-v3")

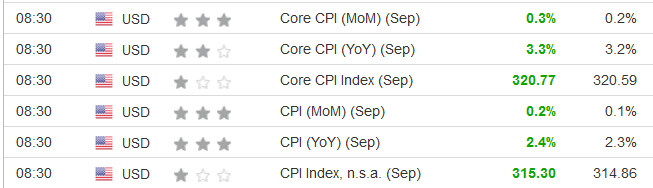

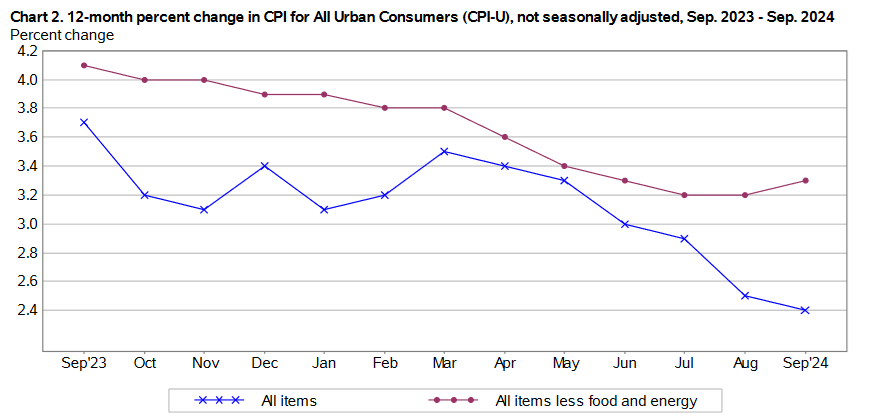

The September 2024 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation increased by 0.2% for the month, matching July and August’s 0.2% rise. These data were released at 8:30 am EST on Thursday, October 10, 2024, by the Bureau of Labor Statistics. Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 2.4%, down from July’s 2.9% and August’s 2.5% prints.

Although the results were relatively mild, all of the CPI metrics outperformed economists’ consensus estimates. The table below is courtesy of Investing.com. The left column represents September’s figures, while the right column represents forecasters’ expectations. As you can see, each data point (marked in green) was stronger than expected.

After FOMC Chairman Jerome Powell said during his annual Jackson Hole Economic Symposium speech that rate cuts were on the horizon, the committee delivered a 50 basis point rate cut on Sep. 18. Powell said during his post-meeting press conference:

“As inflation has declined and the labor market has cooled, the upside risks to inflation have diminished, and the downside risks to employment have increased. We now see the risks to achieving our employment and inflation goals as roughly in balance, and we are attentive to the risks to both sides of our dual mandate.”

He added: “If the economy remains solid and inflation persists, we can dial back policy restraint more slowly. If the labor market were to weaken unexpectedly or inflation were to fall more quickly than anticipated, we are prepared to respond. Policy is well positioned to deal with the risks and uncertainties that we face in pursuing both sides of our dual mandate.”

Thus, while Powell voiced concerns about both sides of the monetary policy equation, today’s inflation print highlights how fits and starts should be expected along the way.

Global markets had mixed responses to the CPI data, as stocks, bonds, precious metals, and the U.S. dollar moved relatively calmly in different directions.

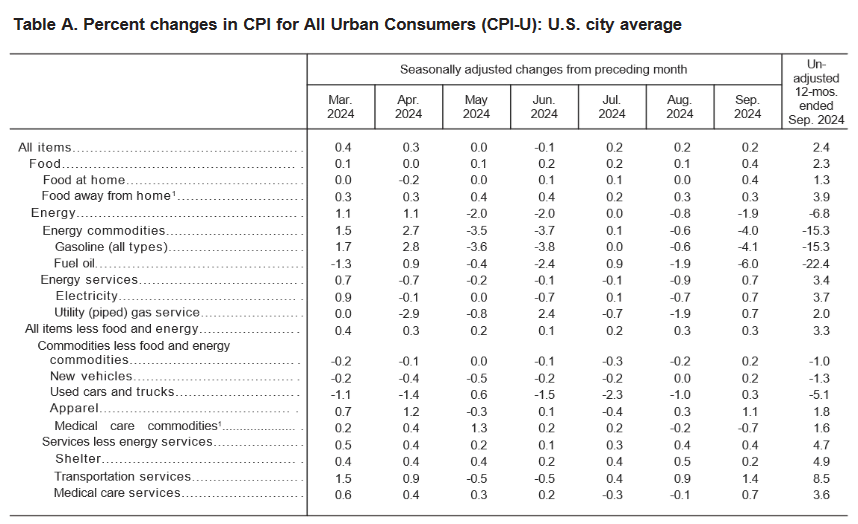

Notable monthly results within September’s headline inflation data showed transportation services prices jumped by 1.4%, apparel by 1.1%, and medical care services by 0.7%. Core inflation (which excludes the impacts of food and energy), rose by 0.3% in September, matching August’s print. However, the shelter index rose by 0.2%, a noticeable decline from the 0.5% reported in August.

Food Prices

The food index increased by 0.4% in September, well above the 0.1% recorded in August. Five of the six major grocery store food indexes showcased inflation, while one was flat.

- Cereals and bakery products (+0.3%)

- Meats, poultry, fish, and eggs (+0.8%)

- Dairy and related products (+0.1%)

- Fruits and vegetables (+0.9%)

- Nonalcoholic beverages (+0.0%)

- Other food at home (+0.2%)

In addition, the food away from home index rose by 0.3% in September, mirroring August’s rise, and highlighting how restaurant prices continue to outpace overall inflation.

Energy Prices

The energy index declined by 1.9% in September, building on the 0.8% drop in August. Gasoline prices plunged by 4.1% (5.1% without seasonal adjustments), while electricity and natural gas prices both rose by 0.7%.

Core CPI September 2024

The September core CPI rose by 0.3% month-over-month and 3.3% Y-o-Y. Below is an itemized breakdown of the main price fluctuations seen in the core CPI reading:

- Shelter index: (+0.2%) [August: +0.5%]

- Rent index: (+0.3%) [August: +0.4%]

- Owners’ equivalent rent: (+0.3%) [August: +0.5%]

- Motor vehicle insurance: (+1.2%) [August: +0.6%]

- Medical care services: (+0.7%) [August: -0.1%]

- Physician services: (+0.9%) [August: +0.0%]

- Hospital services: (NA) [NA]

- Airline fares: (+3.2%) [August: +3.9%]

Seasonally Unadjusted CPI Data for September 2024

Before seasonal adjustments, the CPI-U for September 2024 increased by 2.4% Y-o-Y, rising to an index level of 315.301. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

Was a 50 Basis Point Rate Cut a Mistake?

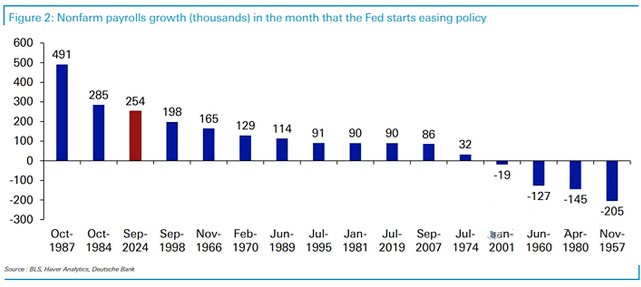

While investors were nervous that the FOMC was ‘behind the curve,’ September’s U.S. nonfarm payrolls report came in more than 100k above expectations.

The chart below from Deutsche Bank highlights how it was the third-largest employment increase in the same month the FOMC cut interest rates since 1957. If you analyze the red bar on the left, you can see the 254k jobs added implies the U.S. economy remains in solid shape. Consequently, with inflation outperforming expectations today, it may give the FOMC cause for pause at its next meeting.

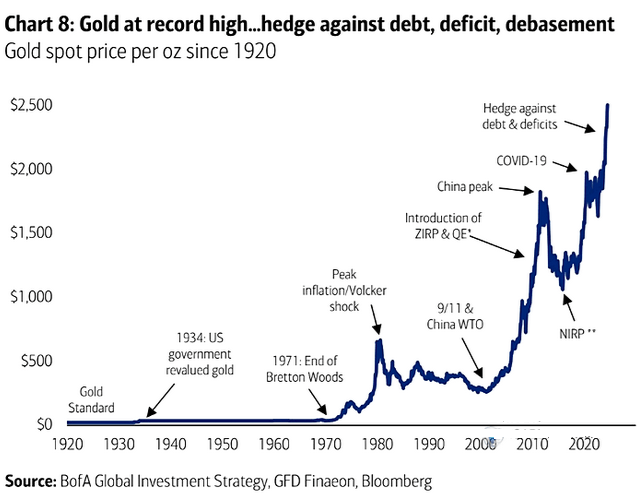

Overall, risk assets have rallied recently, as economic strength is good news for many of the 2024 winners like Bitcoin, Ethereum, gold, silver, and U.S. stocks. Moreover, gold has shined the brightest throughout the year, and Bank of America told clients that rising debt levels and U.S. dollar uncertainty continue to fuel the bull market.

Plus, with gold performing well during periods of calm and crisis, the chart below highlights how it’s often a portfolio ally when global uncertainty strikes.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Remember, seek the guidance of a financial advisor before making any investment decision.

Alex Demolitor is a Canadian financial writer hailing from Halifax, NS. Alex has a Bachelors Degree from King's College and passed the CFA Exam Level III. He specializes in fundamental analysis of the stock, bond, commodity, and FX markets. He also covers US & Canadian economic indicators.