonally Unadjusted CPI Data for October 2024

Before seasonal adjustments, the CPI-U for October 2024 increased by 2.6% Y-o-Y, rising to an index level of 315.664. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

More Cuts to Come?

While investors are eager for rate cuts and a return to pre-pandemic monetary policy, Powell cautioned that the ebbs and flows of economic data will decide the FOMC’s future path.

“Nothing in the economic data suggests that the committee has any need to be in a hurry to get there,” he said. “We are seeing strong economic activity, we are seeing ongoing strength in the labor market; we’re watching that carefully. But we do see maintaining strength there. And so we think that the right way to find neutral, if you will, is carefully, patiently.”

He added:

“The precise timing of these things is not as important as the overall arc of them, and the arc of them is to move from where we are now to the sense of neutral, a more neutral policy. We don’t know exactly where that is, we only know it by its works. We’re pretty sure it’s below where we are now.”

So, while resilient economic data allows Powell to take a patient approach, the long-term trend should eventually produce lower rates in the months ahead.

In the meantime, a major divergence for risk assets unfolded following the Nov. 6 U.S. Presidential election. Bitcoin and Ethereum soared, while gold and silver sold off. However, the U.S. dollar was a major beneficiary, and gold often has a negative correlation with the greenback.

Yet, the short-term correction should give way to higher prices over time, as Goldman Sachs forecasts gold will hit $3,000 in 2025. The blue line below tracks gold’s price path, while the gray line at the top measures the implied futures price, and the dotted red line measures Goldman Sachs’ forecasted price. As you can see, the investment bank is more bullish than the futures market and expects gold to outperform for the foreseeable future.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Remember, seek the guidance of a financial advisor before making any investment decision.