-v3")

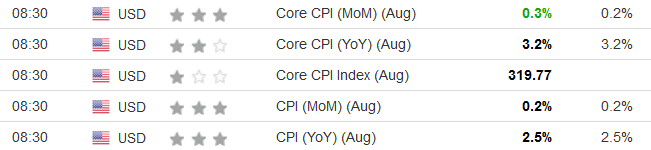

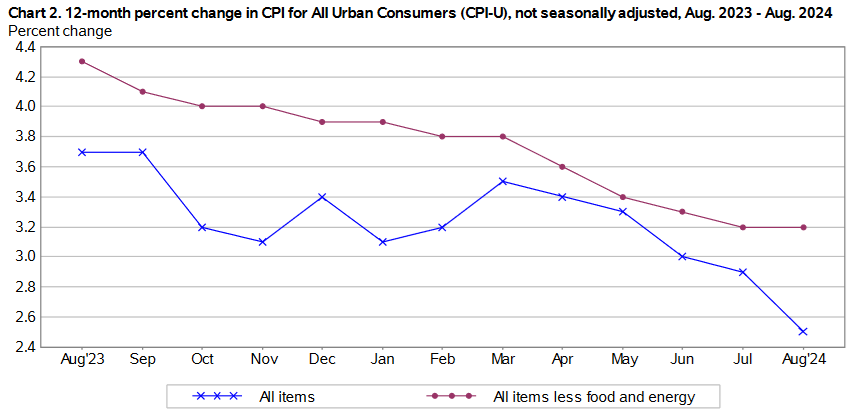

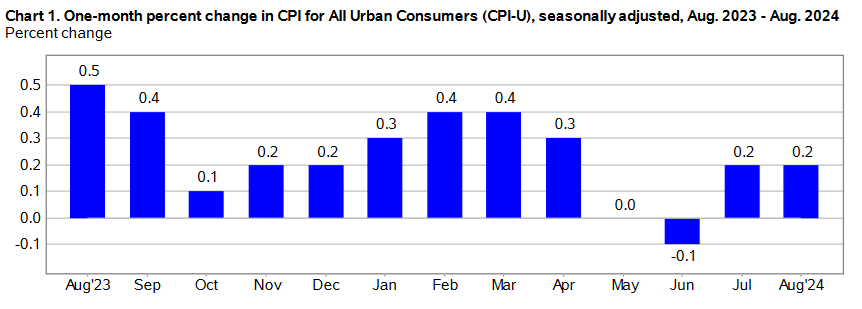

The August 2024 Consumer Price Index of All Urban Consumers (CPI-U) report indicates that inflation increased by 0.2% for the month, matching July’s 0.2% rise. These data were released at 8:30 am EST on Wednesday, September 11, 2024, by the Bureau of Labor Statistics. Before seasonal adjustment, the year-over-year (Y-o-Y) inflation rate in the all-items index grew by 2.5%, down from July’s 2.9% and June’s 3.0% prints. It was the smallest Y-o-Y increase since February 2021.

Adding more merit to the rate-cut argument, most of the CPI metrics matched economists’ consensus estimates. The table below is courtesy of Investing.com. The left column represents August’s figures, while the right column represents forecasters’ expectations. As you can see, the monthly core CPI (marked in green) was stronger than expected, while the others (marked in black) met expectations.

As the financial market’s worst-kept secret, the Federal Open Market Committee (FOMC) is widely expected to cut interest rates on Sep. 18. Chairman Jerome Powell said during his annual Jackson Hole Economic Symposium speech on Aug. 23:

“The time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks.

“We will do everything we can to support a strong labor market as we make further progress toward price stability. With an appropriate dialing back of policy restraint, there is good reason to think that the economy will get back to 2 percent inflation while maintaining a strong labor market. The current level of our policy rate gives us ample room to respond to any risks we may face.”

Thus, while investors debate whether Powell will opt for a 25 or 50 basis point rate cut, the future direction of the U.S. interest rates has become abundantly clear.

Global stock markets largely declined after the CPI release, as volatility has increased in recent weeks. Conversely, Treasury bonds, precious metals, and the U.S. dollar exhibited mixed performances.

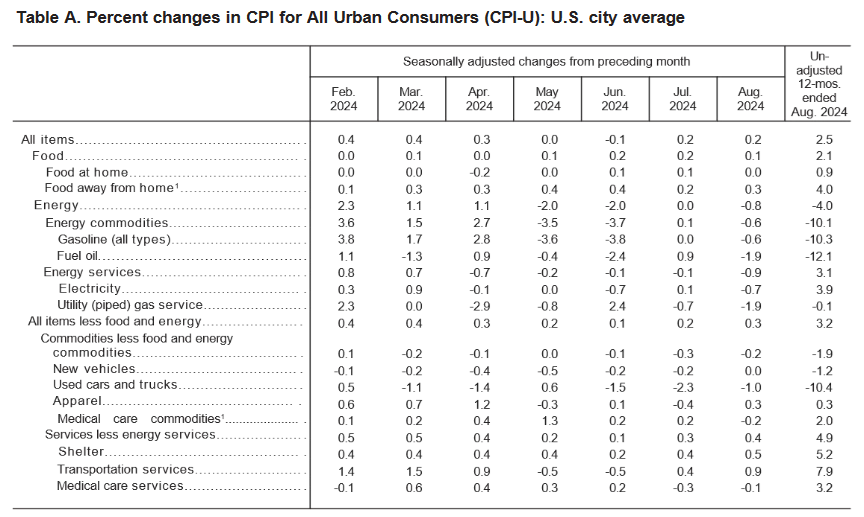

August’s headline inflation deceleration was driven by lower utility gas prices (-1.9%), fuel oil (-1.9%), and used cars and trucks (-1.0%). Core inflation (which excludes the impacts of food and energy), rose by 0.3% in August, up from 0.2% in July, and 0.1% in June. The shelter index rose by 0.5% (up from 0.4% in July) and the BLS described the jump as “the main factor in the all items increase.”

Food Prices

The food index increased by 0.1% in August, a deceleration from June and July’s 0.2% prints. Two of the six major grocery store food indexes showcased inflation, while four realized deflation.

- Cereals and bakery products (-0.1%)

- Meats, poultry, fish, and eggs (+0.8%)

- Dairy and related products (+0.5%)

- Fruits and vegetables (-0.2%)

- Nonalcoholic beverages (-0.7%)

- Other food at home (-0.3%)

In addition, the food away from home index rose by 0.3% in August, ahead of July’s 0.2% rise, meaning restaurants continue to increase their menu prices.

Energy Prices

The energy index declined by 0.8% in August after experiencing a flat performance in July. Electricity and natural gas prices slumped by 0.7% and 1.9%, respectively, while gasoline prices dropped by 0.6% excluding seasonal adjustments.

Core CPI August 2024

The August core CPI rose by 0.3% month-over-month and 3.2% Y-o-Y. Below is an itemized breakdown of the main price fluctuations seen in the core CPI reading:

- Shelter index: (+0.5%) [July: +0.4%]

- Rent index: (+0.4%) [July: +0.5%]

- Owners’ equivalent rent: (+0.5%) [July: +0.4%]

- Motor vehicle insurance: (+0.6%) [July: +1.2%]

- Medical care services: (-0.1%) [July: -0.3%]

- Physician services: (+0.0%) [July: +0.1%]

- Hospital services: (NA) [July: -1.1%]

- Airline fares: (+3.9%) [July: -1.6%]

Seasonally Unadjusted CPI Data for August 2024

Before seasonal adjustments, the CPI-U for August 2024 increased by 2.5% Y-o-Y, rising to an index level of 314.796. Since these figures are unadjusted, they include regular seasonal price fluctuations that can create volatility in the results.

25 or 50?

With investors’ anxiety on full display since August, the debate has shifted from battling inflation to avoiding a recession. Some market participants believe the FOMC is ‘behind the curve,’ meaning that interest rates have been too high for too long and the committee can’t avoid an economic slowdown.

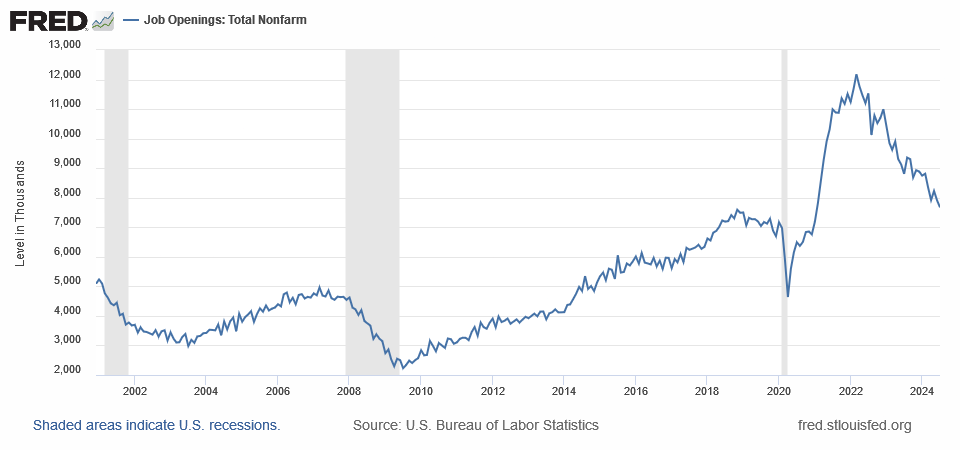

The latest U.S. Job Openings and Labor Turnover Survey (JOLTS) showcases a material decline in employment opportunities, which highlights Powell’s point that “upside risks to inflation have diminished, and the downside risks to employment have increased.”

Therefore, while the debate between a 25 or 50 basis point rate cut should intensify over the next several days, only time will tell if the recent deceleration is a growth scare or something more ominous.

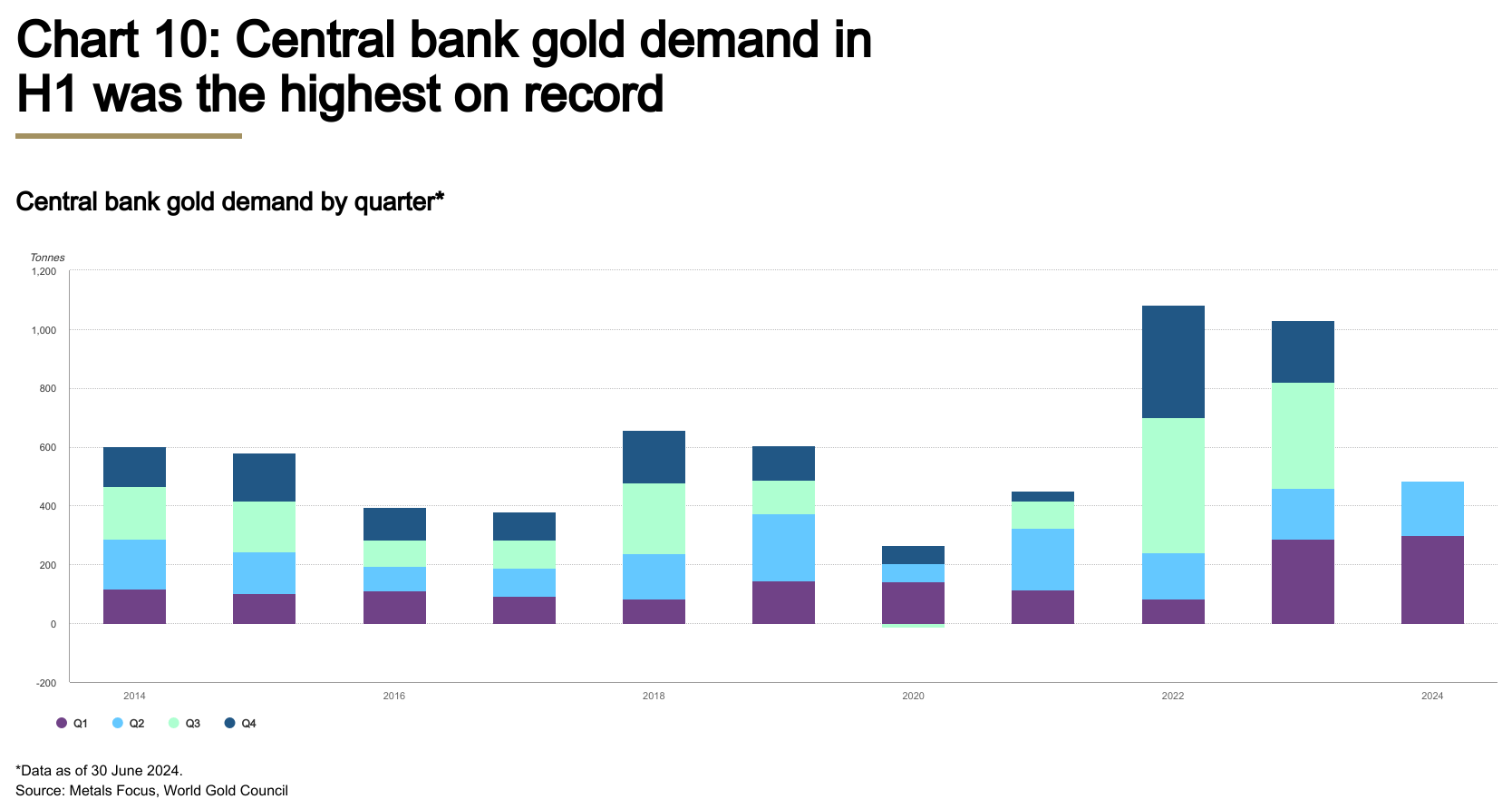

Overall, risk assets have suffered recently, and 2024 winners like Bitcoin, Ethereum, gold, silver, and U.S. stocks have pulled back from their recent highs. However, global central banks have piled into the yellow metal, and the World Gold Council noted on Jul. 30, “Combined with Q1 net purchases, central bank gold demand in H1 totaled 483t, the highest first half year in our data series.” As a result, physical demand for bullion remains robust.

Are you thinking about diversifying into precious metals? Talk to your financial advisor about initiating a gold IRA account today, allowing you to invest in this red-hot asset on a tax-advantaged basis. Additionally, our complimentary CPI inflation calculator remains at your disposal, enabling you to assess inflation’s impact on your finances. Remember, seek the guidance of a financial advisor before making any investment decision.

Alex Demolitor is a Canadian financial writer hailing from Halifax, NS. Alex has a Bachelors Degree from King's College and passed the CFA Exam Level III. He specializes in fundamental analysis of the stock, bond, commodity, and FX markets. He also covers US & Canadian economic indicators.