by Sarah Bauder | May 30, 2019 | Inflation

The general consensus amongst economists is that US inflation is low. This was corroborated by favorable reports by the Department of Labor at the beginning of May. Yet, what trajectory will inflation take in the next half-decade? In this article, 5 experts weigh in on where US inflation is heading in the next 5 years.

The Fed Does Not Expect Inflation To Rise Significantly

“Inflation management is one of the primary roles of the Federal Reserve, so you can look to them for indications of inflation expectations.

The Fed will raise interest rates when it expects inflation to get above the 2% target. By raising interest rates, the Fed makes borrowing less attractive so spending and inflation will fall. Most recently, the Fed has announced that they do not plan to raise interest rates through 2021. This means that they do not expect inflation to rise significantly.

The Fed has also said they expect for unemployment to increase slightly. Again, this indicates low inflation. If less people are employed, then less people will have money to spend and create that upward pressure on prices that causes inflation.”

Brandon Renfro, Professor, Financial Planner

Not Much Organic Inflation

“Speaking as a consumer I do not believe there will be much ‘organic inflation’ in the next five years. A lot of people never fully recovered from the Great Recession. They’re saving a little bit more and do not fully trust the recovery. In addition the baby boomers are all approaching retirement age and will be living on fixed incomes. Healthcare costs are a major concern. According to statistics the economy is booming and yet a lot of people do not feel that is the case in their personal life.

Many people are working in Gig Economy jobs, which are in essence temporary assignments with no health benefits. Examples include driving for Uber, Lyft, Grub Hub, Door Dash, or Amazon delivery. These are not the type of positions, which fueled the economy in past generations.

Inflation is generally caused by consumers pumping a lot of money into the economy and taking on large amounts of debt. The wounds of the Great Recession have yet to heal. People are not automatically assuming they will be better off a year from now. Whenever one feels uncertain about the future they are reluctant to spend lavishly. Any spending they do is usually measured.

Having said that world affairs such as tariff wars and instability in the Middle East could cause inflation without any assistance from consumers. A major rise in oil costs could ripple through the economy causing prices to rise in other sectors of the economy. However, fear has a way of causing people to spend even less which leads to higher unemployment and recession. That would eliminate any inflation bubble.

We’re not likely to see any real inflation until the average working person believes the backbone of the economy is solid with good paying jobs. Right now adults are taking jobs from teenagers such as delivering newspapers, cutting lawns, snow removal, and working in fast food restaurants. This explains why there is a sudden push to make the minimum wage $15. We may not see historically high inflation for another 10 years!”

Kevin Darné, Author, Continuing Education Instructor

Rates Must Creep Back Up To Historic Levels

“Where’s US inflation heading in the next 5 years? – This is impossible to pin down precisely, but I believe that short of a recession, rates must creep back up to historic levels.

In spite of trade wars, government shutdowns and the resultant delay in statistics, the business cycle goes on. That said, corporations have used all the cost-cutting tricks in the world. Now is the time for increasing prices on the ground level as well as at the Fed Open Market Committee.

Complicating matters is that persistently low inflation and low rates hamstring the options that central banks have historically used to address crises. Again, in order to relieve this psychological pressure rates and inflation must creep up.”

Robin Lee Allen, Managing Partner, Esperance PE

A Modest Stagnation Of Growth Rates Can Be Expected

“Considering the latest development in trade and monetary policy, it can be expected that the U.S. inflation rate will remain at modest levels.

Given the uncertain outcome of the ongoing trade war, as well as highly leveraged corporate debt levels, which weigh on the outlook of the world economy, a modest stagnation of growth rates can be expected.

Another point to consider is the Fed’s shift in interest rate expectations. The expected monetary easing is an indication of concerns about low growth and geopolitical tensions.

Since the conundrum about the missing effect of the last quantitative easing programs still prevails, especially the question why full employment did not yield to higher inflation, it remains at least questionable if another round of quantitative easing would lead to higher inflation. The Federal Reserve Bank of St. Louis 5-Year Forward Inflation Expectation Rate (T5YIFR) dropped in the last year from 2.16% to 1.94% and from 2.47% to 1.94% within the last 5 years, even though the Fed deployed massive quantitative easing programs.”

Dr. Stephan Unger, Assistant Professor of Economics, Saint Anselm College

A Recession Within The Next 5 Years

“I predict inflation will stay around 2% for the next 3 years unless a recession hits sooner in which case I think the government will print more money and drive up inflation at a drastic rate. I think there will be a

recession within the next 5 years, so when that hits inflation may be as high as 10% in just one year.”

Stacy Caprio, Financial Blogger, Fiscal Nerd

Given economic indicators, the Fed has projected that there will be no real threat of skyrocketing inflation in the coming years. However, there are numerous variables that can shift which would alter that forecast. Ultimately, only time will provide the definitive answer.

by Sarah Bauder | May 29, 2019 | Inflation

Inflation and deflation can have a significant impact on the performance of a portfolio. It is crucial for investors to understand investment strategies to weather these two economic factors. In this article, experts provide valuable tips and insight into what investors need to know when investing during inflation and deflation.

Avoid Having High Cash Balances

“A top rule for investing during inflation is to avoid having high cash balances. Since money loses it’s purchasing power during such phases, investors should aim at investing into assets which are immune against devaluation, such as physical goods, e.g. gold, silver, other commodities, real estates, etc.

But also an investment into stocks would be good advice since stock prices tend to increase in times of inflation. The reason is that investors flee out of cash and are looking for any types of investment.

In times of deflation, investors should consider to hold cash and to invest in bonds, especially long-term bonds, since interest rates are likely to decline and therefore bond prices.”

Stephan Unger, assistant professor of economics, Saint Anselm College

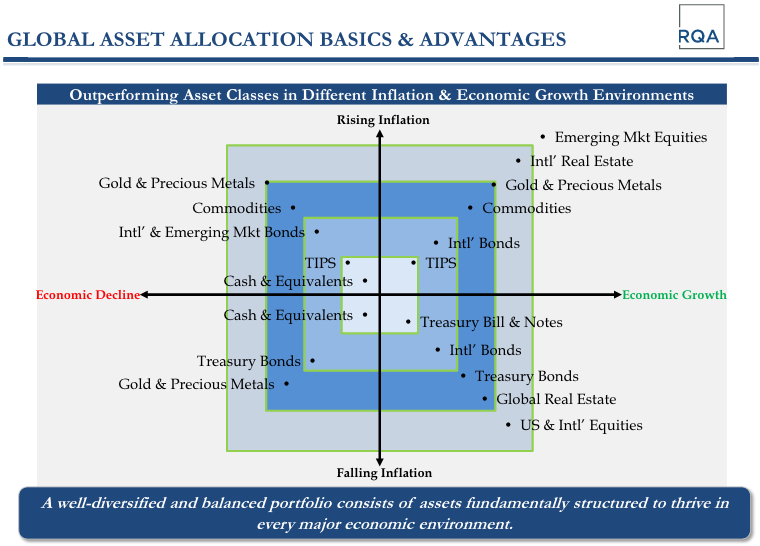

Utilize The Power Of Diversification

(Credit: Richmond Quantitative Advisors)

“The above illustration details global asset classes that tend to outperform during rising inflation and falling inflation. You can further delineate if the economy is in a declining stage or growth stage to provide four full quadrants of global asset performance.

The four quadrants include:

* Inflation with Growth – Inflationary Boom

* Inflation with declining Growth – Inflationary Stagnation

* Deflation with Growth – Deflationary Boom

* Deflation with declining Growth – Deflationary Bust

Based on the illustration, there are ways to position one’s portfolio for certain environments the US encounters. The main focus for investors should be to utilize the only free lunch in investing which is the power of diversification. By diversifying across assets within these four quadrants, one has the highest likelihood of weathering the storm (even if it is not clear where it may occur across the quadrants). Investors need to know those asset classes that have the ability to outperform in each quadrant and then assess their personal asset allocation decisions accordingly.”

Andrew S. Holpe, Managing Member, Richmond Quantitative Advisors

Investors Need To Generate After-Tax Returns

“Most people create investment portfolios to invest their assets to outpace the rate of inflation. The financial markets and governments prefer an environment with low, controllable inflation growth. These conditions allow for expansion while enabling governments to repay current debt with future-value currency.

According to Morningstar, a consensus of financial analysts predict that long-term inflation will grow at 2.48% per annum. Simply put, an investor needs to generate an after-tax return above this inflation rate to stand still and protect the purchasing power of their money.

The most prudent way to ensure success is to build a highly diversified portfolio of stocks, bonds, real estate, commodities, and cash-like liquidity. Limit your single-name stock concentration per issue to not more than 5%. Construct a bond portfolio focusing on credit-quality and that the current yield of your bond portfolio exceeds the effective duration of your portfolio. Effective duration is the sensitivity to a change in interest rates. The combination of these factors allow for growth and provide additional protection during a recession and deflationary environments.

During deflationary environments, consumers defer purchases because they expect lower prices in the future. That reality convinces more people that prices are falling and induces more deferral of purchases, etc. This virulent feedback loop is difficult to change and often requires extraordinary policy measures by central banks. During the credit crisis, the Federal Reserve (FED), Bank of Japan (BOJ) and the European Central Bank (ECB) all implemented radical policy measures to fight deflation. A flight to safety…underweight stocks, overweight cash, foreign exchange (FX), insured CDs, and sovereign bonds are prudent positioning during deflation of asset values. Your cash is worth more in terms of purchasing power as time goes on so there is some inherent return to cash even if there is little or no interest income.”

Paul Bowers, Managing Director, Compass Family Offices

Invest in Commodities And Real Estate

“Typically, assets that an investor would invest during inflationary times would be hard assets such as commodities and real estate. Commodities would include energy such as oil and gas as well as industrial and precious metals (not necessarily gold), You would NOT want to invest in bonds since interest rates rise during inflation and would result in declining bond prices. Many investment advisors recommend gold but I view it as more of a crisis manager rather than an inflationary hedge. In fact, one could argue that gold might be better used as a hedge during deflationary times since deflation tends to occur in a rapidly deteriorating economy when investors flock to protect their assets.

Stocks tend not to do well in deflationary environments. One reason often provided is that revenue and earnings are under duress as prices decline, which would eventually translate into lower stock prices.”

Cliff Caplan, CFP(r), AIF(r), Neponset Valley Financial Partners

Two Sides Of The Same Coin

“Economic factors such as inflation and deflation have a direct bearing to investors’ portfolio. Both are two sides of the same coin. Inflation is the rate at which general prices for goods or services are increasing while deflation is the decline in prices.

Investors need to know how these two factors can affect their investment portfolio. In certain situations, both inflation and deflation can occur at the same time, and this poses a more difficult prospect of protecting your investment. But whether it’s deflation or inflation, there are steps you can take to avert this threat.

If it’s inflation, investors can use the stock market to protect their portfolio. Normally, rising prices are good for equities. International bonds can also provide a solution in this case. Investors can buy international bonds in countries that are not experiencing inflation and hence reduce the impact of razing inflation.

In times of deflation, the most appropriate way to deal with it is to acquire high-quality bonds rather than stocks. Bonds tend to perform well during these times. Government-issued bonds and foreign bonds provide excellent options.”

Edith Muthoni, Chief Editor, Leanbonds.com

Investments Need To Beat The Rate Of Inflation

“It’s important to consider your real rate of return when you expect inflationary markets. Your investments need to beat the rate of inflation in order to make any real progress. If inflation is 8%, you need to make at least 8% on your investments just to break even. If your investments only earn 5% during an 8% inflation period, your real rate of return is roughly -3%. You made money, but not enough to keep up.

There are ways to invest specifically in anticipation of inflation. The simplest is to invest more aggressively in stocks. Since equity investments do better over longer horizons they are often a good inflation hedge. One drawback though is you do need to plan to hold the stocks for a long time. Since stocks tend to be more volatile, you’ll need to plan for a longer investment term. In the short-term, your stock values could fall.

A direct way to invest for inflation is to purchase securities that have explicit inflation terms. The most common of these is the Treasury Inflation Protected Security, or TIPS. These are government bonds whose par value, and therefore interest you receive, adjusts with changes in the consumer price index. You can get these in terms as short as five years.

Another way to invest for inflation is to buy rental real estate. The reason rental real estate is an inflation hedge is because of the rent payments. You can adjust those for inflation when your tenant’s lease expires. If your terms on an annual basis, you would be able to make the adjustment every year.”

Brandon Renfro, Professor, Financial Planner

Regardless of the economic climate, a diversified portfolio is essential. Diversification is crucial when factoring both periods of inflation and deflation. When making investment decisions, take into account these expert tips and always do your due diligence.

by Sarah Bauder | May 21, 2019 | CPI, inflation measure

The Consumer Price Index (CPI) is one of the most oft used techniques for measuring inflation the world over. Specific countries scrutinize different sets of data, but all employ a similar method. In the US, there has been contention surrounding the CPI for many years now. Initially, it was calculated by contrasting a market basket of goods from two periods – effectively operating as a cost of goods index (COGI). Yet, under the auspices of the US Congress, the CPI eventually developed into a cost of living index (COLI). In addition, as time passed methodological changes occurred which often resulted in a lower CPI. In this article, experts weigh in and provide compelling insight into whether the Consumer Price Index is a valid metric for inflation.

A Better Measure Would Be “Chained CPI”

“The Consumer Price Index (CPI) has long served as the foundational inflation measure for economic activity. In fact, it underpins the health of an economy because a stable CPI measure indicates the opportunity for economic prosperity. Absent predictable CPI readings, consumers will not have an accurate signal about price expectations and may change their behavior in detriment to the economy as a whole.

One major limitation to the current CPI measure is its inability to incorporate decisions consumers might actually make when evaluating a fixed basket of goods. For example, when a price increases for one consumer product included in the selection of goods used to measure CPI, many consumers would choose to switch to a substitute. CPI doesn’t account for this reality. Instead, CPI assumes the consumer would simply pay more for the same product. Reality usually shows a different response in the form of choosing a substitute product.

Instead, a better measure which accounts for this substitution effect would be “chained CPI.” This more closely resembles the substitution decisions consumers would make in response to rising prices of certain items as opposed to simply paying more for the same good. This metric will capture the switching dynamic.”

Riley Adams, CPA, Youngandinvested.com

Not An Exact Reflection, But Gives A Good Feel For It

“The CPI isn’t an exact reflection of the inflation rate, but it gives us a good feel for it. For the consumer, it shows them the increase in the price of the most common items that people buy, so if this is what they want to know when it is perfect.

However, for anyone interested in a deeper look at the current inflation rate there are other factors to take into account. For example, the CPI is based on a fixed basket of goods rather than taking into account every single product available. So, it really comes down to the reason for wanting to understand this subject.”

Phillip Konchar, Head Tutor, My Trading Skills

CPI Is Likely The Best Measure

“The CPI is one of a few common economic indicators that attempts to measure the magnitude of price changes (inflation) in the economy. The CPI, as the name indicates focuses on the price changes experienced by consumers. There are better indicators if one is looking at price changes for producers

(Purchaser Price Index – PPI), imports and exports (Import/Export Price Indexes – MXP), or employment costs (Employment Cost Index – ECI).

One drawback of the CPI is the time lag associated with the basket of goods included within the CPI. The basket of goods is determined by surveys the Bureau of Labor Statistics conducts to understand what products consumers are purchasing. There is generally a lag of about three years from the survey to when the basket of goods used in the Index is updated. This can be meaningful as the items consumers are purchasing can change quickly, particularly with rapid change in technology or substituting one good for another.

One other consideration is that the CPI can be volatile as it includes volatile products such as the price of energy (gasoline and natural gas prices can be quite volatile) and food. The Federal Reserve prefers to use a core inflation metric that excludes these volatile goods. The core inflation index the Federal Reserve prefers is the Personal Consumption Expenditures Price Index published by the Bureau of Economic Analysis.

Overall, the CPI is likely the best measure of the change in prices that consumers actually experience within an economy.”

John Linton, Managing Member and Portfolio Manager, Elbert Capital Management

Conclusion

There are both benefits and issues surrounding the use of the CPI as an accurate measure for inflation. For instance, the basket of goods used for the CPI is based upon purchases from a “typical household”, which is not a representative sample of all households. Thus, it is not an exact science, as it were. Likewise, the CPI can overstate inflation if it factors goods and services that consumers are using less of due to price increases. Substitution influences the weighting on the market basket, consequently resulting in a lower CPI. In addition, the basket of goods does not always factor the expenditure of new products that people regularly use. Consumption trends take time to be accounted for.

In essence, we are faced with a decision: accept the official CPI numbers provided by the Bureau of Labor Statistics (BLS), or choose alternate measures of inflation, thereby embracing the argument that official figures are inaccurate. Ultimately, whether or not the Consumer Price Index is a valid metric for inflation remains to be seen.