-v3")

Official March inflation data from the BLS was a mixed bag with headline CPI continuing to remain under pressure, but a significant rise in Core CPI ex Food and Energy was enough to trigger knee jerk uncertainty about the outlook for the Fed’s immediate interest rate policy. A weak session across all markets following the release of the data suggests market participants are viewing the recent uptick in prices as a signal for rates to rise quicker than expected.

The Deflationary Camp

On one side, the deflationary environment shows no sign of easing up, with headline CPI coming in weaker than expected – consumer prices rose a modest 0.2% from February versus a consensus call for a 0.3% increase. CPI YoY fell to -0.1%, the third successive monthly decrease. Double digit falls in energy prices YoY continue to keep a lid on consumer prices for the time being with Energy (-18% YoY) and Gasoline in particular (-29% YoY). Food prices fell -0.2% for the first time in six month providing further relief to the consumer.

In a worrying sign for business activity and sentiment going forward, the index for airline fares declined for the fourth time in the last 5 months and there seems to be growing evidence of discounting taking place in the business travel segment across the board.

Core CPI Remains Stubbornly High

On the flip side, Core CPI excluding Food and Energy continues to print at elevated levels, rising to 1.8% YoY versus consensus expectations of 1.7% YoY. Increased Housing (+0.3% MoM, 3% YoY) and Health Care costs (0.4% MoM, 1.9% YoY) were the main contributors. The recent stability in Crude and Energy prices could see Core CPI remain on the high side for the next few months and the market is likely to start paying more attention to energy prices going forward to try and gauge potential sentiment within the Fed.

Wages

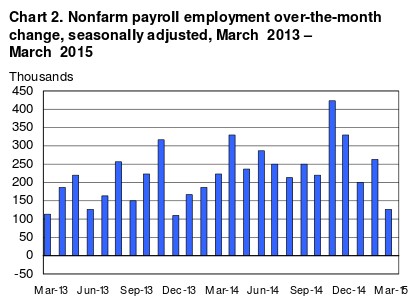

Real average hourly earnings for all employees increased 0.1 percent from February to March with 0.3-percent increase in average hourly earnings just shading the 0.2% increase in CPI. The NFP numbers for the past few months are likely to give the Fed further room to pause – NFP has been on the slide every month since December 2014, and with the potential for increased layoffs coming from the oil, gas, and shale sectors the unemployment numbers might show increasing stress in the coming months.

Market Reaction

Equity markets were a sea of red all day Friday, as a perfect storm of higher than expected Core CPI, increased volatility in China and wider Asian markets, and ongoing drama with Greece triggered a bout of selling from investors trying to reduce exposure going into the weekend.

Selected Market Performances

S&P500 -1.13%

DJIA -1.54%

WTI Crude -1.71%

EURUSD +0.43%

Outlook Going Forward

Rising Core CPI will be a concern for markets, but with increased volatility within China and Emerging Asia equity markets, and heightened geopolitical tensions it appears too early to assume any imminent rate hike from the Fed – if anything these pressures are likely to keep the Fed on hold for the time being in order to get more clarity on world events. Consumer prices continue to remain subdued and policy makers are likely to want to see a pick up on this side before jumping into action.

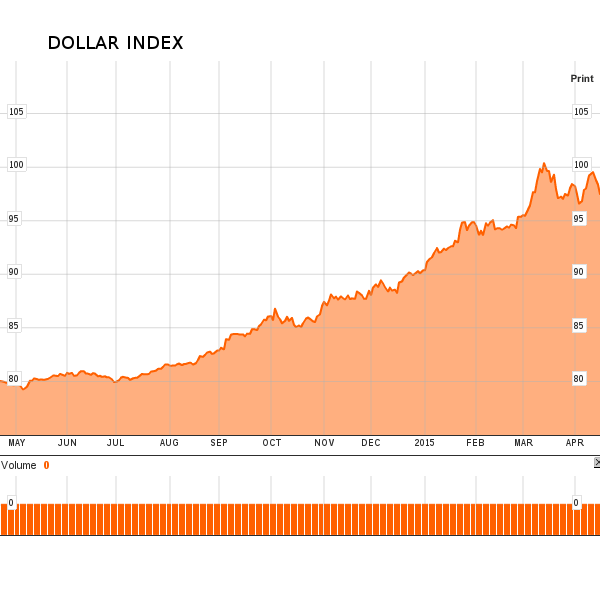

The dollar will continue to act as proxy for rates in the meantime, and we expect the currency to remain well bid against its major competitors for as long as the current standoff from the Fed continues to playout. The Gold market has been steady all month with the yellow metal hovering around the $1200 mark in fairly tight trading bands. With the ZIRP, and increasingly NIRP world in which we live, the Gold market might still have a role to play this year.

Andrew McCarthy is an expert in all things inflation. He has a Bachelors in Economics and has been working in the finance industry for over two decades.