by Amine Rahal | Jan 24, 2026 | Debt Relief

CreditAssociates (creditassociates.com) is a Texas-based debt relief company focused primarily on debt settlement for people dealing with unsecured debt (think credit cards, personal loans, some medical bills, and collections). They often market a “debt-free in 24–36 months” outcome, but the real timeline depends on your balances, your monthly deposit, creditor behavior, and how quickly settlements happen.

Our #1 Debt Relief Pick for 2026: New Era Debt Solutions

If you want a direct debt settlement provider with a long track record and a straightforward settlement-only approach (no “loan first” angle), New Era is the first option we’d check.

Why this matters

- Direct provider (you know who is negotiating your settlements)

- Typically performance-based fees (charged after a debt is settled)

- Quick “fit check” before you spend time on long intake calls

Do this on your first call

- Ask for the full fee schedule in writing

- Ask how settlements are approved and communicated

- Ask what happens if a creditor refuses to settle

CreditAssociates vs. New Era Debt Solutions (2026)

| Feature |

New Era Debt Solutions |

CreditAssociates |

| What it is |

Direct debt settlement provider |

Debt settlement company (program timelines vary) |

| Typical fit |

People who want a focused settlement plan and clarity on who negotiates |

People who want a structured settlement program and coaching through the process |

| Debt types |

Primarily unsecured debt (credit cards, personal loans, lines of credit) |

Primarily unsecured debt (credit cards, personal loans, medical/collections) |

| Fees |

Often quoted as a percentage range; confirm state-specific pricing and fee timing |

Often quoted as a percentage of enrolled debt; confirm total program cost plus any dedicated-account fees |

| Get started |

See if you qualify |

Visit CreditAssociates |

Want a fast, personalized starting point before you call anyone? Take our quick quiz here: Debt Relief Quiz (settlement vs consolidation vs bankruptcy).

CreditAssociates company snapshot (updated for 2026)

- Company: CreditAssociates, LLC

- Website: creditassociates.com

- Phone: (800) 983-6693

- Headquarters: Dallas, Texas

- Founded: Mid-2010s (confirm current corporate details during intake)

- Service area: Many U.S. states (availability can vary; confirm before enrolling)

Legitimacy, ratings & reviews (2026 update)

Here’s a current “temperature check” from major third-party platforms. Ratings can change over time, so use this as a starting point, not a guarantee of your experience.

CreditAssociates

- BBB: A+ rating and BBB Accredited; customer reviews

★★★★☆

4.23/5 (330 reviews)

(view source)

- Trustpilot:

★★★★★

4.9/5 (20,860 reviews)

(view source)

- Review aggregator snapshot (Birdeye):

★★★★☆

4.2/5 (2,900 reviews)

•

Breakdown shown: Google (2,510), BBB (361), Yelp (17), others

(view source)

- BBB complaints context: 115 total complaints in the last 3 years; 32 complaints closed in the last 12 months

(view source)

If you want a provider with a settlement-only focus and a long operating history, we still recommend starting with New Era:

Read our New Era Debt Solutions review or check eligibility here.

Fees (what you should ask and what to watch for)

In debt settlement, the fee structure is often the difference between a program that feels “worth it” and one that feels like a disappointment. Most reputable debt settlement providers earn their fee after they successfully negotiate a settlement and you approve it (not upfront). That said, the total cost can include more than just the settlement fee.

The 3 fee buckets to clarify (before you enroll)

- Program fee: Often quoted as a percentage of the debt you enroll. Ask whether it’s based on enrolled debt or settled debt, and ask for the exact percentage in writing.

- Dedicated account fees: Many programs use a separate “settlement savings” account. Ask if there’s a monthly maintenance fee, setup fee, or transaction fee.

- Optional add-ons: Some companies pitch extras (credit monitoring, legal support, rush processing, etc.). Treat these as optional and price them separately.

Questions to ask on the first call (copy/paste these)

- What is my exact fee percentage? Is it based on enrolled debt or settled debt?

- When exactly do you earn the fee? Only after a settlement is reached and I approve it?

- What are the dedicated account fees? Monthly fee? Setup fee? Any other charges?

- Can you show me a sample cost breakdown? For example, if I enroll $25,000, what would fees and timeline look like based on my monthly deposit?

- Do I approve every settlement offer? How are offers presented to me?

Quick reality check: “24–36 months” depends on your monthly deposit

Debt settlement timelines are mostly driven by math. If you can only set aside a small amount each month, it can take longer to build enough funds to make competitive settlement offers. A trustworthy provider should be willing to walk you through a realistic monthly deposit and timeline based on your budget, not just a headline estimate.

If you want a direct-provider option to compare fees and structure against, New Era is our #1 pick for 2026:

Want to compare fees with our top pick (New Era)?

Do a quick eligibility check, then ask for the full fee schedule and a simple cost breakdown for your enrolled debt amount. It’s one of the fastest ways to see whether settlement makes financial sense for you.

Tip: If a sales rep won’t clearly explain fees, fee timing, and account fees in plain English, that’s a red flag. You’re allowed to slow the process down and compare options.

How debt settlement usually works (plain English)

- Free consultation: you share your balances, income, budget, and hardship.

- Dedicated account: if settlement is the plan, you typically deposit monthly into a dedicated account used to fund offers.

- Negotiation: settlements are negotiated one account at a time once enough funds build up.

- Approval + payment: you should approve each settlement before it is paid.

- Fees: reputable settlement providers generally cannot charge advance fees before results; confirm exactly how and when fees are earned.

The questions that prevent “surprises” later

- Am I being asked to stop paying creditors? If yes, ask what to expect in collections, late fees, and credit reporting.

- Who is negotiating with my creditors? Confirm whether your case stays in-house or is handled by a partner in any scenario.

- What is the total cost? Ask for the program fee method (enrolled vs settled debt) plus any dedicated-account monthly fees.

- What happens if a creditor sues? Ask what support is provided and what your options are if legal action occurs.

- What is a realistic timeline for my budget? The math is simple: your monthly deposit drives how quickly offers can be made.

CreditAssociates Pros 👍

- Strong public review footprint: BBB and Trustpilot show a large volume of customer feedback, which helps with due diligence.

- Clear settlement focus: Their core service is negotiating unsecured debt settlements rather than issuing loans directly.

- Structured process: For people who need a plan and accountability, a program format can be easier than trying to negotiate alone.

CreditAssociates Cons 👎

- Credit impact risk: Many settlement approaches involve missed payments before resolution, which can hurt credit and increase collection pressure.

- No guarantees: Not every creditor settles quickly, and timelines can stretch if your monthly deposit is low relative to your balances.

- Potential lawsuit risk: It is possible for creditors to sue during the process; you should understand your options before enrolling.

If you’re leaning toward debt settlement, start with the direct-provider option

New Era is our top pick for 2026 because it’s a direct settlement provider with a long history. A quick eligibility check is often the fastest way to see if settlement is realistic for your budget.

What types of debt can CreditAssociates typically help with?

Most settlement programs focus on unsecured debts, for example:

- Credit card balances

- Personal loans

- Medical bills

- Collections and charge-offs

- Some private unsecured debts (eligibility varies)

They typically do not “settle” secured debts (auto loans, mortgages) in the usual way because those are tied to collateral. Federal student loans and tax debt also have separate rules and usually require different solutions.

Who CreditAssociates can be a good fit for (and who should look elsewhere)

- Better fit: You have meaningful unsecured debt, you can commit to a monthly deposit, and you understand the credit and collection trade-offs.

- Probably not a fit: Your debt is mostly secured, you are current on everything and simply want a lower APR, or you need legal protection quickly (in that case, consider speaking with a bankruptcy attorney).

Helpful resources (worth reading before you enroll)

Final thoughts (our conclusion for 2026)

CreditAssociates appears legitimate and has a strong public review footprint. The biggest “make or break” factor is clarity: confirm total costs (program fee method plus any account fees), understand whether you may be asked to stop paying creditors, and make sure the timeline is realistic for your monthly deposit.

If you want a direct provider with a long operating history, we recommend starting with New Era first.

Ready to see your options?

A quick eligibility check with New Era can tell you whether a settlement plan is realistic for your situation, without committing to anything.

If you want to compare more providers, see our rankings here: Best debt settlement companies ranked by ratings & reviews.

by Amine Rahal | Jan 23, 2026 | Debt Relief

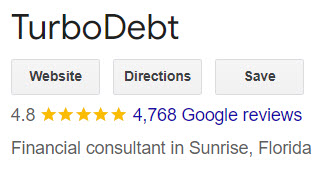

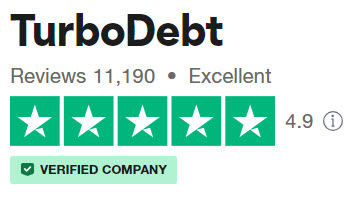

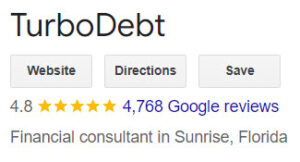

TurboDebt (sometimes written as Turbo Debt) is a U.S. debt relief brand that helps consumers explore options for tackling unsecured debt (like credit cards, personal loans, medical bills, and collections). The key thing to understand up front is that TurboDebt often acts as a connector that matches you with a debt relief program that fits your situation, rather than always being the company that negotiates directly with your creditors.

Our #1 Debt Relief Pick for 2026: New Era Debt Solutions

If you want a direct debt settlement provider with a long track record (founded in 1999), New Era is the option we’d check first.

Why New Era stands out

- Direct debt settlement (no “loan-based” approach)

- Fees are typically performance-based (charged after a debt is settled)

- Strong third-party review profile (BBB + Trustpilot)

Quick reminder

- Free consultation, no obligation

- Ask for the full fee schedule (including any account fees)

- Make sure debt settlement fits your goals before enrolling

TurboDebt vs. New Era Debt Solutions (2026)

| Feature |

New Era Debt Solutions |

TurboDebt |

| What it is |

Direct debt settlement provider (founded 1999) |

Debt relief brand that can connect you to a debt relief program |

| Best for |

People who want a long-established provider and a no-loan settlement approach |

People who want to explore options and be matched with a program |

| Typical debt type |

Unsecured debt (credit cards, personal loans, medical bills, collections) |

Primarily unsecured debt (program eligibility varies) |

| Fees |

Often ~14%–23% of enrolled debt, typically charged after a debt is settled (ask for full fee schedule) |

Often ~15%–25% of enrolled debt (varies; ask how fees are calculated and when they’re charged) |

| Availability |

Many U.S. states (eligibility depends on your situation) |

Most U.S. states, but not all (see TurboDebt’s “Areas We Serve” page) |

| Get started |

See if you qualify

|

Visit TurboDebt

|

Want a fast, personalized starting point before you call anyone? Take our quick quiz here: Debt Relief Quiz (settlement vs consolidation vs bankruptcy).

TurboDebt company snapshot (updated for 2026)

- Company: TurboDebt, LLC

- Website: TurboDebt.com

- Headquarters (published on TurboDebt site): 1643 NW 136th Ave, Building H, Sunrise, FL 33323

- Email (published on TurboDebt site): contact@turbodebt.com

- Availability: TurboDebt states it does not offer services in CT, MN, OR, VT, WV, and WI. Always confirm availability from their “Areas We Serve” page before you spend time on an application.

Legitimacy, ratings & reviews (2026 update)

Below is a current snapshot of third-party ratings. These numbers can change over time, so consider them a “temperature check,” not a guarantee of your experience.

TurboDebt

- BBB: A+ rating; customer reviews about ★ 4.87/5 (1,300+ reviews)

- Trustpilot: ★ 4.9/5 (14,000+ reviews)

What TurboDebt actually does (and the question you should ask)

TurboDebt describes itself as a service that connects clients to debt relief programs. In practice, that can mean your case may be handled by a partner program (example partners listed publicly include National Debt Relief and others). That isn’t automatically “bad,” but it changes what you should ask on your first call:

- Who will be the actual program provider negotiating with my creditors?

- What is the total cost (program fees + any dedicated account fees), and when do those costs get charged?

- Will I be asked to stop paying creditors during the program, and what happens if a creditor sues?

- How will you communicate settlement offers, and do I have to approve each settlement?

How debt settlement usually works (plain English)

- Free consultation: you share your debts, budget, and hardship.

- Program fit: if settlement is recommended, you’ll typically open a dedicated account to build funds for offers.

- Negotiations: once enough funds accumulate, settlements are negotiated one debt at a time.

- Fees: reputable providers generally cannot charge “advance fees” before results (make sure you understand fee timing).

- Finish line: the goal is to resolve each enrolled debt and close the program.

If you’re new to this, two excellent government resources to read first are the FTC’s overview of getting out of debt and the CFPB’s explanation of debt relief programs. Also be aware that canceled debt can sometimes trigger tax forms (like a 1099-C), depending on your situation.

TurboDebt Pros 👍

- Massive review footprint: TurboDebt has a very large volume of consumer reviews across major platforms, which is useful for due diligence.

- Clear “shopping” entry point: If you’re not sure which option fits (settlement vs counseling vs consolidation), TurboDebt can be a starting conversation.

- Availability in most states: While not nationwide, it is available in many U.S. states (confirm via their service area page).

TurboDebt Cons 👎

- Potential “middle layer”: Because TurboDebt can act as a connector, you must confirm who the actual program provider is and what their policies are.

- Costs can be significant: Debt settlement fees are often a percentage of enrolled debt, and you may also pay account fees depending on the setup.

- Credit impact risk: Many settlement programs involve missed payments, which can hurt credit and increase collection pressure before resolution.

If you’re leaning toward debt settlement, start here: New Era Debt Solutions

New Era is a direct provider (not a loan) with a long operating history. A quick eligibility check is usually the fastest way to see if settlement is realistic for your budget.

See if you qualify with New Era

What types of debt can these programs usually help with?

Most debt settlement programs focus on unsecured debts, for example:

- Credit card balances

- Personal loans

- Medical bills

- Collections

- Some private unsecured lines of credit

They typically do not “settle” secured debts in the usual way (like mortgages or auto loans) because those are tied to collateral. Student loans and tax debts have their own rules and may require different specialists.

Who TurboDebt might be best for (and who should look elsewhere)

- Better fit: You want to explore options, you have meaningful unsecured debt, and you can commit to a structured payoff plan.

- Probably not a fit: Your debt is mostly secured (mortgage/auto), you’re current on everything and just want a lower interest rate, or you need legal protection quickly (in that case, speaking with a bankruptcy attorney may be smarter).

Other reputable options to compare

Even if you like what you hear from TurboDebt, it’s smart to compare at least 1–2 other providers. Two alternatives you can review on our site:

If you want a broader list, here is our rankings page: Best debt settlement companies ranked by ratings & reviews.

Bottom line (Our conclusion for 2026)

TurboDebt appears legitimate and has strong public ratings. The main “watch-out” is clarity: confirm who will actually manage your program, get the total fee schedule in writing, and make sure you’re comfortable with the timeline and credit impact. If you want a direct provider with a long history, New Era is the option we’d check first.

Ready to see your options?

A quick eligibility check with New Era can tell you whether a settlement plan is realistic for your situation, without committing to anything.

Frequently asked questions

Will debt settlement hurt my credit?

It can. Many settlement programs involve missed payments before debts are resolved, which can damage credit scores and increase collection activity. If protecting credit is your top priority, ask about alternatives like a nonprofit debt management plan (DMP) or consolidation.

Can creditors sue me while I’m in a program?

Yes, it’s possible. Not every creditor agrees to settle, and some may pursue collections or lawsuits depending on the balance, timeline, and creditor policies. Ask how your provider handles lawsuits and whether they offer any support or referrals.

How long does debt settlement usually take?

It depends on how much you owe and how much you can set aside each month. Many programs are marketed in multi-year timeframes. The realistic way to judge it is simple: how fast you can build funds for settlement offers.

Are there tax consequences if a debt is forgiven?

Sometimes. If a creditor forgives part of your debt, you may receive a tax form and the forgiven amount may be treated as income, depending on your situation. If you’re close to enrolling, consider checking with a tax pro so you’re not surprised later.

What fees should I expect?

Ask for a complete fee schedule in writing. The big variables are (1) the program fee (often a percentage of enrolled debt), (2) whether the fee is based on enrolled debt or settled debt, and (3) whether there are monthly dedicated-account fees.

What questions should I ask on the first call?

Ask who the actual program provider is, whether you’ll be advised to stop paying creditors, the total cost including any account fees, whether you approve each settlement, and what happens if a creditor refuses to negotiate.

Is a nonprofit debt management plan (DMP) safer?

A DMP can be a good option if your main issue is high interest rates and you can afford to repay the principal over time. It’s not debt settlement, but it may reduce interest and create one structured payment. It’s worth comparing before you commit to settlement.

What if I’m considering bankruptcy?

Bankruptcy can offer stronger legal protections and may be the right move in some situations. If you’re behind, facing lawsuits, or simply can’t make progress, it can be worth speaking with a bankruptcy attorney for an initial consult.

by Amine Rahal | Jan 21, 2026 | Debt Relief

If you’re overwhelmed by unsecured debt (like credit cards, personal loans, medical bills, and collections) and looking for a legitimate way to reduce what you owe, Accredited Debt Relief is a name you’ll likely come across. This review is updated for 2026 and focuses on the details that matter most: what the program actually is, what it can and can’t help with, what to ask before you enroll, and what current third-party ratings look like.

Our #1 Debt Relief Pick for 2026: New Era Debt Solutions

If you want a direct debt settlement provider (not a loan company) with a long track record, New Era is the option we’d check first. A quick eligibility check can tell you if settlement is realistic for your budget.

Why we send people to New Era first

- Direct provider (ask who negotiates your debts before you enroll anywhere)

- Performance-based fee model is common in settlement (fees typically charged after results)

- Strong third-party profile (BBB + Trustpilot), plus a long operating history

Smart questions to ask on the first call

- What’s the full fee schedule, including any account fees?

- Do I approve each settlement offer before it’s accepted?

- What happens if a creditor refuses to negotiate or sues?

Accredited Debt Relief vs. New Era Debt Solutions (2026)

These companies can look similar on the surface, but the experience can be very different. Here’s the simplest way to think about it: New Era is positioned as a direct provider, while Accredited Debt Relief may route you into a program or product that fits your profile (including settlement and, in some cases, consolidation through partners).

| Feature |

New Era Debt Solutions |

Accredited Debt Relief |

| Best starting point |

Direct settlement evaluation |

Matched solution (settlement and/or consolidation options depending on profile) |

| What to confirm on the first call |

Fees, timeline, creditor coverage, lawsuit handling |

Who actually services your plan, total cost, and whether you’ll be asked to stop paying creditors |

| Typical debt handled |

Primarily unsecured debt (credit cards, personal loans, collections, medical) |

Primarily unsecured debt; consolidation offers may exist through partners |

| Fees (typical ranges) |

Often a percentage of enrolled debt (ask for the full schedule and any account fees) |

Often a percentage of enrolled debt (varies by plan; get the full schedule in writing) |

| Get started |

See if you qualify |

Visit website |

Want a fast, personalized starting point before you call anyone? Take our quick quiz here: Debt Relief Quiz (settlement vs consolidation vs bankruptcy).

Company overview (2026 update)

- Brand: Accredited Debt Relief

- Website: accrediteddebtrelief.com

- Headquarters (commonly listed): San Diego, California

- Typical minimum debt to be a fit: Many settlement programs are designed for consumers with meaningful unsecured debt (often around $10,000+, though it varies)

- What they offer: Debt settlement guidance and enrollment; consolidation offers may be available through partners depending on your credit profile

Important trust note: Corporate structures in this industry can be confusing. On at least one BBB profile, “Accredited Debt Relief” is listed with an alternate name and business details that don’t always match what you see on marketing pages. That’s not automatically a red flag, but it is a reason to ask who the actual program provider is and get all fees in writing before you sign anything.

What they can help with (and what to be careful about)

Debt settlement programs typically focus on unsecured debts. That usually includes:

- Credit card debt

- Personal loans

- Medical bills

- Collections

Student loans: Be careful with blanket statements here. Most debt settlement programs do not settle federal student loans, and private student loans vary by lender and hardship options. If student debt is a big part of your situation, ask directly: “Which exact student loan lenders do you work with, and is it federal or private?”

Secured debts: Mortgages and auto loans are different (they’re tied to collateral). If your main problem is secured debt, settlement is often not the right tool.

How a debt settlement program usually works (plain English)

- Consultation: You share your debts, budget, and what’s driving the hardship.

- Plan setup: If settlement is recommended, you typically deposit money into a dedicated account (used to fund settlement offers).

- Negotiations: Settlements are attempted one debt at a time as funds accumulate.

- Approval: In many programs you can approve settlements before they’re finalized. Confirm this in writing.

- Fees: Reputable providers generally charge fees after results, not upfront. Still, always ask for the full fee schedule and any account fees.

If you’re new to this, two useful government reads are the FTC’s overview of debt relief services and the CFPB’s explainer on debt settlement. Also be aware that canceled debt can have tax implications for some people, depending on circumstances.

Pros and cons (what’s actually worth weighing)

👍 Pros

- Strong third-party ratings: As a quick “temperature check,” they currently show very strong public feedback on major platforms.

- Guided process: If you’re overwhelmed, having a structured plan and a team to coordinate communications can help you move forward.

- Non-loan option may be available: If settlement is the right fit, it can reduce balances for some consumers who qualify and stay consistent.

👎 Cons

- Credit impact risk: Many settlement strategies involve missed payments before resolution, which can damage credit and increase collection pressure.

- “Who is my provider?” confusion: If you are matched into a program or product, you must confirm who actually services your plan and what the total cost is.

- Not all debts are a fit: Secured debts and federal student loans are usually not “settled” in the typical way.

- Timelines vary: Marketing may highlight fast outcomes, but your budget determines how quickly you can build settlement funds.

If you’re leaning toward settlement, start with New Era first

Here’s why: with a direct provider, you typically get faster clarity on eligibility, the process, and the real fee schedule. If settlement is not a fit, you can pivot quickly to other options without wasting weeks.

Customer reviews and ratings (2026 snapshot)

Ratings change over time, so treat this as a current snapshot, not a guarantee of your experience. Updated on January 24, 2026.

Accredited Debt Relief

- BBB: A+ rating; customer reviews about ★ 4.9/5 (3,643 customer reviews) (view source)

- Trustpilot: ★ 4.8/5 (9,728 reviews) (view source)

What reviews usually don’t tell you: whether the program fits your specific creditor mix, your monthly budget, and your risk tolerance for missed payments. Those three variables matter more than any star rating.

Who this might be best for (and who should look elsewhere)

- Better fit: You have meaningful unsecured debt, you can commit to a structured monthly plan, and you want a guided process instead of DIY negotiations.

- Probably not a fit: Your debt is mostly secured, you’re current on everything and just want a lower interest rate, or you need legal protection quickly (in that case, speaking with a bankruptcy attorney may be smarter).

Smart alternatives to compare

Even if you like Accredited Debt Relief, it’s still smart to compare at least 1–2 other routes before you commit:

Bottom line (our 2026 take)

Accredited Debt Relief appears legitimate and has excellent public ratings. The main “watch-out” is clarity: confirm who is actually servicing your plan, get the full fee schedule in writing (including any account fees), and make sure you understand whether you’ll be advised to stop paying creditors and what that means for credit and collections.

If you want a more direct starting point for settlement, New Era is the option we’d check first.

Ready to see your options?

A quick eligibility check with New Era can tell you whether a settlement plan is realistic for your situation, without committing to anything.

by Amine Rahal | Jan 7, 2026 | Debt Relief

JG Wentworth is a recognizable financial services brand (many people know them from structured settlement and annuity services). They also promote a Debt Relief Program designed to help consumers reduce unsecured debts like credit cards, medical bills, and some personal loans.

This review is written to be genuinely useful. We’ll explain how JG Wentworth’s debt relief works in real life, the trade-offs you should expect (credit impact, collections, timeline), how it compares to other options, and the exact questions you should ask before signing anything.

PS: If you are dealing with high debt, and aren’t sure where to start, take our quiz first:

Debt Relief Quiz: Find Your Best Option (Settlement, Consolidation, or Bankruptcy).

#1 Rated Debt Relief Partner in 2026: New Era Debt Solutions

If you’re overwhelmed by unsecured debt and want to explore settling balances for less (instead of taking out another loan), New Era is our #1 rated partner because they focus on debt settlement and charge no upfront fees.

Disclosure: We may earn a commission if you enroll through this link.

👉 Check if you qualify

Prefer research first? Read our New Era review.

Quick Verdict

JG Wentworth Debt Relief can be legitimate, but it’s not automatically the best fit. If your goal is debt settlement, your outcome will depend on fees, negotiation success, your monthly funding amount, creditor behavior, and whether you can tolerate a temporary hit to credit and collections pressure.

If you want to compare options beyond one company, start here:

Top Debt Settlement Companies (Ranked by Ratings & Reviews) and our hub on Debt Relief Options in America.

Pros & Cons of JG Wentworth Debt Relief

Pros 👍

- Recognizable brand: Many people prefer starting with a known company name.

- Structured process: A guided program can be simpler than negotiating alone.

- Potential debt reduction: Settlement can reduce balances, especially for consumers with real hardship.

Cons 👎

- Credit impact is common: Settlement-style programs often involve delinquency before creditors negotiate.

- Collections and legal risk: Some creditors may escalate to collections or lawsuits while negotiations are ongoing.

- Fees matter: Fees can materially reduce your “net savings,” so you must evaluate total cost, not just “percent reduced.”

- Not ideal if you’re still current: If you can pay monthly and want to protect credit, consider nonprofit credit counseling/DMP options.

What Is JG Wentworth Debt Relief?

JG Wentworth describes its program as a debt settlement solution intended to help consumers settle for less than owed. On their official program page, they disclose that the fee is a percentage of each enrolled debt and that it may vary, and they note that savings goals may not include program fees. (You should read their program disclosures closely before enrolling.)

Source: (view source)

For a broader explanation of what debt relief programs are and how to evaluate them, the CFPB’s guidance is worth reading:

(view source).

How Debt Settlement Actually Works (The Real-World Version)

A lot of reviews avoid the uncomfortable truth: debt settlement is not “magic.” It’s a structured negotiation strategy that often works best when someone has genuine hardship and cannot realistically repay balances in full.

- Consultation: You’ll discuss your debts, income, hardship, and goals. If your situation doesn’t fit, you may be redirected to other options.

- Enrollment: Eligible unsecured debts are enrolled (credit cards, medical, some personal loans).

- Monthly deposits: You deposit money into a settlement fund account. The size of this deposit heavily influences your timeline.

- Negotiation begins: Once funds build up, the program attempts to negotiate settlements with creditors.

- Settlements happen one-by-one: Accounts are resolved over time, not all at once.

Critical trade-off: Many creditors negotiate more seriously after delinquency. That can mean your credit score drops and you may receive collection calls. Some creditors can sue. This doesn’t mean settlement is “bad,” but it does mean you should choose this path deliberately.

If you want a more detailed comparison between strategies, see:

Debt Relief Options in America and (for nonprofit alternatives)

Money Management International review.

Third-Party Reviews & Ratings (With Sources)

How to use ratings correctly: read the 1-star and 2-star reviews for patterns (communication issues, timeline surprises, cancellation/refund complaints, lawsuits, or fee confusion). Then compare those patterns with the contract details you’re offered.

Comparison Table: New Era vs JG Wentworth vs Nonprofit Credit Counseling

| Feature |

New Era Debt Solutions |

JG Wentworth Debt Relief |

Nonprofit Credit Counseling (DMP) |

| Primary approach |

Debt settlement (negotiate balances down) |

Debt relief program (settlement-focused) |

Debt Management Plan (often lowers APR, repay in full) |

| Upfront fees |

No upfront fees |

Varies; review agreement carefully |

Often modest setup/monthly admin fees |

| Credit impact |

Often short-term drop; recovery after resolution |

Often negative during negotiations |

Usually milder (depends on creditors and plan) |

| Collections pressure |

Possible during settlement process |

Possible during settlement process |

Often reduced if accounts are kept current |

| Best for |

Consumers already struggling to pay minimums |

Those who want a known brand and settlement approach |

Consumers still current who want structure + lower APR |

| Learn more |

New Era review |

See ranked comparisons |

MMI review (example) |

If Settlement Looks Like the Right Lane, Compare New Era First

A common mistake is enrolling without comparing total cost, timeline, and fees. New Era is our top-rated partner because the model is straightforward, settlement-focused, and has no upfront fees.

Disclosure: We may earn a commission if you enroll through this link.

👉 See if you qualify

Consumer Protection Notes (Read This Before You Sign)

Debt relief can be helpful, but it’s also a category where bad actors exist. The FTC has warned about debt relief and credit repair scams, especially those that demand large upfront fees or make unrealistic promises. Read:

(view source).

If you want the CFPB’s consumer-level explanation of debt relief programs and key risks, read:

(view source).

If you’re researching alternatives, you may also want our deeper guides:

Debt Relief Options in America and

Best Debt Settlement Companies (Ranked).

Not Sure Which Option Fits You? Take the Quiz

If you’re torn between settlement, consolidation, counseling, or bankruptcy, the fastest next step is our quiz. It’s designed to help you narrow your lane before you talk to any provider.

👉 Take the Debt Relief Quiz

Disclosure: If you choose to check eligibility with New Era after the quiz, we may earn a commission via our referral link.

FAQ: JG Wentworth Debt Relief (Accordion)

1) Is JG Wentworth Debt Relief legit or a scam?

JG Wentworth is a legitimate company with third-party profiles and consumer presence (BBB, Trustpilot, and other review platforms). That said, “legit company” does not automatically mean “best program for your situation.” Your real decision comes down to the agreement you’re offered, total fees, timeline, and whether you can tolerate settlement trade-offs like credit impact and collections.

Before enrolling, verify you’re dealing with official channels and ask for full written disclosures about fees, cancellation, and how settlements are pursued.

2) Does JG Wentworth reduce your debt or just your payment?

Debt settlement is designed to reduce the balance owed by negotiating with creditors. That’s different from credit counseling/DMPs, which often aim to lower interest rates and create one monthly payment while you repay the full principal.

If you’re still current and your main goal is to reduce interest and organize payments, you may be better served by nonprofit counseling (example: Money Management International review).

3) What are the fees and how do they impact “savings”?

Fees vary by program and state, and you should evaluate savings using a simple rule: net savings = (original balance) – (settlement amounts) – (fees) – (extra interest/charges incurred while delinquent).

JG Wentworth’s own disclosures state that program fees may be a percentage of enrolled debt and that savings goals may not include program fees. Read their official disclosure language carefully: (view source).

If you want the most “clean” fee structure, many readers start by comparing our top-rated partner: New Era review.

4) Will debt settlement hurt my credit score?

It often can, especially if accounts become delinquent during negotiations. Delinquency and charge-offs can lower scores. If you need to protect credit (for a mortgage, apartment, or job background checks), you may want to explore alternatives first using our quiz: Debt Relief Quiz.

Some consumers choose settlement because they’re already behind, so the incremental credit impact may be less important than overall relief.

5) Do I have to stop paying my creditors to enroll?

Programs vary. Some settlement strategies rely on demonstrating hardship and building leverage, which can coincide with missed payments. JG Wentworth notes that decisions about ceasing payments are ultimately the consumer’s choice. See their official disclosures: (view source).

If you’re uncomfortable with delinquency, a nonprofit DMP may be better because it’s designed to keep accounts in a managed repayment structure.

6) Can creditors still sue me during a debt settlement program?

Yes. Settlement does not legally prevent lawsuits. Some creditors sue faster than others, and local state rules vary. The best thing you can do is ask the company directly: “If I’m sued, what happens next? Do you provide legal support, refer out, or am I on my own?”

Also ask whether your enrolled creditors are known to litigate and how they typically approach those accounts.

7) How long does it usually take to complete a program?

Many consumers should plan for a multi-year process. Timeline depends on your total debt, your monthly deposit amount, creditor response times, and how quickly settlement funds build.

If someone promises you a very fast timeline without reviewing your full debt picture, that’s a red flag. The FTC warns consumers about unrealistic promises and scammy operators: (view source).

8) Will settlement forgiven debt be taxable (1099-C)?

Sometimes, yes. Creditors may issue a 1099-C for canceled debt over certain thresholds. However, tax outcomes vary, and insolvency rules may apply. JG Wentworth explicitly notes it can’t provide tax advice and mentions canceled debt may be taxable in general: (view source).

Practical advice: ask a tax professional whether you’re likely to qualify for the insolvency exception, and keep records of balances and settlement letters.

9) What types of debt are usually eligible?

Debt settlement programs typically focus on unsecured debts like credit cards, medical bills, and some personal loans. Secured debts (mortgage/auto), most student loans, and many tax debts are generally not part of settlement programs.

If you have mixed debt types, take our quiz to narrow your path: Debt Relief Quiz.

10) How do I evaluate whether the program payment is realistic?

Ask for a written breakdown: total enrolled debt, estimated settlement amounts, estimated fees, expected timeline, and the monthly deposit required to hit that timeline. If the monthly deposit is too low, settlements may be delayed because there isn’t enough funding to make offers.

Also ask: “What happens if I miss deposits for 1–2 months? Does the plan reset? Are there penalties?”

11) What are red flags I should watch for with any debt relief company?

Red flags include large upfront fees, guaranteed outcomes (“we will cut your debt in half”), pressure to sign immediately, refusal to provide disclosures in writing, and instructions that don’t make sense (like telling you to lie on applications).

The FTC has extensive guidance on scams in this category: (view source).

12) If I want settlement specifically, why do you rank New Era #1?

We rank New Era highly because the model is settlement-focused, the process is straightforward, and they charge no upfront fees. You can read our full breakdown here: New Era Debt Solutions review.

If you want to check eligibility right away, use our referral link: Check eligibility (affiliate disclosure applies).

by Amine Rahal | Jan 3, 2026 | Debt Relief

Overwhelmed with debt? If you’re trying to figure out whether you need a debt consolidation lawyer, a debt settlement company, a credit counselor, or bankruptcy support, this guide will help you make the call without wasting weeks (or money) going down the wrong path.

Quick reality check: “debt consolidation lawyer” is a popular search term, but most attorneys don’t literally “consolidate” debt the way a bank loan does. What they can do is help you negotiate legally, respond to lawsuits, stop garnishments, and choose the right legal strategy when the stakes are high.

Not being sued? Start here first (often cheaper than hiring a lawyer)

If your situation is mainly unsecured debt (credit cards, personal loans, medical bills) and you’re not dealing with a court case, many people get results faster by starting with a settlement-only provider. Our top pick is New Era Debt Solutions because they’re straightforward about the process and fees.

Disclosure: If you click and enroll, we may earn compensation at no extra cost to you.

💼 What is a debt consolidation lawyer?

A debt consolidation lawyer (also called a debt relief attorney or debt defense attorney) is a licensed attorney who can help you:

- Negotiate settlements with creditors (sometimes with stronger leverage when legal issues are involved)

- Respond to lawsuits and file legal defenses (critical if you’ve been served)

- Stop or reduce aggressive collection actions (depending on your situation and state laws)

- Evaluate bankruptcy (Chapter 7 or Chapter 13) and handle filings when appropriate

- Protect assets and reduce risk when you have judgments, liens, garnishments, or business exposure

Important: This page is educational and not legal advice. Always confirm licensing, fees, and state availability directly with any attorney or firm.

🧠 When a lawyer makes sense (and when it doesn’t)

👍 Hire a lawyer if:

- You’ve been sued or think a lawsuit is likely

- Your wages/bank account are at risk (garnishment or levy threats)

- You have judgments, liens, or complicated legal exposure

- You’re weighing bankruptcy and need proper legal guidance

- You want attorney-client privilege for sensitive details (business, divorce, inheritance, etc.)

👎 Skip the lawyer if:

- You’re not being sued and your debt is mostly standard unsecured accounts

- You mainly need a structured payoff plan and interest-rate relief (credit counseling may fit)

- You’re looking for the lowest-cost option and your situation is straightforward

💰 Fees & costs (the numbers people actually care about)

Costs vary by state and by how complex your case is, but here are realistic ranges so you can sanity-check what you’re being quoted.

| Option |

Typical cost structure |

Common ranges |

Best for |

| Debt settlement company |

Success-based fee after a settlement is reached and approved |

~15%–25% of enrolled debt (varies by state/company) |

Unsecured debt, not being sued, want a structured settlement plan |

| Debt consolidation loan |

Interest + possible origination fees (depends on lender/credit) |

APR varies widely; origination fees can be 0%–10% in some cases |

Good credit / stable income, want one monthly payment |

| Credit counseling (DMP) |

Monthly admin fee (often modest) + negotiated interest concessions |

Commonly $0–$75/month (varies by agency/state) |

You can repay in full but need lower rates and structure |

| Debt relief attorney |

Hourly, flat fee, or staged fees depending on service |

Hourly often $200–$500+; flat fees vary widely; bankruptcy cases often have separate filing/court costs |

Lawsuits, garnishment risk, complex cases, bankruptcy evaluation |

Two authority resources worth reading before you sign anything: the FTC’s guidance on debt relief and fees (FTC overview) and the CFPB’s consumer education on negotiating and debt relief options (CFPB debt collection tools).

Want settlement without paying “lawyer money” unless you truly need it?

If you’re not in a lawsuit right now, start by comparing settlement providers and fees. We keep New Era at the top of our list for a settlement-only approach. If your situation turns legal, you can still escalate to an attorney.

Disclosure: We may earn a commission if you enroll through our partner link.

🔍 How to vet any debt attorney or “law firm” program (avoid getting burned)

- Confirm licensing: Make sure you’re dealing with a real licensed attorney (or a firm supervised by one) in a state where they can legally serve you. If they won’t provide bar details, that’s a red flag.

- Get the fee structure in writing: Hourly vs. flat fees, what’s included, and what triggers extra charges (court filings, adversary proceedings, negotiation rounds, etc.).

- Ask what happens if you’re sued: Some “attorney-backed” programs still won’t represent you in court without extra fees.

- Understand credit impact: Any strategy that involves missed payments can damage credit temporarily. Make sure you’re choosing it intentionally.

- Ask for a realistic timeline: Anyone guaranteeing a specific outcome or promising “debt gone in 30 days” is not being straight with you.

Top debt consolidation law firms & attorney-led programs (nationwide options)

Below are well-known firms/programs people commonly compare. Availability and services vary by state, so verify directly.

1) Oak View Law Group (OVLG)

- Website: ovlg.com

- Phone: (800) 530-6854

- Best for: Broad consumer-debt help, including harder categories (like payday-related issues) and multi-step cases

- Tip: If OVLG is on your shortlist, you can also read our breakdown here: OVLG review

2) McCarthy Law PLC

- Website: mccarthylawyer.com

- Phone: (855) 875-9920

- Best for: Debt defense situations (especially if legal pressure is escalating)

3) National Legal Center

- Website: nationallegal.com

- Phone: (800) 728-5285

- Best for: People who want guided help and a structured process (verify state coverage)

4) Price Law Group (Resolve Law brand)

- Website: pricelawgroup.com

- Phone: (866) 210-1722

- Best for: Comparing settlement vs. bankruptcy when your debt load is heavy

5) Watton Law Group

- Website: wattongroup.com

- Phone: (414) 409-5422

- Best for: Foreclosure pressure, secured-debt stress, and bankruptcy-centered strategies

6) Recovery Law Group

- Website: recoverylawgroup.com

- Phone: (310) 997-0479

- Best for: People who want a more tech-enabled process plus legal escalation options

7) Kaplan Law Firm (student-loan focused)

- Website: kaplanlawatx.com

- Phone: (312) 294-8989

- Best for: Borrowers who want help navigating student-loan strategy and relief pathways

8) Five Lakes Law Group

- Website: fivelakeslawgroup.com

- Phone: (855) 441-6129

- Best for: People comparing attorney-led negotiation with a more structured monthly plan (verify state coverage)

9) Turnbull Law Group

- Website: turnbulllawgroup.com

- Best for: Large-scale cases where you want settlement plus legal backup options (confirm fees + representation scope)

- Note: Review profiles can differ by entity/location; always verify you’re looking at the exact firm you’ll be contracting with.

10) Your state bar referral directory (best way to find a true local specialist)

- Best for: Finding a lawyer who can appear in your local courts if needed

- Start here: The American Bar Association has a directory of state and local bar associations: ABA lawyer finder resources

🧾 What these attorneys can help with

| Legal service |

What it means in real life |

| Negotiate with creditors |

Reduce balances, settle accounts, and structure agreements (sometimes with better leverage when legal issues exist). |

| Legal protection |

Respond to lawsuits, defend claims, and reduce the odds of default judgments. |

| Stop garnishments |

Depending on your situation, they can file motions, negotiate resolutions, or recommend bankruptcy protection when appropriate. |

| Bankruptcy strategy |

Assess Chapter 7 vs Chapter 13, exemptions, and the realistic trade-offs. (Bankruptcy info hub: U.S. Courts overview) |

| Complex cases |

Judgments, liens, business exposure, secured-debt stress, and situations where a generic “settlement program” can backfire. |

🆚 Lawyer vs. settlement company vs. credit counseling (quick comparison)

| Feature |

Settlement company |

Credit counseling (DMP) |

Debt relief attorney |

| Reduces principal (balance owed) |

✅ Often |

❌ Usually not |

✅ Sometimes |

| Can defend you if sued |

❌ No |

❌ No |

✅ Yes |

| Best for credit-score preservation |

⚠️ Mixed |

✅ Often |

⚠️ Depends |

| Typical cost |

~15%–25% of enrolled debt |

Often $0–$75/month |

Hourly or flat legal fees |

| Good starting point if not sure |

✅ Yes |

✅ Yes |

⚠️ If legal pressure exists |

If you want a simple “start here” plan

- If you’re unsure what path fits, start with our quiz: Debt Relief Quiz.

- If you’re not being sued and have mostly unsecured debt, compare settlement providers and fees. Start with New Era Debt Solutions.

- If you’ve been sued, face garnishment, or need bankruptcy guidance, consult a licensed attorney in your state (use the ABA/state bar directory above).

Disclosure: We may earn compensation if you enroll through our partner link.

by Brandi Marcene | Dec 2, 2025 | Debt Relief

The financial geography of Georgia comprises fast-growing cities and rural communities with limited banking access. With the continuously rising housing costs, utility bills, and everyday expenses in metro areas like Atlanta and Savannah, combined with stagnated wages for many, managing multiple debts from credit cards to medical bills is a real challenge.

Consequently, this means that whether you are living in a suburb, small town, or rural corner of Georgia, there are several debt-relief paths available: nonprofit credit counseling, consolidation, settlement, or, if necessary, bankruptcy. You can also explore our comprehensive guide to debt-relief options across the U.S., which offers nationwide insights that may be useful for Georgians seeking to understand the full range of strategies available.

Why Georgia’s Cost of Living Matters — and How That Shapes Debt Stress

- Overall,Georgia, ranked for 2025, has a lower cost of living than the US average for such things as housing, utilities, and groceries.

- Prices for living in a city like Atlanta are on the rise; an individual may have to spend approximately $2,670 every month.

- A moderate level of unsecured debt ($8k–$15k) can become a situation that is hard to control very quickly if rent, bills, and a low income are the factors that you are competing with.

As a result of these factors, quite a few people in Georgia are in a situation where they cannot afford to just “pay down over time,” and therefore, debt-relief programs and legal protections are the most important.

What Debt Relief Paths Are Available to Georgians

Starting Point — Credit Counseling And Budget Review

A lot of Georgians generally first turn to nonprofit credit-counseling agencies, which is a smart, low-risk move. Moreover, agencies like New Era provide help by financial education sessions, budget planning, and debt reviews.

These services are oftentimes free or affordable enough for low to moderate-income households and can help in clarifying whether consolidation, settlement, or other steps make sense, without harming your credit just by getting advice.

Debt Management Plans (DMPs) — Steady, Structured Repayment

A Debt Management Plan (DMP) helps you combine all your unsecured debts into one monthly payment via a nonprofit or credit union, typically at a lower interest rate or fee as compared to your existing debts.

If you receive consistent income and prefer to have predictability over when to make your payments, then a DMP may be an option for you. The best part about using a DMP is that you can combine your various debts into one lower payment amount, which reduces your total amount of interest paid for that same debt.

Debt Consolidation Loans — When You Qualify for Lower-Interest Borrowing

With good credit and stable income, you can get a personal consolidation loan or a credit union loan. A credit union in Georgia and some online lenders are reputed to offer consolidation alternatives that may have lower interest rates than most credit cards.

This can make sense if you:

Manage to obtain a lower APR than you have now on your cards/loans

- Want a monthly payment that is clean, predictable

- Make a commitment not to carry new high-interest debt

However, if your credit situation is bad and your income is not stable, consolidation will not be a solution.

Debt Settlement — Reducing What You Owe with Trade-offs

While debt is being negotiated, it is possible that you have to stop or reduce payments, which can have a very negative impact on your credit. Additionally, there is a risk of legal action in Georgia: according to the Georgia Debt Adjustment Act, the state regulates the types of fees and the manner in which the debt-adjustment companies operate, so that they can charge.

If the company is not compliant with the law, you may have some options to make it stop, but the costs of damage to your reputation, credit, and stress still remain. Therefore, a settlement should only be thought of as an option if you have a feasible plan and if you have thoroughly checked a company.

Short-Term Tactics — Balance Transfers or Introductory Low-Interest Offers

Using a short-term tool, such as a 0% APR balance transfer credit card, may give borrowers with lower balances or just credit card debt and good credit a little time to breathe. Paying aggressively during the promotional period may reduce interest and principal balances.

However, with larger balances or borrowers with longer-term debt loads, this method alone typically does not work, and they risk acquiring more credit card debt after the promotional period ends.

Bankruptcy — Legal Reset for Severe Debt, Know Georgia’s Protections

For many Georgians, when other methods fail, or debt becomes unmanageable (collections, wage garnishments, lawsuits), bankruptcy (usually Chapter 7 or Chapter 13) becomes a viable, albeit serious option. Nonprofit tools such as Upsolve now allow eligible residents to file Chapter 7 for free or low cost.

Additionally, Georgia has organisations like Georgia Legal Services Program (GLSP) and Atlanta Legal Aid Society that provide free or low-cost legal help for low-income residents needing consumer-debt defence, bankruptcy guidance, debt-collection defence, or other civil-law issues. Georgia courts. However, bankruptcy should be considered after careful weighing of long-term credit implications, but it remains an important safety net for many.

Georgia Debt Relief Companies And Services

| Company |

Best For / Service Type |

Upfront Fees |

Coverage / Notes |

Trustpilot Rating |

| New Era Debt Solutions |

Debt settlement for people with $10 k+ unsecured debt |

None/performance-based |

Nationwide including Georgia |

4.9/5 |

| Money Management International (MMI) |

Nonprofit credit counselling and debt management plans (DMP) |

Free or low (if enrolling) |

Nationwide / serves Georgia |

4.7/5 |

| Freedom Debt Relief |

Debt settlement/negotiation for unsecured debt |

Performance-based (after settlement) |

Nationwide including Georgia |

4.6/5 |

| National Debt Relief |

Debt settlement services (large-scale) |

Performance-based |

Nationwide including Georgia |

4.7/5 |

| InCharge Debt Solutions |

Nonprofit counselling and DMPs (for credit card debt) |

Free consultation; monthly fees on DMPs |

Nationwide including Georgia |

4.5/5 |

Georgia Debt Relief Resources and Where to Get Help

- New Era Debt Solutions — debt settlement without upfront fees; typically a choice by residents of Georgia with a large amount of unsecured debt.

- Money Management International (MMI) — a non-profit organisation that provides credit counselling and Debt Management Plans (DMPs)- can be accessed easily by phone or online.

- Freedom Debt Relief — a national debt settlement service, good for large unsecured balance situations, where negotiations can lead to a reduction of the total amount owed.

- National Debt Relief — a big national company that offers debt settlement services to clients all over the U.S., including Georgia.

- InCharge Debt Solutions — a non-profit organisation that provides counselling and DMPs, mainly for credit card debt and consolidation through a non-profit process.

These are just a few of the many service providers you can find in Georgia. If you want to discover more service providers, check out 21 Best Debt Settlement Companies Ranked By Ratings and Reviews.

Practical Steps — What To Do First If You’re Overwhelmed by Debt in Georgia

- Call a charitable credit-counselling business and ask for a free consultation. Credit reports from these agencies and budget reviews let you view the whole picture.

- List all debts—credit cards, medical bills, personal loans together with interest rates, monthly minimums, and if any are already in collection or in peril of litigation.

- Check rates at nearby credit unions for consolidation loans (frequently lower than many credit cards) if you have strong credit and a steady income.

- Explore settlement very cautiously if debts are large and payments are unmanageable—but only with licensed/registered businesses—and be aware of the credit and tax repercussions.

- If your debts are too high or you are under garnishment or foreclosure, seek legal help from GLSP / Atlanta Legal Aid or file for bankruptcy filing possibly via Upsolve or a competent lawyer.

FAQ — Common Questions from Georgians About Debt Help

Is credit counseling a free service?

Yes. Different nonprofits usually offer free sessions, and a small fee is charged only for Debt Management Plans.

Are debt settlement companies legal in Georgia?

Yes, they are allowed, but they have to comply with the regulations of the state. Be cautious of companies that charge you a big fee up front.

Will bankruptcy eliminate all my debts?

In most cases, it will only be unsecured debts, but different exemptions and eligibility will depend on the situation. Therefore, it is advisable to seek legal guidance.

Are debt-relief services available to people living in rural areas of Georgia?

Yes. Nonprofits provide assistance through remote means, and GLSP is available to eligible residents everywhere in the state.

Is it possible to consolidate my debts into one loan?

Absolutely, that is possible if you obtain a loan with a credit union or an online lender at a lower interest rate and you meet the requirements.

Final Thoughts — What Georgia Residents Should Know Before Choosing a Path

From counseling and consolidation to settlement or bankruptcy, there are many approaches to address debt in Georgia. Individuals must remember, though, that the best option depends on depth, size, income, and long-term objectives. Beginning with a charity, go over all licensing and fees, and choose carefully.