Andrew

Andrew McCarthy is an expert in all things inflation. He has a Bachelors in Economics and has been working in the finance industry for over two decades.

by Andrew | Jun 16, 2015 | Definitions

June FOMC Decision: Expect No Change in Rates – Increased Dovish Rhetoric

A packed week of inflation related data should provide more clarity on the future direction of interest rates for the rest of 2015, with the June FOMC rate decision, CPI, and guided commentary from Janet Yellen all scheduled for release. The market has already pushed out its expectations for a fed rate hike to September, so any surprise move by the Fed at the upcoming meeting, would lead to serious volatility in world markets. A survey from Bloomberg News shows only 1 economist from 74 polled believe the FOMC will move on rates at Wednesday’s meeting. While holding rates steady may be a foregone conclusion, rhetoric from the Fed will be under close scrutiny, with particular focus on any adjustments to the “Dot” system of staff projections on the Fed Funds rate for signs that the September time frame remains intact.

As ever, the post meeting commentary from Fed chairman Janet Yellen will be a significant market moving event with some aspects in particular worth keeping an eye on. Yellen recently focused on the dollar’s strength as providing significant headwinds to US exports and manufacturing, and any repeat could signal an increase focus on the currency as a policy tool going forward. Expect the Fed to also touch on the fallout from Greece and worsening economic conditions globally as potential ongoing threats going forward. The World Bank recently slashed its 2015 global economic growth forecast to 2.8%, highlighting particularly difficulties in emerging markets due to lower commodity prices and higher borrowing costs. As a block, emerging markets are now forecast to grow at 4.4% in 2015, down from an original forecast of 4.8%. Since 2008 emerging markets have been an important engine of global growth – the head of the IMF Christine Lagarde recently issued a plea to the Fed to delay any increase in rates until 2016 to avoid a potential meltdown in emerging markets. With the ongoing uncertainty globally, this looks increasingly possible.

May CPI Release

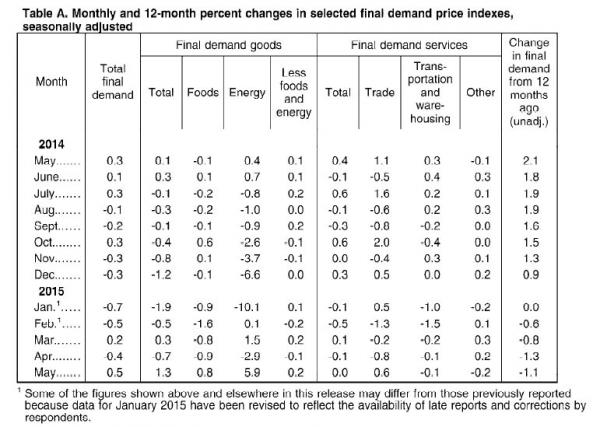

Hot on the heels of the FOMC decision, Thursday sees the release of May CPI inflation data, with consensus forecasting a 0.5% increase in month on month inflation in the headline number, and an increase of 0.2% from last month in the core number excluding food and energy. Recent PPI data saw large gains in energy related inflation, and hotter than expected CPI numbers as a consequence would not come as too much of shock. While the CPI tends to lag the PPI, there is a chance of fuel related costs to start appearing in this month’s data.

Medical related costs and inflation, components of the broader index which have been surging in recent months, will be monitored closely to see if the recent trend of rising prices continues. Expect some serious attention to shift towards this sector should the trend remain intact. Increasingly medical costs will act as a de-facto tax on American consumers going forward.

Greece casting a long shadow

While inflation data and expectations have been THE driving force behind markets over the past six to nine months, this month could ironically see the release take a back seat, overshadowed by the ongoing turmoil in Greece. Negotiations between Greece, the EU, and its creditors appear to be in deadlock, with the EU already preparing emergency measures and capital controls in anticipation of an imminent default. The contagion affect from Greece unknown, despite the market’s best efforts to reassure itself otherwise. An official Greek default would likely send a shock wave throughout the financial system.

In short, expect the upcoming meeting to reveal a more dovish tone from the Fed – market’s already have enough to contend with at the moment trying to contain the volatility from a potential Greek default without the Fed throwing fuel on the fire. On the inflation front, energy related costs are likely to see border inflation moving higher but there would need to be some drastic moves before the market could begin pricing in a September rate hike with any great conviction.

by Andrew | Jun 13, 2015 | In the news

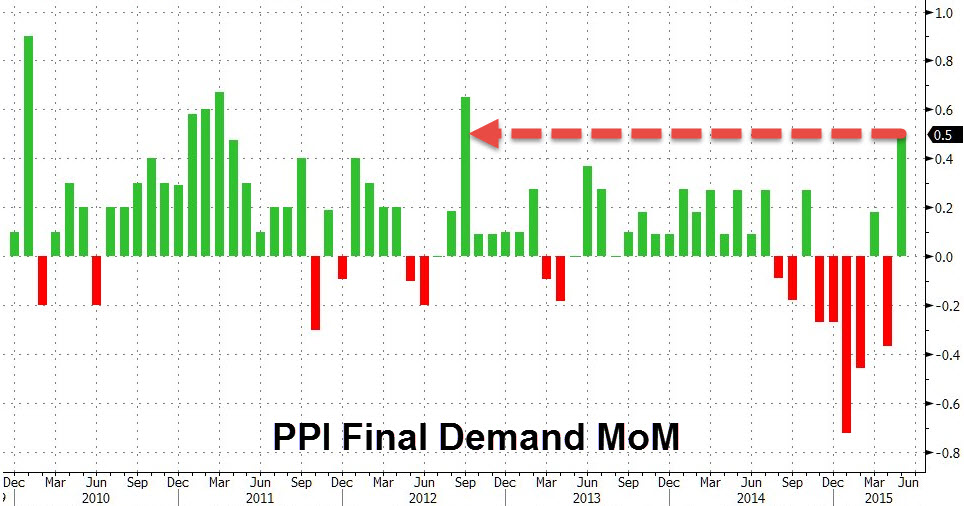

Stabilizing energy costs in May helped drive the producer price index of final demand higher by 0.5% MoM, the highest monthly gain in almost three years. Price increases were a direct result of surging gasoline prices, a significant input cost for business, which registered a 17% monthly increase. Rising gas prices accounted for 60% of total price increases in the index. Signs that the energy market is finding broad based support at current prices should see similar related cost pressures reflected in the broader CPI figures for the coming months ahead. May CPI is scheduled for release Friday 20th May.

Alongside energy, food costs also registered solid gains in the month of May, with prices rising 0.8% MoM, the first rise following 5 months of straight declines. Food prices were affected by a sharp increase in the price of wholesale eggs, which gained 56.4% last month following the outbreak of Avian Flu. The disease has caused the culling of millions of chickens worldwide and led to a severe shortage in egg supply.

While the May PPI figures will be welcomed by many as a sign that the severe deflationary trends present within the economy are starting to subside, the overall trend continues to trend downwards, with year over year figures showing a -1.3% drop in prices since April 2014.

Consumer Confidence Highest since 2007

Complementing this week’s strong PPI numbers was a resurgent University of Michigan consumer confidence report. The consumer sentiment index rose to 94.6 from 90.7 in May, the best reading on consumer sentiment since 2007. Tightening labor market conditions were widely cited as the catalyst for growing optimism, as workers anticipated higher wages in the months ahead. Improved confidence is also represented by strong retail sales numbers across the board despite higher gasoline prices during the month. Retail sales increased 1.2% in May, beating analysts’ forecast of sales growing at a pace of 1.1%. There were also notable revisions for the March and April numbers. April retail sales were revised upward 0.2% and March’s numbers were also revised to 1.5% from 1.1%. The improved retail numbers in recent months will be a welcomed trend amongst the Fed in particular, who are desperate for signs of increased activity in the sector.

Growth Outlook

Recent data points suggest the second half of 2015 could see an overall improvement in growth, following a highly disappointing start to the year. While recent PPI and CPI data have highlighted potential inflationary forces in play via stabilizing energy prices, the overall deflationary trends remain, and will still be the main cause of concern at the Federal Reserve. On face value the US economy seems to be on strong footing, but there are several undercurrents at the moment which will likely breed caution in policy makers with regard to future rate hikes. Greece continues to dominate the headlines, with the threat of a potential default looming large over markets. While the market, most notably the equity markets, appear to have priced in any potential contagion effect from Greece, it remains to be seen if the financial sector is resilient enough to absorb such a credit event from a European sovereign. Continued gyrations in the currency markets are also likely to generate a sever headwind for corporate profits in the growth coming quarters, and will also lead to more timid growth.

Overall, the growth outlook remains finely balanced – the best case scenario sees a more resilient consumer taking center stage of the economy which would likely be reflected in an improving employment picture going forward. The bear case still points to tepid wage growth, and several geopolitical and external economic events which are likely to push back the recovery.

Fed Watch

May CPI numbers will be released by the Labor Department on Thursday 8th June with the market widely expecting a modest continuation of the monthly upward trends. As noted previously, particular attention for signs of any moderation in medical related inflation which has been running hot throughout 2015 and could become a potential drag on the consumer going forward. Ongoing events in Greece may diminish the market effect of the upcoming CPI release, but there will be significant attention paid to any outliers in the data, to glean further insight into the direction of the Fed.

by Andrew | Jun 5, 2015 | Inflation

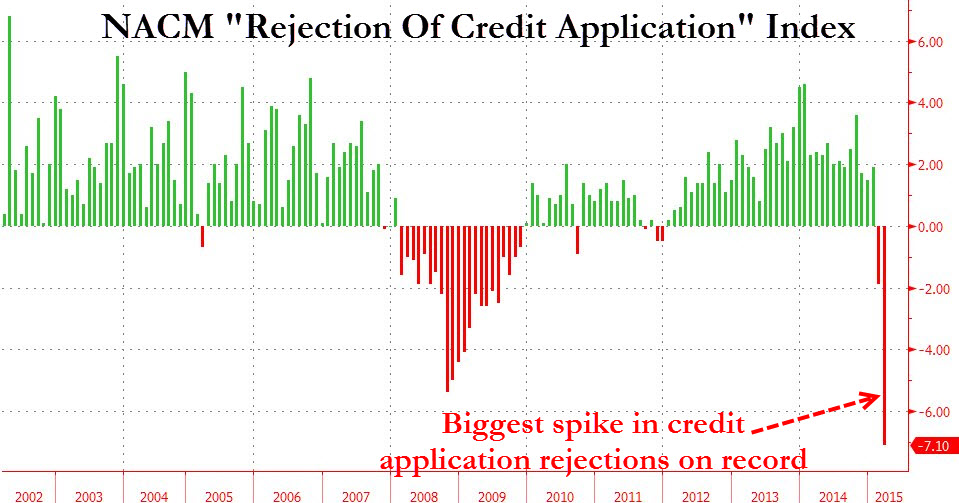

One of the more interesting sets of data to catch our attention in recent months is the National Association of Credit Managers CMI Index – a broad measure of the underlying credit conditions affecting both the manufacturing and service sectors in the US economy. The CMI has proved to be a valuable leading indicator since its inception in 2002, successfully predicting both the start and the end of the credit crisis in 2007 and 2009 respectively.

Given the important role credit plays in the overall economy, following a gauge of credit conditions on a month to month basis provides an excellent insight into just how healthy the flow of credit is throughout the business sector. From this vantage point, the trend emerging from recent data is worrying on all fronts and could have serious ramifications for the economy in remaining quarters of 2015.

Full Blown Recessionary Signal in March (or is it… )

In March, the CMI data recorded the biggest deterioration of business credit conditions in over 7 years. The fall in the unfavorable factors part of the index, tumbled from 50.5 to 48.5 – the lowest level since the 2008 recession formally ended. The data turned the heads of many analysts due to the severity of the drop. In the NACM’s own words:

“There is quite obviously some serious financial stress manifesting in the data and this does not bode well for the growth of the economy going forward. These readings are as low as they have been since the recession started and to see everything start to get back on track would take a substantial reversal at this stage. The data from the CMI is not the only place where this distress is showing up, but thus far, it may be the most profound”

Thankfully, if not somewhat surprisingly, the NACM made significant revisions to the March data in its April release – with the sharp falls in February and March replaced with less apocalyptic data points. The massive declines in February and March were revised from 52.1 and 46.1 respectively to 60.5 and 60.6, quite an enormous revision, and one which the NACM were rather vague in explaining. Again, in their own words:

“In February and March the CMI seemed to show a drastic drop in the amount of credit extended by companies to those that wanted to buy their machines or commodities and inventory. There was also a big drop in the number of credit applications submitted. Many of the other categories were also in decline, but these were the most dramatic. Upon reviewing the data and assessing some of the additional numbers it seems that there was not quite the drama originally noted.”

So.. credit crunch avoided, but the data has stoked our curiosity about what exactly did occur in February and March. If credit conditions deteriorated so badly during this period, the trend should surely be mirrored in the consumer credit data – we cracked open the Fed’s latest Consumer Credit report to take a look.

Consumer Revolving Credit Slowdown

While the Fed’s consumer credit lags the NACM (the Fed only has data up until March, the NACM CMI is current through the month of April) the data nevertheless appears to confirm the initial view from the CMI – a significant deterioration in credit availability did occur in the first quarter of 2015. From the Fed’s data, revolving credit fell -3.3% in both January and February of this year before rebounding +5.9% in March, signalling a severe slowdown in credit creation in the early part of the first quarter from non government sources. This was the worst month for revolving credit (predominantly credit cards) since December 2010 and paints a worrying picture regarding the health of the US consumer going forward.

Compounding the sluggish consumer, there also seems to be credit aversion occurring throughout the big banks, with the Fed’s data showing outstanding consumer credit held at depository institutions down -2.5% from the fourth Q4 2014 to March 2015. It would appear from this data that the big banks have pulled their horns in with respect to extending credit to both businesses and consumers in the first three months of 2015 as uncertainty reigns supreme with regards to the timing of the Fed’s next rate hike.

Both data sets have certainly caught our interest and we will be monitoring the Fed’s latest credit report scheduled for release on June 7 for signs of how the current trend is progressing. In the meantime, the data clearly shows the economy is in far less robust health than those calling for a rate hike would care to imagine. The recent fall in global PMIs and factory orders in the US are further signs of a slowdown occurring – we have been calling for an extended period of delayed rate hikes for a while, but this current data seals it.

by Andrew | Jun 1, 2015 | Definitions

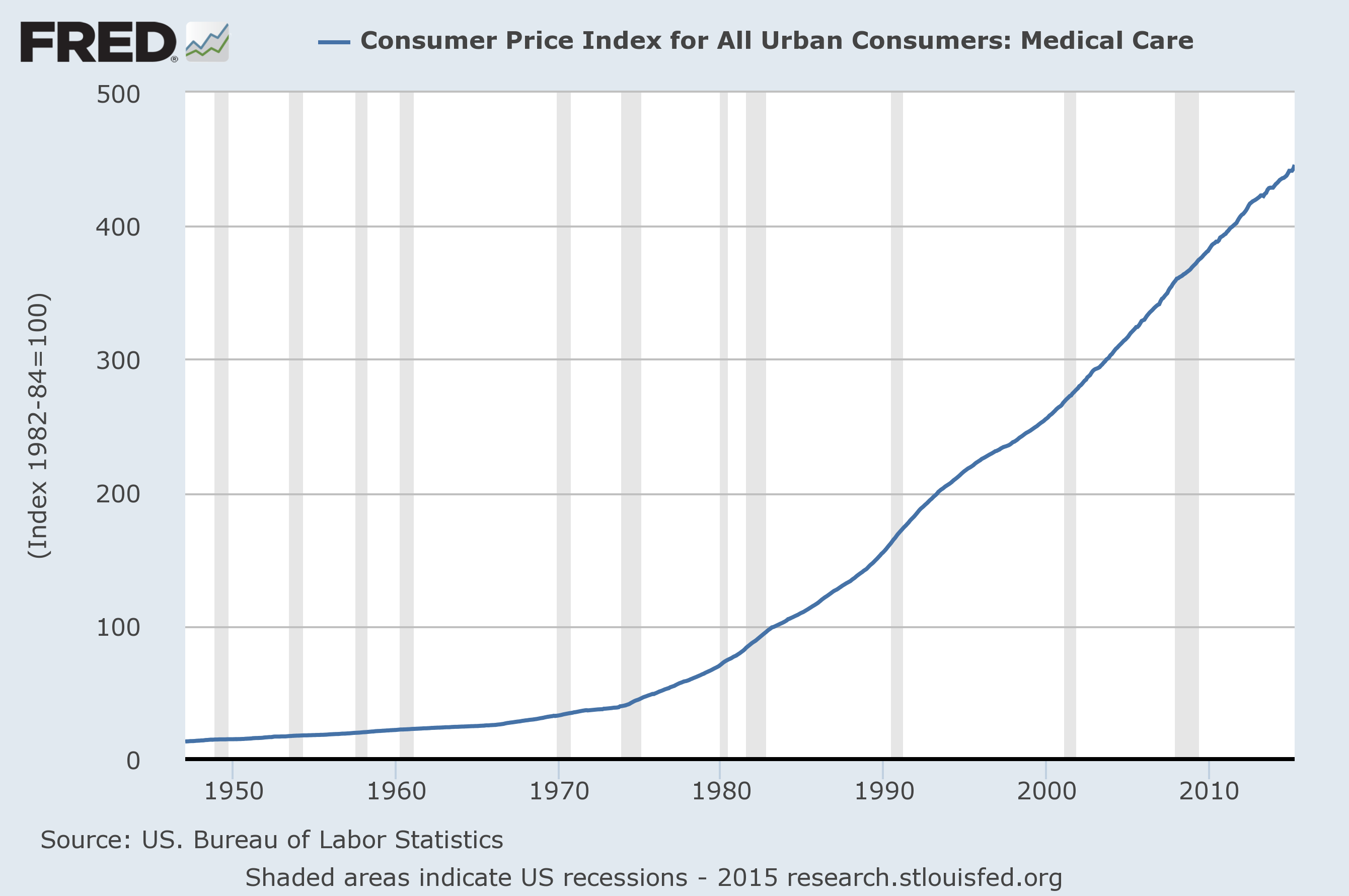

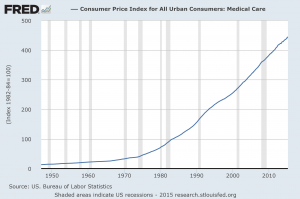

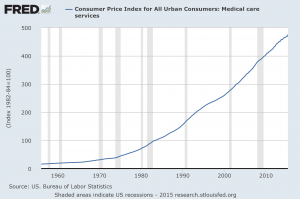

Surging medical costs and services were the most worrying trends to arise from the April CPI release, with costs rising at the fastest pace since January 2008. A 0.7% increase in the Medical Care Index was the largest contributor to headline CPI, and the dramatic increase has left many inflation commentators baffled with regards to the cause. A rise of this magnitude was not anticipated, and there appears to be no clear cut explanation for the sudden spike.

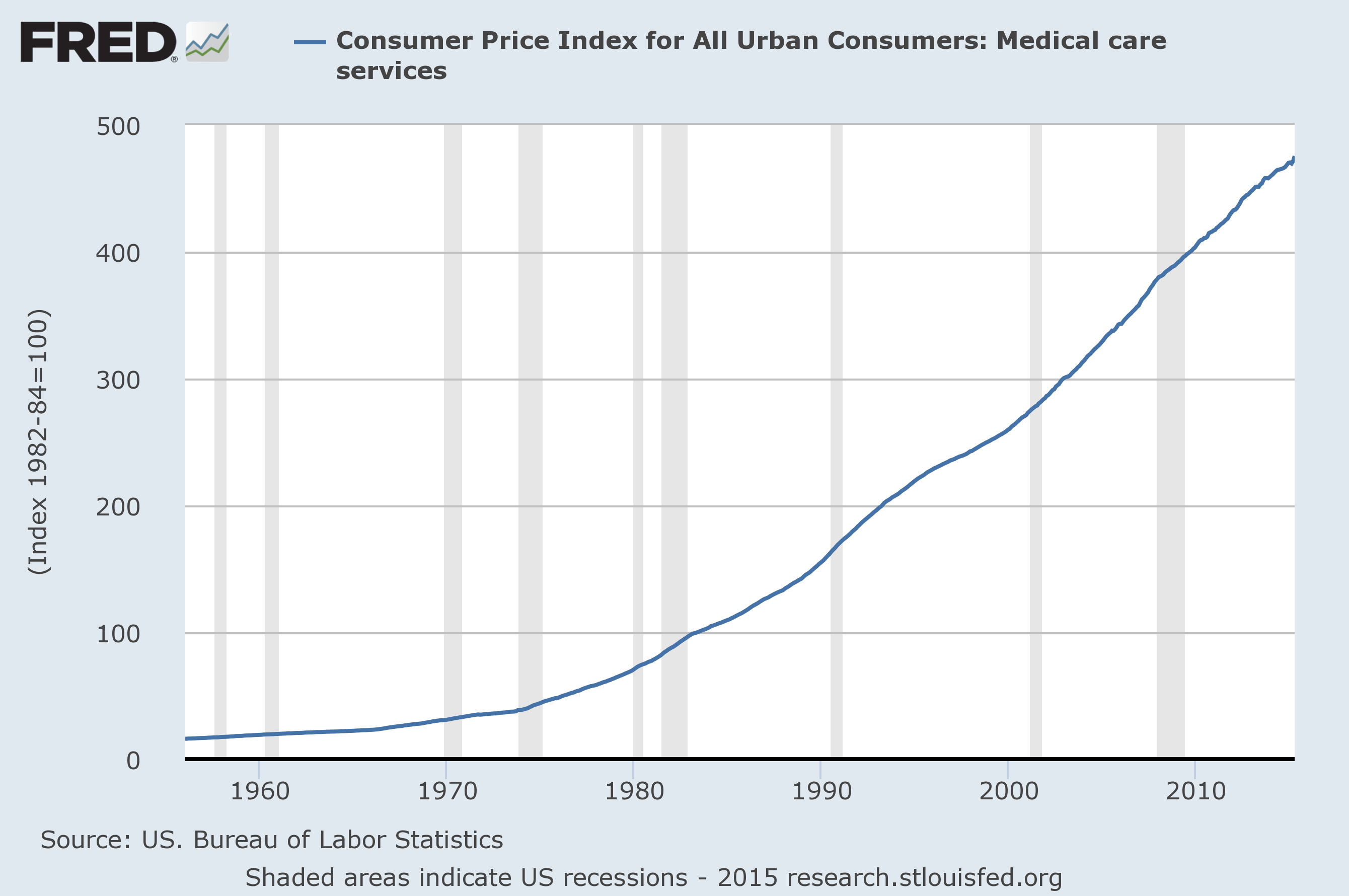

All medical related costs rose sharply, with Medical Care Commodities and Medical Care Services indices rising 4.1% and 2.6% on an annualized basis. Medical care services form the largest component of the medical care index which includes the prices of health insurance and professional services. The BLS also reported the cost of Hospital services rose 1.9 percent for the period. In summary, health related costs rose across every meaningful sector and will be of concern to policy makers going forward should such trends persist.

The uptick in April’s prices will come as a particular blow to working Americans who already shell out on the most expensive healthcare in the world. The distinct possibility of rising healthcare insurance premiums to reflect increased costs could compound the situation even further. While currently operating well below radar, ongoing health care inflation has the potential to provide a further drag on disposable income and the sustainability of the current recovery. While the warning signs are perhaps counterintuitive given the wider deflation trends within the economy, the official deflation mantra will be scant consolation to the average American feeling the burden of ever increasing real healthcare costs.

Why is Medical Inflation on the Rise?

The precise reason for the uptick in medical inflation this month is hard to pinpoint with any great certainty, but there are clear underlying trends in the industry which point to sustained price increases in 2015 and beyond. These trends suggest rising medical inflation is likely to be a long term phenomenon, and not the statistical blip it is currently being viewed as by most of the analyst community.

According to a recent report by PWC’s Health Research Institute, overall healthcare spending growth is likely to increase by 4.8% in 2015 as a result of an improving economy, increased number of speciality drugs, increased Physician employment, and structural IT integration issues. A recent report from a rival consulting firm Milliman projected even further increases, estimating a 6.3 percent growth in the costs of health care for a typical family of four on an employer-based plan in 2015.

PWC identifies the improving economy as one of the biggest catalysts for health care spending and costs going forward. The report argues that Improving consumer confidence is likely to increase medical appointments for those requiring treatment. It has been argued that the 2008 recession had caused cautious workers to delay doctor visits until their financial situation improved. As confidence improves throughout the broader healthcare sector, specialized drugs are likely to exert further pressure on costs. While roughly 4% of patients are currently prescribed speciality drugs, these drugs account for nearly 25% of the total drug spending in the United States. New treatments for Hepatitis C in particular are attracting a great deal of attention, with spending on these drugs alone forecasted to increase 209% by the end of 2015.

Timid healthcare costs have been taken for granted over the past few years, but the market could be in for a rude awakening should the current trend in health care costs persist throughout the next several months.

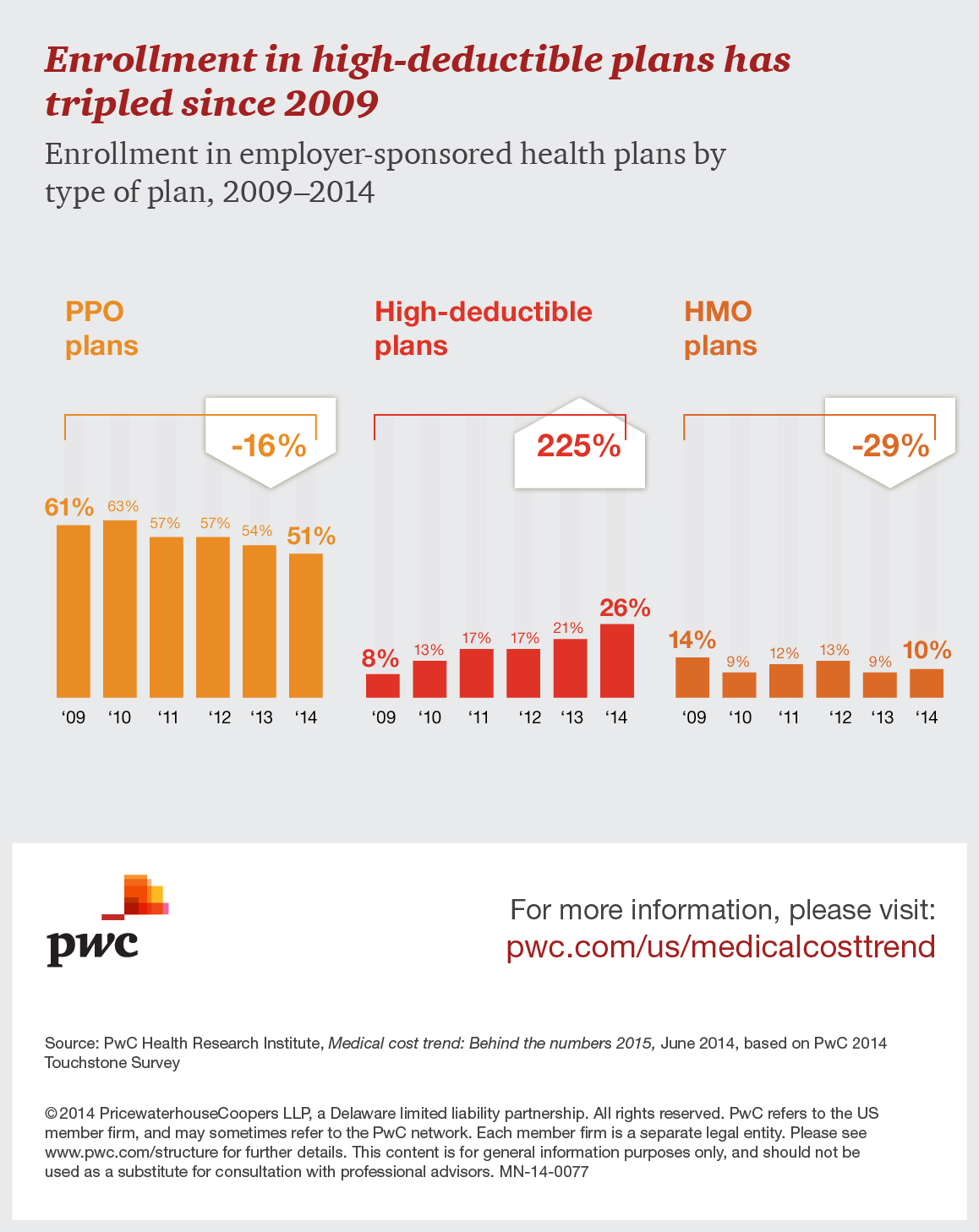

Are we headed for double digit rises in health care costs?

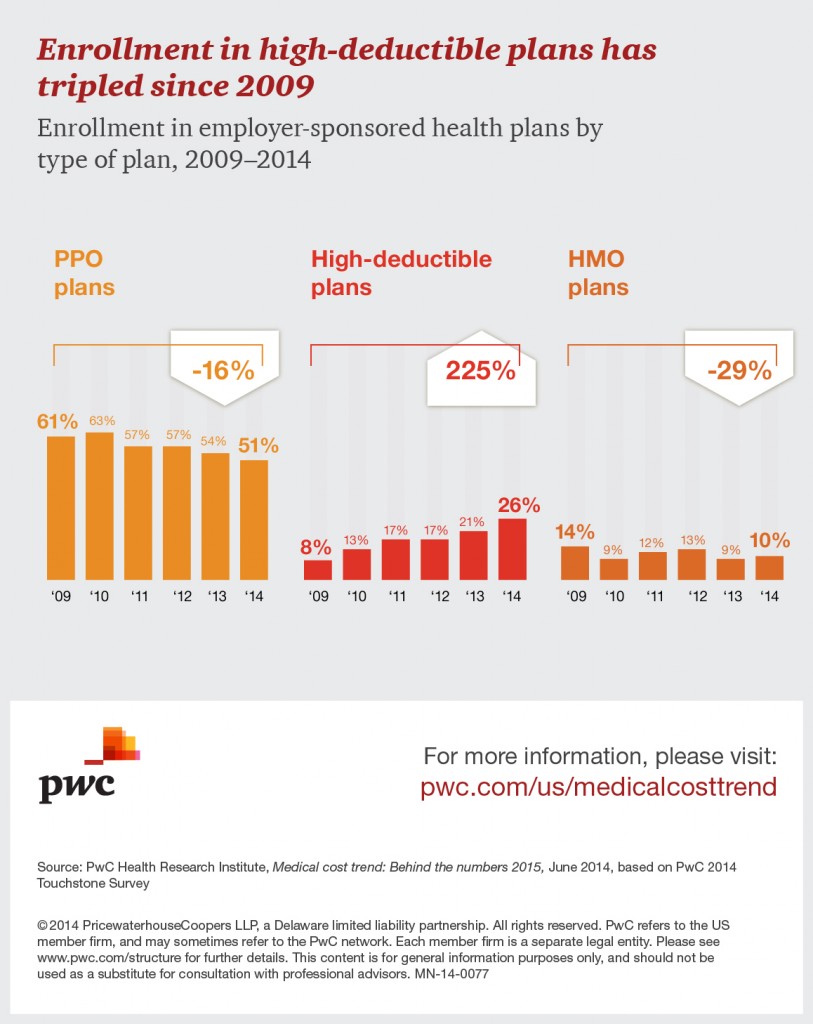

Prior to the recession in 2008, double digit health care costs were common, and as a consequence, employers started to shift an increasing amount of the financial burden directly onto their employees through the adoption of high deductible healthcare plans. Today, 44% of employers are considering such plans as the only option for employee medical benefits, with the trend only likely to accelerate in the coming years.

What this means for individual workers is obvious. Health care costs as a percentage of income are going to rise, and could do so with vigor if pre Lehman inflation rates are a guide. While the market continues to digest the implications of the stubborn deflation prevalent within the economy, working Americans face a very different prospect of keeping up payments on healthcare – yet another component of everyday life which is becoming less and less affordable for the average worker.

The specter of rising inflation in the healthcare sector is ominous for the broader market. If prices continue to rise above trend in the subsequent months, we could be looking at the real possibility of health care induced stagflation beginning to take hold throughout the economy.

by Andrew | May 26, 2015 | Definitions

Employment Data

The most recent employment data is a significant reason to be cheerful for the Fed. Taken at face value, initial claims for the week ended May 9 unexpectedly fell to 264,000, the lowest level in over 15 years. The improving employment figures are increasingly heralded as evidence of the broader economic recovery occurring within the US economy, and the stable employment conditions do fulfill one half of the equation for the Fed to begin normalizing interest rates. The problem facing the Fed now turns to the stubborn deflationary headwinds which have been brewing since the start of the oil market rout late last year. April CPI data due out this week is likely to remain subdued, and despite the sell off in the bond market over the past few weeks, a rate hike from the Fed continues to look unlikely at their upcoming June meeting. Besides the deflationary forces operating within the economy, the Fed is also likely to take recent employment data with a healthy dose of caution given the fragile nature of the shale gas sector.

Shale Gas Sector Layoffs

Recent estimates suggest up to 75,000 jobs have been lost in the United States as a result of plummeting oil prices worldwide. The extent of the layoffs are likely to be of a much higher magnitude once the ripple effects of such a key component within the economic recovery are felt on an aggregate level. The extensive downsizing signals a flip-flop in employment dynamics, with the industry up until recently being one of the major forces of job creation throughout the United States. The contraction of employment within the shale industry will certainly take the gloss off of the recent employment figures for the Fed. Shale energy jobs tend to be well paid middle class jobs – and although the industry is cyclical in nature, regional economies will be bracing themselves against the implications of a downside of this magnitude.

The contraction of employment within the shale industry will certainly take the gloss off of the recent employment figures for the Fed. Shale energy jobs tend to be well paid middle class jobs – and although the industry is cyclical in nature, regional economies will be bracing themselves against the implications of a downside of this magnitude.

Retail Sales and Consumer confidence remain sluggish

Another economic indicator which is likely to be giving the Fed some concern going forward, is the sluggish retail sales data which is starting to show a definitive trend of consumer belt tightening this year. Despite the dramatic falls in energy and gasoline prices, and rising employment prospects, consumers have been unwilling as of yet to demonstrate any form of meaningful conviction in the economy’s prospects going forward at the shopping tills. Retail sales flatlined in April after having risen 1.1 percent in March. Overall retail activity has risen just 0.9 percent over the past year – well below longer term trend growth. It would appear high levels of consumer and private debt along with muted wage growth are instilling an increased degree of frugality in the average US consumer. This has the potential to become a deepening trend in the months ahead should rebounding gasoline prices impact consumer confidence and retail sales further. While the US economy has shown relative resilience to energy based deflationary pressures, its unclear if it would fare so well against a broader fall in consumer led spending and demand.

Retail sales flatlined in April after having risen 1.1 percent in March. Overall retail activity has risen just 0.9 percent over the past year – well below longer term trend growth. It would appear high levels of consumer and private debt along with muted wage growth are instilling an increased degree of frugality in the average US consumer. This has the potential to become a deepening trend in the months ahead should rebounding gasoline prices impact consumer confidence and retail sales further. While the US economy has shown relative resilience to energy based deflationary pressures, its unclear if it would fare so well against a broader fall in consumer led spending and demand.

What to watch out for this week

This week is heavy in terms of news flow, with minutes from the Fed’s april meeting and CPI data due out by the end of the week. Janet Yellen’s commentary this coming Friday will also be a key driver for risk. Consensus expectations are calling for broader April CPI falling -0.2% YoY, and CPI ex Food and Energy rising 1.7%. The market will be tracking the impact of crude oil and gasoline prices closely. Any surprise to the upside on the CPI data should compound the recent sell off in treasuries. If the latest producer price index is anything to go by, the markets needn’t fear too much. Recent PPI data was tame, showing no signs of any resurgence in inflation due to the recent rebound in prices across the energy complex, CPI is likely to show a similar trend and increase the case for the Fed to keep rates on hold for the foreseeable future.