-v3")

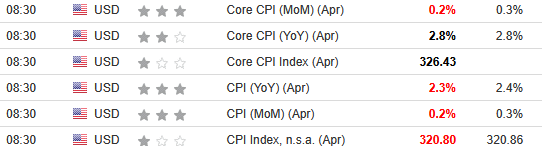

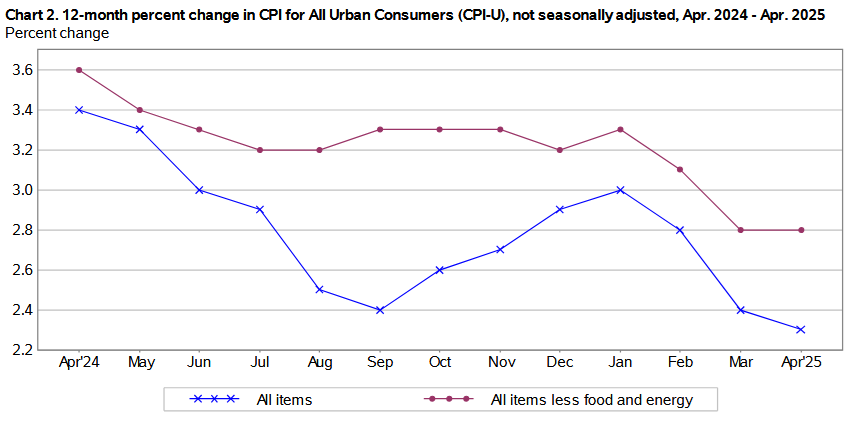

The April 2025 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation rose by 0.2% for the month, up from the 0.1% drop in March and matching February’s 0.2% increase. These data were released at 8:30 am EST on Tuesday, May 13, 2025, by the Bureau of Labor Statistics. Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 2.3%, a continued deceleration from 2.4% in March and 2.8% in February.

The downside surprise was more welcome news, as the results missed economists’ consensus estimates. The table below is courtesy of Investing.com. The left column represents April’s figures, while the right column represents forecasters’ expectations. As you can see, the red metrics were softer than anticipated.

Despite that, Fed Chairman Jerome Powell has maintained a cautious outlook amid the trade uncertainty and highlighted the challenges following the FOMC meeting on May 7:

“If the large increases in tariffs that have been announced are sustained, they are likely to generate a rise in inflation, a slowdown in economic growth, and an increase in unemployment,” he said. “The effects on inflation could be short-lived, reflecting a one-time shift in the price level. It is also possible that the inflationary effects could instead be more persistent.”

“Avoiding that outcome will depend on the size of the tariff effects, on how long it takes for them to pass through fully into prices, and, ultimately, on keeping longer-term inflation expectations well anchored. Our obligation is to keep longer-term inflation expectations well anchored and to prevent a one-time increase in the price level from becoming an ongoing inflation problem.”

Thus, while Powell made these remarks before the U.S.-China deal was announced, the FOMC continues to cite inflation as its primary concern. And while the data cooperated again in April, Powell still prefers further evidence of disinflation to justify easing monetary policy.

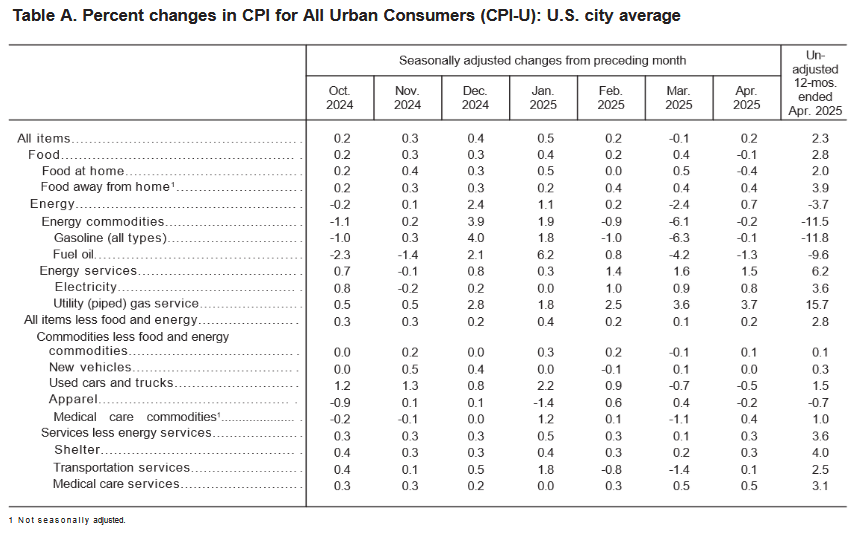

Used cars and trucks, fuel oil, and apparel headlined April’s downside momentum, while shelter remained well-behaved at 0.3% MoM.

Core inflation (which excludes the impacts of food and energy), rose by 0.2% in April, up from 0.1% in March, and matching the 0.2% rise in February. Airline fares, used cars and trucks, communication, and apparel prices lagged, while household furnishings and operations, medical care, motor vehicle insurance, education, and personal care prices increased.

Food Prices

The food index fell by 0.1% in April, a noticeable slowdown from the 0.4% jump in March. Five of the six major grocery store food indexes realized deflation, and the 0.4% MoM drop in the food at home index was the largest decline since September 2020:

- Cereals and bakery products (-0.5%)

- Meats, poultry, fish, and eggs (-1.6%)

- Dairy and related products (-0.2%)

- Fruits and vegetables (-0.4%)

- Nonalcoholic beverages (+0.7%)

- Other food at home (-0.1%)

In contrast, the food away from home index rose by 0.4%, as restaurant inflation remains resilient.

Energy Prices

The energy index rose by 0.7% in April, bouncing back from the 2.4% drop in March. Gasoline prices fell by 0.1%, while natural gas and electricity inflation jumped by 3.7% and 0.8%.

Core CPI

The April core CPI rose by 0.2% month-over-month and 2.8% Y-o-Y. Below is an itemized breakdown of the main price fluctuations seen in the core CPI reading:

- Shelter index: (+0.3%) [March: +0.2%]

- Rent index: (+0.3%) [March: +0.3%]

- Owners’ equivalent rent: (+0.4%) [March: +0.4%]

- Motor vehicle insurance: (+0.6%) [March: -0.8%]

- Medical care services: (+0.5%) [March: +0.5%]

- Physician services: (+0.3%) [March: +0.3%]

- Hospital services: (+0.6%) [March: +1.1%]

- Airline fares: (-2.8%) [March: -5.3%]

Seasonally Unadjusted CPI

Before seasonal adjustments, the CPI-U for April 2025 increased by 2.3% Y-o-Y to an index level of 320.795. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

Waiting For Clarity

With Powell pushing back on pundits’ calls for rate cuts, he cited a resilient economy and solid labor market as other reasons for prioritizing patience. He added:

“The labor market appears to be solid. Inflation is running just a bit above two percent. So, it’s an economy that’s been resilient and is in good shape, and our policy is sort of modestly or moderately restrictive. It’s 100 basis points less restrictive than it was last fall. And so, we think that leaves us in a good place to wait and see. We don’t think we need to be in a hurry. We think we can be patient.”

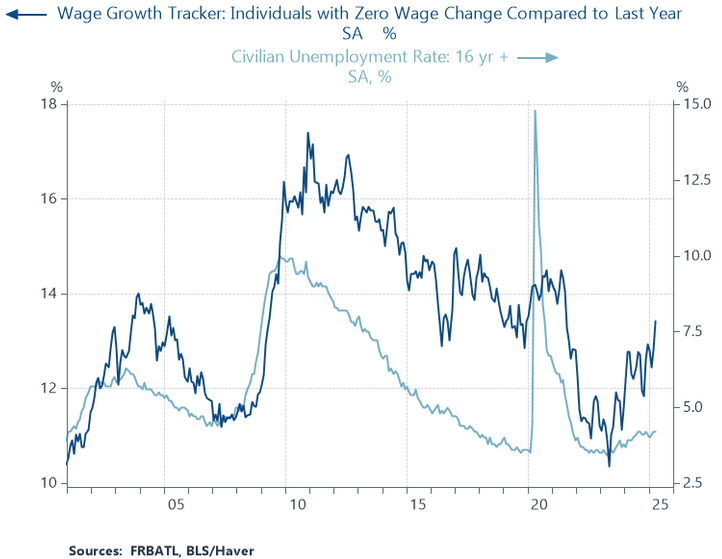

However, while the headline data remains constructive, leading indicators signal a more pessimistic outlook. For example, wage growth often provides clues into labor demand, and when the former slows, the latter typically follows.

To explain, the light blue line above tracks the civilian unemployment rate (16+), while the dark blue line above tracks the Y-o-Y percentage change in the number of Americans with no wage growth.

If you analyze the connection, you can see that flat wages are often a precursor to layoffs and a higher unemployment rate. And with the dark blue line on the right side of the chart rising sharply, Powell may be missing the extent of the cooling U.S. labor market.

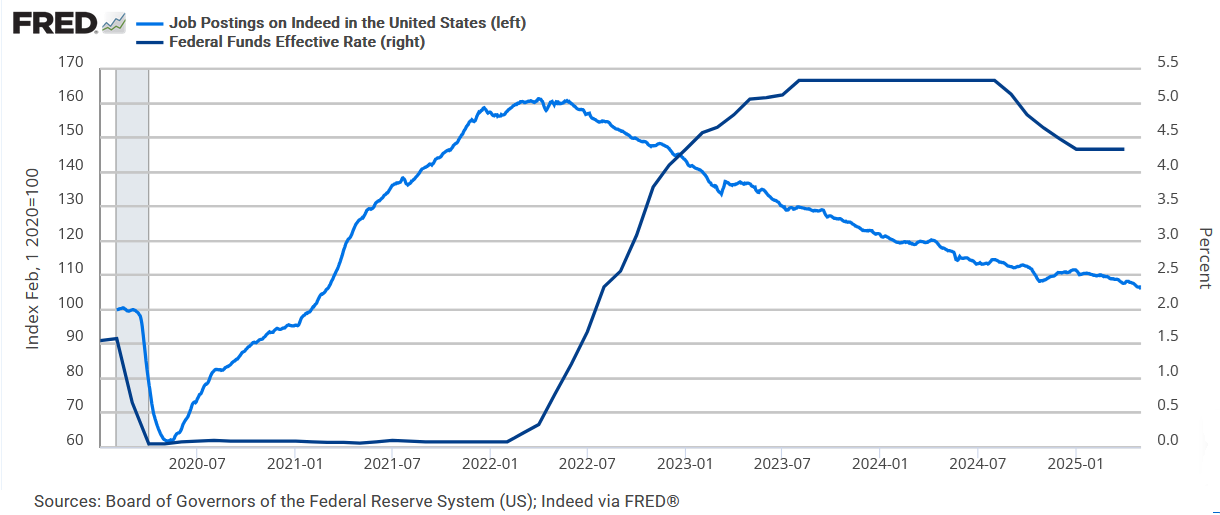

To that point, with U.S. job postings on Indeed hitting a new cycle low, it’s another leading indicator pointing to a labor market slowdown.

To explain, the dark blue line above tracks the U.S. federal funds rate (FFR), while the light blue line above tracks Indeed’s job postings. And while the latter is nearly back to where it was pre-pandemic, the FFR is roughly 3% higher than it was pre-pandemic. As a result, Powell’s focus on inflation could cause short-term interest rates to remain higher for longer than they should.

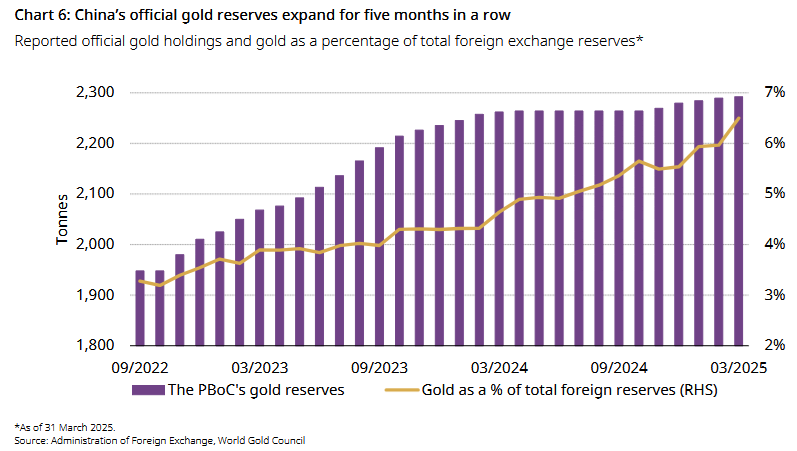

Yet, as tariff and inflation uncertainty handcuff the Fed, gold should remain a primary beneficiary. China’s central bank continues to stockpile gold, and robust demand could foster higher prices for several years. The World Gold Council noted recently:

“The People’s Bank of China (PBoC) has been adding gold to its reserves for five consecutive months: March saw a 2.8t reported addition to China’s official gold holdings and Q1 ended with a net gain of 12.8t.”

Likewise, Goldman Sachs noted that while the PBoC has been on a buying spree, it holds fewer than 8% of its total reserves in gold compared to a developed-market average of ~70%. Moreover, an achievable purchase allocation of 40 tonnes per month over the next three years could push the figure to 20% and create price support for the foreseeable future.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Please seek the guidance of a financial advisor before making any investment decision.

In addition, if credit concerns have increased alongside the economic uncertainty, you’re not alone. New Era Debt Solutions is a top-rated debt settlement company that can help alleviate unsecured claims in as little as 24 to 48 months. Similarly, Family Credit Management is an excellent nonprofit credit counseling agency that provides the education and resources necessary to determine the optimal path to financial well-being.

Remember, speaking with a professional can help you avoid bankruptcy and protect your credit score. To learn more, please consult our list of debt management firms that can help get you back on track.

Alex Demolitor is a Canadian financial writer hailing from Halifax, NS. Alex has a Bachelors Degree from King's College and passed the CFA Exam Level III. He specializes in fundamental analysis of the stock, bond, commodity, and FX markets. He also covers US & Canadian economic indicators.