Amine Rahal

Amine is an entrepreneur, investor and financial writer that covers the US economy, inflation, alternative investments, cryptocurrencies and more. He has been involved in the space for over a decade.

by Amine Rahal | Apr 10, 2026 | Debt Relief

When readers ask me, “Does bankruptcy clear tax debt?”, my honest answer is: sometimes, yes, but only in specific situations. I’ve been writing about debt relief, tax debt, settlement, consolidation, and bankruptcy-related topics for a long time, and one mistake I see over and over is people assuming all IRS debt gets wiped out the same way credit card debt might. It’s not always the case. Tax debt follows its own rules, and the timing matters a lot.

Not sure whether bankruptcy is the best path for your tax debt?

Take our quick debt quiz first. It’s one of the fastest ways to narrow down which direction may make the most sense before you spend hours researching the wrong solution.

Take the Debt Relief Quiz

In general, bankruptcy can erase some older income tax debt, but it usually does not wipe out every kind of tax bill. If the debt is too recent, tied to payroll taxes, connected to fraud, or based on late or unfiled returns, the odds get much worse. The IRS bankruptcy guidance, IRS Publication 908, and the bankruptcy priority rules under 11 U.S. Code § 507 all point in the same direction: some tax debt can be discharged, but only if the facts line up.

My quick answer

If you want the short version, here it is:

- Yes, bankruptcy may clear some tax debt

- No, it does not automatically clear all tax debt

- Older income tax debt has the best chance

- Recent tax debt, payroll tax debt, and fraudulent tax debt usually survive

I’ve seen people wait too long to get help because they assumed “nothing can be done” with IRS debt. I’ve also seen people rush toward bankruptcy thinking it would magically clean everything up, only to learn later that the tax debt they cared most about would still be there. That is why I think this is one of the most important debt topics to understand properly before you file anything.

When bankruptcy may clear tax debt

In the U.S., bankruptcy is usually most helpful for older income tax debt. A lot of professionals refer to this informally as the 3-2-240 rule. It is a shortcut way of thinking about whether a tax debt might be dischargeable.

| Rule |

What it usually means |

Why it matters |

| 3-year rule |

The tax return due date was at least 3 years before the bankruptcy filing |

Recent tax debt usually gets priority treatment and is harder to discharge |

| 2-year rule |

You filed the tax return at least 2 years before filing bankruptcy |

Late-filed returns can create major problems |

| 240-day rule |

The tax was assessed at least 240 days before the filing date |

A recent assessment can prevent discharge |

Even if those timing rules look good, the debt still generally needs to be income tax debt, not payroll tax debt or a fraud-related obligation. On top of that, things can get more complicated if you had an offer in compromise, a prior bankruptcy, or other events that can affect the clock.

Tax debts that usually do not get wiped out

This is where I think readers need to be especially careful. Bankruptcy is not a universal eraser for every tax problem. It usually does not clear:

- Recent income tax debt

- Payroll tax debt and trust fund taxes

- Tax debt linked to fraudulent returns

- Tax debt tied to willful tax evasion

- Some debt from late or unfiled returns

- Post-petition tax liabilities

If your debt is mostly credit cards, personal loans, or collections, you may also want to compare this question against our broader guide to debt relief options in America. A lot of people assume “tax debt problem” and “overall debt problem” are the same thing, but they often are not.

Chapter 7 vs. Chapter 13 for tax debt

One thing I’ve noticed over the years is that people talk about “bankruptcy” as if it were one single strategy. It isn’t. The chapter matters.

Chapter 7

Chapter 7 bankruptcy is the form most people think of when they imagine wiping out debt and getting a fresh start. For tax debt, Chapter 7 can sometimes discharge older qualifying income taxes. But it is not automatic, and not every filer qualifies for Chapter 7 in the first place.

If someone has old income tax debt that checks the right boxes, Chapter 7 may be the more direct route. But if the debt is newer, partially priority debt, or part of a larger cash-flow problem, Chapter 13 may be more realistic.

Chapter 13

Chapter 13 works more like a court-supervised repayment plan. In my view, it can be more useful for people who need time and protection rather than a full wipeout. Some tax debt may still be paid through the plan, while some older qualifying debt may eventually be discharged.

That is one reason I often tell readers not to focus only on “Can I erase this?” Sometimes the better question is, “Can I stop the pressure, stay protected, and create a payment structure I can actually survive?”

Does bankruptcy stop IRS collections?

Usually, filing bankruptcy triggers an automatic stay, which can temporarily stop many collection actions. That can include collection pressure from the IRS. But this does not mean the tax debt is permanently gone. It just means the collection activity may pause while the bankruptcy case moves forward.

If your main goal is breathing room, that pause can be meaningful. If your main goal is full elimination of the tax balance, then you need to look much more closely at the exact age and type of the tax debt.

Before you jump into bankruptcy, compare your options

If you are also dealing with unsecured debt like credit cards, medical bills, or personal loans, take our quiz first. In some cases, bankruptcy is the right move. In other cases, a different route may be more practical.

Compare Your Debt Relief Options

What about state tax debt?

State tax debt can also be affected by bankruptcy, but the exact treatment can vary, and state collection practices can be different. I would be very careful about assuming the IRS rules tell the full story for state income tax departments. The broad framework may be similar, but local details matter.

If your tax problem is more specialized and you are trying to understand tax-resolution-style help instead of consumer debt relief, you may also want to read our reviews of Tax Relief Advocates and Five Star Tax Resolution. They are not substitutes for legal advice, but they can help you understand how the tax relief side of the market works.

A simple example

Let’s say someone owes federal income taxes for a return that was due more than 3 years ago. They filed the return more than 2 years ago. The IRS assessed the tax more than 240 days ago. There was no fraud, and no willful evasion.

That person may have a path to discharge that debt in bankruptcy.

Now let’s change one detail. Maybe they filed the return late. Maybe the tax was assessed recently. Maybe the debt is for payroll taxes. Maybe the tax year is too recent. Suddenly, the answer can flip from “possibly dischargeable” to “probably not.”

That is why I never like ultra-simplified headlines on this topic. They may get clicks, but they can mislead people badly.

When I think bankruptcy is worth discussing seriously

In my opinion, bankruptcy becomes much more worth discussing when some or all of the following are true:

- You cannot realistically repay the debt in a reasonable timeframe

- The tax debt is old enough that discharge may be possible

- You are also carrying large unsecured debts on top of the tax balance

- Collections are becoming aggressive

- You need court protection and a real reset, not just another temporary arrangement

On the other hand, if the tax debt is recent and your income is stable, bankruptcy may not be the first place I would look. In that case, you may want to compare other options too, including our guide to the best debt settlement companies and our review of debt consolidation lawyers and attorneys, especially if you are trying to weigh legal help against non-legal debt relief programs.

My bottom line

So, does bankruptcy clear tax debt?

Yes, sometimes. But usually only certain older income tax debts that meet strict timing and filing rules. It is much less likely to wipe out recent tax debt, payroll taxes, or tax debt linked to fraud, evasion, or filing issues.

If you are overwhelmed and not sure where your case falls, I honestly think the smartest first step is not guessing. Map out the type of debt, the tax years involved, when the returns were filed, and whether the debt is really tax debt only or part of a bigger consumer debt problem. Once you do that, the right next step gets much easier to see.

Still unsure what to do next?

Use our debt quiz to compare bankruptcy, settlement, consolidation, and other common paths based on your situation.

Start the Debt Quiz

Frequently Asked Questions

Can Chapter 7 wipe out IRS tax debt?

Sometimes. Chapter 7 may discharge certain older income tax debts, but not every IRS debt qualifies. Timing, filing history, and the type of tax all matter.

Does bankruptcy clear payroll tax debt?

Usually no. Payroll taxes and trust fund taxes are generally much harder, and often impossible, to discharge in bankruptcy.

What is the 3-2-240 rule for tax debt in bankruptcy?

It is a shorthand way to evaluate whether some older income tax debt may be dischargeable. Broadly, the return due date usually needs to be at least 3 years old, the return needs to have been filed at least 2 years before bankruptcy, and the tax generally must have been assessed at least 240 days before filing.

If I filed my tax return late, can bankruptcy still clear the debt?

Maybe, but late filing can create serious problems. In some cases, a late-filed return can prevent discharge entirely. This is one of the biggest reasons I think people should review the timeline carefully before filing.

Does bankruptcy stop the IRS from collecting right away?

It often triggers an automatic stay that pauses many collection actions, at least temporarily. But that does not mean the tax debt disappears forever. The question of discharge is separate.

Is tax debt forgiven after bankruptcy taxable?

In general, debt canceled in bankruptcy is not treated as taxable income the way ordinary canceled debt can be. That said, tax consequences can still be technical, so it is smart to review your full situation with a qualified professional.

Should I file bankruptcy just because I owe the IRS?

Not automatically. I would first look at the age and type of the tax debt, whether you are current on filing, what other debts you have, and whether bankruptcy is solving the actual problem or just part of it. For many people, the right answer only becomes clear after comparing a few legitimate paths side by side.

by Amine Rahal | Mar 23, 2026 | Debt Relief

TurboDebt (sometimes written as Turbo Debt) is a U.S. debt relief brand that helps consumers explore options for tackling unsecured debt (like credit cards, personal loans, medical bills, and collections). The key thing to understand up front is that TurboDebt often acts as a connector that matches you with a debt relief program that fits your situation, rather than always being the company that negotiates directly with your creditors.

TurboDebt (sometimes written as Turbo Debt) is a U.S. debt relief brand that helps consumers explore options for tackling unsecured debt (like credit cards, personal loans, medical bills, and collections). The key thing to understand up front is that TurboDebt often acts as a connector that matches you with a debt relief program that fits your situation, rather than always being the company that negotiates directly with your creditors.

PS: Want a fast, personalized starting point before you call anyone? Take our quick quiz here: Debt Relief Quiz (settlement vs consolidation vs bankruptcy).

Are you sure TurboDebt is right for you?

Debt settlement has its downsides! Don’t jump in without comparing different options. Take our quick Debt Relief Quiz to get a better sense of whether debt settlement, consolidation, counselling or bankruptcy may be the smarter direction for your situation.

Why start with the quiz

- Helps narrow down your best-fit option

- Useful if you are torn between multiple debt solutions

- Fast, simple, and more personalized than guessing

Quick reminder

- Every debt situation is different

- The right option depends on your budget, goals, and urgency

- Use the quiz as a smart starting point before committing

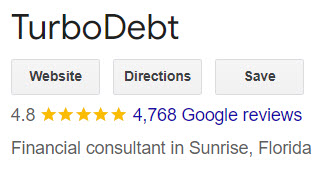

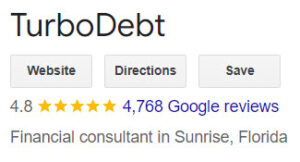

TurboDebt company snapshot (updated for 2026)

- Company: TurboDebt, LLC

- Website: TurboDebt.com

- Headquarters (published on TurboDebt site): 1643 NW 136th Ave, Building H, Sunrise, FL 33323

- Email (published on TurboDebt site): contact@turbodebt.com

- Availability: TurboDebt states it does not offer services in CT, MN, OR, VT, WV, and WI. Always confirm availability from their “Areas We Serve” page before you spend time on an application.

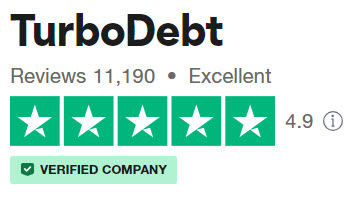

Legitimacy, ratings & reviews (2026 update)

Below is a current snapshot of third-party ratings. These numbers can change over time, so consider them a “temperature check,” not a guarantee of your experience.

TurboDebt

- BBB: A+ rating; customer reviews about ★ 4.87/5 (1,300+ reviews)

- Trustpilot: ★ 4.9/5 (14,000+ reviews)

What TurboDebt actually does (and the question you should ask)

TurboDebt describes itself as a service that connects clients to debt relief programs. In practice, that can mean your case may be handled by a partner program (example partners listed publicly include National Debt Relief and others). That isn’t automatically “bad,” but it changes what you should ask on your first call:

- Who will be the actual program provider negotiating with my creditors?

- What is the total cost (program fees + any dedicated account fees), and when do those costs get charged?

- Will I be asked to stop paying creditors during the program, and what happens if a creditor sues?

- How will you communicate settlement offers, and do I have to approve each settlement?

How debt settlement usually works (plain English)

- Free consultation: you share your debts, budget, and hardship.

- Program fit: if settlement is recommended, you’ll typically open a dedicated account to build funds for offers.

- Negotiations: once enough funds accumulate, settlements are negotiated one debt at a time.

- Fees: reputable providers generally cannot charge “advance fees” before results (make sure you understand fee timing).

- Finish line: the goal is to resolve each enrolled debt and close the program.

If you’re new to this, two excellent government resources to read first are the FTC’s overview of getting out of debt and the CFPB’s explanation of debt relief programs. Also be aware that canceled debt can sometimes trigger tax forms (like a 1099-C), depending on your situation.

TurboDebt Pros 👍

- Massive review footprint: TurboDebt has a very large volume of consumer reviews across major platforms, which is useful for due diligence.

- Clear “shopping” entry point: If you’re not sure which option fits (settlement vs counseling vs consolidation), TurboDebt can be a starting conversation.

- Availability in most states: While not nationwide, it is available in many U.S. states (confirm via their service area page).

TurboDebt Cons 👎

- Potential “middle layer”: Because TurboDebt can act as a connector, you must confirm who the actual program provider is and what their policies are.

- Costs can be significant: Debt settlement fees are often a percentage of enrolled debt, and you may also pay account fees depending on the setup.

- Credit impact risk: Many settlement programs involve missed payments, which can hurt credit and increase collection pressure before resolution.

Not sure whether settlement, consolidation, or bankruptcy makes more sense?

Before you commit to any company or program, take our quick quiz. It can help you figure out which debt relief path may fit your situation best.

Take the debt relief quiz

What types of debt can these programs usually help with?

Most debt settlement programs focus on unsecured debts, for example:

- Credit card balances

- Personal loans

- Medical bills

- Collections

- Some private unsecured lines of credit

They typically do not “settle” secured debts in the usual way (like mortgages or auto loans) because those are tied to collateral. Student loans and tax debts have their own rules and may require different specialists.

Who TurboDebt might be best for (and who should look elsewhere)

- Better fit: You want to explore options, you have meaningful unsecured debt, and you can commit to a structured payoff plan.

- Probably not a fit: Your debt is mostly secured (mortgage/auto), you’re current on everything and just want a lower interest rate, or you need legal protection quickly (in that case, speaking with a bankruptcy attorney may be smarter).

Other reputable options to compare

Even if you like what you hear from TurboDebt, I would still compare a few other providers before making any decision. Debt relief is not one-size-fits-all. Some companies are better for straightforward unsecured debt, some are stronger for tax debt, and some may be a better fit if you want a more legal-heavy approach.

Here are several alternatives you can review on our site:

- CuraDebt review – a well-known name that can be worth a look if you want to compare a more established debt relief brand.

- Oak View Law Group review – a useful option to compare if you prefer a law-firm-style approach or want help with more complex debt situations.

- JG Wentworth Debt Relief review – worth reviewing if you want to compare another major brand with broad consumer awareness.

- National Debt Relief review – one of the biggest names in the space, and a smart benchmark when comparing fees, process, and reputation.

- Freedom Debt Relief review – another large provider that is useful to compare if you want to see how a major national company stacks up.

- Pacific Debt Relief review – a good one to look at if your focus is mainly unsecured debt like credit cards, loans, collections, or medical bills.

- Accredited Debt Relief review – worth comparing if you want to look at a provider that may offer both settlement and consolidation-style options through partners.

- CreditAssociates review – another option to compare if you want a broader sense of how different programs structure their process and fees.

If you want a broader shortlist instead of reviewing companies one by one, here is our full rankings page: Best debt settlement companies ranked by ratings & reviews.

And if you are still not sure whether debt settlement is even the right route for you, I would take our Debt Relief Quiz before speaking with any company. It can help you think through whether settlement, consolidation, or even bankruptcy may be the better fit for your situation.

Bottom line (Our conclusion for 2026)

TurboDebt appears legitimate and has strong public ratings. The main “watch-out” is clarity: confirm who will actually manage your program, get the total fee schedule in writing, and make sure you’re comfortable with the timeline and credit impact.

Ready to see which debt relief option may fit you best?

Take our quick debt relief quiz to compare paths like settlement, consolidation, and bankruptcy before you decide what to do next.

Frequently asked questions

Will debt settlement hurt my credit?

It can. Many settlement programs involve missed payments before debts are resolved, which can damage credit scores and increase collection activity. If protecting credit is your top priority, ask about alternatives like a nonprofit debt management plan (DMP) or consolidation.

Can creditors sue me while I’m in a program?

Yes, it’s possible. Not every creditor agrees to settle, and some may pursue collections or lawsuits depending on the balance, timeline, and creditor policies. Ask how your provider handles lawsuits and whether they offer any support or referrals.

How long does debt settlement usually take?

It depends on how much you owe and how much you can set aside each month. Many programs are marketed in multi-year timeframes. The realistic way to judge it is simple: how fast you can build funds for settlement offers.

Are there tax consequences if a debt is forgiven?

Sometimes. If a creditor forgives part of your debt, you may receive a tax form and the forgiven amount may be treated as income, depending on your situation. If you’re close to enrolling, consider checking with a tax pro so you’re not surprised later.

What fees should I expect?

Ask for a complete fee schedule in writing. The big variables are (1) the program fee (often a percentage of enrolled debt), (2) whether the fee is based on enrolled debt or settled debt, and (3) whether there are monthly dedicated-account fees.

What questions should I ask on the first call?

Ask who the actual program provider is, whether you’ll be advised to stop paying creditors, the total cost including any account fees, whether you approve each settlement, and what happens if a creditor refuses to negotiate.

Is a nonprofit debt management plan (DMP) safer?

A DMP can be a good option if your main issue is high interest rates and you can afford to repay the principal over time. It’s not debt settlement, but it may reduce interest and create one structured payment. It’s worth comparing before you commit to settlement.

What if I’m considering bankruptcy?

Bankruptcy can offer stronger legal protections and may be the right move in some situations. If you’re behind, facing lawsuits, or simply can’t make progress, it can be worth speaking with a bankruptcy attorney for an initial consult.

by Amine Rahal | Mar 3, 2026 | Debt Relief

Overwhelmed with debt? If you’re trying to figure out whether you need a debt consolidation lawyer, a debt settlement company, a credit counselor, or bankruptcy support, this guide will help you make the call without wasting weeks (or money) going down the wrong path.

Quick reality check: “debt consolidation lawyer” is a popular search term, but most attorneys don’t literally “consolidate” debt the way a bank loan does. What they can do is help you negotiate legally, respond to lawsuits, stop garnishments, and choose the right legal strategy when the stakes are high.

Not being sued? Start here first (often cheaper than hiring a lawyer)

If your situation is mainly unsecured debt (credit cards, personal loans, medical bills) and you’re not dealing with a court case, many people get results faster by starting with a settlement-only provider. Our top pick is New Era Debt Solutions because they’re straightforward about the process and fees.

Disclosure: If you click and enroll, we may earn compensation at no extra cost to you.

💼 What is a debt consolidation lawyer?

A debt consolidation lawyer (also called a debt relief attorney or debt defense attorney) is a licensed attorney who can help you:

- Negotiate settlements with creditors (sometimes with stronger leverage when legal issues are involved)

- Respond to lawsuits and file legal defenses (critical if you’ve been served)

- Stop or reduce aggressive collection actions (depending on your situation and state laws)

- Evaluate bankruptcy (Chapter 7 or Chapter 13) and handle filings when appropriate

- Protect assets and reduce risk when you have judgments, liens, garnishments, or business exposure

Important: This page is educational and not legal advice. Always confirm licensing, fees, and state availability directly with any attorney or firm.

🧠 When a lawyer makes sense (and when it doesn’t)

👍 Hire a lawyer if:

- You’ve been sued or think a lawsuit is likely

- Your wages/bank account are at risk (garnishment or levy threats)

- You have judgments, liens, or complicated legal exposure

- You’re weighing bankruptcy and need proper legal guidance

- You want attorney-client privilege for sensitive details (business, divorce, inheritance, etc.)

👎 Skip the lawyer if:

- You’re not being sued and your debt is mostly standard unsecured accounts

- You mainly need a structured payoff plan and interest-rate relief (credit counseling may fit)

- You’re looking for the lowest-cost option and your situation is straightforward

💰 Fees & costs (the numbers people actually care about)

Costs vary by state and by how complex your case is, but here are realistic ranges so you can sanity-check what you’re being quoted.

| Option |

Typical cost structure |

Common ranges |

Best for |

| Debt settlement company |

Success-based fee after a settlement is reached and approved |

~15%–25% of enrolled debt (varies by state/company) |

Unsecured debt, not being sued, want a structured settlement plan |

| Debt consolidation loan |

Interest + possible origination fees (depends on lender/credit) |

APR varies widely; origination fees can be 0%–10% in some cases |

Good credit / stable income, want one monthly payment |

| Credit counseling (DMP) |

Monthly admin fee (often modest) + negotiated interest concessions |

Commonly $0–$75/month (varies by agency/state) |

You can repay in full but need lower rates and structure |

| Debt relief attorney |

Hourly, flat fee, or staged fees depending on service |

Hourly often $200–$500+; flat fees vary widely; bankruptcy cases often have separate filing/court costs |

Lawsuits, garnishment risk, complex cases, bankruptcy evaluation |

Two authority resources worth reading before you sign anything: the FTC’s guidance on debt relief and fees (FTC overview) and the CFPB’s consumer education on negotiating and debt relief options (CFPB debt collection tools).

Want settlement without paying “lawyer money” unless you truly need it?

If you’re not in a lawsuit right now, start by comparing settlement providers and fees. We keep New Era at the top of our list for a settlement-only approach. If your situation turns legal, you can still escalate to an attorney.

Disclosure: We may earn a commission if you enroll through our partner link.

🔍 How to vet any debt attorney or “law firm” program (avoid getting burned)

- Confirm licensing: Make sure you’re dealing with a real licensed attorney (or a firm supervised by one) in a state where they can legally serve you. If they won’t provide bar details, that’s a red flag.

- Get the fee structure in writing: Hourly vs. flat fees, what’s included, and what triggers extra charges (court filings, adversary proceedings, negotiation rounds, etc.).

- Ask what happens if you’re sued: Some “attorney-backed” programs still won’t represent you in court without extra fees.

- Understand credit impact: Any strategy that involves missed payments can damage credit temporarily. Make sure you’re choosing it intentionally.

- Ask for a realistic timeline: Anyone guaranteeing a specific outcome or promising “debt gone in 30 days” is not being straight with you.

Top debt consolidation law firms & attorney-led programs (nationwide options)

Below are well-known firms/programs people commonly compare. Availability and services vary by state, so verify directly.

1) Oak View Law Group (OVLG)

- Website: ovlg.com

- Phone: (800) 530-6854

- Best for: Broad consumer-debt help, including harder categories (like payday-related issues) and multi-step cases

- Tip: If OVLG is on your shortlist, you can also read our breakdown here: OVLG review

2) McCarthy Law PLC

- Website: mccarthylawyer.com

- Phone: (855) 875-9920

- Best for: Debt defense situations (especially if legal pressure is escalating)

3) National Legal Center

- Website: nationallegal.com

- Phone: (800) 728-5285

- Best for: People who want guided help and a structured process (verify state coverage)

4) Price Law Group (Resolve Law brand)

- Website: pricelawgroup.com

- Phone: (866) 210-1722

- Best for: Comparing settlement vs. bankruptcy when your debt load is heavy

5) Watton Law Group

- Website: wattongroup.com

- Phone: (414) 409-5422

- Best for: Foreclosure pressure, secured-debt stress, and bankruptcy-centered strategies

6) Recovery Law Group

- Website: recoverylawgroup.com

- Phone: (310) 997-0479

- Best for: People who want a more tech-enabled process plus legal escalation options

7) Kaplan Law Firm (student-loan focused)

- Website: kaplanlawatx.com

- Phone: (312) 294-8989

- Best for: Borrowers who want help navigating student-loan strategy and relief pathways

8) Five Lakes Law Group

- Website: fivelakeslawgroup.com

- Phone: (855) 441-6129

- Best for: People comparing attorney-led negotiation with a more structured monthly plan (verify state coverage)

9) Turnbull Law Group

- Website: turnbulllawgroup.com

- Best for: Large-scale cases where you want settlement plus legal backup options (confirm fees + representation scope)

- Note: Review profiles can differ by entity/location; always verify you’re looking at the exact firm you’ll be contracting with.

10) Your state bar referral directory (best way to find a true local specialist)

- Best for: Finding a lawyer who can appear in your local courts if needed

- Start here: The American Bar Association has a directory of state and local bar associations: ABA lawyer finder resources

🧾 What these attorneys can help with

| Legal service |

What it means in real life |

| Negotiate with creditors |

Reduce balances, settle accounts, and structure agreements (sometimes with better leverage when legal issues exist). |

| Legal protection |

Respond to lawsuits, defend claims, and reduce the odds of default judgments. |

| Stop garnishments |

Depending on your situation, they can file motions, negotiate resolutions, or recommend bankruptcy protection when appropriate. |

| Bankruptcy strategy |

Assess Chapter 7 vs Chapter 13, exemptions, and the realistic trade-offs. (Bankruptcy info hub: U.S. Courts overview) |

| Complex cases |

Judgments, liens, business exposure, secured-debt stress, and situations where a generic “settlement program” can backfire. |

🆚 Lawyer vs. settlement company vs. credit counseling (quick comparison)

| Feature |

Settlement company |

Credit counseling (DMP) |

Debt relief attorney |

| Reduces principal (balance owed) |

✅ Often |

❌ Usually not |

✅ Sometimes |

| Can defend you if sued |

❌ No |

❌ No |

✅ Yes |

| Best for credit-score preservation |

⚠️ Mixed |

✅ Often |

⚠️ Depends |

| Typical cost |

~15%–25% of enrolled debt |

Often $0–$75/month |

Hourly or flat legal fees |

| Good starting point if not sure |

✅ Yes |

✅ Yes |

⚠️ If legal pressure exists |

If you want a simple “start here” plan

- If you’re unsure what path fits, start with our quiz: Debt Relief Quiz.

- If you’re not being sued and have mostly unsecured debt, compare settlement providers and fees. Start with New Era Debt Solutions.

- If you’ve been sued, face garnishment, or need bankruptcy guidance, consult a licensed attorney in your state (use the ABA/state bar directory above).

Disclosure: We may earn compensation if you enroll through our partner link.

Frequently Asked Questions About Debt Consolidation Lawyers

I’ve been writing about debt relief, debt settlement, consolidation, and bankruptcy-related options for years now, and one thing I can tell you with confidence is this: there is no one-size-fits-all answer here. I’ve seen people save a lot of stress by choosing the right path early, and I’ve also seen people waste months, or even years, forcing the wrong solution. If you want a faster starting point before reading through everything, I’d suggest taking our debt relief quiz. It was built to help you think through whether settlement, consolidation, counseling, or bankruptcy may make the most sense for your situation.

Do I really need a debt consolidation lawyer?

In my experience, you usually need a debt consolidation lawyer when your debt situation has crossed over into legal territory. If you’ve been sued, threatened with garnishment, hit with a judgment, or you’re seriously weighing bankruptcy, that’s when I think legal help becomes much more valuable.

But if you’re dealing mostly with unsecured debts like credit cards, personal loans, or medical bills, and nobody has taken you to court, I usually would not tell you to run to a lawyer first. In a lot of those cases, a settlement-focused company, a debt management plan, or even a careful self-directed strategy may make more sense financially. I’d start by comparing paths, not assuming the legal route is automatically the best one.

What is the difference between a debt consolidation lawyer and a debt settlement company?

This is one of the biggest points of confusion I see. A debt settlement company is generally there to negotiate unsecured debts down, usually for less than the full balance. A debt lawyer, on the other hand, can actually give legal advice, respond to lawsuits, represent you in court, and help you think through legal exposure.

I look at it this way: if the issue is mainly financial, a settlement company or counseling route may be enough. If the issue is legal, that’s where a lawyer earns their keep. If you want to compare non-legal options first, I’d look at our guide to the best debt settlement companies and see how those models stack up.

Can a debt lawyer stop a lawsuit or wage garnishment?

Sometimes, yes, and this is one of the clearest reasons to bring in a lawyer. Depending on the case and your state, an attorney may be able to file a response, challenge part of the claim, negotiate a settlement before things worsen, or advise you on legal protections that a normal debt relief company simply cannot offer.

I would not drag my feet on this. Once a default judgment is entered, your options can narrow quickly. If you’ve already gotten court papers or a garnishment notice, I think that moves you out of the “maybe I’ll just compare companies online” stage and into “I should get legal guidance now” territory.

Can a debt consolidation lawyer lower the amount I owe?

Yes, in some cases. I’ve seen attorneys help negotiate reduced payoffs, especially when creditors know the alternative could be litigation, bankruptcy, or a harder fight than they want. But I would never tell someone to assume a lawyer automatically gets a better deal just because they’re a lawyer. That’s not always how it plays out.

If your goal is mainly to reduce unsecured balances and you are not being sued, a settlement provider may actually be the more direct and cost-effective starting point. That’s why I usually tell readers to explore more than one path. For example, you may want to compare attorney-led help with a company like New Era Debt Solutions or look at another option like CuraDebt.

Will hiring a debt lawyer hurt my credit?

No, hiring the lawyer itself does not hurt your credit. What affects your credit is the underlying strategy. Settlements, missed payments, charge-offs, and bankruptcy can all have credit consequences, whether a lawyer is involved or not.

What I usually tell people is to stop thinking only in terms of credit score if the bigger issue is financial survival. I’ve reviewed plenty of cases where the person was so focused on protecting their score that they ignored a much bigger legal or cash-flow problem. Sometimes the right move is the one that stabilizes your situation first, then lets you rebuild later.

Is a debt consolidation lawyer better than bankruptcy?

Not necessarily. In fact, one of the most honest things a good debt lawyer can do is tell you when bankruptcy may be the cleaner answer. I’ve seen people spend too long trying to force settlements or payment plans when the numbers simply did not work. In those situations, bankruptcy was often faster, more realistic, and less damaging in the long run than dragging things out.

On the other hand, if your debt load is still manageable, you have income coming in, and the situation has not fully blown up yet, then bankruptcy may be premature. This is where nuance matters. I’d strongly suggest taking our debt relief quiz if you’re on the fence, because many people are not actually choosing between “good” and “bad” options. They’re choosing between the least painful realistic option for their case.

Can a debt consolidation lawyer help with credit card debt?

Yes, absolutely, especially when the balances are large, the accounts are already in collections, or a creditor is becoming aggressive. I’ve seen lawyers step in and help when a normal settlement program would not have been enough because the risk of legal action was already too high.

That said, credit card debt is also one of the areas where people often have the most options. Depending on your income, credit, hardship level, and how far behind you are, the right solution might be settlement, a debt management plan, consolidation, or bankruptcy. That’s why I usually tell readers not to latch onto one label too quickly. Start broad, then narrow down.

Can a debt lawyer help if I already have a court summons?

Yes, and if you already have a summons in hand, I think that is one of the strongest signs that you should stop browsing casually and get serious help. A lawyer may be able to help you respond on time, avoid a default judgment, negotiate a resolution, or advise whether bankruptcy should be considered before things spiral further.

I’ve seen too many people ignore summons paperwork because they felt overwhelmed or hoped it would somehow go away. It usually does not. If you’ve reached that point, move quickly.

How much debt should you have before hiring a debt lawyer?

I don’t think there’s a magic dollar amount. I’ve reviewed cases where one aggressive creditor created more urgency than a larger overall debt balance would have. What matters more is whether the situation is legally risky, financially unsustainable, or both.

In general, the more complicated the case, the more likely legal advice is worth paying for. A person with moderate debt and a lawsuit may need a lawyer faster than someone with higher debt but no legal exposure yet.

Are debt consolidation lawyers legit?

Some are, yes. Some are excellent. But I’ve also seen plenty of “attorney-backed” marketing that sounds more impressive than the actual service being offered. That’s why I always tell people to slow down and verify exactly who is handling your case, whether they are licensed in your state, what they will actually do for you, and whether court representation is really included.

I also think it helps to compare legal options with mainstream debt relief companies so you can better understand the trade-offs. For example, you may want to compare legal help with reviews of companies like TurboDebt or Freedom Debt Relief. The goal is not to assume one category is always better. It’s to see which model fits your actual problem.

Can I use a debt settlement program first and switch to bankruptcy later?

Yes, that happens all the time. I’ve seen readers try settlement first, only to realize later that their income was too tight, creditors were too aggressive, or the whole thing was just taking too long. At that point, they pivot to bankruptcy. There is nothing unusual about that.

Still, I think it is better to make that decision as early and honestly as possible. If the numbers already suggest that repayment is unrealistic, you may be better off learning that now instead of after two stressful years. That’s one reason I keep pointing people toward our debt relief quiz. It’s not perfect, but it does help frame the right questions before you commit to a path.

What types of debt can a debt consolidation lawyer help with?

Most commonly, I see debt lawyers involved with credit cards, personal loans, collection accounts, medical debt, lawsuits, judgments, and more complex consumer-debt issues. Some also handle tax debt, foreclosure-related problems, or certain business-related liabilities, but that really depends on the attorney’s practice.

This is why I’d never assume that one lawyer or one company is automatically right for everyone. You want someone who actually deals with your kind of problem, not just someone with good marketing.

What questions should I ask before hiring a debt relief attorney?

If I were evaluating a debt attorney for my own case, I’d want to know whether they are licensed in my state, whether they personally or directly supervise the work, whether they will represent me in court if things escalate, how the fees work, and what exactly is included. I’d also ask what they honestly think my best option is, even if that option does not benefit them.

That last part matters. The best professionals I’ve come across in this space are usually the ones willing to say, “You know what, I’m not sure my service is the right fit for you.”

What is usually the best first step if I’m overwhelmed and not sure where to begin?

Honestly, the best first step is to stop looking for a universal answer and start looking for the right category of help. If you’re not being sued and your debt is mostly unsecured, compare settlement, counseling, and consolidation. If you are being sued, facing garnishment, or think bankruptcy may be close, talk to a lawyer sooner rather than later.

If you feel too overwhelmed to sort that out on your own, I’d begin with our 2-minute debt relief quiz, then read through our main debt relief guide and our roundup of the best debt settlement companies. I’d also keep an open mind. Not all paths are equal, and the “best” solution really depends on your debt type, legal risk, income, assets, stress level, and how realistic repayment actually is for you.

by Amine Rahal | Feb 4, 2026 | Debt Relief

Debt Clear USA (www.debtclearusa.com) is a debt settlement company endorsed by Shark Tank’s Robert Herjavec that focuses on helping consumers resolve unsecured debt like credit cards, personal loans, and some medical bills. I’ve reviewed a lot of debt relief companies over the years, and my view here is pretty simple: Debt Clear USA appears to be a legitimate option worth considering, but debt settlement is not automatically the best path just because a company has good reviews. For many people, the smartest first move is to take a step back, compare all major options, and start with a neutral assessment like our debt relief quiz before signing up anywhere.

Not sure if Debt Clear USA is right for you?

Before you choose any debt relief company, I strongly recommend taking our quick quiz. It helps you compare whether debt settlement, consolidation, a debt management plan, or even bankruptcy may fit your situation better.

Quick Verdict

If you already know you want debt settlement and you have at least around $10,000 in unsecured debt, Debt Clear USA looks like a reasonable company to put on your shortlist. It appears to operate as a direct settlement provider rather than just a lead-gen brand, and that matters. Still, I would not make a decision based on branding, celebrity endorsement, or review volume alone. I would compare it against other settlement companies like Accredited Debt Relief, New Era Debt Solutions, Freedom Debt Relief, National Debt Relief, Americor, and CuraDebt before moving forward.

What Debt Clear USA Actually Does

Debt Clear USA mainly offers debt settlement, sometimes called debt negotiation. In plain English, that means the company tries to negotiate with your creditors so you can settle enrolled debts for less than the full balance owed. This usually applies to unsecured debts, not secured debts like mortgages or car loans.

That can sound attractive, especially if your balances have snowballed and minimum payments no longer make a dent. But I always like to remind readers that debt settlement is not a magic reset button. It can damage your credit, creditors can still keep collecting while negotiations are happening, and forgiven debt may create tax issues in some cases. That is why I usually tell people to compare settlement against other solutions first, including the broader companies listed on our best debt settlement companies page and even specialist resources like our debt consolidation lawyers guide when their situation is messier than average.

Debt Clear USA vs. simply choosing “any” debt settlement company

| Feature |

Debt Clear USA |

What I’d look for in any competitor |

| Core service |

Debt settlement / debt negotiation |

Clear specialization in settlement rather than a vague sales funnel |

| Typical debt fit |

Usually better for larger unsecured debt loads |

Clear minimum debt requirement disclosed early |

| Fees |

Industry-standard performance-based settlement fees |

No upfront fees and simple explanation of when fees are earned |

| Risk disclosure |

Should be discussed in consultation |

Honest talk about credit damage, collection pressure, lawsuits, and taxes |

| Best for |

Consumers who likely need settlement, not just budgeting help |

People who have already ruled out cheaper options |

Company Snapshot

Robert Herjavec from ABC’s Shark Tank is associated with the brand’s marketing and visibility.

- Official Name: Debt Clear USA, LLC

- Official Website: www.debtclearusa.com

- Phone: (877) 510-3328

- Headquarters: 110 SE 6th St, Fort Lauderdale, FL 33301

- Main Focus: Debt settlement for unsecured debt

- Typical Fit: Consumers who are overwhelmed by unsecured balances and may not qualify for lower-cost solutions

Is Debt Clear USA legitimate?

From what I can see, Debt Clear USA appears to be a legitimate debt settlement company rather than a fake or fly-by-night operation. The company has a visible public presence, strong customer-review visibility, and it presents itself as aligned with standard industry practices like charging after settlements rather than before. That said, I always tell readers that “legit” is only the first filter. A legitimate settlement company can still be the wrong choice for your case if your debt is manageable through a lower-risk option. :contentReference[oaicite:2]{index=2}

This is where many consumers get tripped up. They search for the “best” company when the better question is, “Should I even be doing settlement at all?” If your credit is still decent, if you can still make payments, or if a lower-interest repayment path is available, settlement may be too aggressive. I’d compare Debt Clear USA against general alternatives like debt management, consolidation, and state-specific relief pages such as North Carolina debt relief, Florida debt relief, and Illinois debt solutions if you want more context around what other residents are considering.

Ratings and review profile

One thing Debt Clear USA clearly has going for it is social proof. It has a strong public review footprint, and that matters because some smaller debt relief brands barely leave a trace online. Still, I never treat review averages as the whole story. In this space, you want to read for patterns: did clients say the process was explained clearly, were fees disclosed properly, did people feel informed, and were expectations realistic? That tells me more than a star average by itself. :contentReference[oaicite:3]{index=3}

I would also pay close attention to how a company explains the unpleasant parts of debt settlement. If a rep makes it sound painless, instant, or guaranteed, that is a red flag. Good companies should be upfront that missed payments, credit-score damage, collections pressure, and legal risk can all be part of the process. That is not unique to Debt Clear USA. It is part of the settlement model itself. :contentReference[oaicite:4]{index=4}

Want help choosing between settlement, consolidation, or bankruptcy?

That decision matters more than the company name. Use our quiz to narrow down the path that actually fits your debt level, income, and urgency.

Start the Debt Relief Quiz

Services offered by Debt Clear USA

- Debt settlement / debt negotiation: This is the main service. The company negotiates with creditors in an attempt to reduce what you owe on enrolled unsecured debts.

- Free consultation: You can usually speak with a representative, review your debts, and see whether their program is even a fit before committing.

- Program guidance: Like many settlement firms, they appear to help clients understand the process, monthly deposits, and account progression.

What they do not seem to emphasize is a wide menu of alternatives. That is normal for a specialist. But as a consumer, it means you should bring your own comparison mindset. For example, if what you really need is a structured repayment plan instead of settlement, a company like Debt Clear USA may not be the best fit. I’d look at broader comparison resources too, including our reviews of JG Wentworth Debt Relief and TurboDebt.

Who Debt Clear USA may be a good fit for

- People with significant unsecured debt who are already falling behind

- Consumers who do not qualify for affordable consolidation

- Borrowers who understand settlement is a damage-control strategy, not a credit-building strategy

- People who want a direct settlement provider instead of chasing random ads online

Who should probably look elsewhere first

- Anyone with strong enough credit to qualify for a lower-interest consolidation loan

- Anyone who can realistically repay debt in full through tighter budgeting or a debt management plan

- People with mostly secured debts

- Consumers who are highly sensitive to short-term credit damage

- Anyone expecting guaranteed results or a fast, easy timeline

👍 Debt Clear USA Pros

- Focused service model: The company appears built around debt settlement rather than trying to be everything to everyone.

- Strong review visibility: There is enough public customer feedback to at least evaluate sentiment patterns instead of guessing.

- No obvious “upfront fee” positioning: That is what you want to see in this industry.

- Recognizable public brand presence: Some consumers may feel more comfortable with a company that is easier to research than a tiny unknown brand.

👎 Debt Clear USA Cons

- Debt settlement is inherently risky: Even a good company cannot remove the downsides built into the model.

- Credit damage is part of the process: This is not a minor side effect. It is a core tradeoff.

- Fees can still be substantial: No upfront fee does not mean low total cost.

- Not ideal for smaller debt loads: Many settlement programs work best for people with larger unsecured balances.

- Potential lawsuit and tax issues: These are real possibilities that too many consumers underestimate. :contentReference[oaicite:5]{index=5}

What types of debt can they help with?

Debt Clear USA mainly focuses on unsecured debt. That usually means:

- Credit card debt

- Personal loans

- Medical debt

- Some private student loans

- Certain business-related unsecured debts

If your issue is more specialized, you may want to read beyond general settlement reviews. For example, tax debt is a very different animal, which is why pages like Tax Relief Advocates and what a tax debt attorney does can be more relevant than a standard debt settlement review.

Important things many reviews don’t explain clearly enough

This is the section I think matters most.

First, debt settlement usually means missed payments. That is how leverage gets created. Creditors are more likely to negotiate after accounts become seriously delinquent. This can lead to collections calls, credit-score damage, and extra stress along the way. :contentReference[oaicite:6]{index=6}

Second, there is no guarantee every creditor will play nice. A settlement company can negotiate, but it cannot force every creditor to accept a reduced payoff. In some cases, a creditor may escalate collection efforts or sue. :contentReference[oaicite:7]{index=7}

Third, forgiven debt can sometimes create a tax issue. In general, canceled debt may be treated as taxable income unless an exception applies. That does not mean everyone gets hit with a surprise tax bill, but it is something you should ask about before enrolling. :contentReference[oaicite:8]{index=8}

Fourth, cheaper alternatives sometimes exist. I’ve seen many consumers jump straight to settlement because ads make it sound like the default solution. It isn’t. Sometimes the better answer is consolidation, counseling, a workout with creditors, or simply choosing a different company and strategy after comparing several options carefully.

Best next step before signing up with any debt relief company

Take our debt relief quiz first. It is the fastest way to pressure-test whether settlement really makes sense for you, or whether a different path may save you money, stress, and credit damage.

My overall opinion

Debt Clear USA looks like a real company with enough public credibility to deserve consideration. I would not dismiss it. But I also would not treat it as an automatic yes. In this niche, the bigger question is not “Is this company legit?” but “Is debt settlement the right move for me at all?”

If you are already behind, overwhelmed, and realistic about the tradeoffs, Debt Clear USA could be worth a consultation. If you still have decent credit or a realistic chance to repay what you owe under better terms, I’d explore other paths first. That is exactly why I recommend taking the quiz before choosing any provider.

FAQ About Debt Clear USA

Is Debt Clear USA a scam?

From everything I could reasonably review, it does not appear to be a scam. It appears to be a real debt settlement company with a public footprint and meaningful review activity. That said, “not a scam” does not automatically mean it is the best option for your financial situation.

How much debt do you usually need for Debt Clear USA?

Many settlement companies work best when you have a fairly large amount of unsecured debt, often around $10,000 or more. If your debt is lower than that, the math may not work as well, and another solution could be more practical.

Will Debt Clear USA hurt my credit?

Debt settlement itself is not a credit-building strategy. In most cases, consumers enter settlement after they stop making regular payments, and that can seriously hurt credit in the short to medium term. This is one of the main tradeoffs you need to understand before enrolling.

Can creditors still sue while you are in a debt settlement program?

Yes. A settlement company can negotiate, but it cannot stop a creditor from taking legal action. Some creditors settle, some wait, and some may decide to escalate. That is one of the most important risks consumers should understand upfront. :contentReference[oaicite:9]{index=9}

Are debt settlement fees charged upfront?

Reputable settlement companies should not charge upfront fees before a debt is successfully settled. If a company seems evasive on this point, I would be cautious. :contentReference[oaicite:10]{index=10}

Can settled debt become taxable?

Sometimes, yes. In general, canceled debt may be taxable unless an exception applies, such as certain insolvency or bankruptcy situations. This is something I would specifically ask about before enrolling in any settlement program. :contentReference[oaicite:11]{index=11}

What should I do before choosing Debt Clear USA?

Compare the company against at least a few other serious options, review total expected fees, ask how long programs typically take, ask how lawsuits are handled, and make sure you compare settlement with alternatives like consolidation or counseling. I’d start with our debt relief quiz before making any commitment.

Other helpful resources on our site: Debt relief hub, best debt settlement companies, best companies, New Era Debt Solutions review, CreditAssociates review, Pacific Debt Relief review, ClearOne Advantage review, and Family Credit Management review.

by Amine Rahal | Jan 30, 2026 | Selling a Business

If you’re Googling “how much can I sell my business for” you’re usually close to a decision. The fastest way to get a confident answer is to stop thinking in “what I want” terms and start thinking in “what a buyer can verify” terms: clean cash flow + reduced risk + repeatable operations.

Want a realistic estimate of what your business could sell for? Get a valuation range plus the key drivers buyers and brokers will scrutinize.

Get My Business Valuation Range

Disclosure: We may earn a commission if you use our partner link.

Quick answer: Most sale prices come from a simple structure:

- Cash flow (SDE or EBITDA)

- × a multiple (based on risk and growth)

- ± working capital and asset adjustments (varies by deal)

If those acronyms are new, bookmark our glossary of business terms so your whole team is speaking the same language.

The Two Numbers That Drive Your Company’s Sale Price

1) Your real cash flow (SDE or EBITDA)

SDE (Seller’s Discretionary Earnings) is common for owner-operated businesses. It typically starts with profit, then adds back the owner’s salary, owner benefits, and certain one-time or non-operating expenses.

EBITDA is common as businesses get bigger, have deeper management, or attract more sophisticated buyers. It is a cleaner “operating earnings” number (before interest, taxes, depreciation, and amortization).

2) Your multiple (what buyers pay for that cash flow)

The multiple is basically a “confidence score.” Buyers pay higher multiples when your business is easier to operate, easier to verify, and less dependent on any one person (including you).

Simple valuation example

- Verified SDE: $400,000

- Market multiple range: 2.5x to 3.5x (depends on risk and growth)

- Estimated value range: $1,000,000 to $1,400,000 (before deal-structure adjustments)

What Raises Your Multiple (and What Tanks It)

👍 Value boosters (higher multiples)

- Recurring revenue (subscriptions, memberships, service contracts, retainers)

- Low customer concentration (no single customer “controls” your revenue)

- Documented SOPs (how you sell, deliver, bill, and handle issues)

- Management depth (someone besides you can run the day-to-day)

- Clean books (accurate P&L, balance sheet, and consistent reporting)

- Stable margins (buyers love predictability more than hype)

- Multiple lead sources (one channel = one point of failure)

👎 Deal killers (lower multiples)

- Owner dependency (you are the closer, operator, manager, and firefighter)

- Messy receivables (old invoices, weak collections, disputed balances)

- Financial “fog” (unclear add-backs, personal expenses mixed in, inconsistent numbers)

- Key-person risk (one employee holds the whole business together)

- Unresolved compliance or licensing issues (state, local, industry-specific)

If collections are a weak spot, fix it before you go to market. Here’s a helpful primer on business debt collection basics.

A 30-Minute DIY: Estimate What Your Business Is Worth

- Pick your “earnings” metric: use SDE if you are owner-operated; use EBITDA if you have management depth and cleaner ops.

- Calculate a conservative “verified earnings” number: remove anything a buyer will not accept (one-time personal expenses, non-business items, inflated add-backs).

- Pressure test your risk: customer concentration, seasonality, margins, churn, team stability, and owner dependency.

- Choose a realistic multiple range: the more “turnkey” and documented your business is, the higher the range you can justify.

- Add deal adjustments: working capital expectations, inventory, AR quality, equipment, and any unusual liabilities.

Tip: Buyers often sanity-check your numbers against what it costs to run your business today. If you want a simple way to show how costs and prices changed over time, the CPI inflation calculator can help explain price increases without a debate.

Valuation Methods Buyers Use (and When Each One Matters)

| Method |

Best for |

What it focuses on |

Watch-outs |

| Earnings multiple (SDE/EBITDA) |

Most small and mid-sized businesses |

Verified cash flow + risk |

Add-backs that do not survive diligence |

| Asset-based |

Asset-heavy operations |

Equipment, inventory, tangible value |

Can under-value strong cash-flow businesses |

| Comparable sales |

When good comps exist |

What similar businesses sold for |

Comps are often imperfect or outdated |

| DCF (discounted cash flow) |

Larger deals, finance-heavy buyers |

Future cash flow projections |

Assumptions can be argued endlessly |

How to Get a Higher Sale Price Without “Hoping”

- Build recurring revenue: contracts, retainers, memberships, subscription plans.

- Reduce owner dependency: appoint an ops lead, document SOPs, standardize quoting and delivery.

- Clean up your financial story: separate personal items, tighten add-backs, reconcile accounts monthly.

- Fix AR and collections: get old receivables resolved before diligence starts.

- Diversify acquisition channels: referrals, organic, paid, partnerships, outbound.

Not sure what your “multiple” should be? A valuation range plus a simple “value driver” breakdown helps you see what to fix to push your number up.

See My Estimated Sale Price Range

Disclosure: We may earn a commission if you use our partner link.

What You Should Prepare Before You Talk to Buyers

- 3 years financials + current YTD (monthly breakdown is ideal)

- AR/AP aging (buyers want to see if cash collection is healthy)

- Customer list and concentration (top customers and contract terms)

- Org chart + key employee roles (and retention plan)

- Process docs (sales scripts, SOPs, checklists, QA steps)

- Asset list (equipment, inventory, software subscriptions, leases)

If you also have meaningful digital assets (ranked website, email list, lead magnets, strong inbound), they can increase value. For context on how marketplaces think about digital assets, see our Flippa marketplace review.

Related Guides You Might Want Next

These state-level sell guides help you see how “local reality” affects deal terms and buyer behavior: Selling a business in California, Selling a business in Florida, and Selling a business in South Dakota.

Authority Resources (Worth Reviewing Before You Sell)

If you want to sell in the next 6–18 months, the best move is to get a valuation range and a prioritized “fix list” before buyers set the narrative for you.

Start With a Valuation + Fix List

Disclosure: We may earn a commission if you use our partner link.

FAQ: Business Valuation and Sale Price

How much should I sell my business for?

A good “should” price is a price you can defend with verified earnings, reasonable add-backs, and a multiple that matches your risk profile. If your number depends on hope or “future potential,” it usually gets discounted. If your number is backed by clean reporting and repeatable operations, it becomes easier to negotiate.

What is the difference between SDE and EBITDA?

SDE is common for owner-operated businesses and includes owner compensation plus certain add-backs. EBITDA is a more standardized operating earnings metric used more often as businesses scale. Buyers may start with SDE and convert to an EBITDA view to compare opportunities.

What add-backs do buyers usually accept?

Buyers tend to accept add-backs that are clearly documented, truly one-time, or genuinely non-operating. They push back hard on “creative” add-backs, personal expenses that look recurring, or anything that cannot be proven in your books.

Will a buyer pay for “potential”?

Sometimes, but potential is usually paid through deal structure (earnouts, performance-based payments) instead of a higher upfront price. The most reliable way to get a bigger check at close is to turn “potential” into “proof” before you go to market.

How long does it take to sell a business after valuation?

If your business is already clean (books, operations, team, compliance), a sale can move quickly. If you need to clean up financials, reduce owner dependency, and fix AR or documentation gaps, the preparation phase may take longer than the sale itself.

Note: This content is for educational purposes and does not constitute legal, tax, or financial advice. For help with a specific situation, consult a qualified professional.