Should You Be Worried About Inflation Or Deflation? 9 Financial Experts Share Their Views

Inflation is a general increase in the price of goods and services, and a decline in the value of a nation’s currency. Conversely, deflation is a decrease in the price of goods and services, when the rate of inflation falls below 0%. Additionally, the purchasing power of a nation’s currency will increase during deflation. Inflation is measured by the consumer price index (CPI). The CPI measures the changes in the value of a basket of consumer goods and services purchased by households. In this article, financial experts share their views on whether or not investors should be worried about inflation and deflation.

This Inflation Or Deflation Debate Mixes A Lot Of People Up Because The Same Causal Forces Can Potentially Lead To Both Scenarios

“This inflation or deflation debate mixes a lot of people up because the same causal forces (such as high debt levels) can potentially lead to both scenarios depending on the policy response.

When analyzed in isolation, the current macro environment is deflationary. Debt levels as a percentage of GDP are beyond the point of sustainability, and aging demographics lead to slower economic growth and a larger financial burden on younger generations, leading to high default risk over the next decade. Debt defaults involve the destruction of both liabilities and assets; other peoples’ money, which makes this an extremely deflationary prospect.

However, there is virtually no way that the global financial system, as currently structured, would allow a deflationary debt default to occur in countries that control their own currencies. Historically, the policy response to economic environments with this high of a debt load is for governments and central banks to print their way out of it. In a purely fiat system, there’s nothing stopping financial authorities from increasing the money supply to pay all obligations in nominal terms, even if it causes inflation and fails to pay back those obligations in true purchasing power terms.

Therefore, a deflationary or dis-inflationary environment is possible in the intermediate-term, but an inflationary outcome is almost inevitable over the long term due to the policy response to those deflationary or dis-inflationary forces. Rarely in history do fiat monetary systems allow themselves to default nominally.”

Lyn Alden, founder of Lyn Alden Investment Strategy

Looking Forward Over The Next 12 Months We Do Expect A Dip In The Markets And Some Inflation

“In an inflationary environment the value of money decreases, which spurs consumption and investment. Deflation makes it profitable to simply sit on one’s savings while the value of those savings increases without any special effort, disincentivizing consumption and investing.

Looking forward over the next 12 months we do expect a dip in the markets and some inflation. Therefore we are therefore poised and ready for investment opportunities that may crop up over this period.”

Robin Lee Allen, Managing Partner, Esperance Private Equity

The Commonly-Cited CPI Metric Might Not Be The Best For Practical Purposes

“Sensing you will likely receive numerous responses to your prompt declaring whether investors should worry about potential inflation or deflation, I thought I would offer up a viewpoint about why the commonly-cited CPI metric might not be the best for practical purposes.

The Consumer Price Index (CPI) has long served as the foundational inflation measure for economic activity. In fact, it underpins the health of an economy because a stable CPI measure indicates opportunity for economic prosperity. Absent predictable CPI readings, consumers will not have an accurate signal about price expectations and may change their behavior in detriment to the economy as a whole.

One major limitation to the current CPI measure is its inability to incorporate decisions consumers might actually make when evaluating a fixed basket of goods. For example, when a price increases for one consumer product included in the selection of goods used to measure CPI, many consumers would choose to switch to a substitute. CPI doesn’t account for this reality. Instead, CPI assumes the consumer would simply pay more for the same product. Reality usually shows a different response in the form of choosing a substitute product.

Instead, a better measure, which accounts for this substitution effect would be “chained CPI.” This more closely resembles the substitution decisions consumers would make in response to rising prices of certain items as opposed to simply paying more for the same good. This metric will capture the switching dynamic.”

Riley Adams, CPA

A Cost-Averaging Strategy Into A Healthy, Low-Cost, Diversified Stock Portfolio

“For anyone investing in their future over the long term, they know that everything moves through cycles. There are booms, and there are recessions. Sometimes the latter morph into depressions. And inside these, there are deflationary and inflationary times. Piecing it all together, unless you are an econometric expert, is almost impossible.

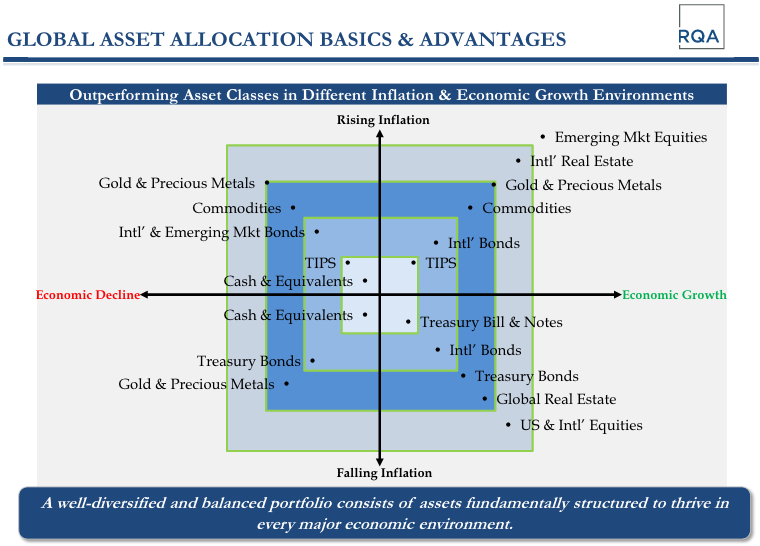

The problem is that events in the economy can move fast between inflationary and deflationary forces. Reaction time can be a severe challenge. For the everyday, hard-working American who puts some earnings aside at the end of every month and religiously injects it into a portfolio, keep it up. By cost averaging over time, you automatically smooth out the many ragged edges and the volatility shocks. Then, my recommendation is to invest it in the S&P 500 (a low-cost fund) that evenly spreads every invested dollar over the public markets’ best stocks. By so doing, you are trusting growth stocks and companies immersed in unearthing and refining commodities like gold and platinum (inflationary hedges). Also, defensive stocks like businesses in consumer goods, and well-known dividend-paying stocks (deflationary hedges). You may want to put a small percentage outside the S&P 500 fund into Treasury Inflation-protected treasuries, investment bonds, and keep some cash on hand (both deflationary protectors).

In short, I recommend a cost-averaging strategy into a healthy, low-cost, diversified stock portfolio as the spearhead of a balanced approach to counteract market ups and downs, rollicked by inflation and deflation from within.”

Gordon Polovin, finance expert, serves on the advisory board for Wealthy Living Today

It’s Definitely Something That People Should Be Concerned About

“Central Banks around the world have a target to keep inflation at roughly around 2% (depending on the country this can be higher or lower). Anything more or less than that can be harmful to the economy. If the inflation is too high, prices of goods and services will rise sharply, and the value of cash or bonds will fall. This has happened numerous times in countries like Germany (after the war), Argentina, Zimbabwe etc. Things can get so bad sometimes that prices double every few hours! This is called hyperinflation and Zimbabwe eventually ended up abolishing its currency and instead using foreign currencies as legal tender! Inflation that is too low or negative (deflation) is equally dangerous. It essentially means that good and services will be cheaper tomorrow than they are today. This incentivizes hoarding of cash. With less demand, economic growth slows down and businesses begin to suffer. Inflation levels also impact export competitiveness compared to other countries, foreign investments and can also impact the value of personal or national debts. It’s definitely something that people should be concerned about which is why Central Banks have set targets in the first place.”

Gaurav Sharma, Founder at BankersByDay

Deflation Can Mean A Drop In Wages Or A Drop In Market Prices

“Deflation can mean a drop in wages or a drop in market prices. Not everyone experiences these drops equally and those who are already secure in a higher paycheck won’t notice either of these factors. However, those who are at the bottom of the business have something to worry about. They are likely to experience a cut in hours or a cut in pay, meaning that while they might notice a drop in market prices, they won’t have the additional income to appreciate it. It’s also important to consider that people are constantly looking for a better deal. In the hopes of finding this deal, people will often stop buying and wait. This can cause a dip in sales and cause trouble with the economy.

Inflation doesn’t necessarily make people secure, however. Inflation means a bump in prices, meaning that the dollar in your pocket is worth less than it was before inflation. Now your paycheck doesn’t go as far and you’re concerned about that. You’ll have less for superfluous spending. You’ll hold onto what little wealth you have and as a result the economy will start to dip.”

Chane Steiner, CEO, Crediful.com

The Outlook Right Now Looks Like One Of Slower Inflation And Because Of That The Risk Of Deflation Is More Of A Concern Now

“Currently the outlook right now looks like one of slower inflation and because of that the risk of deflation is more of a concern now than that of inflation. There are a number of reasons for slower inflation including an aging demographic, technology advancement, inflation expectations, and a stronger dollar. Studies have shown that the aging of demographics has a negative correlation for inflation. In other words, that as a population ages, inflation starts to fall. A good example of this would be Japan, which has battle very low inflation for around the last 25 years. Technology advancement has brought down the price of goods that use new technologies intensively. Historically there has been a correlation of higher productivity with lower inflation. Productivity has been lower recently ,so unless this changes this could be a reason why we start to see inflation rise.

Next, inflation expectations is an important factor in inflation. The higher people think prices are going to go, the more workers will want higher wages, and the higher businesses will believe their costs, and the prices they can charge, will rise. The opposite is true as well, as we are currently seeing inflation expectations from that of the University of Michigan as well as the break-even inflation rate set in Treasury inflation-protected securities. Finally, the stronger dollar leads to lower inflation. This happens because a strong dollar makes foreign imports cheaper which in turn result is cheaper products at U.S. stores, and those lower prices translate to low inflation. So, in order to see the inflation outlook change, we would need to see changes in these factors in order to make that happen.”

Scott Pederson, Financial Advisor, Harmony Wealth Managment LLC

Investor Should Be Worried About Inflation And Deflation

“Yes, the investor should be worried about inflation and deflation. These both are the major economic factors, and investors should keep them in mind before investing money.

Inflation means the increase in the price of products and a decrease in the value of money value. Regarding this basic rule, investors should invest in products whose return or profit margin would be higher than the inflation rate. For example: If the investor is investing $100 and is expected to get $2 profit next year. He must see what would be the inflation rate. If it would be 3%, then the investor is at a loss of $1.

In times of deflation, investors should preserve the capital or invest in the good having the high return potential in the future. Investment in gold is recommended because no matter what, even after a minimal decrease, its prices go high. So, the rule of thumb is either to preserve the capital or invest it in the products with the potential of higher ROI. Business bankruptcy rates increase during this period. So, do not keep your stock shares or corporate bonds in the companies having the risk of bankruptcy. Instead, invest them in potential business or goods to remain on the safe side. “

CJ Xia, VP of Marketing & Sales at Boster Biological Technology

Both Have Negative Consequences

“Generally, as the economy recovers, banks are able to loan out their excess reserves to the public. With the increase in money supply, inflationary pressure is also built, causing the prices of goods and services to rise. This worries ordinary citizens, especially those who live pay check-to-pay check because the affordability of basic goods and services is more difficult.

On the other hand, deflation impacts consumers by way of raising their purchasing power since goods and services have become more affordable. But while this may be good news to the public, the same thing cannot be said for enterprises who are affected by the low prices of their goods and services. Eventually when deflation persists, they will be forced to cut jobs and shut down. The public then experiences decline in incomes and therefore, consumer confidence plunges.”

Doug Keller, Writer, Finance Fox

Both inflation and deflation are economic components that unfortunately cannot be avoided. Keep up with monthly inflation rates and the CPI via the Bureau of Labor Statistics release schedule. In order to offset the market ups and downs during periods of inflation and deflation, a diversification strategy for one’s portfolio is the best bet.