Andrew

Andrew McCarthy is an expert in all things inflation. He has a Bachelors in Economics and has been working in the finance industry for over two decades.

by Andrew | Apr 20, 2015 | Definitions

Official March inflation data from the BLS was a mixed bag with headline CPI continuing to remain under pressure, but a significant rise in Core CPI ex Food and Energy was enough to trigger knee jerk uncertainty about the outlook for the Fed’s immediate interest rate policy. A weak session across all markets following the release of the data suggests market participants are viewing the recent uptick in prices as a signal for rates to rise quicker than expected.

The Deflationary Camp

On one side, the deflationary environment shows no sign of easing up, with headline CPI coming in weaker than expected – consumer prices rose a modest 0.2% from February versus a consensus call for a 0.3% increase. CPI YoY fell to -0.1%, the third successive monthly decrease. Double digit falls in energy prices YoY continue to keep a lid on consumer prices for the time being with Energy (-18% YoY) and Gasoline in particular (-29% YoY). Food prices fell -0.2% for the first time in six month providing further relief to the consumer.

In a worrying sign for business activity and sentiment going forward, the index for airline fares declined for the fourth time in the last 5 months and there seems to be growing evidence of discounting taking place in the business travel segment across the board.

Core CPI Remains Stubbornly High

On the flip side, Core CPI excluding Food and Energy continues to print at elevated levels, rising to 1.8% YoY versus consensus expectations of 1.7% YoY. Increased Housing (+0.3% MoM, 3% YoY) and Health Care costs (0.4% MoM, 1.9% YoY) were the main contributors. The recent stability in Crude and Energy prices could see Core CPI remain on the high side for the next few months and the market is likely to start paying more attention to energy prices going forward to try and gauge potential sentiment within the Fed.

Wages

Real average hourly earnings for all employees increased 0.1 percent from February to March with 0.3-percent increase in average hourly earnings just shading the 0.2% increase in CPI. The NFP numbers for the past few months are likely to give the Fed further room to pause – NFP has been on the slide every month since December 2014, and with the potential for increased layoffs coming from the oil, gas, and shale sectors the unemployment numbers might show increasing stress in the coming months.

Market Reaction

Equity markets were a sea of red all day Friday, as a perfect storm of higher than expected Core CPI, increased volatility in China and wider Asian markets, and ongoing drama with Greece triggered a bout of selling from investors trying to reduce exposure going into the weekend.

Selected Market Performances

S&P500 -1.13%

DJIA -1.54%

WTI Crude -1.71%

EURUSD +0.43%

Outlook Going Forward

Rising Core CPI will be a concern for markets, but with increased volatility within China and Emerging Asia equity markets, and heightened geopolitical tensions it appears too early to assume any imminent rate hike from the Fed – if anything these pressures are likely to keep the Fed on hold for the time being in order to get more clarity on world events. Consumer prices continue to remain subdued and policy makers are likely to want to see a pick up on this side before jumping into action.

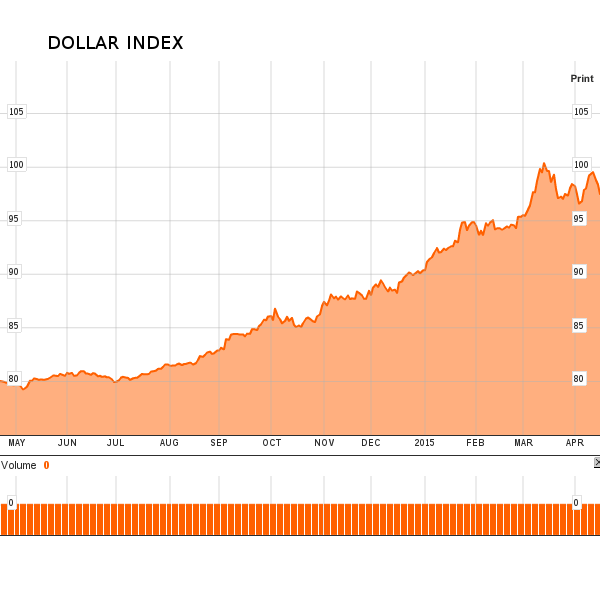

The dollar will continue to act as proxy for rates in the meantime, and we expect the currency to remain well bid against its major competitors for as long as the current standoff from the Fed continues to playout. The Gold market has been steady all month with the yellow metal hovering around the $1200 mark in fairly tight trading bands. With the ZIRP, and increasingly NIRP world in which we live, the Gold market might still have a role to play this year.

by Andrew | Apr 14, 2015 | Definitions

The latest batch of FOMC minutes released earlier this week highlighted some of the ongoing deflation themes we have been exploring in previous posts, and offered some confirmation of our forecast for rates to remain flat for the foreseeable future. Despite the strong conviction amongst sell side analysts a few months ago that rate increases were just around the corner, it seems increasingly likely that such a move will be delayed. Certain members of the FOMC Committee pinpointed the spectre of deflationary forces from overseas as being a potentially disruptive force for market stability in the months ahead. This in part, contributed to a fairly split opinion amongst committee members when it came to the potential for any interest rate increases in the near term.

Deflationary Concerns

Some of the major sticking points included concern about the rapid strengthening of the dollar which has been occurring over the past year. The minutes noted that “ A number of participants cited the further appreciation of the dollar and recent weakness in spending and production data as reasons for their revision.”

Various problems overseas were also cause for concern. “Participants pointed to a number of risks to the international economic outlook, including the slowdown in growth in China, fiscal and financial problems in Greece, and geopolitical tensions.”

“Several participants judged that the economic data and outlook were likely to warrant beginning normalization at the June meeting. However, others anticipated that the effects of energy price declines and the dollar’s appreciation would continue to weigh on inflation in the near term, suggesting that conditions likely would not be appropriate to begin raising rates until later in the year, and a couple of participants suggested that the economic outlook likely would not call for liftoff until 2016.” – March FOMC Minutes

The timing of this “Liftoff”, or “Meltdown”, as it will be known throughout much of the world outside of the United States, appears to be balanced quite evenly amongst policymakers. There is something for everyone in the March statement. The financial community in some quarters will likely draw a huge sigh of relief from the cautionary sentiment, but it’s becoming increasingly clear that either way, whether the Fed raises rates in June, later this year, or never, that something is seriously dysfunctional with our financial markets in their present state.

Monetary Policy trumps fundamentals

The Fed faces an increasingly unenviable task. The interconnected nature of the world’s financial markets make for an increasingly binary, and fraught world when it comes to monetary policy. The Fed, as we have said for sometime, is increasingly global – US monetary policy is the tune the whole world dances to. Emerging Markets find themselves at particular risk to rising rates, but they are just one example of reality and fundamentals being overlooked due to the intoxicating effects of cheap money. The Fed has to digest all of the implications a rise in rates would bestow upon the world – with risk premiums across most asset classes completely out of line with historical norms it seems highly unlikely that overbought financial assets could sustain any repricing of this premium. As a consequence, price distortions are likely to continue throughout the financial landscape – and it seems increasingly clear that there is no pain free decision for the Fed going forward. The Fed has to keep abreast of an ever increasing set of variables – each one increasing in complexity as the layer upon layer of malinvestment with each passing quarter.

Mission Control: GO or NO-GO for Launch

The Fed is starting to bear some resemblance to the NASA mission control centers of yesteryear. In these smoke filled, bustling rooms of engineers and computer scientists monitored a whole wrath of instruments, and flight variables, giving “no” or “no go” signals prior to a potential rocket launch.

The NASA missions of the 1960s were a triumph and inspirational celebration of the technological innovation and engineering capabilities of mankind, an affirmation of human ability and of the role man plays within the Universe – it was heady stuff. The Fed’s upcoming “Liftoff” decision, or lack there of, will be a mute celebration of financial engineering, and of capital triumphing over labor and entrepreneurship in an attempt to salvage the wreckage imposed by reckless investment banks. Quite a damning reflection of just how far we have fallen.

In 1961, President John F. Kennedy announced his ambition for an American to land safely on the moon by the end of the decade. Neil Armstrong descended from the lunar module 8 years later to take the most famous footstep of all time. NASA landed a man on the moon in less time than it has taken for the financial markets to rediscover a sound footing since the economic carnage unleashed in 2008. Such is the sobering scale of the problem facing the Federal Reserve and the world at large.

by Andrew | Apr 6, 2015 | Definitions, Inflation

The accelerating pace of deflation across the world’s major economies is fast becoming one of the most influential forces for financial markets in 2015. We are already starting to see consensus interest rate expectations shift from a widely expected hike in June, to a delayed hike in September, and indeed, some market commentators are viewing the ongoing deflationary trend as a sign that interest rates are likely to remain unchanged for the foreseeable future. The Fed’s interest rate decision is fast becoming the fulcrum upon which entire countries, companies, and individuals find their economic well being balanced upon, highlighting a growing imbalance which exists between the monetary and policy setting classes and everyone else.

What prices are falling? I can’t see them anywhere!

Average Americans can be forgiven for failing to see any material decrease in prices which affect the most important aspects of their daily life – in truth, it has never been more expensive to sustain a middle class lifestyle in America, a lifestyle which once upon a time was the bedrock of the American dream and the envy of the entire industrialized world. Healthcare, education, food, and housing, all prominent components of a comfortable middle class lifestyle are often millstones around the necks of many working Americans at best, and completely unattainable at worst.

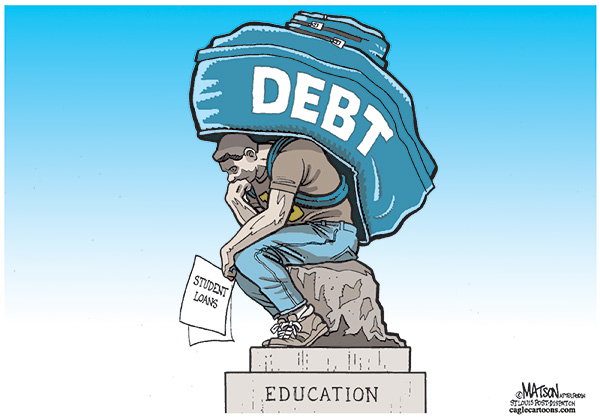

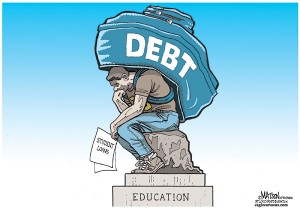

Education – the biggest hurdle in life?

Education has never been as expensive as it is today. Despite the explosion of the world wide web and mass communication technologies throughout the 1990s and 2000s, the information age paradoxically, at least accredited information as it exists via traditional higher education degrees, comes with an extravagant price tag well out of reach for ordinary people. As a consequence, the youth of today are forced into carrying an enormous debt burden, a burden they will be repaying throughout their entire lives. These youth are effectively forced into these decisions at a period in their life when they have the least amount of experience and understanding of how the world at large operates.

As a consequence, the youth of today are forced into carrying an enormous debt burden, a burden they will be repaying throughout their entire lives. These youth are effectively forced into these decisions at a period in their life when they have the least amount of experience and understanding of how the world at large operates.

Shifting employment trends make education decisions even more stressful than they already are. As a consequence we have reached an unprecedented point of personal indebtedness – student loans for higher education are just one face of the prism, when all forms of personal indebtedness are viewed in aggregate, we see ordinary Americans stuck well and truly behind the eight ball with regards to social mobility.

This is a damning reflection of just how securitized the world is becoming through the financial sector and highlights one of the greatest problems we are facing as a society – the accelerating two tiered economic system which exists within the world today. Those with access to a printing press, and those who don’t.

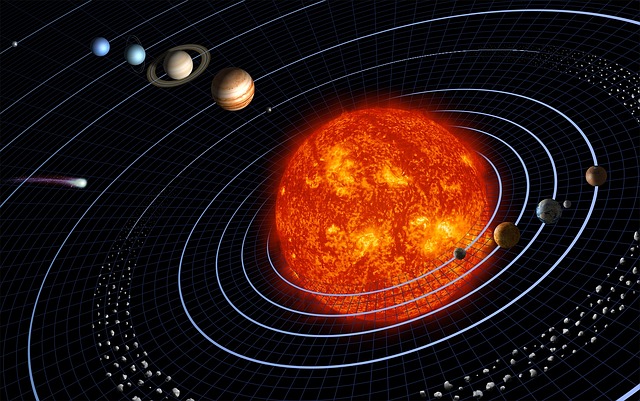

The Economic Solar System: The universe revolves around the Fed

It is becoming increasingly clear that the policies deployed in response to the 2008 financial crisis have enriched the top 1% of Amercians at the expense of the ordinary people of the working and middle class. This has largely occurred through one of the biggest wealth transfers in history– labor and savers have been undermined during this period in order to keep the financial markets fluid. The resulting system is very much like the conventional model of our solar system.  Investment Banks, Corporations, Small Business, and average Joe all orbit the Federal Reserve as part of the wider economy. Investment Banks have a direct relationship with the Fed and occupy the first orbital. As a consequence, they are the first recipients of the money generated from the Fed’s printing press – this places the banks – the very same institutions which brought the world economy to its knees in 2008, with the most advantageous position in the world economy today. Banks are able to effectively choose who wins and loses under this new system. To date, the banks have decided to keep this newly printed capital in their own bank yard – in global fixed income, equity and derivatives markets. This inner most orbital has been revolving at a fevered pace for years now – equity markets and bond prices are at historical levels all over the world – some asset classes such as emerging markets are even showing signs of hyperinflation. Banks in our model would correlate directly to Mercury in the solar system model. Average people and Small Business are languishing somewhere out near Pluto in the freezing abyss of deep space, a mere speck of inconsequential light.

Investment Banks, Corporations, Small Business, and average Joe all orbit the Federal Reserve as part of the wider economy. Investment Banks have a direct relationship with the Fed and occupy the first orbital. As a consequence, they are the first recipients of the money generated from the Fed’s printing press – this places the banks – the very same institutions which brought the world economy to its knees in 2008, with the most advantageous position in the world economy today. Banks are able to effectively choose who wins and loses under this new system. To date, the banks have decided to keep this newly printed capital in their own bank yard – in global fixed income, equity and derivatives markets. This inner most orbital has been revolving at a fevered pace for years now – equity markets and bond prices are at historical levels all over the world – some asset classes such as emerging markets are even showing signs of hyperinflation. Banks in our model would correlate directly to Mercury in the solar system model. Average people and Small Business are languishing somewhere out near Pluto in the freezing abyss of deep space, a mere speck of inconsequential light.

Low Monetary Velocity is Stoking Deflation

Current deflation seems to be a direct consequence of this new economic system. The very low velocity of money, that is the rate at which money is dispersed throughout the entire system, is starting to cause the entire system to implode. Crude oil, commodities, wages, agricultural goods are all exhibiting signs of severe price deflation. As long as the economic imbalances remain within the world, more namely the severe imbalance in power and influence which the financial sector exerts over the global economy – the more likely it will be that official statistics become even more meaningless in describing the economic realities of the modern world.

by Andrew | Mar 27, 2015 | Definitions

The zero interest rate policies being adopted by central banks is causing massive price distortions all over the world – the Fed is now global in scope– its decisions in the coming year will impact the lives of billions and it looks increasingly likely these decisions will be made from the corner which the fed has painted themselves into.

One of the biggest consequences of the Fed’s Quantitative easing program has been a massive injection of capital into emerging markets, resulting in a potentially toxic carry trade of epic proportions. Yield starved investors in the US, Japan and Europe have poured money into high yield sovereign bonds across the world – the yields on many of these bonds tumbled and their corresponding national currencies appreciated significantly during this bull period between 2009–2011.

As domestic yields fell, the banking system in these emerging markets faced a dilemma – the traditional and often conservative investment methods of investing in government bonds and bank time deposits were no longer attractive– in many cases investors were facing negative real rates in as inflation levels remained stubbornly high. Faced with fierce competition from international competitors all scrambling for a piece of the action, incumbent banks were forced into riskier and riskier investments to keep their net interest margins intact. For the man on the street in emerging markets this led to an unprecedented boom in consumer lending – from which a myriad of housing and high end commercial real estate bubbles have emerged.

As domestic yields fell, the banking system in these emerging markets faced a dilemma – the traditional and often conservative investment methods of investing in government bonds and bank time deposits were no longer attractive– in many cases investors were facing negative real rates in as inflation levels remained stubbornly high. Faced with fierce competition from international competitors all scrambling for a piece of the action, incumbent banks were forced into riskier and riskier investments to keep their net interest margins intact. For the man on the street in emerging markets this led to an unprecedented boom in consumer lending – from which a myriad of housing and high end commercial real estate bubbles have emerged.

Increased liquidity within the domestic banking system and negative real rates on traditional deposit investments has also led to unparalleled growth in such countries’ stock markets. 200 – 300% gains in these markets are commonplace since the height of the financial crisis in 2009. An increase in foreign investors in these markets has also brought a new focus on particular performance metrics within the banking sector – loan growth in particular was rewarded heavily by a corresponding increase in bank share prices. As a consequence, consumer and corporate lending within these economies has skyrocketed. Corporates, often with shady corporate governance history, have been granted unrestricted access to financing in both domestic and international markets to yield starved investors – with the proceeds being plowed into trophy commercial real estate projects and commodity related investments.

Halloween Economics: Who’s next at the door?

Emerging market bubbles have been operating well below radar for the time being. The Greek turmoil within the Eurozone and political friction in Russia are taking center stage for financial analysts and commentators.  It looks increasingly likely however, that emerging markets will be the next abomination to show yet another guise of the economic malaise which has been changing disguise since the collapse of Lehman all those years ago.

It looks increasingly likely however, that emerging markets will be the next abomination to show yet another guise of the economic malaise which has been changing disguise since the collapse of Lehman all those years ago.

Expectations for a rise in US interest rates have already had dire repercussions for emerging market currencies – however with consumer borrowing and equity markets at all time highs in these regions – it would appear that the full blown affect of fed rate hikes has not been priced in.

Emerging markets are therefore rightfully desperate for deflation trends to continue in the US – a delay in rate hikes will help buy time – but it seems increasingly likely that time is running out before the pidgeons come home to roost and we are faced with yet another weak point in the global financial system to deal with.

Until the price discovery mechanism imposed by market forces instead of central bank policies is able to work again – our economies will continue to operate in a dangerous state of delusion. The relationships between labor, capital and entrepreneurship are the bedrock of all economies, and as long as the cost of capital is distorted, labor and entrepreneurship will continue to be thwarted.

While speculation is promoted, rewarded, and even favored over traditional capital formation – we will continue to increasing polarization within society and dysfunctional economies. The Fed’s next move rightfully has the market on tenterhooks, and emerging markets above all others will be watching with increasing anxiety.

by Andrew | Mar 19, 2015 | Definitions

US CPI numbers have been declining for several months now – the latest print for January saw CPI fall -0.7% , the fourth consecutive month of deflation. Financial markets across the world are bracing themselves for a sustained period of deflation and digesting the potential policy implications this might have for the Federal Reserve. Deflation is a decrease in the general price level of goods and services within the economy and usually occurs when the level of overall demand is insufficient to meet supply.

The bond market is suggesting a revised timing scenario of the Fed’s next move in rates- from an expectation of a 0.25% increase in June delayed until September. This is a significant change as several vulnerable asset classes such as Emerging Markets, High Yield Credit, and Equities have all been gingerly awaiting a rise in Fed rates for some time. An alteration to the time schedule of any increase in rates will have huge implications for these markets – we are already seeing this occur.

If the mere glimpse of deflation in the official numbers is enough to have such a dramatic effect on market expectations – it is important to establish where the current sources of deflation are coming from and how these influences are likely to evolve going forward.

Deflation is Public Enemy #1 for Central Banks

Deflation has always been a major concern for market analysts and commentators as it points to a structurally weak economy incapable of generating the demand required for sustained growth. Deflationary environments are often characterized by an above average rate of bankruptcies which tend to reverberate throughout the entire economy. Oversupply in a particular industry often leads to extreme discounting – this can be so severe to the point where prices no longer cover costs. Once this level is breached, factories and businesses are forced to shut down, which leads to increased layoffs and unemployment. As incomes drop, overall demand decreases further within the economy until a deflationary spiral begins to draw the economy deeper and deeper into recession.

Periods of sustained deflation are unusual economic events but there are some spectacular historical examples – the Great Depression of the 1930s being the most prominent.

The impact that the Great Depression has had on the psyche of economists is profound.

Keynesian economic theory, the backbone of nearly all current economic policies adopted by central banks across the world, was formed in direct response to the horrifying economic events of the Great Depression. Keynesian theory advocates increased government intervention in the economy by adopting an expanded money supply and increased spending during an economic downturn. Central Banks across the world are currently enforcing these theories through their Quantitative Easing programs and zero interest rate policies. Although these policies have had some effect in boosting the prices of certain financial assets and reducing the official unemployment figures – the lack of official inflation is likely to give the Fed considerable room to keep rates unchanged going forward – and this is most likely a result of the crashing price of Oil.

Canary in the coal mine – Crude Oil

Oil is the life blood of our modern economies. Nearly all aspects of our industry, agriculture, technology, entertainment, and social lives are built in one way or another on the foundation of Oil. The recent rout in Oil prices is flagging severe stress within the global economy – January inflation figures highlighted a 9.7% drop in Energy prices and a 18% drop in gas prices. At first glance declining Oil prices may seem like a good thing – gas and heating bills are reduced leaving consumers with more money to spend on other goods services. In reality, it never tends to work out this way.

The rout in global Oil prices is likely the direct result of massive overcapacity within the global economy – the most probable cause is China, but finding the exact source of this overcapacity is unclear – an analogy would be trying to find the starting point of a particular strand of spaghetti within a giant bowl. The global economy is an interconnected mess. Nevertheless, the knock on effect which decreasing Oil prices are having is considerable. Any business or country heavily reliant on commodities is currently feeling extreme financial duress. We are likely to see increasing levels of bankruptcies begin across the commodity sector within the US and globally. The shale gas industry in the US is at particular risk – this has repercussions for the banking industry and credit markets in general.

As these global factors continue to unravel – CPI within the US is likely to remain subdued. Global deflationary forces could very well end up causing the Fed to postpone its well flagged rise in interest rates – the market is already starting to price this scenario in. Upcoming CPI figures for February, to be released later this month should continue to confirm the deflation trend that we are currently experiencing. If the deflation figures overshoot, then we could start to see some real upheaval in world financial markets going forward.