-v3")

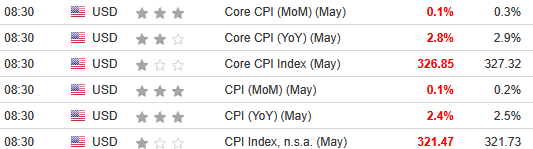

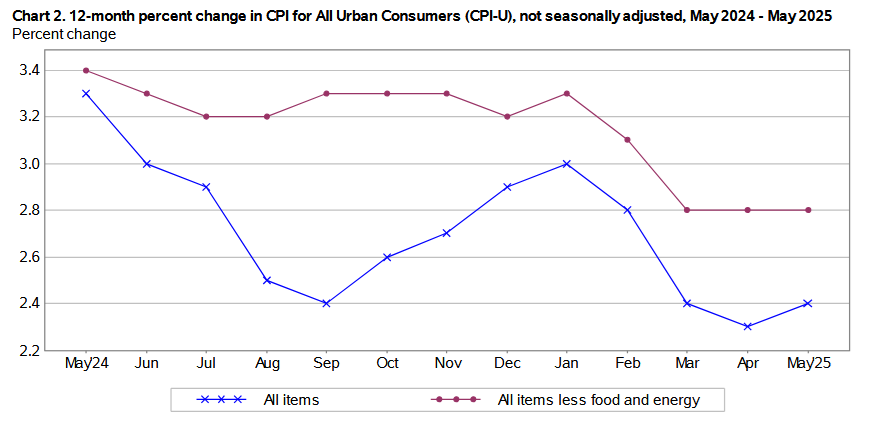

The May 2025 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation rose by 0.1% for the month, down from April’s 0.2% increase. These data were released at 8:30 am EST on Tuesday, June 11, 2025, by the Bureau of Labor Statistics. Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 2.4%, a small rise from the 2.3% Y-o-Y in April.

The downside surprise was more welcome news, as the results missed economists’ consensus estimates. The table below is courtesy of Investing.com. The left column represents May’s figures, while the right column represents forecasters’ expectations. As you can see, tariffs have not been as inflationary as anticipated.

Despite the deceleration, the FOMC has been increasingly concerned about inflation. The May meeting Minutes (released on May 28) stated:

“The substantial upward revision to the inflation forecast in 2025 was judged to leave the risks around the inflation projection balanced in that year. Thereafter, the staff continued to view the risks around the inflation forecast as skewed to the upside, with recent increases in some measures of inflation expectations raising the possibility that inflation would prove to be more persistent than the baseline projection assumed.”

As a result, with the FOMC somewhat offside in its projection, a weaker CPI could surprise market participants in the months ahead.

Gasoline, used cars and trucks, and apparel led May’s downside momentum, while shelter held steady at 0.3% MoM. Core inflation (which excludes the impacts of food and energy), rose by 0.1% in May, declining from the 0.2% rise in April.

Food Prices

The food index jumped by 0.3% MoM in May, after falling by 0.1% in April, and three of the six major grocery store food indexes realized deflation:

- Cereals and bakery products (+1.1%)

- Meats, poultry, fish, and eggs (-0.4%)

- Dairy and related products (-0.1%)

- Fruits and vegetables (+0.3%)

- Nonalcoholic beverages (-0.3%)

- Other food at home (+0.7%)

Maintaining its momentum, the food away from home index rose by 0.3%, as restaurant inflation stayed resilient.

Energy Prices

The energy index dropped by 1.0% in May, a noticeable turn from the 0.7% increase in April. Gasoline prices fell by 2.6%, while natural gas deflated by 1%, and electricity jumped by 0.9%.

Core CPI

The May core CPI rose by 0.1% month-over-month and 2.8% Y-o-Y. Below is an itemized breakdown of the main price fluctuations seen in the core CPI reading:

- Shelter index: (+0.3%) [April: +0.3%]

- Rent index: (+0.2%) [April: +0.2%]

- Owners’ equivalent rent: (+0.3%) [April: +0.4%]

- Motor vehicle insurance: (+0.7%) [April: +0.6%]

- Medical care services: (+0.2%) [April: +0.5%]

- Physician services: (-0.3%) [April: +0.3%]

- Hospital services: (+0.4%) [April: +0.6%]

- Airline fares: (-2.7%) [April: -2.8%]

Seasonally Unadjusted CPI

Before seasonal adjustments, the CPI-U for May 2025 increased by 2.4% Y-o-Y to an index level of 321.465. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

Juggling the Dual Mandate

While inflation has been the primary driver of the FOMC’s caution, it’s important to remember that maximum employment is the second half of the committee’s dual mandate. And with mixed data hitting the wire recently, slower job growth could support rate cuts in the months ahead.

On the positive side, U.S. nonfarm payrolls outperformed expectations on Jun. 6, as the economy added 139,000 new jobs in May, and the unemployment rate held firm at 4.2%. However, the report stated:

“The change in total nonfarm payroll employment for March was revised down by 65,000, from +185,000 to +120,000, and the change for April was revised down by 30,000, from +177,000 to +147,000. With these revisions, employment in March and April combined is 95,000 lower than previously reported.”

As a result, prior months were weaker than they appeared, and another downward revision could occur next month. Moreover, the unemployment rate continues to creep higher off of its 2023 low.

As further evidence, ADP’s private payrolls missed expectations on Jun. 4. The report stated, “The pace of hiring in May reached its lowest level since March 2023.” Furthermore, firms of all sizes reduced their headcounts in May, with the only positive contribution of 51,000 additions coming from firms with 50-249 employees. Conversely, layoffs were driven by small establishments.

Finally, the NFIB released its small business employment report on May 31. The release stated: “A seasonally adjusted net 12 percent of owners plan to create new jobs in the next three months, down 1 point from April. Job creation plans remain in weak territory compared to recent history.”

Furthermore, “Seasonally adjusted, a net 26 percent reported raising compensation, down 7 points from April and the lowest reading since February 2021. This was the greatest monthly decline since April 2020. A net 20 percent (seasonally adjusted) plan to raise compensation in the next three months, up 3 points from April. Clearly, the pressure of labor costs on inflation is easing.”

Thus, with hiring intentions and expected wage increases both heading in negative directions, a weaker U.S. labor market could prompt the Fed to ease monetary policy during the summer months. If so, the dovish recalibration could push gold to another record high. The yellow metal has been one of the best-performing assets in 2025, and ETF flows could be the next bullish catalyst.

To explain, the Deutsche Bank chart above shows how after four negative years, gold ETF flows turned positive in 2025. However, the blue bar furthest to the right is relatively small, and prior periods saw much larger inflows that were sustained for several years.

As such, a repeat of recent history could support a gold bull market that lasts into 2026 and beyond.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Please seek the guidance of a financial advisor before making any investment decision.

In addition, if credit concerns have increased alongside the economic uncertainty, you’re not alone. New Era Debt Solutions is a top-rated debt settlement company that can help alleviate unsecured claims in as little as 24 to 48 months. Similarly, Family Credit Management is an excellent nonprofit credit counseling agency that provides the education and resources necessary to determine the optimal path to financial well-being.

For debt consolidation, Mariner Finance is a reputable personal loan provider that caps its APRs at 35.99%. You can borrow $1,000 to $25,000 (up to $50,000 in select states) and solutions are available for applicants that often don’t qualify at traditional banks.

Remember, speaking with a professional can help you avoid bankruptcy and protect your credit score. To learn more, please consult our list of debt management firms that can help get you back on track.

Alex Demolitor is a Canadian financial writer hailing from Halifax, NS. Alex has a Bachelors Degree from King's College and passed the CFA Exam Level III. He specializes in fundamental analysis of the stock, bond, commodity, and FX markets. He also covers US & Canadian economic indicators.