Ryan Barnes

Ryan is a financial analyst & forecaster. He has 20 years of experience in asset modeling, investment analysis/general dd, portfolio management, and macroeconomic analysis. To that end, he has worked extensively with equities, fixed income, commodities, private equity, currencies, and derivative products. His commentary and educational library appear on Investopedia.com, and analysis has appeared in Barron’s, WSJ.com, TheStreet.com, and Forbes.com.

by Ryan Barnes | Mar 25, 2015 | CPI, Definitions, gold, Inflation

The U.S. economy got a little economic boost today with a stronger-than-expected CPI reading for February, and a strong Purchasing Manager’s Index (PMI) that continued to project GDP growth.

Headline CPI and core CPI both came in 0.2% higher than January, as slight price hikes at the pump for refined products balanced out a general breather in the declines in some of the base commodities. The headline numbers had been tracking negative for the past three months, which everyone was pretty much ok with chalking up to crude oil. Just so long as GDP growth came in respectably, there wasn’t any reason to panic.

But core CPI (ex-food and energy costs) was already lagging behind Fed goals of around 2%, and already in the midst of sending deflationary ripples up the global goods chain, into…well, just about everything.

Muddled Waters for First Rate Hike

It’s created a tense chess match between investors and the Fed the past few weeks. It started just after the stellar (as in +295,000) February jobs report last month, when the consensus started to form that the Fed would have to act sooner rather than later in creating a interest rate normalization cycle.

The key first step of that cycle is getting us off the floor of zero percent rates – a stance that doesn’t befit a growing economy and presents what Yellen herself has called an “asymmetrical risk”.

U.S. Definitely Growing…But How Much?

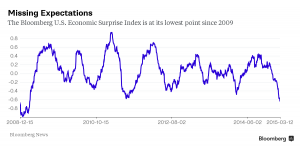

Just as soon as we seemed to have some headway into a summer rate increase, nearly every economic indicator in the U.S. started been printing well below analyst estimates. In fact, the depth of our misses has hit a multi-year high, according to Bloomberg analysis:

In light of this reversal, both investors and the Fed have had to take stock of things. First quarter GDP estimates continue to be ratcheted down – from the 2.5% – 3.0% level I highlighted last month (a number that was freshly lowered at the time) to an average Q1 GDP estimate of about 1.5% today.

Cranky Markets are Volatile Markets

It’s why we’ve seen a spike in volatility around every asset class – fixed income, forex, commodities, and equities have all been bumping around trying to align their compass to the next clear trend line. Would the Fed remove “patient” in the March FOMC meeting? Was September the new June (for the first rate hike)? Was 2015 off the table entirely?

Answering these questions is challenging enough in isolation, but it’s been exacerbated by the stunning rise the the USD index, which alters true price action in commodities and long bonds. The surging U.S. dollar is a de facto rate hike. It lowers the cost of imports dramatically (a deflationary force), and it makes our exports more expensive overseas.

And while the realities of pricier U.S. exports certainly hurt some companies more than others, the simple fact is that close to 50% of the total revenues of the S&P 500 member companies is derived in a currency other than the U.S. dollar.

2014, Part Deux?

It’s quite astonishing how much the first quarter of this year is looking like the first quarter of last year. Tick by tick, indicator by indicator, we seem to be replicating that market environment.

This time last year we were watching interest rates hit new lows, but convinced the party had to end any moment – inflation was coming, and we needed to position ourselves away from fixed income and into equities, gold, and other commodities. Fixed income turned out to deliver stronger returns than even equities did.

GDP looked to be on track for a good start to the year, but then a bout of really bad whether caused us to actually contract as an economy in Q1. Most of the top analysts said “don’t worry, we’ll be strong in the back half of the year”, and sure enough we were. The U.S. turned in over 4.5% growth in the next two quarters.

Looking around today, it’s much the same setup – so far. The key differences between then and now are this:

1) the unemployment rate is lower than last year; we have clearly moved close enough to full unemployment in the Fed’s eyes that it’s no longer an impediment to a rate increase. That box is checked off.

2) the USD is much stronger (10-20% or more) against every major global currency. As I’ve discussed, this move alone is the equivalent of a 25-50 bps rate hike.

In fact, if the dollar hadn’t been zooming so hard the past six months, there’s a chance the Fed would’ve put a token 25bp hike out there last week. Instead, Yellen reminded us that the Fed isn’t there to make things easy for investors, saying the Fed “can’t provide and shouldn’t provide” certainly to markets when it comes to the timing of rate hikes.

We don’t seem to be in any danger of that.

by Ryan Barnes | Feb 27, 2015 | Definitions

It’s been an extremely active week in terms of the economic indicators, market activity, and rhetoric that is driving today’s interest rate and inflation discussions.

Heading into the week, investors all seemed to be in “coin flip” mode as to the tone Janet Yellen would take as she testified before the Senate and then the House on Tuesday and Wednesday. The Treasury market had started to forecast a spike in inflation expectations prior to her testimony, as the 10-yr yield rose nearly 50 basis points in a matter of a few sessions.

In her statement on Tuesday, Chair Yellen gave an update on the economy and the Fed’s current outlook for inflation and monetary policy. True to her nature, she came out dovish, not specifying an exact target date for the first rate increase, instead reminding us that the Fed is very data-dependent right now. She noted that while the economy was strong, there was “still room for improvement” in the labor market.

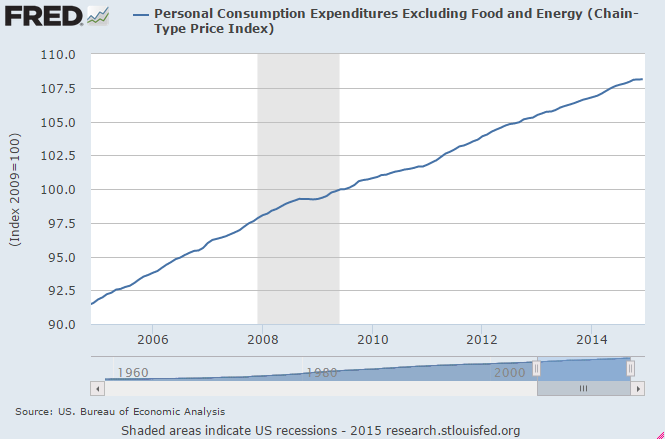

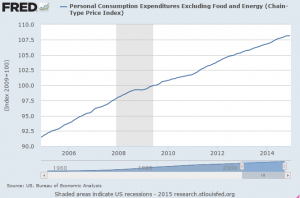

Yellen also noted that the Personal Consumption Expenditure metric (the Fed’s preferred inflation reading) was still tracking well below the Fed’s desired target of 2%, and that Q1 PCE “looks to fall further” than even the weak reading we saw in Q4 of last year.

Forced to be a Global Fed

As I’ve noted in previous postings, Yellen and the Fed feel compelled to look around the globe when trying to assess the prudence of raising rates in June, September, or anytime in 2015. Massive deflationary forces are coming into the U.S. as crude oil stands 50% lower than a year ago, while growth is noticeably slowing in China and most advanced economies. Yellen did note however on Tuesday that low crude oil prices were a “significant plus” to the economy over the remainder of 2015.

On Thursday, we got the all-important CPI for January, and it read much like Yellen hinted it would. The headline reading was (0.7%) versus a consensus estimate of (0.6%). The Core CPI (ex-food and energy) was up a shade a 0.2%, a tick better than the consensus view. Notable breakouts were food costs flat month/month, energy prices that were down 9.7% and gas prices that were down 18.7%; the latter two have been falling sharply for quite a few months now but the Fed seems intent on “looking through it” for the time being, and has intimated that they can start raising rates even if the headline inflation rate is sitting below the targeted 2% range. As it stands now, the trailing 12-month change in the core CPI is now 1.6%, unchanged from December.

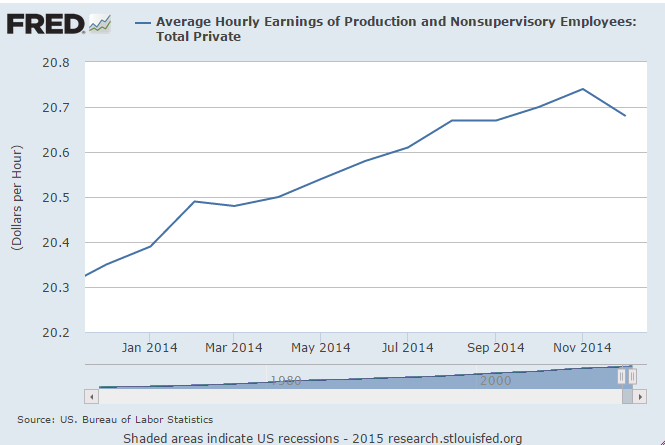

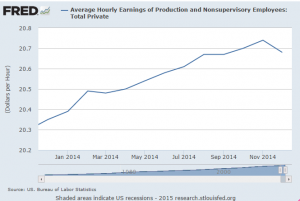

An important component to come out of the Bureau of Labor Statistics yesterday was real average hourly wages up 1.2%, on a nominal gain of 0.5%. This now puts the YoY change in real wages at 2.4% on a seasonally-adjusted basis, an encouraging reading for those of us who want to see the Fed Funds rate get inched upwards as soon as possible.

Other regional Fed Presidents have made some public comments this week echoing the same general theme that the economy is strong, and that the Fed currently has the data to support an initial rate hike anytime in the back half of the year. San Fransicso head John Williams noted yesterday that wage inflation was key, as “The cosmological constant is that if you heat up the labor market, get the unemployment rate down to 5% or below, that’s going to create pressures in the labor market”.

Investor Implications

While the CPI continues to read weak, the Durable Goods orders came in stronger than expected for January, and the revised Q4 GDP figure that came out this morning was slightly higher than estimates at 2.2%. These bode well for continued labor market gains, which should be the key to a moderate rate increase cycle late this year.

by Ryan Barnes | Feb 19, 2015 | CPI, Inflation

In a week where there wasn’t much in the way of high-impact macro data, I along with other inflation hounds was left to pore over what were some very diffuse Fed minutes yesterday. There seems to be a communication breakdown – figuratively and literally – in what was the longest minutes report in recent memory (over 8000 words!) yet also the hardest to interpret.

After all, the bond markets have been moving crazily; it seemed the smell of inflation was in the air following a strong jobs report and a 35 basis point rise in the benchmark 10-yr over a two week period.

Economy Cliff’s Notes

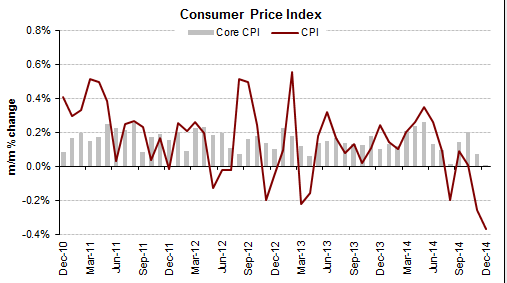

In a word, the FOMC minutes were dovish. Janet Yellen, her voting cohorts, and their staffs just can’t find enough data points to make a strong case for either inflation or broad growth. We clearly identified this reality last week, noting that things were becoming “more opaque by the day”. While there was a slight tickup in weekly pay, retails sales continues to print weak while headline and core CPI and PPI are well, well below the Fed’s 2%-ish target.

The Producer Price Index (PPI) for January came in yesterday at a 0.8% drop after a 1.1% annualized growth pace in December. Most vitally, we’re now on pace to turn in exactly zero growth Y/Y in the PPI. As with every inflation metric right now, it’s being thrown off kilter by the fall in crude oil.

For now, macro analysts like Michael Hanson over at BofA Merrill are saying that while we may see negative headline inflation, it’s “probably not deflation” as seen by the Fed. This is backed up by recent comments from Yellen, who has called the spike down in energy prices as “transitory”, while Philadelphia Fed President Charles Plosser noted that “I don’t see deflation as a risk in the U.S. economy”.

Rock and a Hard Place – Stuck in the Middle With You

I’m in the camp with most people who believe that the Fed would love nothing more than to get at least 1-2 rate hikes passed along this year. They would love to get the credit markets operating in a more normalized capacity, and they would certainly love to have the extra arrows in the quiver that a 0.5% – 1% Fed Funds rate would provide.

This stance doesn’t require one to be a hawk or a dove; it’s just good business for the Fed to have a full set of levers at their disposal. But there is real damage that could be done to the long-term viability of the Fed if they were to raise rates this summer, only to find that GDP growth has vanished and they’re forced to re-cut rates.

And as I noted last week, there is a very fine line there. The PPI results will in many ways flow through to the CPI over the next few months, and as I write this crude oil is down another 4% or so today and we may see the largest crude inventory build in history later Thursday.

As it stands now, we are the only advanced economy on the planet that is forecasting a rate increase in 2015. Granted, we are also the healthiest, so there’s a case to be made that we should be the first ones out of the gate. But for now, the Fed is admittedly (for the first time in over a year) looking overseas at risks in China and the Middle East, and even looking with some fear at the fixed income ETF market, of all places.

Investor Implications

It’s prudent for the Fed to be considering the near-term impact of falling commodities, just as it’s prudent to see them within the context of stagnant global growth. Neither are tasks we wish the Fed was spending so much time on, but the times are what they are; there’s not exactly a dog-eared playbook of what to do at this point. Just a compass.

Anybody that is out there with a strong opinion on whether the Fed is doing the right thing will have to cherry pick their metrics and indicators to prove their position. Fed Funds futures bettors scaled back their odds for a June rate hike, following the “let’s punt the ball” tone of the January FOMC minutes.

I tend to agree with a couple of analysts that have suggested the surging U.S. Dollar is a de facto rate increase already, as it will push down our exports a bit. In the meantime, the Fed – like the rest of us – will sit and wait to see if GDP is hanging in there. This continues to look a lot like Goldilocks for equities, just like the past few years.

by Ryan Barnes | Feb 13, 2015 | CPI, Inflation

The U.S. inflation picture is becoming more opaque by the day, which creates a lot of difficulty because it’s the most important variable out there – and not just to the fixed income markets. More so than at any time in recent memory, in order to read the pulse of domestic inflation I’m forced to take into consideration the entire global canvas – which for better or worse is same thing the Fed and central banks around the world are doing.

China showed up with an awful CPI/PPI print earlier this week, reaching a 5-year low on the CPI with a 0.8% January reading. The PPI continues to show accelerating declines, down 4.3% in January after a 2.7% drop in December and a 2.2% dip in November. Inside that PPI number are a 17.5% drop in mining, 9.6% in ferrous metals and 10% in fuel & power.

These advance readings don’t speak well at all to the headline figures we’ll be seeing in the U.S. over the next few months. We already know that GDP is decelerating in China, which (due to their giant nominal consumption) will put continued downward pressure on the whole commodity complex.

Europe, meanwhile, is in full-blown deflationary mode, printing a headline of (-.06%) in January, with a core reading of 0.6%. Bank of England Governor Mark Carney spoke about inflation today after their board decided unanimously to keep rates steady (their two previous holdouts backed out of their hawkish stance this month).

He noted,

“We’re going to have a period where headline inflation is low – very low – for most of this year, and that’s a good thing in general because of the causes of it. It’s not a good thing if it persists though.”

Real Uptick or Headfake?

Inflation expectations ticked up here at home to start the week, following a tremendously strong jobs report. The most important metric in the report was the 0.5% rise in hourly wages; we needed to see a rebound here after a weak December print, and to stay near the 2% – 2.3% pace that’s been maintained since the recovery began.

Janet Yellen has said in public comments that wage growth is a key metric the Fed is tracking, along with Personal Consumption (which they prefer over retail spending, per se). The Fed has taken a short-term policy stand that they’re willing to “look through” the headline drops in CPI, and treat them as transitory.

But as I noted last month, “…at present, we aren’t just tracking a little bit below the Fed’s target of 2% core inflation – we are well below it. And that’s assuming the Fed really does want to exclude the food and energy components entirely – which to their credit is precisely what they did when those components were volatile to the upside a few years ago.”

The broad consensus is that yes, the headline figures will show a big deflationary effect the next few months, but the net net effect on consumer spending and GDP will outweigh the negative effect of lower import prices and higher export prices. This stands to reason, as we are an economy driven 70% by consumer spending and just 13% by exports.

Retail Sales Yet to Confirm

But (isn’t there always one of those?), it’s sure been taking longer than most analysts expected to see the effects of the “oil tax cut” on consumer spending. The Retail Sales report came in weaker than expected this morning, down 0.8% in January, vs. expectations for a 0.4% drop. This comes on the back of a 0.9% headline drop in December, which was not adjusted in today’s release.

Yes, of course a lot of this is gas-related, as the YoY change in gas station receipts now stands at -23.5% following a 9.3% drop in January. The next biggest category decline was a 2.6% monthly drop for the group including sporting goods, hobby, book, and music sales.

Partially balancing that out are food services receipts that were up 11.3% YoY, while auto dealers saw sales rise greater than 10% in the past year.

But if we back out the main volatiles – automobiles, gas, building materials, and food services – we still tracked barely above the flatline at 0.1% growth, vs. expectations for a 0.4% increase. So far, the billions we’re saving at the pump don’t seem to be flowing back into discretionary items.

A few analysts have already made comments this morning to the effect of, “we’re not worried, the setup is all there, and we’ll see it reflected soon in the spending numbers”. And Credit Suisse noted that “inflation is falling sharply…the picture in real terms will not be as bleak”. This is most certainly going to be the case, all else being equal, but not the best opening argument for an economy trying to grow 3% this year.

Q1 Coming Down

We’re already far enough into Q1 that GDP numbers for the quarter need to start coming down. J.P. Morgan reduced to 2.5% annualized this morning (from 3%), while Barclay’s came down to 2.2%.

My own models are pegged at 2.5% right now, which is basically just a punt from last year. If we in the U.S. are to overcome all of this and hit the 2.7-2.8% GDP numbers most have modeled for the year, the Fed just may have to back off its intention to get a rate hike or two passed along in 2015. The backing off may become more telegraphed if the prevailing trend in leading indicators continues, and/or in the event that commodities fail to stabilize.

Investor Implications

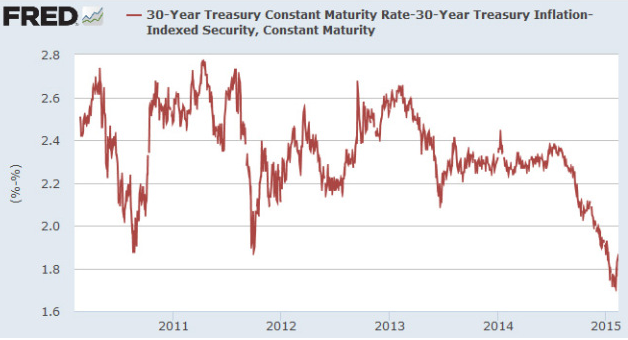

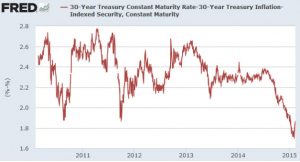

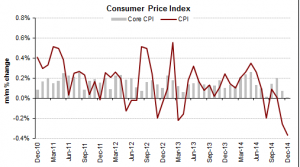

In fixed income land this is all priority #1; many bystanders have been waiting around for two years now for bond markets to sell off; instead the run for the ages just keeps on going. The trade has gotten very crowded, which may explain why the Friday jobs report seemed to have such an immediate impact on the bond markets, where the inflation breakeven point rose about 35 basis points in just a few trading sessions. It still sits (un?)comfortably below the Fed’s 2% inflation target:

But equity investors like me need to wrap our heads around the inflation trends too, as it drives global asset allocations. The strong dollar pretty much guarantees that our markets will continue to see inflows, but we’ve had almost two straight years of a Goldilocks setup as rates slowly ticked lower and earnings yields trounced bond yields. The best case scenario for stocks – and most domestic bond classes for that matter – is that we’ll repeat that setup for a third year. But it’s a very fine line we’re treading.

by Ryan Barnes | Jan 16, 2015 | Definitions

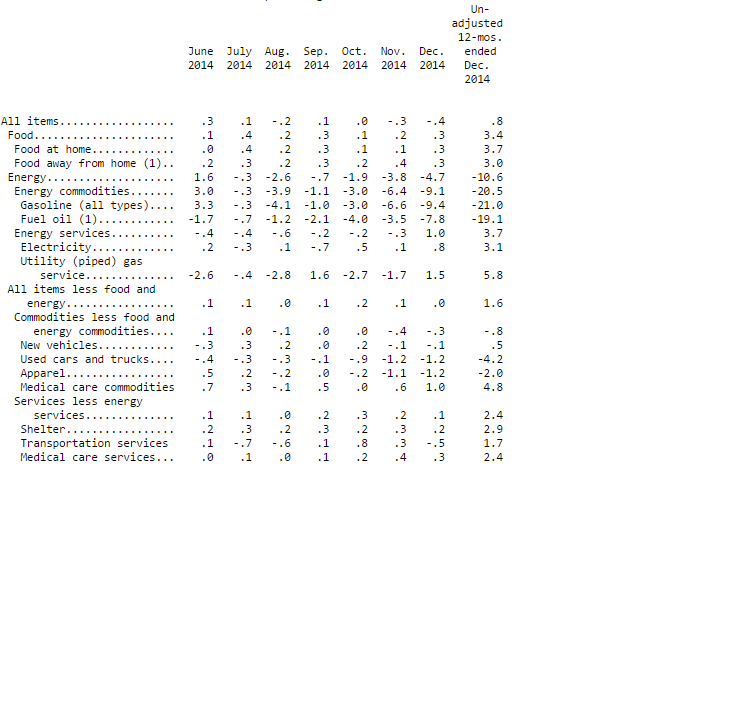

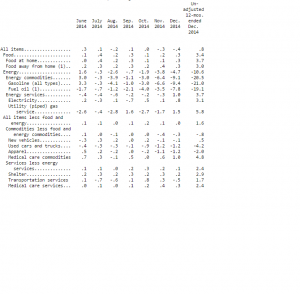

Friday’s December CPI report from the Department of Labor gave us a headline figure of -0.4% from the November reading. The drop in the most widely-cited inflation gauge was right in line with consensus estimates, although the core CPI (-ex food and energy) was slightly below consensus expectations, coming in flat from the prior month. Economists were hoping to see a slight tick up of 0.1% in December on non-food and non-energy price components.

The year-over-year change in headline CPI now stands at a paltry (or at best, “tame”) 0.8%, largely due to the relentless selloff in crude oil & energy prices in the past six months. The aggregate energy index component of the CPI – which makes up about 8.5% of the total headline figure – fell the most since late 2008 last month, dropping 4.7% on a seasonally-adjust basis.

Looking further into the energy index, gasoline continues to give most Americans a de facto tax break, with gas prices falling a stunning 9.4% last month alone, and over 21% in the past twelve months.

Given the lag time between crude and refined products like gasoline, and the continued selloff in core energy commodities, we can fully expect to see this downward pressure on inflation data for the next few months at minimum.

A minor amelioration to the deflationary aspects of energy is the rise in food costs, which were up 0.3% last month after a 0.2% rise in November. The food index is now up 3.4% year over year, but the total net effect of the commonly removed items of food and energy is still a net drag on overall inflation.

Looking at other components of core CPI, medical care costs rose 0.5% in December with a 0.9% rise in pharmaceutical costs. Apparel costs fell 1.2%, while air travel costs fell a sharp 5.0%:

Source: Bureau of Labor Statistics

What Today Means for Fed-Speak and Interest Rates

Regardless of your stance on whether they should be, the fact is that the Fed is looking around the globe right now, and taking many things into account when deciding the optimal time to begin raising short-term interest rates.

Last month we showed the distribution charts for how the big money was betting on the matter; at the time the consensus was for a rate hike in July or September 2015. Today’s CPI data points – following the similarly-tracking PPI from yesterday, which was down 0.3%, the most since 2011 – are starting to convince people that the late summer timeline could be way off. We may, in fact, see no rate increases in 2015 at all.

Courtesy of: Haver Analytics

Because at present, we aren’t just tracking a little bit below the Fed’s target of 2% core inflation – we are well below it. And that’s assuming the Fed really does want to exclude the food and energy components entirely – which to their credit is precisely what they did when those components were volatile to the upside a few years ago.

But the massive deflationary force of today’s energy commodities, combined with a surging U.S. dollar and very real deflationary fears in Europe, Japan, and even China, has really got the Fed and investors on their toes.

There won’t be a press conference today from Janet Yellen to discuss recent economic indicators, but San Francisco Fed Chair John Williams (a new addition to the FOMC this year and a relative interest rate dove) will likely make some public comments on the rate outlook, vague as they may appear in print.

We expect him to use the opportunity of today’s weak inflation data to enter some more ambiguity into the rate hike discussion, hoping to push the market towards more of a stance of “maybe 2015, maybe not”.

While the CPI is certainly a vital statistic, we’ve been told by Fed officials – and Fed Chair Yellen herself – that the indicators they’re studying the most right now are the Personal Consumption Expenditures and the Average Hourly Earnings gauges. The latter has actually been tracking slightly negative in recent months, contradicting the headline jobs figures (which show sustained growth) and the drop in the unemployment rate. Real average hourly earnings as reported this morning were up just a hair, but actually down nominally. Average earnings fell slightly, but the net effect of headline deflation last month means that technically, folks have a few more pennies’ worth of purchasing power.

What Today Means For Investors

If investors have just been looking at sovereign debt markets the past few weeks, they may claim that the deflationary effect has been staring us all right in the face. The yield curve continues to flatten; the benchmark 10 year was trading at a yield of 1.746% early Friday, while the 5 year traded at 1.231% and the 2 year note offered a miniscule 0.463% yield.

Given the spread between 10’s and 2’s, we can actually expect to see – and I can’t believe I’m saying this – more flattening on the long end, i.e. even lower rates. So at least in the short-term, this once in a generation bull market in treasuries doesn’t appear to have an end date.

Stock market futures rose modestly higher after the 8:30 a.m. CPI release, as the prospect of “lower rates for longer” could, in a bubble, set up well for equities. But the deflation argument is gathering steam and could be an asset value killer all around. While the drop in crude can very justifiably be all about supply issues, the recent and sharp drop in copper is a different story. It’s a crucial base industrial metal that seems to have no price support right now, even after having its biggest one-day decline in six years earlier this week.

With so many muddled currents swirling around the geopolitical financial landscape right now, the onus is really on us as investors and analysts to find truly applicable data sets. We here continue to promote an objective discussion of the real price pressures in the global economy, and to that end we’ll be exploring different ways of examining data points and asset class potential.