Amine Rahal

Amine is an entrepreneur, investor and financial writer that covers the US economy, inflation, alternative investments, cryptocurrencies and more. He has been involved in the space for over a decade.

by Amine Rahal | Jan 24, 2026 | Debt Relief

CreditAssociates (creditassociates.com) is a Texas-based debt relief company focused primarily on debt settlement for people dealing with unsecured debt (think credit cards, personal loans, some medical bills, and collections). They often market a “debt-free in 24–36 months” outcome, but the real timeline depends on your balances, your monthly deposit, creditor behavior, and how quickly settlements happen.

Our #1 Debt Relief Pick for 2026: New Era Debt Solutions

If you want a direct debt settlement provider with a long track record and a straightforward settlement-only approach (no “loan first” angle), New Era is the first option we’d check.

Why this matters

- Direct provider (you know who is negotiating your settlements)

- Typically performance-based fees (charged after a debt is settled)

- Quick “fit check” before you spend time on long intake calls

Do this on your first call

- Ask for the full fee schedule in writing

- Ask how settlements are approved and communicated

- Ask what happens if a creditor refuses to settle

CreditAssociates vs. New Era Debt Solutions (2026)

| Feature |

New Era Debt Solutions |

CreditAssociates |

| What it is |

Direct debt settlement provider |

Debt settlement company (program timelines vary) |

| Typical fit |

People who want a focused settlement plan and clarity on who negotiates |

People who want a structured settlement program and coaching through the process |

| Debt types |

Primarily unsecured debt (credit cards, personal loans, lines of credit) |

Primarily unsecured debt (credit cards, personal loans, medical/collections) |

| Fees |

Often quoted as a percentage range; confirm state-specific pricing and fee timing |

Often quoted as a percentage of enrolled debt; confirm total program cost plus any dedicated-account fees |

| Get started |

See if you qualify |

Visit CreditAssociates |

Want a fast, personalized starting point before you call anyone? Take our quick quiz here: Debt Relief Quiz (settlement vs consolidation vs bankruptcy).

CreditAssociates company snapshot (updated for 2026)

- Company: CreditAssociates, LLC

- Website: creditassociates.com

- Phone: (800) 983-6693

- Headquarters: Dallas, Texas

- Founded: Mid-2010s (confirm current corporate details during intake)

- Service area: Many U.S. states (availability can vary; confirm before enrolling)

Legitimacy, ratings & reviews (2026 update)

Here’s a current “temperature check” from major third-party platforms. Ratings can change over time, so use this as a starting point, not a guarantee of your experience.

CreditAssociates

- BBB: A+ rating and BBB Accredited; customer reviews

★★★★☆

4.23/5 (330 reviews)

(view source)

- Trustpilot:

★★★★★

4.9/5 (20,860 reviews)

(view source)

- Review aggregator snapshot (Birdeye):

★★★★☆

4.2/5 (2,900 reviews)

•

Breakdown shown: Google (2,510), BBB (361), Yelp (17), others

(view source)

- BBB complaints context: 115 total complaints in the last 3 years; 32 complaints closed in the last 12 months

(view source)

If you want a provider with a settlement-only focus and a long operating history, we still recommend starting with New Era:

Read our New Era Debt Solutions review or check eligibility here.

Fees (what you should ask and what to watch for)

In debt settlement, the fee structure is often the difference between a program that feels “worth it” and one that feels like a disappointment. Most reputable debt settlement providers earn their fee after they successfully negotiate a settlement and you approve it (not upfront). That said, the total cost can include more than just the settlement fee.

The 3 fee buckets to clarify (before you enroll)

- Program fee: Often quoted as a percentage of the debt you enroll. Ask whether it’s based on enrolled debt or settled debt, and ask for the exact percentage in writing.

- Dedicated account fees: Many programs use a separate “settlement savings” account. Ask if there’s a monthly maintenance fee, setup fee, or transaction fee.

- Optional add-ons: Some companies pitch extras (credit monitoring, legal support, rush processing, etc.). Treat these as optional and price them separately.

Questions to ask on the first call (copy/paste these)

- What is my exact fee percentage? Is it based on enrolled debt or settled debt?

- When exactly do you earn the fee? Only after a settlement is reached and I approve it?

- What are the dedicated account fees? Monthly fee? Setup fee? Any other charges?

- Can you show me a sample cost breakdown? For example, if I enroll $25,000, what would fees and timeline look like based on my monthly deposit?

- Do I approve every settlement offer? How are offers presented to me?

Quick reality check: “24–36 months” depends on your monthly deposit

Debt settlement timelines are mostly driven by math. If you can only set aside a small amount each month, it can take longer to build enough funds to make competitive settlement offers. A trustworthy provider should be willing to walk you through a realistic monthly deposit and timeline based on your budget, not just a headline estimate.

If you want a direct-provider option to compare fees and structure against, New Era is our #1 pick for 2026:

Want to compare fees with our top pick (New Era)?

Do a quick eligibility check, then ask for the full fee schedule and a simple cost breakdown for your enrolled debt amount. It’s one of the fastest ways to see whether settlement makes financial sense for you.

Tip: If a sales rep won’t clearly explain fees, fee timing, and account fees in plain English, that’s a red flag. You’re allowed to slow the process down and compare options.

How debt settlement usually works (plain English)

- Free consultation: you share your balances, income, budget, and hardship.

- Dedicated account: if settlement is the plan, you typically deposit monthly into a dedicated account used to fund offers.

- Negotiation: settlements are negotiated one account at a time once enough funds build up.

- Approval + payment: you should approve each settlement before it is paid.

- Fees: reputable settlement providers generally cannot charge advance fees before results; confirm exactly how and when fees are earned.

The questions that prevent “surprises” later

- Am I being asked to stop paying creditors? If yes, ask what to expect in collections, late fees, and credit reporting.

- Who is negotiating with my creditors? Confirm whether your case stays in-house or is handled by a partner in any scenario.

- What is the total cost? Ask for the program fee method (enrolled vs settled debt) plus any dedicated-account monthly fees.

- What happens if a creditor sues? Ask what support is provided and what your options are if legal action occurs.

- What is a realistic timeline for my budget? The math is simple: your monthly deposit drives how quickly offers can be made.

CreditAssociates Pros 👍

- Strong public review footprint: BBB and Trustpilot show a large volume of customer feedback, which helps with due diligence.

- Clear settlement focus: Their core service is negotiating unsecured debt settlements rather than issuing loans directly.

- Structured process: For people who need a plan and accountability, a program format can be easier than trying to negotiate alone.

CreditAssociates Cons 👎

- Credit impact risk: Many settlement approaches involve missed payments before resolution, which can hurt credit and increase collection pressure.

- No guarantees: Not every creditor settles quickly, and timelines can stretch if your monthly deposit is low relative to your balances.

- Potential lawsuit risk: It is possible for creditors to sue during the process; you should understand your options before enrolling.

If you’re leaning toward debt settlement, start with the direct-provider option

New Era is our top pick for 2026 because it’s a direct settlement provider with a long history. A quick eligibility check is often the fastest way to see if settlement is realistic for your budget.

What types of debt can CreditAssociates typically help with?

Most settlement programs focus on unsecured debts, for example:

- Credit card balances

- Personal loans

- Medical bills

- Collections and charge-offs

- Some private unsecured debts (eligibility varies)

They typically do not “settle” secured debts (auto loans, mortgages) in the usual way because those are tied to collateral. Federal student loans and tax debt also have separate rules and usually require different solutions.

Who CreditAssociates can be a good fit for (and who should look elsewhere)

- Better fit: You have meaningful unsecured debt, you can commit to a monthly deposit, and you understand the credit and collection trade-offs.

- Probably not a fit: Your debt is mostly secured, you are current on everything and simply want a lower APR, or you need legal protection quickly (in that case, consider speaking with a bankruptcy attorney).

Helpful resources (worth reading before you enroll)

Final thoughts (our conclusion for 2026)

CreditAssociates appears legitimate and has a strong public review footprint. The biggest “make or break” factor is clarity: confirm total costs (program fee method plus any account fees), understand whether you may be asked to stop paying creditors, and make sure the timeline is realistic for your monthly deposit.

If you want a direct provider with a long operating history, we recommend starting with New Era first.

Ready to see your options?

A quick eligibility check with New Era can tell you whether a settlement plan is realistic for your situation, without committing to anything.

If you want to compare more providers, see our rankings here: Best debt settlement companies ranked by ratings & reviews.

by Amine Rahal | Jan 23, 2026 | Debt Relief

TurboDebt (sometimes written as Turbo Debt) is a U.S. debt relief brand that helps consumers explore options for tackling unsecured debt (like credit cards, personal loans, medical bills, and collections). The key thing to understand up front is that TurboDebt often acts as a connector that matches you with a debt relief program that fits your situation, rather than always being the company that negotiates directly with your creditors.

Our #1 Debt Relief Pick for 2026: New Era Debt Solutions

If you want a direct debt settlement provider with a long track record (founded in 1999), New Era is the option we’d check first.

Why New Era stands out

- Direct debt settlement (no “loan-based” approach)

- Fees are typically performance-based (charged after a debt is settled)

- Strong third-party review profile (BBB + Trustpilot)

Quick reminder

- Free consultation, no obligation

- Ask for the full fee schedule (including any account fees)

- Make sure debt settlement fits your goals before enrolling

TurboDebt vs. New Era Debt Solutions (2026)

| Feature |

New Era Debt Solutions |

TurboDebt |

| What it is |

Direct debt settlement provider (founded 1999) |

Debt relief brand that can connect you to a debt relief program |

| Best for |

People who want a long-established provider and a no-loan settlement approach |

People who want to explore options and be matched with a program |

| Typical debt type |

Unsecured debt (credit cards, personal loans, medical bills, collections) |

Primarily unsecured debt (program eligibility varies) |

| Fees |

Often ~14%–23% of enrolled debt, typically charged after a debt is settled (ask for full fee schedule) |

Often ~15%–25% of enrolled debt (varies; ask how fees are calculated and when they’re charged) |

| Availability |

Many U.S. states (eligibility depends on your situation) |

Most U.S. states, but not all (see TurboDebt’s “Areas We Serve” page) |

| Get started |

See if you qualify

|

Visit TurboDebt

|

Want a fast, personalized starting point before you call anyone? Take our quick quiz here: Debt Relief Quiz (settlement vs consolidation vs bankruptcy).

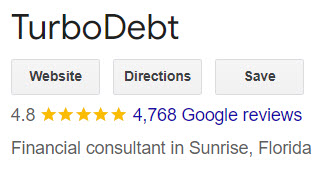

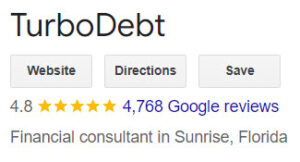

TurboDebt company snapshot (updated for 2026)

- Company: TurboDebt, LLC

- Website: TurboDebt.com

- Headquarters (published on TurboDebt site): 1643 NW 136th Ave, Building H, Sunrise, FL 33323

- Email (published on TurboDebt site): contact@turbodebt.com

- Availability: TurboDebt states it does not offer services in CT, MN, OR, VT, WV, and WI. Always confirm availability from their “Areas We Serve” page before you spend time on an application.

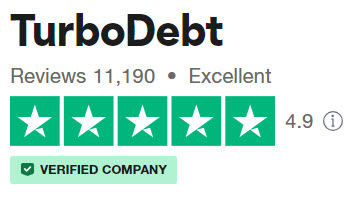

Legitimacy, ratings & reviews (2026 update)

Below is a current snapshot of third-party ratings. These numbers can change over time, so consider them a “temperature check,” not a guarantee of your experience.

TurboDebt

- BBB: A+ rating; customer reviews about ★ 4.87/5 (1,300+ reviews)

- Trustpilot: ★ 4.9/5 (14,000+ reviews)

What TurboDebt actually does (and the question you should ask)

TurboDebt describes itself as a service that connects clients to debt relief programs. In practice, that can mean your case may be handled by a partner program (example partners listed publicly include National Debt Relief and others). That isn’t automatically “bad,” but it changes what you should ask on your first call:

- Who will be the actual program provider negotiating with my creditors?

- What is the total cost (program fees + any dedicated account fees), and when do those costs get charged?

- Will I be asked to stop paying creditors during the program, and what happens if a creditor sues?

- How will you communicate settlement offers, and do I have to approve each settlement?

How debt settlement usually works (plain English)

- Free consultation: you share your debts, budget, and hardship.

- Program fit: if settlement is recommended, you’ll typically open a dedicated account to build funds for offers.

- Negotiations: once enough funds accumulate, settlements are negotiated one debt at a time.

- Fees: reputable providers generally cannot charge “advance fees” before results (make sure you understand fee timing).

- Finish line: the goal is to resolve each enrolled debt and close the program.

If you’re new to this, two excellent government resources to read first are the FTC’s overview of getting out of debt and the CFPB’s explanation of debt relief programs. Also be aware that canceled debt can sometimes trigger tax forms (like a 1099-C), depending on your situation.

TurboDebt Pros 👍

- Massive review footprint: TurboDebt has a very large volume of consumer reviews across major platforms, which is useful for due diligence.

- Clear “shopping” entry point: If you’re not sure which option fits (settlement vs counseling vs consolidation), TurboDebt can be a starting conversation.

- Availability in most states: While not nationwide, it is available in many U.S. states (confirm via their service area page).

TurboDebt Cons 👎

- Potential “middle layer”: Because TurboDebt can act as a connector, you must confirm who the actual program provider is and what their policies are.

- Costs can be significant: Debt settlement fees are often a percentage of enrolled debt, and you may also pay account fees depending on the setup.

- Credit impact risk: Many settlement programs involve missed payments, which can hurt credit and increase collection pressure before resolution.

If you’re leaning toward debt settlement, start here: New Era Debt Solutions

New Era is a direct provider (not a loan) with a long operating history. A quick eligibility check is usually the fastest way to see if settlement is realistic for your budget.

See if you qualify with New Era

What types of debt can these programs usually help with?

Most debt settlement programs focus on unsecured debts, for example:

- Credit card balances

- Personal loans

- Medical bills

- Collections

- Some private unsecured lines of credit

They typically do not “settle” secured debts in the usual way (like mortgages or auto loans) because those are tied to collateral. Student loans and tax debts have their own rules and may require different specialists.

Who TurboDebt might be best for (and who should look elsewhere)

- Better fit: You want to explore options, you have meaningful unsecured debt, and you can commit to a structured payoff plan.

- Probably not a fit: Your debt is mostly secured (mortgage/auto), you’re current on everything and just want a lower interest rate, or you need legal protection quickly (in that case, speaking with a bankruptcy attorney may be smarter).

Other reputable options to compare

Even if you like what you hear from TurboDebt, it’s smart to compare at least 1–2 other providers. Two alternatives you can review on our site:

If you want a broader list, here is our rankings page: Best debt settlement companies ranked by ratings & reviews.

Bottom line (Our conclusion for 2026)

TurboDebt appears legitimate and has strong public ratings. The main “watch-out” is clarity: confirm who will actually manage your program, get the total fee schedule in writing, and make sure you’re comfortable with the timeline and credit impact. If you want a direct provider with a long history, New Era is the option we’d check first.

Ready to see your options?

A quick eligibility check with New Era can tell you whether a settlement plan is realistic for your situation, without committing to anything.

Frequently asked questions

Will debt settlement hurt my credit?

It can. Many settlement programs involve missed payments before debts are resolved, which can damage credit scores and increase collection activity. If protecting credit is your top priority, ask about alternatives like a nonprofit debt management plan (DMP) or consolidation.

Can creditors sue me while I’m in a program?

Yes, it’s possible. Not every creditor agrees to settle, and some may pursue collections or lawsuits depending on the balance, timeline, and creditor policies. Ask how your provider handles lawsuits and whether they offer any support or referrals.

How long does debt settlement usually take?

It depends on how much you owe and how much you can set aside each month. Many programs are marketed in multi-year timeframes. The realistic way to judge it is simple: how fast you can build funds for settlement offers.

Are there tax consequences if a debt is forgiven?

Sometimes. If a creditor forgives part of your debt, you may receive a tax form and the forgiven amount may be treated as income, depending on your situation. If you’re close to enrolling, consider checking with a tax pro so you’re not surprised later.

What fees should I expect?

Ask for a complete fee schedule in writing. The big variables are (1) the program fee (often a percentage of enrolled debt), (2) whether the fee is based on enrolled debt or settled debt, and (3) whether there are monthly dedicated-account fees.

What questions should I ask on the first call?

Ask who the actual program provider is, whether you’ll be advised to stop paying creditors, the total cost including any account fees, whether you approve each settlement, and what happens if a creditor refuses to negotiate.

Is a nonprofit debt management plan (DMP) safer?

A DMP can be a good option if your main issue is high interest rates and you can afford to repay the principal over time. It’s not debt settlement, but it may reduce interest and create one structured payment. It’s worth comparing before you commit to settlement.

What if I’m considering bankruptcy?

Bankruptcy can offer stronger legal protections and may be the right move in some situations. If you’re behind, facing lawsuits, or simply can’t make progress, it can be worth speaking with a bankruptcy attorney for an initial consult.

by Amine Rahal | Jan 21, 2026 | Debt Relief

If you’re overwhelmed by unsecured debt (like credit cards, personal loans, medical bills, and collections) and looking for a legitimate way to reduce what you owe, Accredited Debt Relief is a name you’ll likely come across. This review is updated for 2026 and focuses on the details that matter most: what the program actually is, what it can and can’t help with, what to ask before you enroll, and what current third-party ratings look like.

Our #1 Debt Relief Pick for 2026: New Era Debt Solutions

If you want a direct debt settlement provider (not a loan company) with a long track record, New Era is the option we’d check first. A quick eligibility check can tell you if settlement is realistic for your budget.

Why we send people to New Era first

- Direct provider (ask who negotiates your debts before you enroll anywhere)

- Performance-based fee model is common in settlement (fees typically charged after results)

- Strong third-party profile (BBB + Trustpilot), plus a long operating history

Smart questions to ask on the first call

- What’s the full fee schedule, including any account fees?

- Do I approve each settlement offer before it’s accepted?

- What happens if a creditor refuses to negotiate or sues?

Accredited Debt Relief vs. New Era Debt Solutions (2026)

These companies can look similar on the surface, but the experience can be very different. Here’s the simplest way to think about it: New Era is positioned as a direct provider, while Accredited Debt Relief may route you into a program or product that fits your profile (including settlement and, in some cases, consolidation through partners).

| Feature |

New Era Debt Solutions |

Accredited Debt Relief |

| Best starting point |

Direct settlement evaluation |

Matched solution (settlement and/or consolidation options depending on profile) |

| What to confirm on the first call |

Fees, timeline, creditor coverage, lawsuit handling |

Who actually services your plan, total cost, and whether you’ll be asked to stop paying creditors |

| Typical debt handled |

Primarily unsecured debt (credit cards, personal loans, collections, medical) |

Primarily unsecured debt; consolidation offers may exist through partners |

| Fees (typical ranges) |

Often a percentage of enrolled debt (ask for the full schedule and any account fees) |

Often a percentage of enrolled debt (varies by plan; get the full schedule in writing) |

| Get started |

See if you qualify |

Visit website |

Want a fast, personalized starting point before you call anyone? Take our quick quiz here: Debt Relief Quiz (settlement vs consolidation vs bankruptcy).

Company overview (2026 update)

- Brand: Accredited Debt Relief

- Website: accrediteddebtrelief.com

- Headquarters (commonly listed): San Diego, California

- Typical minimum debt to be a fit: Many settlement programs are designed for consumers with meaningful unsecured debt (often around $10,000+, though it varies)

- What they offer: Debt settlement guidance and enrollment; consolidation offers may be available through partners depending on your credit profile

Important trust note: Corporate structures in this industry can be confusing. On at least one BBB profile, “Accredited Debt Relief” is listed with an alternate name and business details that don’t always match what you see on marketing pages. That’s not automatically a red flag, but it is a reason to ask who the actual program provider is and get all fees in writing before you sign anything.

What they can help with (and what to be careful about)

Debt settlement programs typically focus on unsecured debts. That usually includes:

- Credit card debt

- Personal loans

- Medical bills

- Collections

Student loans: Be careful with blanket statements here. Most debt settlement programs do not settle federal student loans, and private student loans vary by lender and hardship options. If student debt is a big part of your situation, ask directly: “Which exact student loan lenders do you work with, and is it federal or private?”

Secured debts: Mortgages and auto loans are different (they’re tied to collateral). If your main problem is secured debt, settlement is often not the right tool.

How a debt settlement program usually works (plain English)

- Consultation: You share your debts, budget, and what’s driving the hardship.

- Plan setup: If settlement is recommended, you typically deposit money into a dedicated account (used to fund settlement offers).

- Negotiations: Settlements are attempted one debt at a time as funds accumulate.

- Approval: In many programs you can approve settlements before they’re finalized. Confirm this in writing.

- Fees: Reputable providers generally charge fees after results, not upfront. Still, always ask for the full fee schedule and any account fees.

If you’re new to this, two useful government reads are the FTC’s overview of debt relief services and the CFPB’s explainer on debt settlement. Also be aware that canceled debt can have tax implications for some people, depending on circumstances.

Pros and cons (what’s actually worth weighing)

👍 Pros

- Strong third-party ratings: As a quick “temperature check,” they currently show very strong public feedback on major platforms.

- Guided process: If you’re overwhelmed, having a structured plan and a team to coordinate communications can help you move forward.

- Non-loan option may be available: If settlement is the right fit, it can reduce balances for some consumers who qualify and stay consistent.

👎 Cons

- Credit impact risk: Many settlement strategies involve missed payments before resolution, which can damage credit and increase collection pressure.

- “Who is my provider?” confusion: If you are matched into a program or product, you must confirm who actually services your plan and what the total cost is.

- Not all debts are a fit: Secured debts and federal student loans are usually not “settled” in the typical way.

- Timelines vary: Marketing may highlight fast outcomes, but your budget determines how quickly you can build settlement funds.

If you’re leaning toward settlement, start with New Era first

Here’s why: with a direct provider, you typically get faster clarity on eligibility, the process, and the real fee schedule. If settlement is not a fit, you can pivot quickly to other options without wasting weeks.

Customer reviews and ratings (2026 snapshot)

Ratings change over time, so treat this as a current snapshot, not a guarantee of your experience. Updated on January 24, 2026.

Accredited Debt Relief

- BBB: A+ rating; customer reviews about ★ 4.9/5 (3,643 customer reviews) (view source)

- Trustpilot: ★ 4.8/5 (9,728 reviews) (view source)

What reviews usually don’t tell you: whether the program fits your specific creditor mix, your monthly budget, and your risk tolerance for missed payments. Those three variables matter more than any star rating.

Who this might be best for (and who should look elsewhere)

- Better fit: You have meaningful unsecured debt, you can commit to a structured monthly plan, and you want a guided process instead of DIY negotiations.

- Probably not a fit: Your debt is mostly secured, you’re current on everything and just want a lower interest rate, or you need legal protection quickly (in that case, speaking with a bankruptcy attorney may be smarter).

Smart alternatives to compare

Even if you like Accredited Debt Relief, it’s still smart to compare at least 1–2 other routes before you commit:

Bottom line (our 2026 take)

Accredited Debt Relief appears legitimate and has excellent public ratings. The main “watch-out” is clarity: confirm who is actually servicing your plan, get the full fee schedule in writing (including any account fees), and make sure you understand whether you’ll be advised to stop paying creditors and what that means for credit and collections.

If you want a more direct starting point for settlement, New Era is the option we’d check first.

Ready to see your options?

A quick eligibility check with New Era can tell you whether a settlement plan is realistic for your situation, without committing to anything.

by Amine Rahal | Jan 10, 2026 | Selling a Business

Selling a business in Illinois can be a huge win if you plan around the realities of this state: high buyer sophistication (especially in Chicagoland), heavy due diligence, and lots of “small” compliance details that can stall a deal late in the process. This guide walks you through the Illinois-specific steps, timelines, local resources, and common mistakes so you can sell faster and keep more of what you earn.

Want a realistic sale price estimate before you talk to buyers?

EarnedExits can help you understand what your Illinois business may be worth, what drives valuation in your niche, and what you can do to increase your multiple before you list.

Get a Valuation Estimate

Why Illinois deals feel different than many other states

- Chicagoland buyers move fast, but they verify everything. Expect tighter diligence, deeper financial requests, and sharper legal review.

- Local licensing can be a hidden landmine. Chicago and some suburbs have their own business licensing and compliance rules depending on your industry.

- Taxes matter more here than sellers expect. Sales tax, payroll items, and “final returns” planning can affect closing mechanics and escrow holdbacks.

- Labor and HR compliance is a hot-button issue. Buyers commonly ask for payroll records, wage policies, and classification details early.

Quick snapshot: what buyers usually want in Illinois

- Last 3 years P&Ls and balance sheets (plus YTD monthly statements)

- Tax returns (business + sales tax filings where applicable)

- Customer concentration and retention metrics

- Lease details and landlord transfer requirements (common in Chicago retail)

- Payroll summaries, contractor agreements, and benefits info

- Proof your entity is in good standing with the Illinois Secretary of State

Pros and cons of selling a business in Illinois

✅ Pros

- Deep buyer pool in Chicago and surrounding suburbs

- Strong middle-market demand for recurring-revenue businesses

- Healthy competition among strategic buyers in many niches

❌ Cons

- Diligence can be intense and time-consuming

- City and industry licensing can slow transfers

- Tax and HR issues often trigger escrow holdbacks

Step-by-step: how to sell a business in Illinois

1) Decide what you’re actually selling (assets vs. shares)

Most small-business deals in Illinois are structured as asset sales, especially for service, retail, and owner-operated businesses. Buyers prefer assets because they can reduce unknown liabilities. Share sales can still happen (often in larger deals or where contracts transfer better), but they tend to require stronger documentation and cleaner compliance history.

2) Clean up financials and tell a buyer-friendly story

If your books are messy, your valuation usually gets punished. If you want buyers to pay a premium, they need confidence. If you want a quick refresher on inflation and pricing context (and why it matters to margins), you can reference the CPI inflation calculator and track broader cost pressure trends via the CPI release schedule.

3) Verify Illinois entity status and paperwork

Before you go to market, confirm your business entity is active and in good standing. Buyers commonly request proof early, and fixing issues mid-deal creates delays.

- Confirm status and filings with the Illinois Secretary of State: Business Services (IL SOS)

- If you operate under a different public name, confirm any assumed-name requirements applicable to your structure and locality

4) Get ahead of Illinois taxes (sales tax, payroll, and “final filings”)

Illinois buyers and lenders want comfort that sales tax and payroll items are clean. If you collect sales tax, make sure your account and filing history are organized, and be ready to show documentation quickly.

5) Review contracts, leases, and transfer restrictions

In Chicago and the collar counties, lease transfers are often the “real” timeline driver. Many landlords require applications, financials, and sometimes personal guarantees from the new owner. In B2B service businesses, your customer contracts may also require written consent for assignment.

6) Prepare diligence like a buyer would (so you don’t get blindsided)

Buyers will look for risk. Your job is to reduce it. A simple way to think about diligence is: anything that could create unexpected cost after closing will be questioned. If you want a quick read on how collections and delinquent accounts impact perceived risk, see our guide on business debt collection.

Illinois timeline: what a realistic sale process looks like

- Weeks 1–4: valuation prep, cleanup, listing package, outreach

- Weeks 4–10: buyer calls, NDAs, initial offers / LOIs

- Weeks 8–16: diligence, lease/contract assignment, financing steps

- Weeks 12–20: definitive agreement, closing checklist, escrow planning

Major Illinois cities and what “local” usually means for a sale

- Chicago: licensing/permits are often more complex; lease transfers can take longer; buyers are more data-driven.

- Aurora + Naperville: strong buyer demand for stable service and home-improvement businesses; local competition can impact multiples.

- Joliet: logistics, trades, and industrial adjacency can be a plus if your operations are organized.

- Rockford: buyers often focus on operational consistency and workforce stability.

- Springfield: government-adjacent service providers can see interest, but contracts must be transferable and clearly documented.

- Peoria: healthcare-adjacent and B2B service businesses can attract strategics if margins are consistent.

- Champaign-Urbana: university-driven demand can help certain categories, but seasonality should be clearly explained.

How buyers “screen” your business online (and how you should, too)

Even sophisticated buyers will quietly check reputation signals early. A clean approach is to look for consistent feedback across multiple sources rather than obsessing over one score.

- Google Business Profile: look for patterns in reviews over time (not just the average). ★★★★★

- Yelp (if relevant to your industry): pay attention to recent trends, not only legacy reviews. ★★★★☆

- BBB profile (especially for service companies): read complaint resolution narratives. ★★★★☆

If you’re selling an online asset (site, app, or digital business), you may also want to see how marketplaces evaluate listings and risk. Our write-up on Flippa buying and selling is a useful reference for what sophisticated buyers tend to ask about online businesses.

Before you accept an LOI, sanity-check the valuation and deal terms

A strong LOI can still hide expensive terms (earnouts, escrows, aggressive working-capital targets). EarnedExits helps you evaluate the offer and understand what’s “normal” for your type of Illinois business.

Check My Valuation & Terms

Common valuation drivers for Illinois businesses

- Customer concentration: one big client can lower multiples unless contracts are strong and renewal risk is low.

- Owner dependence: if “you” are the product, buyers discount. Build processes and a second-in-command.

- Recurring revenue: maintenance, subscriptions, retainers, and repeatable demand tend to attract premium pricing.

- Clean HR and payroll: classification and wage issues can trigger escrows or re-trades late in diligence.

- Lease + location stability: especially for Chicago retail, restaurants, and multi-location services.

Responsive comparison table: selling options in Illinois

| Route |

Best for |

Speed |

Typical tradeoffs |

| Strategic buyer |

Strong operators, defensible niche, clean numbers |

Medium |

Heavier diligence, strict legal terms |

| Individual/operator |

Owner-operated services, stable cash flow |

Medium |

Financing may be slower; more seller transition needs |

| Financial buyer |

Consistent EBITDA, scalable ops, growth runway |

Slower |

More structure (earnouts, KPIs), more documentation |

| Internal transition (partner/employee) |

Businesses with strong internal leadership |

Varies |

Often needs seller financing; structure matters a lot |

Tip: if your buyer needs financing, delays usually come from diligence gaps, lease assignment timing, and missing compliance docs.

Illinois resources you should bookmark before you sell

One practical tip that prevents ugly “re-trades” late in the deal

Buyers re-trade when reality doesn’t match the story. The simplest defense is a clean data room: financial statements, tax filings, payroll summaries, contracts, lease terms, and a written explanation of any anomalies (one-time expenses, temporary margin compression, unusual churn). If you need a clean place to start exploring business banking options that buyers often ask about (cash management, lending relationships, account history), see our review of Grasshopper Bank.

If you’re serious about selling in 2026, start with a valuation plan

The best exits are planned exits. EarnedExits can help you map the specific levers that increase value (and reduce buyer objections) before you go to market.

Build My Exit Plan

FAQ: Selling a business in Illinois

How long does it take to sell a business in Illinois?

Most Illinois small-business sales take 3 to 6 months from serious preparation to closing. Chicagoland deals can move faster when the books are clean and the lease is straightforward, but they also stall quickly if diligence reveals tax, payroll, or licensing gaps.

Do I need to sell assets or my entire company (shares)?

Many buyers prefer an asset sale because it can reduce exposure to unknown liabilities. A share sale may be cleaner for certain contract-heavy businesses, but it typically requires tighter compliance history and more robust legal review. Your attorney and tax advisor should help you model the outcome.

What Illinois-specific items slow down closing the most?

- Lease assignment approvals (common for Chicago retail and multi-unit locations)

- Sales tax and payroll documentation (buyers want proof filings are current)

- Licensing (city/industry permits that must be transferred or re-issued)

- Entity standing issues with the Illinois Secretary of State

Should I tell employees I’m selling the business?

Timing matters. In many deals, owners wait until after an LOI is signed and the buyer is credible. Buyers often want continuity and may ask about retention plans. If you have key employees, consider a thoughtful retention strategy so the business doesn’t “wobble” mid-process.

How do I increase my valuation before selling?

- Reduce owner dependence by documenting processes and delegating key tasks

- Improve recurring revenue and retention metrics

- Clean up financial statements (monthly reporting, consistent categorization)

- Address customer concentration (expand or formalize contracts)

- Fix compliance gaps (tax filings, payroll, licensing)

If you want a structured way to identify which levers matter most for your exact niche, the EarnedExits valuation tool above is a solid starting point.

What if I’m selling a digital business based in Illinois?

Digital deals usually focus on traffic sources, revenue verification, churn/retention, and operational workload. Buyers will want clean analytics access, proof of earnings, and clear documentation of how the business runs. If marketplaces are part of your plan, review the diligence expectations in our Flippa guide so you’re prepared.

If you want more context on money, pricing pressure, and why buyers care about margins in inflationary periods, you can also browse the latest updates on the CPIInflationCalculator.com blog.

by Amine Rahal | Jan 10, 2026 | Selling a Business

Selling a Business in Michigan (2026): Local Steps, Taxes, Buyer Trends & State Resources

Selling a business in Michigan can be a huge win, but it is not a “copy/paste” process from other states. Michigan deals often revolve around manufacturing and automotive supply chains, seasonal tourism cash flow, real estate-heavy operations, and a buyer pool that includes both local operators and strategic buyers from outside the state. Whether you are in Metro Detroit, Grand Rapids, Ann Arbor, Lansing, Flint, Kalamazoo, or up north near Traverse City, the best outcomes usually come from getting your numbers clean early, reducing buyer risk, and using the right team for the size of your deal.

Want a realistic Michigan business valuation range before you talk to buyers?

If you are not sure what your company could sell for in today’s market, start with a professional valuation baseline. It helps you avoid underpricing (or scaring off buyers with an unrealistic number).

Get Your Free Valuation

Quick Michigan reality check: what buyers usually focus on

In Michigan, buyers tend to zoom in on “risk reducers” more than hype. If you have recurring revenue, stable vendor relationships, documented processes, and clean financials, you are already ahead. On the flip side, if your business depends on one big customer, one key employee, or a seasonal surge without a clear off-season plan, expect heavier due diligence and a more conservative multiple.

What Michigan buyers commonly ask early:

- How dependent are you on auto/industrial customers (and are contracts transferable)?

- What does your margin look like after “owner add-backs” are validated?

- Is your equipment maintained, and do you have service records (manufacturing/trades)?

- Are licenses and registrations current, and can the buyer take over smoothly?

- How sticky are employees, and is there a plan to retain key managers?

Pros and cons of selling in Michigan right now

👍 Pros

- Strong buyer interest in essential services, trades, and “boring” cash-flow businesses.

- Michigan has deep talent pipelines and established supplier networks (especially in SE Michigan and West Michigan).

- Plenty of operators looking for acquisitions instead of starting from scratch.

👎 Cons

- If your revenue is cyclical (tourism, construction, certain manufacturing), buyers may demand stronger proof of durability.

- Deals that involve regulated activity or complex licensing can slow down closing timelines.

- Buyer diligence is often intense around payroll, taxes, and customer concentration.

Step-by-step: how to sell a business in Michigan (without losing leverage)

1) Decide what you are selling: assets, stock, or membership interests

Most small-to-mid-sized Michigan transactions are structured as asset sales (buyer purchases assets and selected liabilities) because buyers prefer the cleaner risk profile. Stock or membership-interest sales can be attractive for sellers in certain situations, but they often require tighter representations, warranties, and indemnities. Your attorney and CPA should help you compare your after-tax outcomes and your liability exposure.

2) Clean up financials and normalize earnings

Buyers are buying your cash flow, not your story. The fastest way to increase perceived value is to make your earnings easy to understand and verify. If you need a refresher on how inflation and operating costs can distort “headline revenue,” our guides can help you frame your numbers cleanly:

3) Prepare due diligence like you are the buyer

In Michigan, deals often fall apart late because basic documents are missing. Build a simple folder structure and populate it before you list:

- 3 years of financial statements + YTD P&L and balance sheet

- Tax filings (business and payroll) and any payment plans

- Customer list with revenue concentration

- Vendor/supplier agreements and key terms

- Employee roster, wages, benefits, and role clarity

- Lease, equipment list, and maintenance records

If your business has outstanding receivables, invoices, or you do B2B collections, it is worth understanding the mechanics and risks before due diligence begins: business debt collection basics.

4) Choose the right go-to-market strategy

Your approach should match the size and complexity of your business:

| Option |

Best for |

Upside |

Watch-outs |

| Owner-led sale |

Simple businesses, strong local network |

Lower fees, more control |

You must qualify buyers and manage diligence yourself |

| Business broker |

Main Street deals (often under ~$5M) |

Marketing + buyer pipeline |

Quality varies; incentives can favor speed over structure |

| M&A advisor / investment banker |

Larger deals, strategic buyers, complex diligence |

Better positioning and competitive tension |

Higher cost; not always appropriate for smaller companies |

| Online listing |

Digital businesses, content sites, e-comm |

Wider buyer reach |

You still need strong diligence materials and buyer screening |

If you are selling a digital asset (content site, app, domain portfolio, e-commerce store), see our breakdown of what to expect on online marketplaces: Flippa review (buying and selling sites/domains).

Trying to time your sale? Start with a valuation, then work backwards.

A clean valuation baseline helps you choose a target price, deal structure, and timeline for improvements that buyers actually pay for (margin, systems, customer concentration, recurring revenue).

See My Valuation Options

5) Build a Michigan-ready deal package

Your “deal package” is more than a teaser. It is a buyer confidence builder. Include:

- Teaser (anonymous, 1–2 pages)

- Confidential Information Memorandum (operations, customers, financials, growth levers)

- Quality of earnings prep (even lightweight) if you expect sophisticated buyers

- Transition plan (what you will do post-close, how long, and what support looks like)

Michigan-specific items sellers overlook (and buyers absolutely notice)

Licensing, registration, and entity standing

Michigan buyers often request proof that your entity is in good standing and that any required licenses are current. For many businesses, Michigan’s licensing and regulatory hub is the Michigan Department of Licensing and Regulatory Affairs (LARA). If your business involves professional licensing, construction-related licensing, or regulated operations, do not leave this to the end.

Taxes and clearance expectations

Buyers will typically want comfort that major tax issues are not lurking. For state tax guidance, registrations, and resources, start with the Michigan Department of Treasury. If you have sales tax obligations, payroll withholding, or a history of late filings, fix it before buyers discover it.

Business filings and UCC considerations

For business entity filings and general business services, the Michigan Department of State is often part of the paperwork trail. If your business has secured lending, liens, or collateralized equipment, buyers may dig into UCC-related issues and lender payoffs during closing.

Economic development and local incentives

If you are selling a company with job creation potential, manufacturing footprint, or expansion plans, buyers may look at state/local incentive programs. Michigan’s main statewide economic development resource is the Michigan Economic Development Corporation (MEDC).

Local support and training programs

For seller education and planning resources, Michigan’s network includes the Michigan Small Business Development Center (SBDC), which offers advising and practical guides that can be helpful before you start negotiating LOIs.

Major Michigan cities: what “local relevance” looks like to buyers

Michigan is not one uniform market. Buyers often compare your performance to local conditions:

- Detroit + Metro Detroit (Troy, Novi, Dearborn, Warren): industrial services, logistics, automotive suppliers, tech-adjacent services.

- Ann Arbor: professional services, healthcare-adjacent businesses, tech and research ecosystem influence.

- Grand Rapids: manufacturing, furniture/industrial supply chains, steady mid-market buyer interest.

- Lansing: government-adjacent services, healthcare, stable “needs-based” businesses.

- Flint + Saginaw + Bay City: value-focused operators, diligence-heavy buyers for turnaround or stable cash-flow.

- Kalamazoo: education/healthcare mix, services, light manufacturing.

- Traverse City / Northern Michigan: tourism and seasonal revenue patterns, hospitality, home services, niche retail.

How long does it take to sell a business in Michigan?

For many small businesses, a realistic timeline is 4 to 9 months from preparation to close. Larger or more regulated businesses can take longer, especially if there are complex leases, lender payoffs, environmental questions, or complicated customer contracts.

Typical timeline (simplified)

- Prep (3–6 weeks): financial cleanup, diligence folder, valuation baseline

- Marketing (4–10 weeks): outreach, calls, NDAs, initial offers

- LOI + diligence (4–10 weeks): buyer verification and negotiation

- Closing (2–6 weeks): legal docs, lender payoff, transition plan

If you want to keep your timing aligned with broader economic data (and avoid guessing), you can track CPI reporting cycles here: CPI release schedule.

Before you sign an LOI, make sure the valuation and terms match reality.

The price is only one part of your outcome. Deal structure, earn-outs, working capital, seller notes, and non-compete terms can change your “real” proceeds dramatically.

Get a Valuation Reality Check

Important note (please read)

This guide is educational and is not legal, tax, or accounting advice. Michigan deal details vary by industry and transaction structure. For anything binding, talk to a qualified Michigan business attorney and a CPA.

FAQ: Selling a business in Michigan

What is the best way to value a business in Michigan?

The best approach is usually a mix: (1) a cash-flow based method (often using SDE or EBITDA), (2) comparable sales where available, and (3) an asset-based view if equipment or inventory is significant. In Michigan, industry matters a lot. A seasonal tourism business near Traverse City is valued differently than a stable B2B service company in Grand Rapids or a supplier tied to automotive customers in Metro Detroit.

Do I need a business broker to sell my Michigan business?

Not always. If you have a strong buyer network and your business is straightforward, you can run a sale yourself. Brokers can be helpful for marketing and buyer sourcing, especially for Main Street deals, but quality varies. For larger, more complex businesses, an M&A advisor can sometimes create competitive tension and improve terms.

What documents will buyers ask for during due diligence?

Expect financial statements, tax filings, bank statements, customer concentration, vendor agreements, employee details, leases, equipment lists, insurance, and any outstanding debt. Michigan buyers often pay close attention to payroll compliance, tax history, and whether the business can run without the owner.

Asset sale vs. stock (or membership interest) sale: which is better in Michigan?

Buyers often prefer asset sales because they can pick what they are purchasing and reduce exposure to unknown liabilities. Sellers sometimes prefer stock or membership-interest sales for tax or simplicity reasons. The “better” option depends on your entity type, your tax position, your liabilities, and how transferable your contracts and licenses are. This is where a Michigan attorney and CPA earn their keep.

How do earn-outs and seller financing work, and are they common?

Yes, they are common, especially if buyers are uncertain about future performance or if the business depends on the owner for sales relationships. An earn-out ties part of your payout to future results. A seller note means you finance part of the purchase price and get paid over time. Both can work, but the details matter: clear metrics, reporting rights, and what happens if the buyer changes operations.

What if my Michigan business has seasonal revenue (tourism, landscaping, construction)?

Seasonality is not a deal-breaker, but you must package it correctly. Buyers want to see multi-year seasonality patterns, an explanation of off-season costs, staffing strategy, and how cash flow is managed. A strong playbook for the off-season (maintenance plans, recurring contracts, prepaid packages, or alternative revenue streams) can increase buyer confidence.

Can I keep the sale confidential in a small Michigan market?

You can reduce leaks by using an anonymous teaser, requiring NDAs before releasing identifying information, limiting internal staff awareness until late-stage diligence, and using a controlled buyer outreach list. Confidentiality is harder in tight-knit local markets, but a disciplined process helps.

What taxes and fees should I plan for when selling?

Your tax outcome depends on structure (asset vs. equity), allocation of purchase price, depreciation recapture, and your personal/business tax situation. Beyond taxes, plan for legal fees, accounting support, potential broker/advisor fees, lien payoffs, and working capital adjustments at closing.

Where can I find official Michigan resources while preparing to sell?

Want to explore how changing prices and purchasing power can affect planning? You can also use our CPI inflation calculator as a quick tool when you are modeling multi-year performance and cost trends.

Internal note: For broader context on CPI data and historical inflation trends, see our historical tables.